Recent Trends in Aviation Finance and Leasing: Post-Pandemic Guidance For Operating Lessors and Financiers

17 min read

In addition to being a crucial time for aviation finance and leasing lawyers to navigate their clients through the numerous challenges which it presented, the onset and duration of the COVID-19 pandemic required lawyers to provide specific and important advice to clients on the legal and practical realities of either forbearing or enforcing under many existing transactions.

With the aviation industry now largely recovered from the pandemic (overall, IATA estimates that air traveller numbers will exceed pre-pandemic levels by next year (2024)), White & Case partners Justin Benson and Mark Moody, counsel David Wright and associates James Turner and Rishi Raheja discuss their collective experiences and valuable lessons reminded from the pandemic.

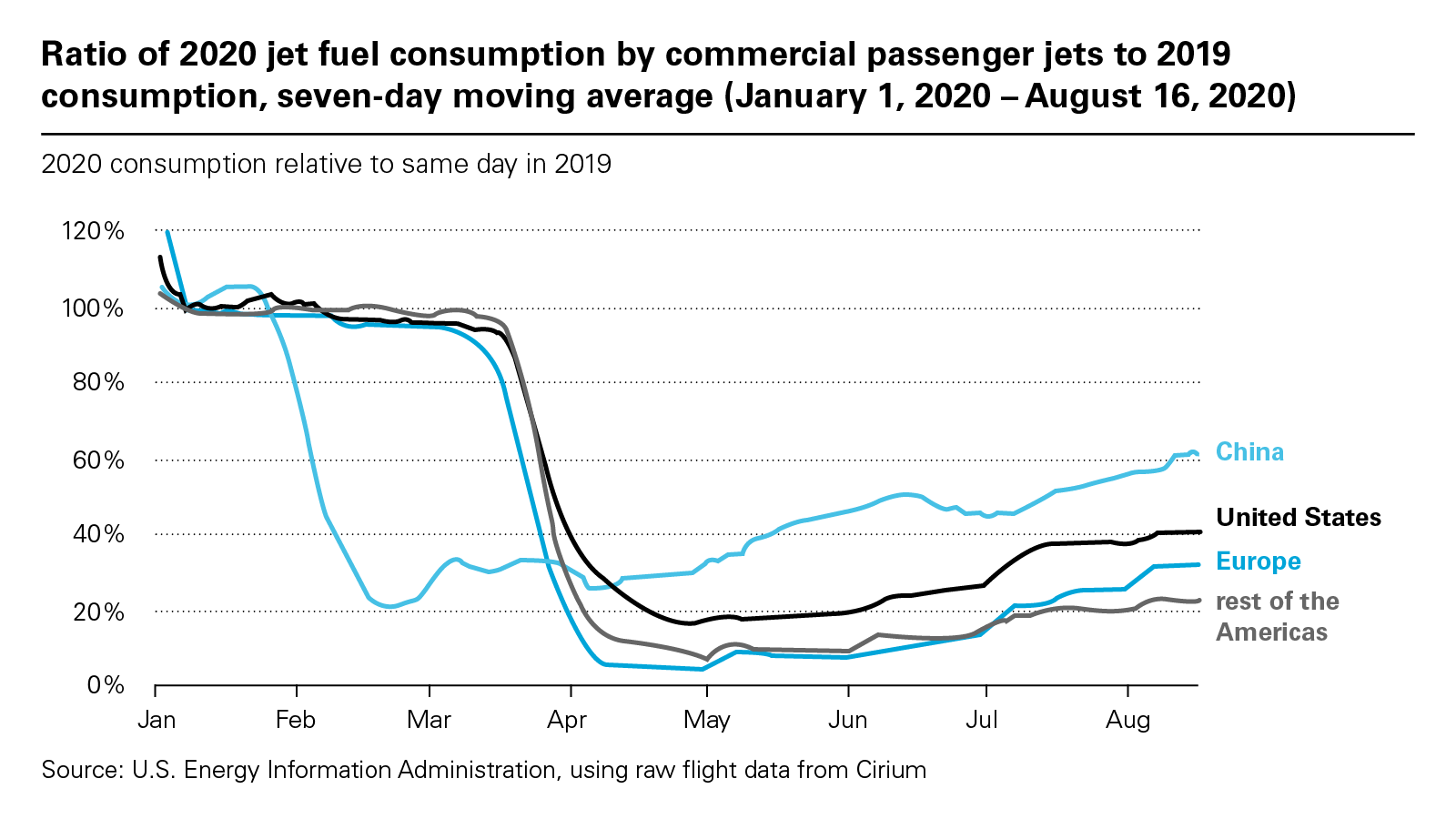

The announcement on 23 March 2020 of an immediate "stay at home" order by the UK government, trailed by similar measures adopted by governments of other countries affected earliest by the COVID-19 pandemic, including Italy and Spain. Similar moves followed by governments across the world, including notably for the aviation industry all except five states of the United States of America by 6 April 2020. It is estimated that by 28 April 2020, up to half of the world's population was subject to complete or partial lockdowns, representing almost 60% of global GDP.

In addition to restricting the movement of the majority of the global populace through containment measures, the first wave of global lockdowns was followed by travel restrictions, including requirements for proof of a negative COVID-19 test and, thereafter, proof of vaccination.

Of the industries hit hardest by the dual impact of lockdowns and travel restrictions, the aviation industry is clearly one of them. For participants in the aviation finance and leasing business, the combined impact of travel restrictions and lockdowns was a uniquely challenging time. In this article, we sum up our experience of the common responses to those challenges, the legal issues that arose and the common solutions.

Forbearance and deferrals

The impact of government lockdowns quickly required a commercial response by operating lessors and financiers alike. With the business model of many airlines being highly leveraged and cash-liquidity dependent (with limited cash reserves), reports from our clients of payment defaults soon manifested. Immediate reactions of terminating the leasing under an operating lease or accelerating the debt under a facility agreement were not, in most cases, readily viable options. A decision to terminate or accelerate would result in an operating lessor or financier seeking to recover an asset which was not readily remarketable at that time, and if other operating lessors and financiers were to do the same, the situation would exacerbate for all participants. Moreover, in many instances, aircraft could not physically be recovered due to travel restrictions.

"54% of estimated percentage of the global population were subject to full or partial lockdown measures by 28 April 2020"

