US dealmaking robust despite COVID-19

US M&A activity fell precipitously in the first half of the year but picked up again in H2, especially at the upper end of the market

After the initial shock of the pandemic, M&A activity rebounded significantly in H2. Nevertheless, challenges remain—despite low interest rates and strong stock prices

The past year has been an exceptionally challenging one for societies and economies globally, and many companies were hit hard by COVID-19 lockdowns and travel restrictions.

The huge uncertainty that gripped capital markets early in the pandemic put equities into sharp decline and dealmaking largely on hold as strategic buyers and private equity (PE) firms turned inwards to support existing portfolios. The challenges posed by remote due diligence and uncertainty around valuations provided further reasons for market participants to hold back from transacting.

After this initial period of disruption, however, deal activity rebounded strongly, with total value in H2 significantly higher than the same period in 2019. Buyers assessed COVID-19 business risks, PE owners provided portfolio companies with the necessary support where required and proceeded to look outwards for opportunities to improve companies through acquisitions.

Low interest rates and extensive government support for the economy have helped to revive deal activity. Resilient companies in industries that fared relatively well through lockdowns—such as TMT, food and beverage, and healthcare—have been able to take advantage of high levels of cash and strong stock prices to execute acquisitions.

The rise in deal activity in the second half obscures a bifurcated market, however. Even as activity at the top end of the market exceeded pre-pandemic levels, M&A in the middle-market remained muted, likely due to greater uncertainty around valuations.

Our overall outlook for the next 12 months is cautiously optimistic. A series of successful clinical trials have led to vaccine rollouts, providing a major boost to close the year. And stock markets have looked beyond the pandemic to crest new highs.

A more stable outlook could spark a resurgence of middle-market deals, as well as continue to encourage deal activity among larger firms.

After a difficult period, there is reason for optimism that conditions in 2021 will support the momentum in M&A markets that started to build in the final quarter of 2020.

US M&A activity fell precipitously in the first half of the year but picked up again in H2, especially at the upper end of the market

