European leveraged finance markets look remarkably healthy as we enter 2022. This may come as a surprise, after 12 months of economic volatility underpinned by everything from a new COVID-19 variant to growing inflationary pressures. What does this mean for the months ahead?

The start of the new year is full of positives in the European leveraged finance market. There has been a clear shift from survival to growth strategies among lenders and borrowers, setting the stage for significant activity in almost all sectors.

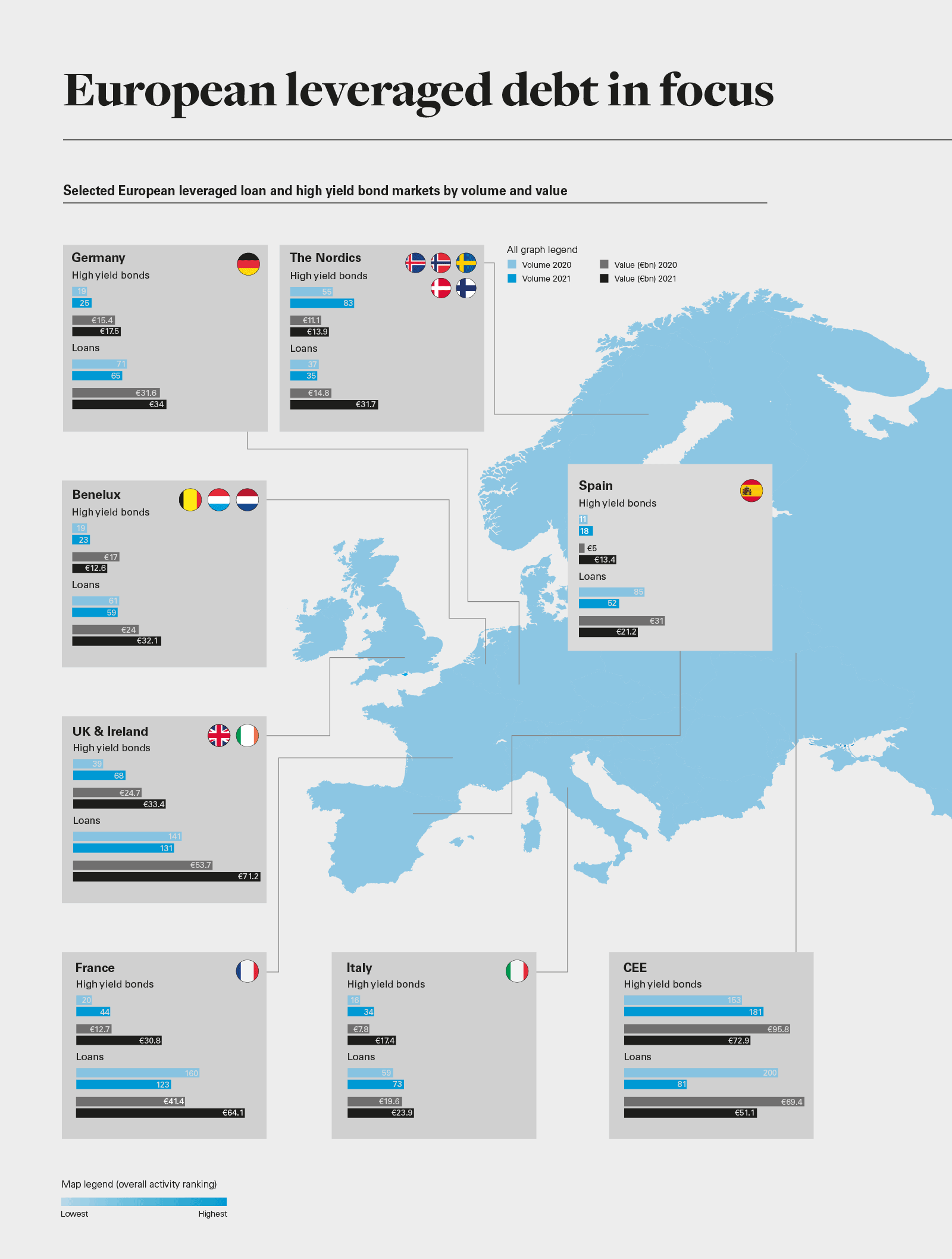

The numbers paint a clear picture. European leveraged loan issuance climbed more than 25% in 2021, year-on-year. High yield bond markets in the region were even more enthusiastic, with issuance for the year up 47% on 2020's total.

Ongoing government support in the EU and the UK helped companies that might otherwise have fallen victim to the pandemic stay afloat. Low interest rates and pricing sparked a wave of refinancing. CLO activity—most of which was intended for refinancing and resets—pushed new CLO issuance up by 75% year-on-year.

A bottleneck of demand as well as significant private equity dry powder also brought a flood of new deal money into the market. Companies that were once hesitant to sell encountered enthusiastic buyers aggressively looking for targets. Buyers, meanwhile, found themselves in a better position to judge whether a potential target was likely to struggle or grow in 2022 and beyond. Lenders reaped the benefits, with high deal volume in which to participate. At the same time, unlike many other industries, European direct lending funds avoided any significant downturn in deployment and deal activity due to COVID-19. According to data from Debtwire Par, direct lending issuance in the region reached €36.2 billion in 2021, surpassing 2020's full-year total of €21.4 billion. This provided a liquid and competitive market for finance products.

Possibilities and pitfalls

Set against this positive backdrop, does the future look entirely bright for leveraged finance? Not necessarily—some challenges remain, and each may have an impact on European issuance.

For example, climbing COVID-19 case numbers driven by the Omicron variant may convince some corporates to hold on to their reserves. Any resulting new lockdowns or restrictions could also be the final straw for businesses that have already struggled during the pandemic.

Inflation and attendant interest rate rises are also likely to influence potential borrowing decisions in the coming months. The UK got the ball rolling with its first interest rate rise in three years in December 2021, and the EU may follow suit in 2022—despite claims to the contrary by the European Central Bank.

Any rise in the cost of debt will affect M&A and buyout activity, as well as financing. Some may pause while others—from corporates in good financial shape to PE firms with money to spend—may decide to invest in a post-COVID-19 future. Either way, M&A and buyout deals in the pipeline already suggest that issuance will remain healthy in the first half of the year at least.

And, finally, environmental, social and corporate governance criteria will be on the menu for every European business. New benchmarks due in 2022—from the EU's Sustainable Finance Disclosure Regulation to the European Leveraged Finance Association's updated Sustainability Linked Loan Principles—are already making lenders and borrowers sit up and take notice.

All this activity means the stage is set for companies hoping to thrive rather than simply survive. Lenders chasing higher-yield opportunities will be on the hunt for new investments, and borrowers can be expected to provide lenders with a healthy volume of demand for debt financing in 2022.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)