At that time, we were aware of some initial attempts by airlines to argue or imply that the pandemic constituted a "force majeure" event which would prevent the airline from complying with its lease obligations. In our experience, and from an English law perspective, such arguments warranted a swift rebuttal by lessors and financiers. Not only would it be very unusual for an English law operating or finance lease to contain a force majeure clause, early cases during the pandemic such as Fibula Air v Just-US Air and Salam Air v Latam Airlines demonstrated the English courts would be reluctant to view the COVID-19 pandemic as something which prevents or frustrates a lessee in the performance of its obligation to pay money. From a lessor's perspective, it is precisely why the "hell or high water" clause is included, and the ACG v Olympic case had already given lessors (and financiers) the judicial backing needed to uphold and refer to that clause in negotiations.

"a dry aircraft lease is a challenging context to establish frustration" Salam Air v Latam Airlines

Consistent with this, the typical solution we saw was not for rent to be avoided, but for a portion of rent to be deferred, and whereby after a deferral period, rent payments were increased for the remainder of the lease term. This was sometimes coupled with a "power by the hour" arrangement where, during the deferral period, rent was payable based on an hourly rate of usage of the aircraft, if the aircraft was flown at all. For financing transactions, principal repayments were typically deferred by increasing future principal repayments, provided that interest on all outstanding principal continued to be paid during the deferral period.

It should be noted that in the post-pandemic environment, prior rent deferral arrangements can still be a relevant consideration. For example, when an aircraft is being sold or refinanced, it is an appropriate question to ask the parties involved whether the portion of future rent representing deferred rent attributable to the deferral period, and whether any "spring back" of the deferred rent in the case of a lease event of default should form part of the new lessor's post novation rights or (as the case may be) the financier's collateral.

"a discharge from any debt or liability under the bankruptcy law of a foreign country outside the United Kingdom is a discharge therefrom in England if, and only if, it is a discharge under the law applicable to the contract" Antony Gibbs & Sons v La Société Industrielle et Commerciele des Métaux

Secondary debt trading

Deferral arrangements were not a suitable solution for all airlines nor for all scenarios. In particular, circumstances encountered by some airlines were such that even with short term deferral arrangements or loan term extensions, one of the following outcomes would be true:

- Category 1: the airline would not emerge from the pandemic as a going concern; or

- Category 2: the airline would emerge from the pandemic after some form of bankruptcy proceedings with an altered fleet composition.