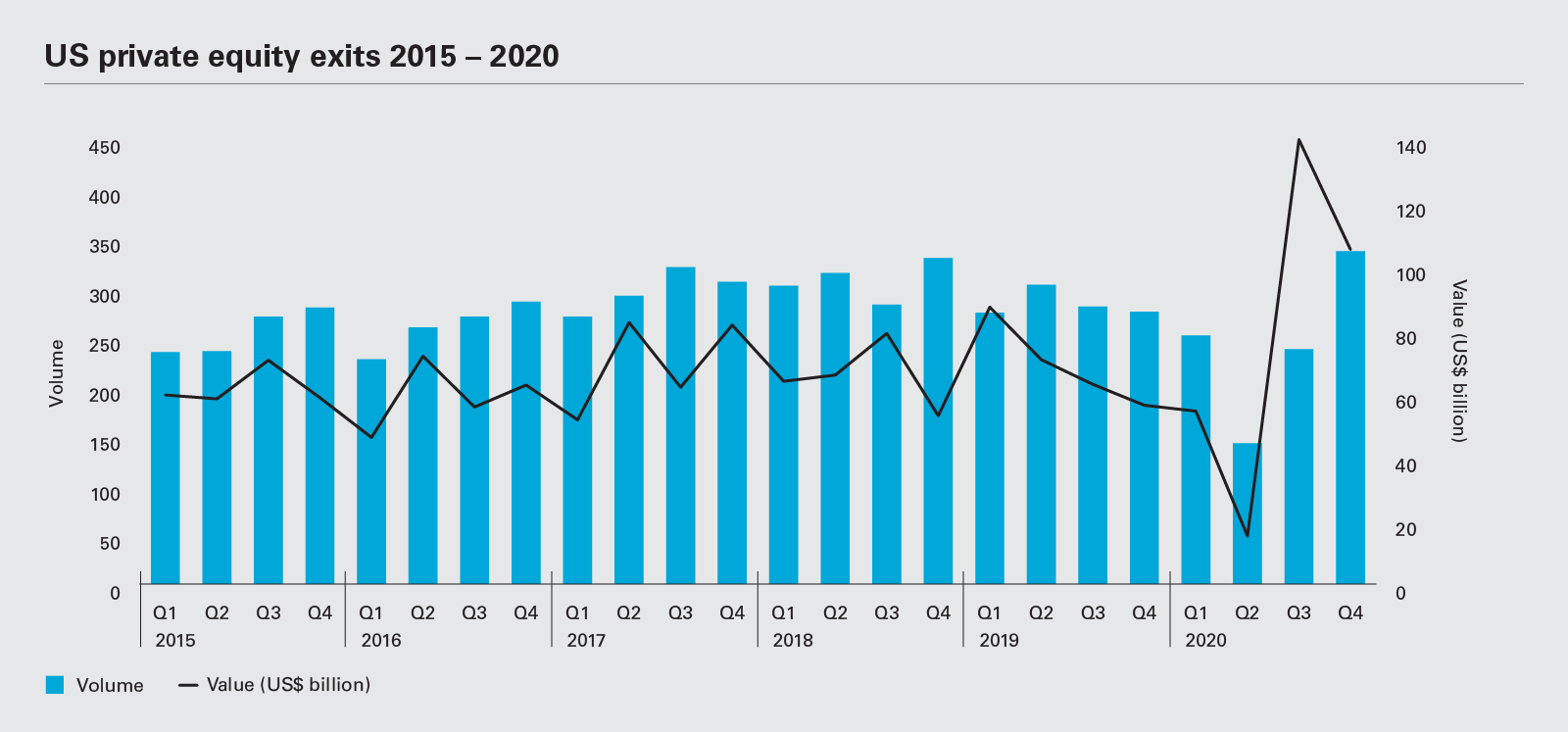

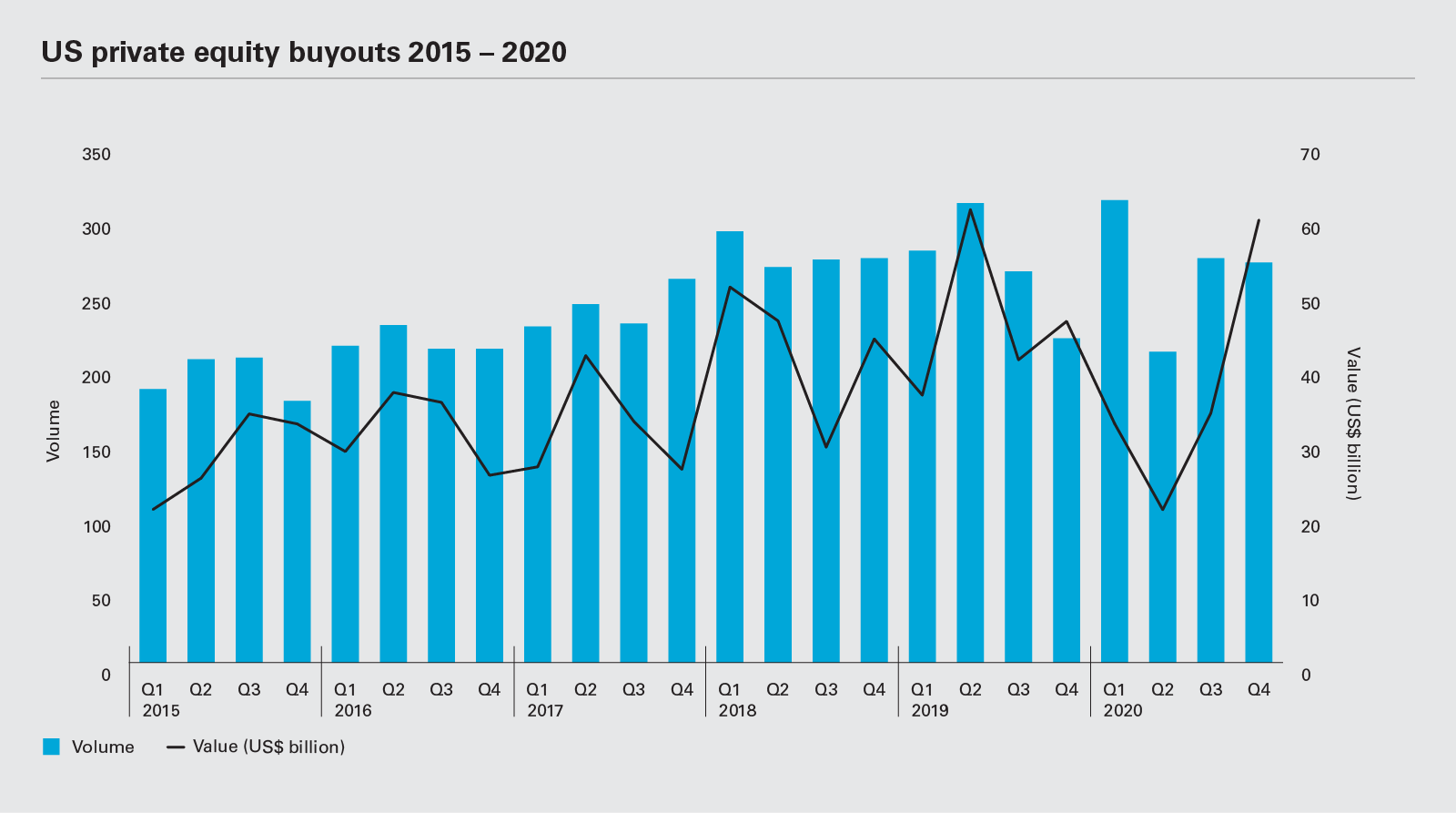

US buyout activity at the top end of the market dropped significantly but exit value held up in 2020

The TMT sector was buoyed by global spikes in demand as the world shifted toward virtual interactions in every walk of life

Deal activity in the oil & gas sector was severely impacted by the COVID-19 pandemic, as commodities prices plummeted

Businesses and consumers have relied on technology more than ever through the course of the pandemic, supporting strong dealmaking at the top end of the market

M&A value in the healthcare sector (incorporating pharma, medical and biotech) stayed relatively robust in 2020, even without the kind of blockbuster deals the sector had become accustomed to seeing in recent years

Total M&A value in the consumer sector has dropped only 1 percent year-on-year thanks to several significant transactions in the food industry.

Real estate portfolios exposed to hospitality and retail assets have struggled through COVID-19 lockdown periods, but healthcare and logistics investments have performed strongly

2020 saw several decisions from the Delaware courts that will affect M&A dealmaking. We focus on four that may prove especially consequential

The past year has been tumultuous for M&A activity, but with a COVID-19 vaccine rollout underway and pent-up demand among PE firms, the fundamentals are in place for a busy year in 2021

US buyout activity at the top end of the market dropped significantly but exit value held up in 2020

Stay current on global M&A activity

Explore the data

Despite volatile valuations, travel restrictions and difficult trading conditions for portfolio companies, PE figures held up relatively well. There were 2,027 PE-related deals (including both exits and buyouts) worth US$459.8 billion in 2020. Although this represents an 8 percent year-onyear drop in volume, value remained steady and the overall declines for M&A were much bigger.

Moreover, the full-year figures mask PE’s strong performance in the second half of 2020. Total value of PE-related deals in H2 came to US$337.7 billion—a 177 percent increase compared to the first six months of the year, and an impressive 64 percent rise on H2 2019.

US $337.7 billion

The value of US PE-related deals in H2 2020—a 64 percent increase compared to the same period in 2019

Much of this heightened activity was due to large exit transactions. Of the top-ten largest PE-related transactions in 2020, eight were exits. In contrast, in 2019, only four of the top-ten PE deals were exits.

Exit value totaled US$244.6 billion in the second half of 2020, more than double the US$118.9 billion struck in the last six months of 2019. Volume over this period rose 3 percent to 573 deals.

Even including the tough first half, total exit value for the year as a whole reached US$314 billion, up 14 percent compared to 2019, although exit volume fell by 15 percent.

Buyout activity was more muted. There were 1,061 buyouts in 2020 as a whole, worth US$145.9 billion—a 1 percent drop in volume and a 21 percent drop in value compared to 2019. Total buyout value improved substantially in H2 compared to H1, however, rising 77 percent to US$93.1 billion, 7 percent higher than the figures for the second half of 2019.

Additionally, many of these buyouts were minority investments— the number of PE investments made in exchange for a stake of less than 50 percent rose 7 percent year-on-year to 532 deals in 2020. The total value of these deals came to US$99.4 billion, a 49 percent increase on the year before.

As businesses in certain sectors struggled in the face of the historic uncertainty unleashed by the COVID-19 pandemic, many turned to selling non-controlling stakes to raise cash—and the highly adaptable PE industry stepped up to provide capital at attractive valuation multiples.

TMT was far and away the largest sector for PE by both volume and value, with 769 deals worth US$217.6 billion

Technology, media and telecoms (TMT) was far and away the largest sector for PE by both volume and value, with 769 deals worth US$217.6 billion—unsurprisingly, given that the technology sector has emerged as the biggest beneficiary of the pandemic.

Exits in the TMT sector were especially robust, totaling US$160.2 billion, more than triple the US$48.2 billion across 2019.

This was due primarily to activity at the top end of the market, as volume remained steady at 449 deals.

Buyouts in the TMT sector, on the other hand, dropped 28 percent year-on-year, to US$57.4 billion. As with exits, volume held steady at 320 over the same period.

The second-largest sector by value was healthcare (incorporating pharma, medical and biotech), which recorded 267 deals worth US$60.1 billion—a 17 percent rise in volume and a 30 percent increase in value compared to 2019.

The largest PE deal of the year embodied several of the trends discussed above: The US$14.8 billion sale of Livongo Health to Teladoc was an exit for investors Kleiner Perkins, General Catalyst Partners and 7wire Ventures. Livongo Health sits at the intersection of technology and healthcare as a digital health platform.

With routine healthcare appointments canceled or postponed due to concerns about COVID-19, telehealth solutions have become more attractive to consumers, but the pandemic has accelerated digital adoption in other segments as well. InterContinental Exchange’s acquisition of mortgage technology provider Ellie Mae, for instance, is symptomatic of digital transformation in an industry that still heavily relies on manual processes.

The election of Joe Biden as president and the Democratic Party's control of both houses of Congress may lead to increases in corporate and capital gains tax rates, as well as stricter antitrust enforcement. But even if tax policy changes, it is unlikely to have a major impact on levels of PE activity. Taxation is rarely the primary motivator for a transaction and any changes to tax policy will be factored into valuations. And stricter antitrust enforcement may give sponsors a leg up in sale processes, although buy-and-build deals by their portfolio companies may face challenges.

As vaccines for COVID-19 are rolled out, enabling economies to reopen, PE firms may once again be more active on the buy-side. Greater stability and a better understanding of how companies are coping with the pandemic’s effects in 2021 will encourage greater activity, especially given the high level of capital at the industry's disposal—US$1.7 trillion in dry powder, according to data provider Preqin.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

US private equity exits 2015 – 2020

US private equity exits 2015 – 2020

US private equity buyouts 2015 – 2020 Volume

US private equity buyouts 2015 – 2020 Volume