European leveraged finance in 2023 was saddled with the negative effects of elevated interest rates. But as the market adjusts to the "new normal", rate and price stability offer hope for a brighter 2024.

European leveraged finance overview

Rising interest rates have pushed up borrowing costs and constrained issuance activity

Subdued M&A pipeline and cautious underwriting by banks limit buyout financing opportunities

Where transactions have progressed, the bulk of activity has been propelled by refinancing deals

Private credit proves resilient in the face of wider dislocation, attracting banks into the segment

Jumbo Worldpay financing shows that investor appetite for high-quality credits remains strong, with a potential warming for backdrop in 2024

After a slow year, market behaviour will mimic certain human traits, which will act as drivers in leveraged finance markets in 2024, as lenders and borrowers look to increase activity levels

Restlessness, imitation, creativity, distraction and optimism will, in their own way, each propel market participant activity levels

More banks may move to build out their private debt capabilities, imitating the successful private debt model that demonstrated its resilience through the current cycle

In a flat market, creativity will see lenders repurpose existing funding sources and develop new products to unlock liquidity

Among alternative assets, private debt has matured rapidly and is enjoying a 'golden moment' as a markedly attractive floating-rate product

In 2024, a mounting interest burden will give rise to novel debt structures for LBOs

As a typical credit is held by a single lender or small club, the private debt model enables providers to move more quickly than their peers

Not wishing to miss this golden opportunity, investment banks are quickly establishing or building up their private debt desks, introducing another valuable option to the funding mix

After a challenging period for sponsor deal activity and limited access to finance, the outlook for the year ahead is improving

Expectations of interest rate stability are raising hopes that pricing and modelling capital structures will be easier and allow gaps in pricing expectations between buyers and sellers to narrow

High levels of dry powder and unexited assets will put structural pressure on managers to do deals, improving prospects for deal financing pipelines

Private debt has gained market share and will remain a key part of the acquisition finance mix, but loan and bond markets are rallying, providing sponsors with a wider set of financing options

After a slow year, market behaviour will mimic certain human traits, which will act as drivers in leveraged finance markets in 2024, as lenders and borrowers look to increase activity levels

Restlessness, imitation, creativity, distraction and optimism will, in their own way, each propel market participant activity levels

More banks may move to build out their private debt capabilities, imitating the successful private debt model that demonstrated its resilience through the current cycle

In a flat market, creativity will see lenders repurpose existing funding sources and develop new products to unlock liquidity

After a slow 12 months characterised by tepid financing activity, 2024 will be a year when we see human traits defining how dealmakers and investors will return back into the market.

We outline five human behaviours and psychological triggers that could shape European debt capital markets in 2024 after an anxious 2023.

1. Restlessness

Transaction volumes slowed markedly in 2023, with year-on-year European syndicated loan issuance declining by 10 per cent in 2023, and buyout M&A activity dropping by almost three-quarters.

After limited opportunities to transact, restlessness could propel financial sponsors back to the market. Buyout funds still have more than US$1 trillion of uninvested dry powder to deploy, according to Bain & Co analysis, with private debt dry powder sitting at approximately US$400 billion, according to Apollo figures. There is also growing urgency on the sell-side for sponsors to deliver exits, with Bain & Co estimating that the value of unexited assets in private equity portfolios is at four times the levels observed during the 2008 global financial crisis.

There is a structural imperative to transact built into the private markets model, and with large pools of undeployed capital to invest, sponsors will be obliged to return to dealmaking after pausing for breath in 2023.

There is also pent-up demand on the lender side for more deal and financing opportunities, as seen with the strong appetite in the private debt community to fund Permira and Blackstone's buyout of European online classifieds business Adevinta. The €4.5 billion credit deal to fund the transaction was oversubscribed by approximately €2.5 billion, with direct lenders offering €7 billion.

2. Imitation

Private debt has emerged from the current downcycle in credit market in a strong position, delivering yields on senior secured risk in the region of 10 per cent and continuing to finance deals. Investment banks have noted the success of the private debt model, and 2024 could see increasing numbers of banks move to imitate this model by launching and expanding their own private credit capabilities.

Citigroup, Barclays, Morgan Stanley and JPMorgan Chase are among the banks that have already moved to build out their private credit capabilities.

Private debt has emerged from the current downcycle in credit markets in a strong position, delivering yields on senior secured risk in the region of 10 per cent and continuing to finance deals.

Banks that make debt commitments to borrowers when underwriting leveraged loans and high yield bonds, with a view to selling this debt on to investors, have found it harder to syndicate debt in the current market, and have found themselves exposed to more unsold tranches of debt than planned.

Moving into private credit mitigates syndication risk and also allows banks to compete directly with private debt funds, which have shown their ability to finance larger credits and take market share from the syndicated loan and high yield bond desks of the banks. Expect more banks to make their moves in private credit in 2024.

3. Creativity

Depressed deal activity and a contraction in mainstream financing issuance has given dealmakers space and time to think of how to repurpose existing funding sources and develop new products to unlock liquidity.

The necessity for creativity has already seen the emergence of new financing structures, as lenders and borrowers adapt to changing circumstances.

Examples include the rapid expansion of NAV financing—credit facilities issued against the funds of financial sponsors. This once esoteric corner of the financing market is expected to expand sixfold to US$600 billion by 2030, according to Pitchbook, as sponsors explore different ways to fund portfolios and make distributions, and banks see an opportunity to keep putting money to work when other deal pipelines are constrained.

Private debt players, meanwhile, have not only grown market share by underwriting ever-larger ticket sizes, but are now also bundling portfolios of loans and selling on these tranches of assets to investors in the first private debt CLOs.