It is perhaps testament to the robustness of the aviation industry and the measures adopted by the industry that not many airlines actually fall into the first category.

For those airlines falling into the second category, we saw an uptick in the secondary debt trading of loans involving those airlines. It was not unusual to see commercial lenders and financial institutions deciding to exit transactions (below par) rather than (1) pursue enforcement action (with or without consensus of other lenders required to form an instructing group) or (2) await the outcome of applicable bankruptcy proceedings. This scenario (with one exception mentioned below) was also a reminder of the importance of ensuring, from a lender's perspective, that qualifying lender and other restrictions on loan transfers and assignments are disapplied when an event of default or enforcement event has occurred, to ensure the lender has maximum flexibility to reduce its exposure in a default scenario.

"a discharge from any debt or liability under the bankruptcy law of a foreign country outside the United Kingdom is a discharge therefrom in England if, and only if, it is a discharge under the law applicable to the contract" Antony Gibbs & Sons v La Société Industrielle et Commerciele des Métaux

The exception was any financings involving export credit agency (ECA) support, where in our experience lenders were able (as expected) to claim under their ECA support arrangements and remained as lenders of record.

Bankruptcy overlay

As intimated above, when an airline underwent local bankruptcy proceedings during the pandemic period, consideration had to be given to the legal impact and potential outcome of those proceedings.

In the wake of the pandemic, it is well known that a number of airlines filed (for example) for Chapter 11 bankruptcy protection in the United States. One impact of this was that any action by financiers or lessors to terminate the leasing of the aircraft under a finance lease or operating lease could result in the financier or lessor violating the "stay" (or moratorium) under the Chapter 11 proceedings. Typically, the bankruptcy stay also prevented the original (or existing) financiers from being able to accelerate the debt in defaulting transactions, because the acceleration of the debt would often automatically trigger the termination of the leasing and thereby (indirectly) a violation of the bankruptcy stay (this no doubt being something which hastened decisions by commercial lenders to exit through the secondary debt market).

In our experience, the combination of the bankruptcy overlay and the sale of loans to financial institutions who were not "commercial" lenders, served as a reminder of the need for carefully drafted default remedies. For example, default remedies under a loan agreement could include the right to declare that the debt is not accelerated but is payable on demand – that declaration could be a means of ensuring that certain of the transaction security became enforceable without triggering the termination of the leasing (and thereby a violation of the stay).

Key worldwide events affecting the aviation industry

- Mid-April 2020: A 95% fall in traffic observed by Airports Council International (ACI) in 18 airports in major aviation markets in Asia-Pacific and the Middle East. Global inactive fleet increased to almost 14,400, over two thirds of the 22,000 mainline passenger airliners.

- 28 April 2020: Estimated that 54% of the world's global population subject to full or partial lockdown measures.

- Manufacturers in 2020: Airbus cut its monthly production from 60 to 40 A320s, from 4.5 to 2 A330s, and from 9 to 6 A350s. Boeing reduces output per month from 14 to 6 787s, from 5 to 2 x 777s, and 737 Max production was already halted.

- Travel restrictions 2020 to 2021: Throughout 2020 and 2021, countries impose intermittent lockdowns and travel restrictions including requirements for negative lateral flow tests and/or proof of vaccination.

- Recovery 2022 to 2024: As at January 2023, industry has made a fast recovery and ICAO analyses estimate that air transport and seat capacity and passenger totals globally are reaching 80% of pre-pandemic levels. Pre-pandemic levels expected to be exceeded in 2024.

Gibbs rule

Related to the bankruptcy overlay was the potential application of the English law Gibbs rule in cases where an airline's local bankruptcy proceedings also involved English law transactions.

In practical terms, the so-called 'Gibbs rule' means that liabilities in respect of English law governed contractual obligations will not be treated as having been discharged in foreign insolvency or bankruptcy proceedings without the consent of the relevant creditor. But there is an important exception to the Gibbs rule where the relevant creditor participates in or consents to the foreign insolvency or bankruptcy proceedings or otherwise submits (expressly or otherwise) to the jurisdiction of the foreign courts. The exception is generally considered to apply in circumstances in which a creditor submits claims or proves in the foreign insolvency or bankruptcy proceedings.