These CLOs, a significant development in private credit, illustrate the creativity and innovation that is set to drive lending activity and provide more liquidity in the next 12 months.

4. Distraction

Financial sponsors and lenders will be preparing for higher volumes of new deal activity in 2024, but time and resources allocated to new deals will have to be balanced with ongoing obligations to manage out legacy assets that have underperformed and haven't yet been restructured or dealt with via continuation funds. Stewarding portfolios of underperforming assets could remain a distraction through the course of 2024.

Indeed, ratings agency Fitch expects the sustained period of elevated interest rates to continue filtering through markets during the next 12 months, driving further increases in leveraged finance defaults in 2024. According to Fitch, European default rates for high yield bonds and leveraged loans are forecast to reach 4 per cent in 2024 and 2025.

Liability management exercises and amend-and-extend deal volumes are set to remain a feature of the market for the foreseeable future, and could continue to absorb lender and borrower bandwidth, diverting focus and attention from pursuing new deals.

5. Optimism

After a challenging 2023, there is cautious optimism that M&A activity and debt issuance volume will begin to rebound in 2024.

Leveraged finance stakeholders have noted a growing consensus that interest rates are expected to flatten out during the next 12 months. A stabilising interest rate backdrop will provide greater certainty on financing costs and availability. This in turn will make it easier for buyers and sellers to price risk, which will help to narrow the gap between buyer and seller asset valuation expectations, which hindered deal progress in 2023. Gains in European stock markets (the Stoxx Europe 600 Index climbed by more than 10 per cent in 2023) also serve as a positive, forward-looking indicator for deal activity.

After a year of focusing on downside risk and waiting for markets to show clearer direction, borrowers, investors and lenders will be gearing up teams in preparation for an anticipated uptick in deal activity.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

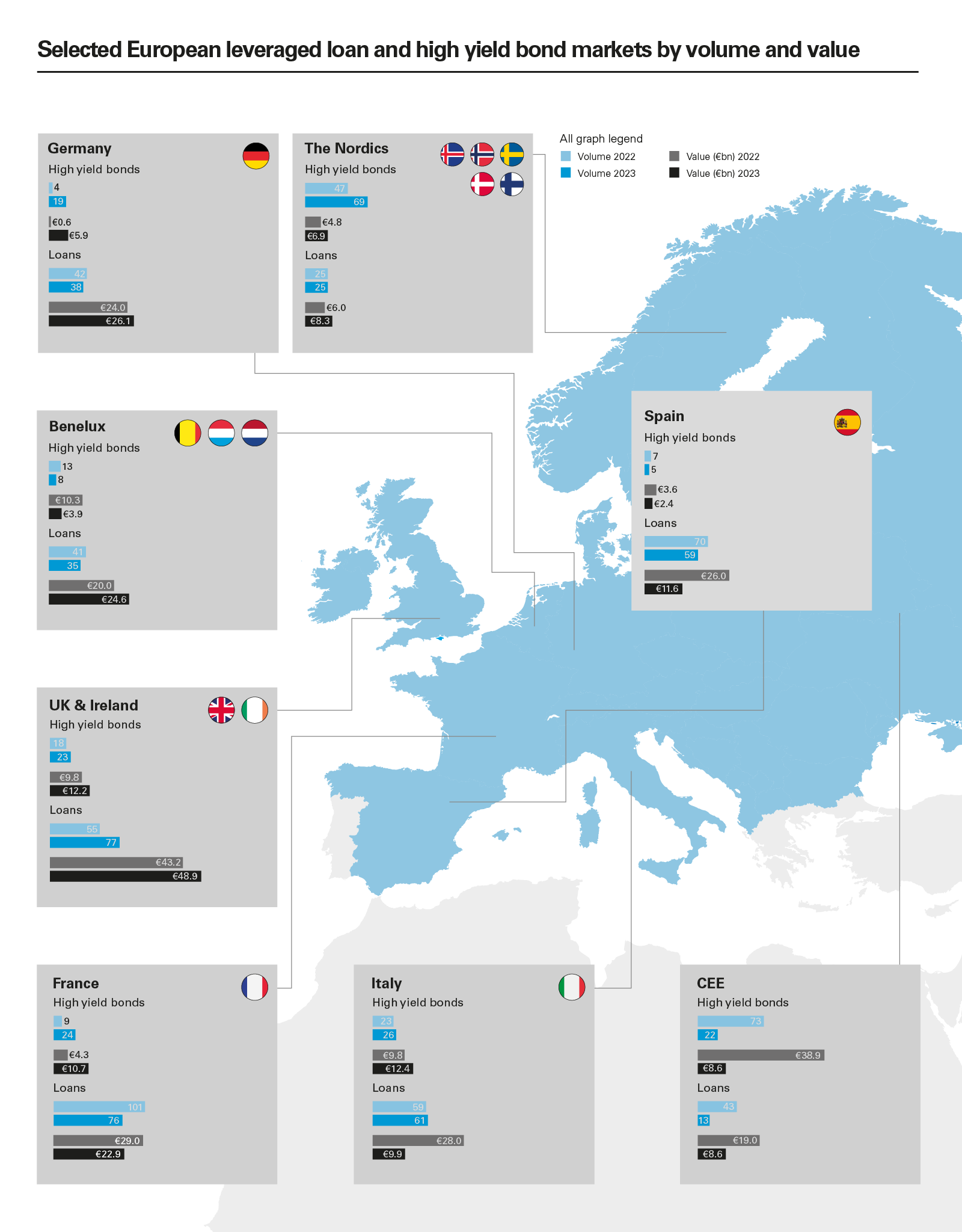

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)

View full image: Selected European leveraged loan and high yield bond markets by volume and value (PDF)