From a financier's or lessor's perspective in the English law context, this requires an assessment as to whether it is prudent to file claims in any local proceedings (and thereby potentially have a chance to participate in any court-sanctioned recoveries available to creditors) or abstain from filing and so preserve a creditors' right to claim under English law by virtue of the Gibbs rule.

That assessment should always be considered on a case-by-case basis with legal advice, but the decision is likely to hinge on whether the airline concerned has significant assets outside of the local jurisdiction which the creditor has a reasonable prospect of enforcing against (there are also other considerations, such as the interesting question of whether failing to file in local proceedings is actually a failure to mitigate losses).

View full image (PDF)

View full image (PDF)

Enforcing

We also saw an increase in security being enforced in certain contexts, particularly in the case of loan transactions which were sold in the secondary debt market. In cases where enforcement was pursued, it was time for a critical and detailed review of the operative provisions of the security documents. In those cases, it was not unusual to see existing security trustees (who were also commercial lenders) seeking to resign (no doubt concerned with potential liabilities that could arise from enforcement) and be replaced with a corporate service provider. Those instances highlighted again the importance of ensuring that all security documents contain or apply (directly or indirectly) appropriate assignment and transfer provisions.

In those financing transactions which did result in enforcement action, it was interesting to see how the choice of a New York law mortgage resulted in separate enforcement processes which did not necessarily proceed in tandem with the English law enforcement process. Since the Blue Sky case, it is not unusual for an English law financing transaction to be secured by a New York law mortgage, in order to avoid the "strict" need for an English law mortgage to be perfected when the aircraft is in a jurisdiction which recognises an English law mortgage as a valid mode of security.

In these financing transactions, other security documents, such as the assignment of the lease, were governed by English law. Although any enforcement action should be determined by reference to applicable law and the exact wording of the security documents, this could result in a security trustee having to comply with fewer statutory restrictions when selling lease claims than when enforcing the security over the aircraft under New York law (for which UCC requirements could apply). This could also result in enforcement processes being conducted according to different time schedules. In practical terms, this potential for discordant enforcement procedures may, in some transactions, be a reason why the lenders prefer to insist on an English law international interest agreement or mortgage.

"The aviation industry has arguably made a fast recovery and ICAO analyses estimate that air transport and seat capacity and passenger totals globally have now reached 80% of pre-pandemic levels. IATA expects overall traveler numbers to exceed pre-pandemic levels next year in 2024"

Best price reasonably obtainable

The potential for enforcement action also required us to revisit with clients the English law duty of a mortgagee to obtain the "best price reasonably obtainable". It is frequently the case that in English law security that a security trustee's liability is excluded except for acts of gross negligence or wilful misconduct, and that the security trustee is given broad rights to enforce the security in such manner and for such consideration as the security trustee deems fit.

Notwithstanding such exculpatory provisions, a careful construction and interpretation of the relevant provisions is necessary to determine to what extent, if at all, the duty to obtain the best price reasonably obtainable has been disapplied or varied.

Mitigation

We found that another key question raised by lenders in relation to enforcing security was whether the security trustee was under a duty to mitigate its losses. This question was particularly pertinent in cases involving finance leases, where creditors sought to maximise their claims in bankruptcy proceedings (and thereby maximise the creditors' potential recoveries in the event of a court sanctioned award in favour of creditors).

A finance lease can typically contain onerous return conditions, requiring the airline to return the aircraft in "full life" return condition, thereby incentivising the airline to exercise its purchase option in the event the leasing is terminated or expires. In these transactions, the lenders' potential claims against the airline may comprise the sum of the return condition claim (for the airline failing to return the aircraft in full life return condition), the termination value claim under the lease (as liquidated damages) and all losses covered by contractual indemnities under the finance lease.

Under English law, the rule of mitigation requires a claimant to take steps to minimise its loss and to avoid taking unreasonable steps that increase its loss, and provides that the injured party cannot recover damages for any loss (whether caused by a breach of contract or breach of duty) which could have been avoided by taking reasonable steps.

Jurisdiction, interim remedies and enforcement

Whilst a lessor's primary concern is often to seek a consensual return of the aircraft following a lessee default, lessors will often make a parallel assessment of their enforcement options in the event that negotiations are not successful. A primary consideration in making such an assessment is to establish where, and against whom, a claim can be brought under the relevant lease documents. Lease agreements are often subject to English or New York court jurisdiction, although an agreement to arbitrate is often included in leases where the lessee is based in a jurisdiction where an English or New York court judgment is not readily enforceable. However, the jurisdictional analysis can be complex, particularly where there is a multi-tier lease structure and/or lessee guarantees in place.

Notwithstanding an express submission to court jurisdiction or an agreement to arbitrate, it is important to identify whether such submission or agreement is exclusive or non-exclusive. Lease agreements often contain non-exclusive jurisdiction clauses, which permit the lessor to bring proceedings in other jurisdictions, such as the jurisdiction of the lessee or lessee guarantor or the jurisdiction in which the aircraft is located. On a related note, we have also seen lessors consider the availability of any interim remedies, such as an order for delivery up of the aircraft and, where the lessee is in clear breach of the lease agreement (such as with respect to non-payment of rental), the possible availability of a claim for summary judgment that it can then seek to enforce against the lessee.

However, when considering litigation or arbitration options it is important to consider the ease of enforcement against a defaulting lessee in its jurisdiction of incorporation and/or in jurisdictions in which its assets are located. Moreover, in a context where the lessee is in financial difficulty, lessors will also be mindful of the possibility of the lessee filing for insolvency protection and the impact that a moratorium may have on a lessor's ability to enforce against the lessee, even where the lessor is successful in obtaining a judgment in its favour.

"[t]hese authorities … clearly establish that the equitable assignee can be regarded realistically as the person entitled to the assigned chose [right] and is able to sue the debtor on that chose [right], but that save in special circumstances the court will require him to join the assignor as a procedural requirement so that the assignor might be bound and the debtor protected" Three Rivers District Council v Bank of England (No 1) 17 [1996] QB 292, Peter Gibson LJ

Final considerations

Numerous other issues were highlighted during the forbearance and repossession environment which resulted from the COVID-19 pandemic – from these, a few final ones are worth a mention:

Legal advice: Before taking any step to accelerate debt, terminate leasing or enforce security, or to sell debt under a distressed aircraft financing transaction, it is almost always advisable to take legal advice first. There can be ‘hidden' notice and other requirements placed in the transaction documents which lenders are required to comply with, as well as consequences if actions are taken in violation of applicable bankruptcy proceedings. Law firms should be tasked with reviewing the transaction documents in detail to devise an enforcement strategy which complies with all relevant provisions and applicable law.

Insurance: In all cases where we advised clients in connection with terminating leasing or exercising remedies, clients were asked to consider the position under insurances. Terminating an airline's right of possession of an aircraft can result in an aircraft ceasing to be the insurance responsibility of the airline, which can necessitate contingent cover to be in place to ensure there is no gap in insurances.

Equitable assignments: In our experience, enforcing security served as a reminder of the benefits of a legal assignment versus an equitable assignment. Under English law, a security assignment of a lease can be "equitable" rather than "legal", if the assignment does not meet all the statutory requirements for a legal assignment under the Law of Property Act 1925 – for example, where the assignment is partial.

In the aircraft financing context, and in particular in the case of JOLCO transactions, it is not unusual for security assignments to include carve-outs from the assigned property, where certain contractual rights (such as the return condition claim) are excluded from the security assignment in favour of the security trustee. Alternatively, there can be "co-extensive" rights which a lessor is entitled to exercise co-extensively with the security trustee.

Such provisions may result in the security assignment being equitable rather than legal.

Confidentiality: Finally, secondary debt trading during the pandemic reminded us of the importance of a carefully drafted confidentiality clause in the aircraft financing context. For a lender seeking to sub-participate or sell its participation under a distressed aircraft financing loan, it is not unusual to see that disclosure of the lease documents is permitted to potential new lenders or sub-participants. What is not so common is to see clear disclosure rights entitling a security trustee to disclose a lease to a prospective purchaser of the claims under that lease.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP