Mining & metals 2024: Geopolitics in the driver’s seat

2023 was a boom year for interest in the mining & metals sector from an ever-expanding array of manufacturers, consumers, and governments. 2024 promises more of the same. To get a read of what will drive and affect sector activity in the year ahead, White & Case has conducted its eighth annual survey of industry participants, with 240 senior decision-makers sharing their thoughts—our largest-ever class of respondents.

16 min read

Explore Trendscape

Our take on the interconnected global trends that are shaping the business climate for our clients.

One thing is clear: Geopolitics will dominate the year ahead while firms manage the tail-end of pandemic challenges such as supply chain disruptions and skilled labor shortages as well as local political conditions driving changes in tax, trade, and regulatory policies. With so much uncertainty ahead of US and other elections, firms will have to move fast to lock in financing and partnerships ahead of any volatility while planning for a market likely to be rocked by tandem trade and geopolitical tensions.

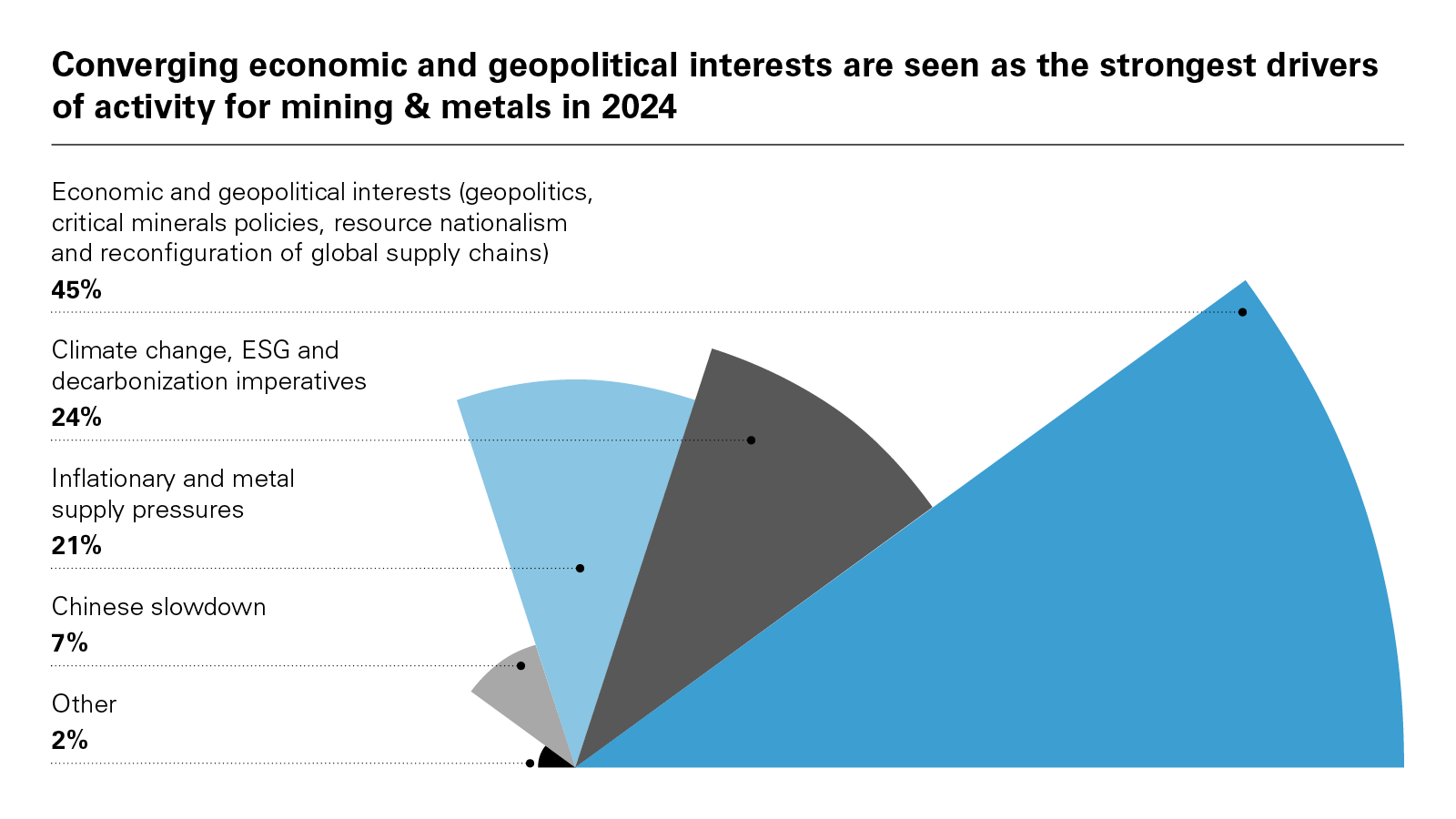

View full image: Converging economic and geopolitical interests (PDF)

View full image: Converging economic and geopolitical interests (PDF)

At the same time, there are growing concerns about a squeeze on the availability of metal supplies, particularly for copper where disruptions to major mines and tight supply/demand balances flipped market expectations from surplus to deficit in 2024 in the closing weeks of last year. 45% of respondents identified factors primarily driven by geopolitics as their primary trend driving activity in 2024: geopolitics (20%), resource nationalism (11%), the reconfiguration of mining & metals supply chains (7%), and industrial and critical minerals policies (7%). All other categories intersect with these trends in some way, highlighting the degree to which geopolitics is driving sector activity over the year ahead.

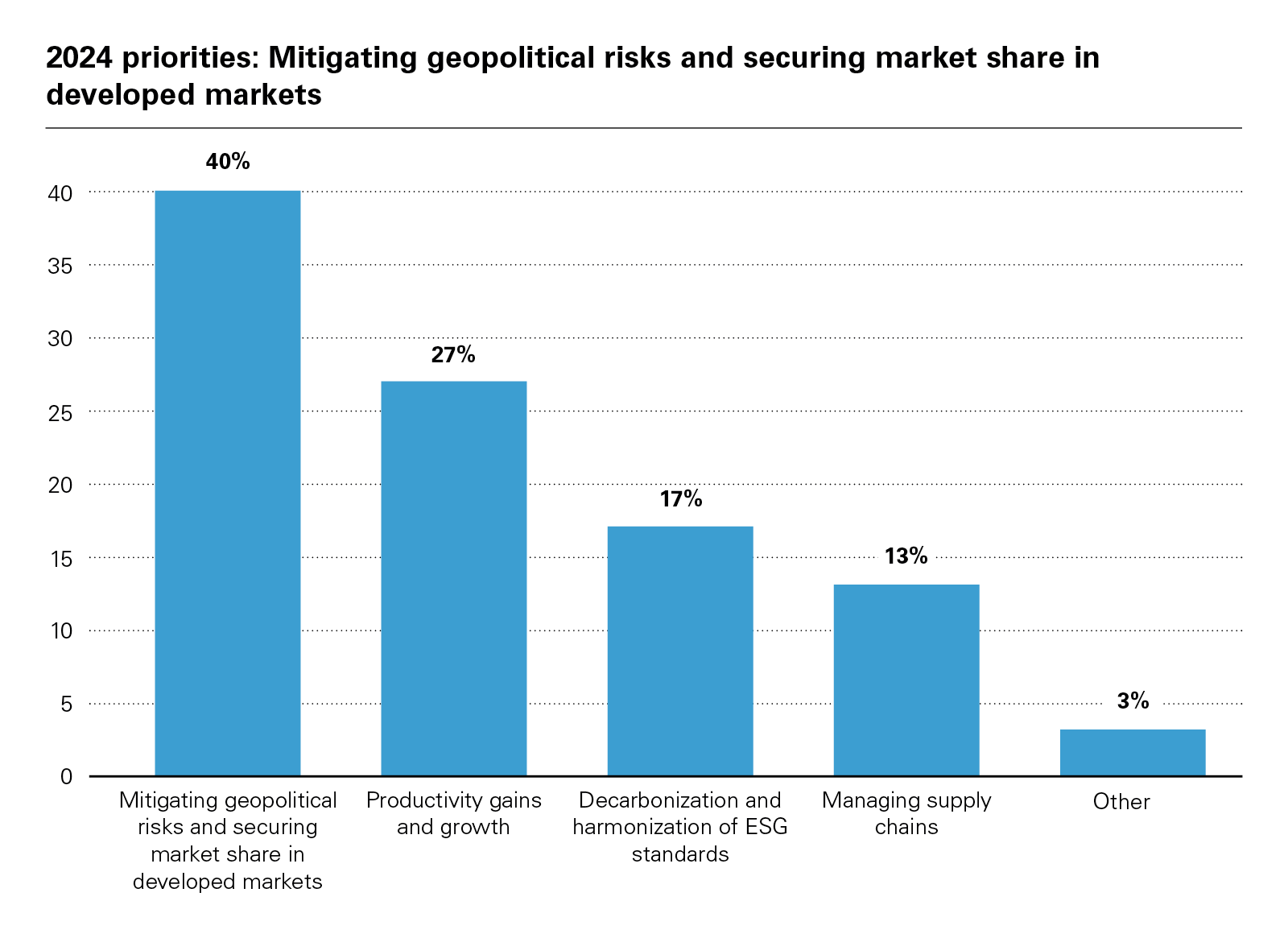

View full image: 2024 priorities: Mitigating geopolitical risks and securing market share in developed markets (PDF)

View full image: 2024 priorities: Mitigating geopolitical risks and securing market share in developed markets (PDF)

With so much uncertainty ahead of US and other elections, firms will have to move fast to lock in financing and partnerships ahead of any volatility while planning for a market likely to be rocked by tandem trade and geopolitical tensions

80%

Lithium prices dropped a whopping 80% year-on-year during 2023 and could fall further still in 2024 on supply growth

These trends come as market conditions are turning a corner in some respects. Higher interest rates depressed M&A activity for much of 2023 and complicated project financing and refinancing for miners lacking significant cashflow from operating assets. US growth has paced developed economies, proving remarkably resilient despite higher interest rates and the US is increasingly likely to achieve a 'soft landing' without recession. Markets have pivoted on rate expectations with the odds of US rate cuts in H1 2024 despite a hotter than expected 0.3% CPI print in December driven by stronger real wage growth and one-year inflation expectations have fallen to 2.9%, the lowest level since December 2020. Slowing construction demand in China has contributed to lower prices, but imports of copper ores have remained strong. The IMF expects moderating global GDP growth of 3.0% for 2023 and 2.9% for 2024. Despite weaker prices over much of the year, the growth outlook for demand has remained comparatively strong following the fastest and largest rate hiking cycle since 1983.

As of now, US GDP growth for the year ahead is expected to fall below 2% and the Eurozone is likely to grow at or less than 1% if it manages to avoid recession. While forecasts for China's GDP growth are still in the range of 4.5-5%, the continuing rotation of capital out of real estate and the decline of property values will alter the composition of metals demand growth and points to additional downside risks absent a change in policy to boost domestic consumption. With the global economy shifting gear downwards in the year ahead, there was a surprising lack of agreement about dominant themes across the sector. Decarbonisation and ESG remain the top line selling points, but respondents noted that survival might be the dominant reality and "global supply and demand factors will continue to dictate production, investment and pricing patterns while ESG and related efforts will be secondary." Just one respondent flagged recycling as a potential theme.

A changing, more nuanced, business cycle for mining & metals?

Since the pandemic, activity in the mining & metals sector has largely synced up with the global growth cycle. The year ahead may see more differentiation by product given that investment into mines, processing, refining, smelting, and manufacturing across energy transition supply chains continues at elevated levels, aided by national policies offering tax credits, preferential trade access, state aid, EV incentives and other forms of support. Current EV demand has not led to a supply crunch for lithium. Lithium prices dropped a whopping 80% year-on-year during 2023 and could fall further still in 2024 on supply growth. Nickel market surpluses are expected to remain or even widen in 2024 as increases in Class 2 supplies, driven by new mines and refining capacity in Indonesia, have been matched with higher refining and smelting production to meet battery demand for nickel-cobalt-manganese batteries. Nickel was the worst-performing on the London Metals Exchange for 2023 with prices down roughly 45% in annual terms, partially a result of volatility from the supply fears and exaggerated speculative positioning that led to market-breaking volatility in March 2022. Against this backdrop, 21% of our respondents believe geopolitical tensions will contribute to a slowdown in commodities demand, creating a drag on prices.

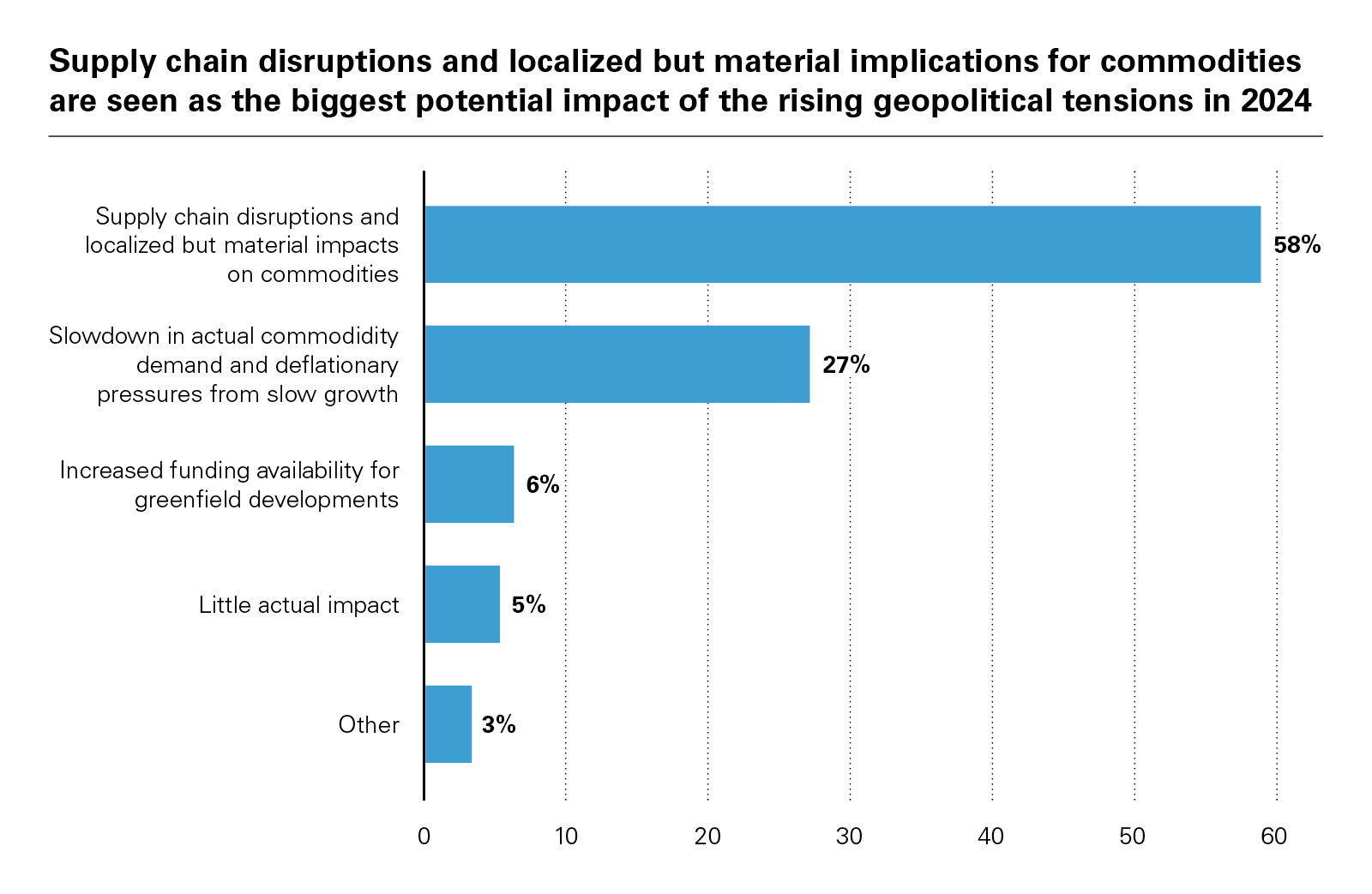

The persistence of concerns regarding supply chain disruptions was one of the more interesting findings from our respondents, with 45% of respondents citing it as the biggest impact of geopolitical tensions. Two respondents noted the "shift in jurisdictions that are deemed fundable" and "increase in non-technical risks" such as labor supply contributing to and compounding these pressures.

View full image: Supply chain disruptions (PDF)

View full image: Supply chain disruptions (PDF)

Since the pandemic, activity in the mining & metals sector has largely synced up with the global growth cycle

Over the last 12 months, measures of supply chain bottlenecks have significantly eased and driven much of the disinflation now supporting potential rate cuts from the Federal Reserve in H1. Houthi attacks on shipping in the Red Sea and the launch of Operation Prosperity Guardian are the most visible reminder of heightened geopolitical risks directly affecting the transit of goods. Climate-related risks are impacting as well. Low water levels in the Panama Canal linked to drought are expected to reduce the draft of vessels using the route for at least another 10 months. The increase in freight rates and greater logistical costs from more expensive, less efficient routes raise operating costs for mining & metals firms and are beyond their control, hurting margins.

A combination of growing variation between metals for supply/demand movements and growing anxieties among end users about the 'normalization' of supply chains may drive strategic project and deal activity irrespective of price expectations or the cost of capital. Governments continue to push businesses to secure strategically important sources of critical minerals. While project financing deal flows reflect lower levels of interest at current levels, 'defensive' investments intended to ensure continuity and diversity of supply backed by governments may play a greater role in the next 12-18 months.

Evolving disruption risks

The upswing for mining & metals firms that took off during 2023 is unlikely to abate, but the rate and nature of growth and investment will evolve and mature over the year ahead

However, our respondents' concerns and their identified market trends point to a more complex picture shaped by the difficulties commercializing projects across energy transition supply chains in the year ahead. Various subsidy programs, tax credits, and preferential trade policies have dramatically elevated business interest in midstream and downstream projects for critical minerals and metals across developed markets, particularly the United States. But standing up a bevy of new refining and manufacturing projects for battery, electric vehicles, and renewable energy input are hostage to completion risks in the early stages of project financing and development. Since offtake underwrites the bankability of projects and businesses, especially battery manufacturers and OEMs, are racing to secure critical minerals offtake from mines directly, delays can have knock-on effects across emergent 'friendshored' supply chains. These delays can arise from difficulties financing, issues with complex permitting processes, and unforeseen changes in ESG and regulatory standards. For example, recent guidance from the US Treasury Department regarding the exclusion of batteries and vehicles using inputs from so-called 'foreign entities of concern' (FEOC) from eligibility for tax credits per the Inflation Reduction Act (IRA) has opened the door to a greater degree of uncertainty for OEMs closing offtake arrangements or licensing IP or technology from Chinese counterparties.

Disruptions to supply chains can also arise from these mismatches in timing for project development due to an increasingly imbalanced market structure. China's real estate slowdown in 2023 had a comparatively muted impact on ferrous metals prices. Iron ore found consistent support above $100/ton thanks to low inventories. Aluminium similarly found support at or around $2,250 a ton due to low inventories. However, the loss of economic growth associated with less investment into property has prompted a state-level drive to funnel credit at the regional level into manufacturing, leading to a boom of lending and development of battery and automotive production capacity. In parallel, Chinese metals firms have expanded investment into new copper refining capacity in the last 12 months cornering the market for most of the offtake from new copper mines providing marginal increases in global production. The result is an intensification of the structural imbalances within the Chinese economy and pressure on newer market entrants competing with Chinese incumbents for market share.

US$2,250

The price of aluminium in international commodity markets reached US$2,250 per ton in 2023

Projects in developed markets in the automotive and renewable energy supply chain will potentially face headwinds from a growing surplus of exports from China even with policy support. These risks dovetail with the growing use of resource nationalism measures across commodity exporting economies, most recently exemplified by the Panamanian government's ordering First Quantum Minerals to cease all operations at the major Cobre copper mine on December 8, 2023. Respondents identify a wide range of risks, but all of them are shaped by the rapid (geo)politicization of metals markets in the last 18 months and the long shadow of the wide range of elections in developing and developed markets in 2024. One respondent noted that "regulations regarding permitting and development pose disruption risks, particularly in the US where five potential tier one copper projects remain stalled." Supply gaps may emerge without success pursuing permitting reform in developed markets more generally.

ESG is now BAU

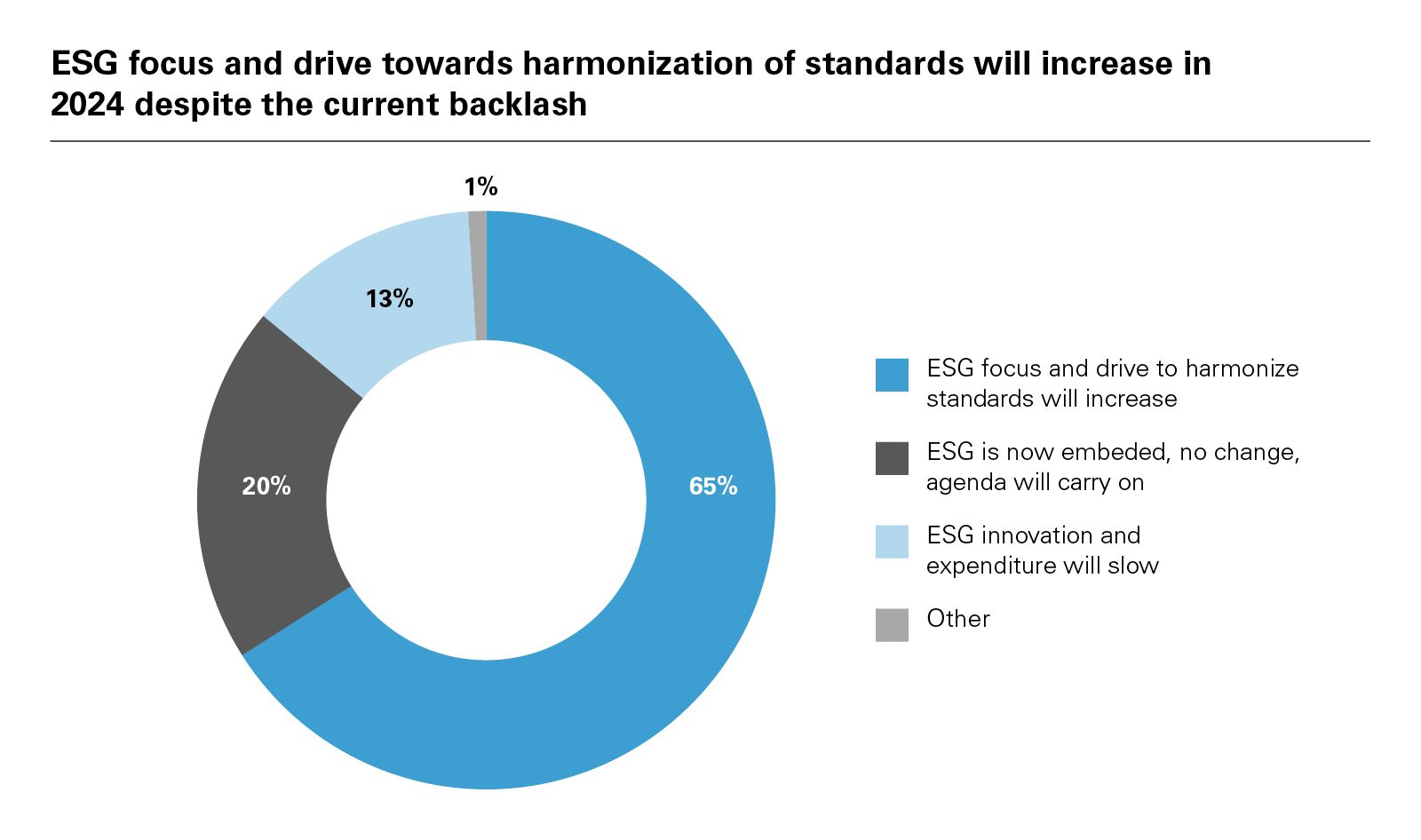

Interestingly, our survey shows there is little evidence of a "retreat from ESG" despite growing political backlash and perceived concerns over competition between jurisdictions that prioritize growth over enforcing high regulatory standards. Our respondents expect that sector participants will only intensify their efforts towards adopting ESG best practices to access financing and ensure compliance with policy support, with 36% citing difficulty accessing capital without it and another 29% expecting to see greater pressure to harmonize sector ESG practices. The latter point remains the primary challenge for mining & metals firms, which will likely encourage further efforts to come up with a sector-led solution until a framework achieves critical mass.

View full image: ESG focus and drive (PDF)

View full image: ESG focus and drive (PDF)

ESG criteria may be supplanted by new vocabulary, but has become business as usual for most firms operating in the sector, especially among the relevant sources of financing. Respondents also noted that as growing volumes of data regarding the emissions, environmental, and social impact of mining become available, firms failing to invest in their capabilities or embedding data collection into operational decision-making risk falling behind. These measures extend to supply chain diligence. As one respondent noted, "downstream supply chains will come under greater scrutiny. No one wants to be caught selling to unfriendly arms makers."

ESG criteria may be supplanted by new vocabulary, but has become business as usual for most firms operating in the sector

Growing scrutiny over the environmental footprint and biodiversity impact of mining operations intersects with pressures typically identified with resource nationalism. These can create technical bottlenecks for projects whenever frontier production methods are at play. Chile is a leading example with last year's lithium reforms mandating the use of Direct Lithium Extraction (DLE) for all projects to minimize water use in the Atacama Desert. The problem, however, is that no major lithium producer has successfully commercialized DLE at scale, DLE processes must be tailored for each individual project based on local geological conditions, and aside from Albemarle and existing plans to launch a DLE pilot project in Arkansas, Chinese miners have a head start on the relevant tech.

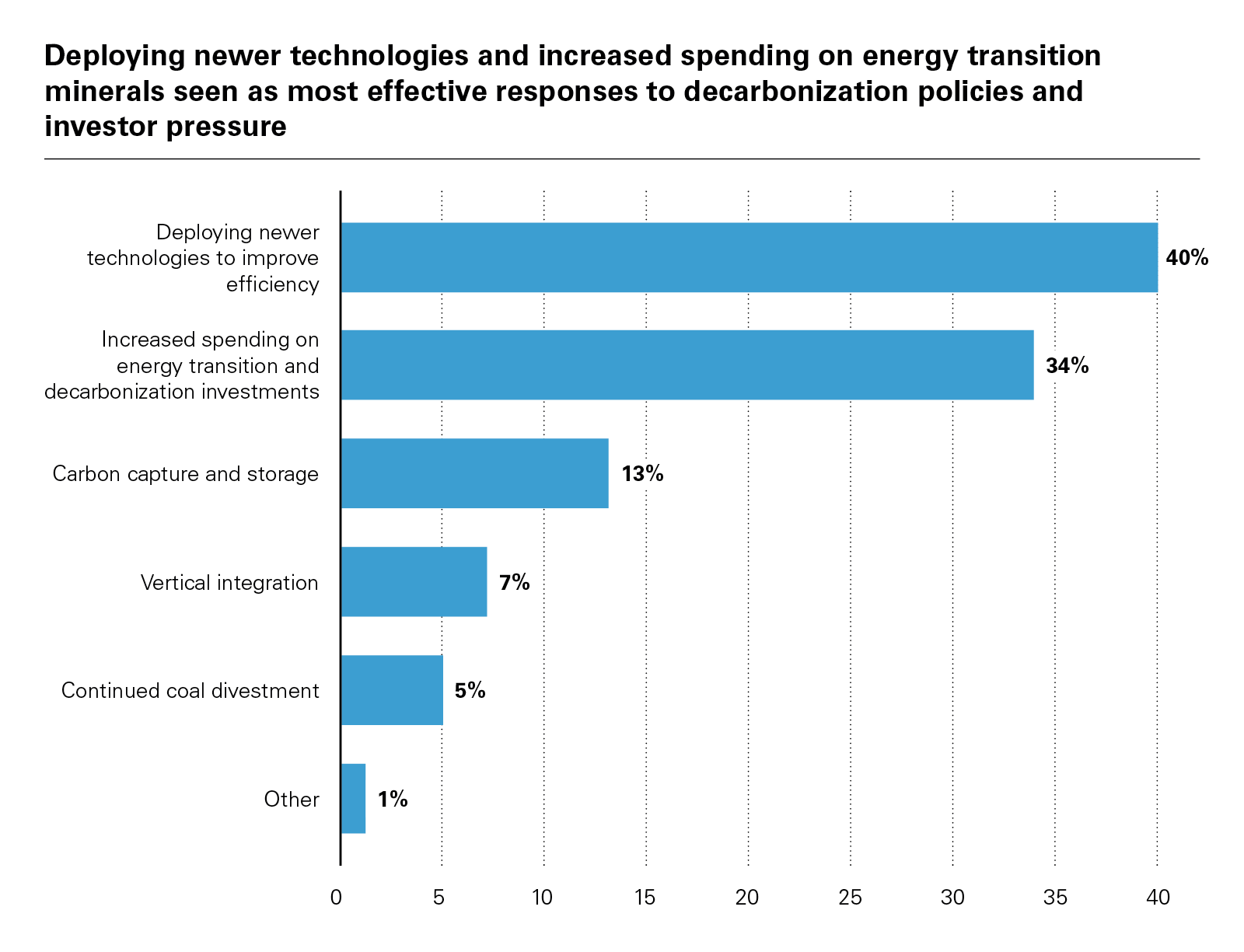

Even as classifications move on from traditional ESG labels, mining & metals firms continue to pursue investments into additional renewable power generation capacity, venture capital and strategic acquisitions for decarbonisation IP, and seek reductions of emissions across scopes 1, 2, and 3. There is little reason to foresee a significant step back, even in a tougher price environment with elevated operating costs. One respondent noted, however, that "there remain risks of a split between governments and jurisdictions that see ESG measures as a market advantage and others who prioritize growth and investment above all else." OEMs and newer offtakers will continue to play a leading role maintaining relevant criteria through their compliance and procurement standards across developed, emerging, and frontier markets. Further, stricter adherence may reduce tensions with local and national governments threatening policy interventions that may otherwise derail project completion or pose expropriation risks. 40% of respondents believe that investments and deployments of tech to improve efficiency and reduce emissions will dominate the decarbonization agenda in 2024.

View full image: Deploying newer technologies (PDF)

View full image: Deploying newer technologies (PDF)

Companies will continue to acquire their own IP to do so to mitigate potential dependence on riskier counterparties and find new sources of competitive advantage should they be able to scale solutions to sell to the broader market.

Trading places

Efforts to secure parts of emerging mining & metals value chains crucial to the energy transition will continue to dominate national policies. 2024 is likely to see an intensification of diplomacy seen the last 12 months regarding preferential trade access to key economies and blocs, namely the US, USMCA, and EU as well as further action among the 14 members of the Indo-Pacific Economic Framework for Prosperity (IPEF). 25% of respondents cited localization requirements for beneficiation and processing as the top challenge for miners in the year ahead when it comes to market interventions, an increasingly common measure in frontier markets to force firms to invest into value-added production domestically. For instance, Namibia and Zambia have banned the export of unrefined spodumene, forcing companies to process it locally. Lithium poses its own challenges – lithium hydroxide does not travel long distances as well as lithium carbonate – but other transition metals, particularly copper, may face growing dissonance between efforts to expand midstream refining and processing domestically in China versus those onshore more of the metals value chain closer to primary production.

There is also no clear view on the link between greater geopolitical risks, negative effects on the sector from slowing growth, and counterparty risks. Comparatively rapid disinflation in the US and outright deflation risks in the Eurozone have given rise to hopes of faster-than-expected rate cuts in H1, providing a potential buffer against a further slowdown.

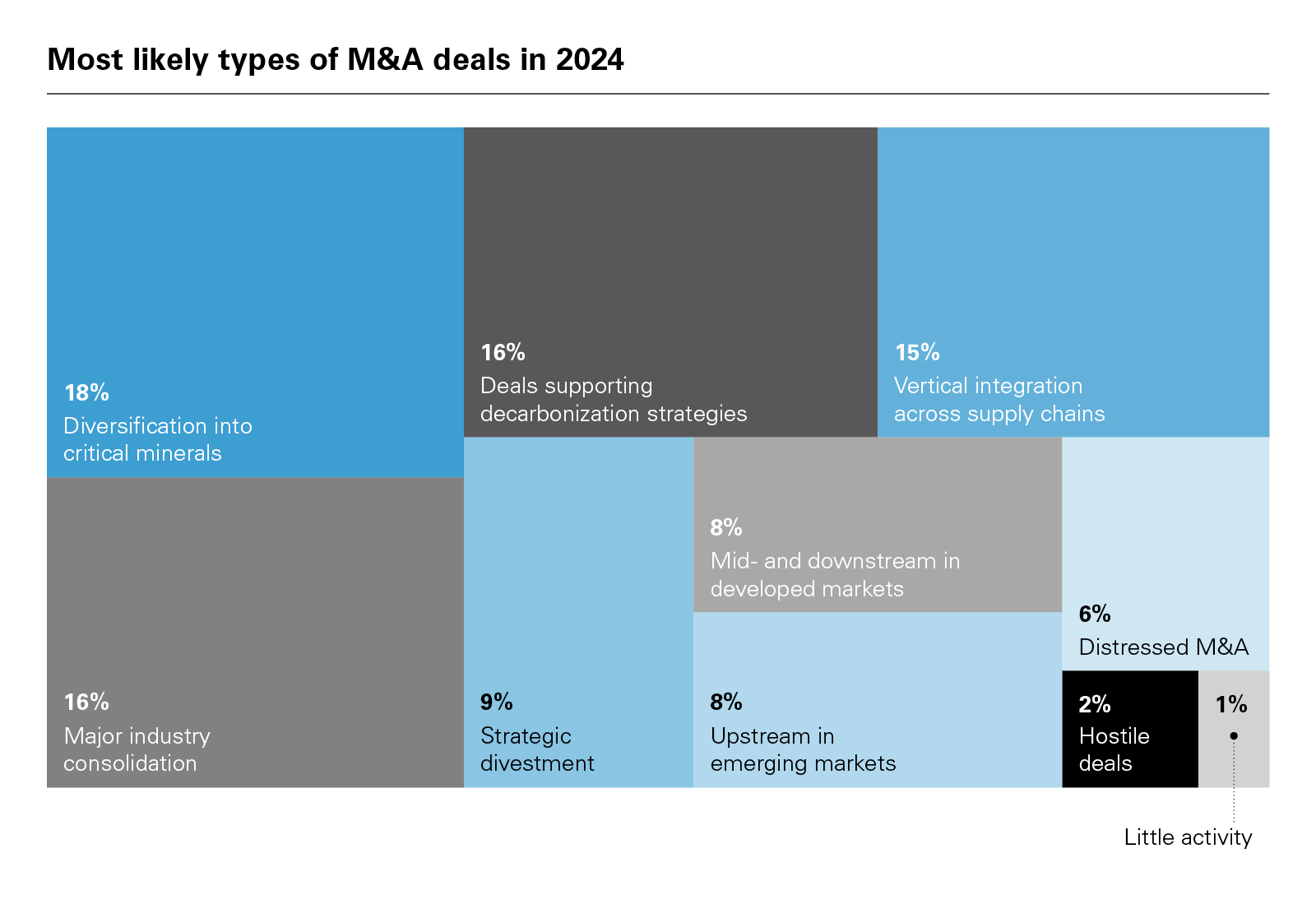

A weaker USD alongside falling rates would benefit metals prices, though the relative over-performance of the US economy compared to other developed peers may offer additional support depending on capital flows. Monetary conditions have already eased over the last few months from better-than-expected US inflation prints and expectation of more rapid easing from the Federal Reserve, leading to a surge of FX-denominated emerging market borrowing as investors 2023 reposition themselves after several years of avoiding higher-risk sovereign debt. Emerging Markets issued US$51 billion in sovereign debt in the first week of January alone. Where 2023 was about economic 'normalization' of China and strong growth in the US, the year ahead may prove better than expected for emerging markets as the dollar most likely falls. Respondents see a comparatively diverse array of drivers for M&A in 2024, with mineral diversification (18%), sector consolidation (16%), vertical integration (15%), and decarbonization (14%) leading the way. One respondent expected an uptick in activity "because of global competition for capital due geopolitical pressures and, when relevant, increasingly stringent ESG requirements from lenders."

View full image: Most likely types of M&A deals in 2024 (PDF)

View full image: Most likely types of M&A deals in 2024 (PDF)

Whether mining companies can benefit will be heavily influenced by the scrutiny applied to projects' impact on local communities, the willingness of governments to intervene for political or social reasons, and the availability of necessary infrastructure. South Africa accounts for nearly 60% of global platinum group metals (PGM) production, but ongoing shortages of electricity from an inefficient, underinvested power system continues to cause interruptions and force miners to build out their own additional generation capacity. National policies promoting sector development may also foster greater volatility as projects and operators run into unexpected constraints. Without a strong rebound in price levels, it seems less likely that governments will seek to increase tax burdens on mining & metals firms in the next 12 months unless they dominate a specific metal or niche.

As yet, there is limited evidence of a broad-based metals price rebound with a majority of the bullish case linked to lower inventory levels for metals used in construction and the slackening of real estate demand in China. Investor appetite for emerging market debt and falling interest rates should reduce fiscal constraints on many governments, allowing them to opt for more aggressive tax policies, excluding those with comparatively narrow tax bases, a high level of dependence on minerals for the stability of the state budget and current account, and significant sociopolitical pressures.

Weaker prices pushing consolidation

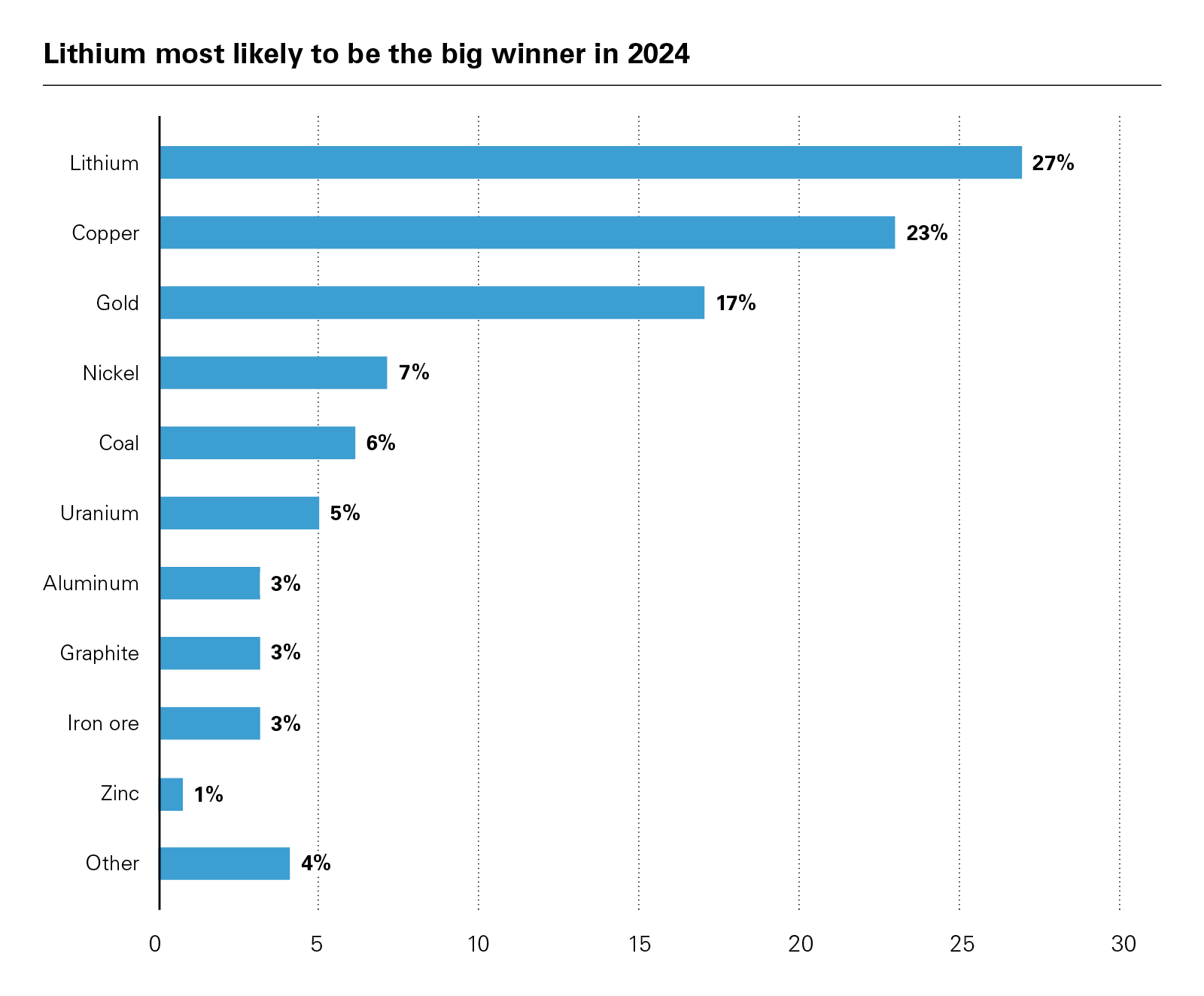

Copper remains an outlier because of the large discrepancy between current price levels, available supply expansions, and expected demand. Lithium seemed to score highly because of its massive selloff – a roughly 80% decline for most existing benchmarks – over the previous 12 months, creating potential for a low-base effect. The relative absence of concern about scrutiny for counterparty risks in the year ahead also underscores expectations that in a tougher market environment, mining & metals firms will turn to offtakers as needed regardless of emerging concerns from investors given political volatility. Lower prices have cooled interest from automakers who are newer entrants to the market such as Ford and GM to provide financing for new mine projects to secure offtake now that scarcity fears for lithium and cobalt have subsided.

View full image: Lithium most likely to be the big winner in 2024 (PDF)

View full image: Lithium most likely to be the big winner in 2024 (PDF)

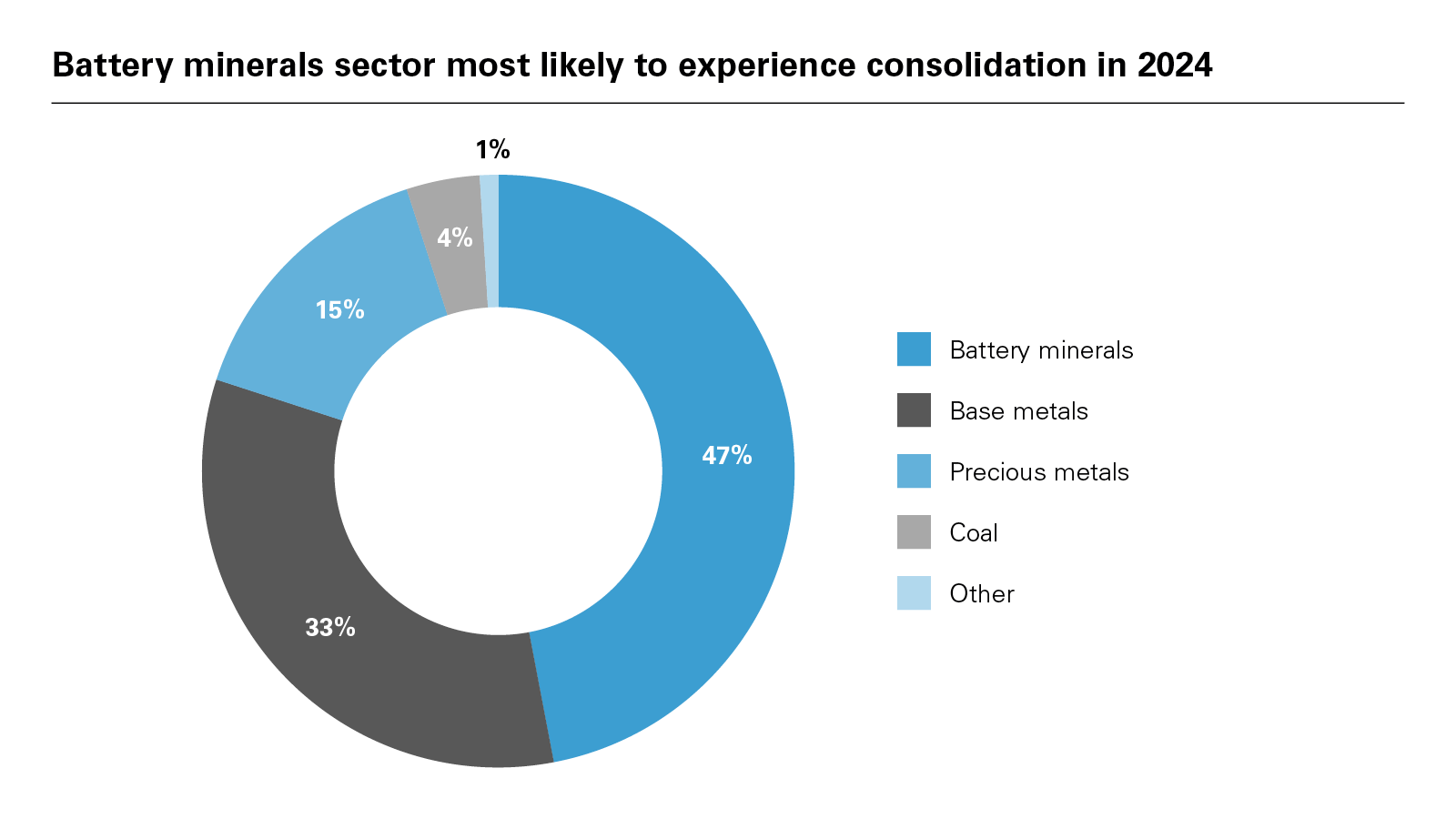

Metals price indices are relatively flat year-on-year outside of battery metals, which points to greater difficulty securing financing for early-stage projects. However, lower prices and easing constraints on the cost of capital point to scope for consolidation in the battery metals, the sector 47% of respondents named the likeliest to experience consolidation in 2024.

Falling interest rates should ease the squeeze on the project development pipeline, but an uptick in M&A is likelier to follow based off our respondents' view that the cost of capital remains the largest obstacle. 2023 saw nearly $71 billion in M&A across the mining & metals led by a 40% increase in deals for lithium, cobalt, and nickel assets over 2022. A falling rate environment will be conducive to continued activity at similar or higher levels, but the nature of M&A remains at risk depending on the outcome of elections. Acquisitions reliant on existing tax credits and trade policies written into the Inflation Reduction Act are exposed to a significant disruption next year in the event that President Joe Biden does not win re-election.

View full image: Battery minerals sector most likely to experience consolidation in 2024 (PDF)

View full image: Battery minerals sector most likely to experience consolidation in 2024 (PDF)

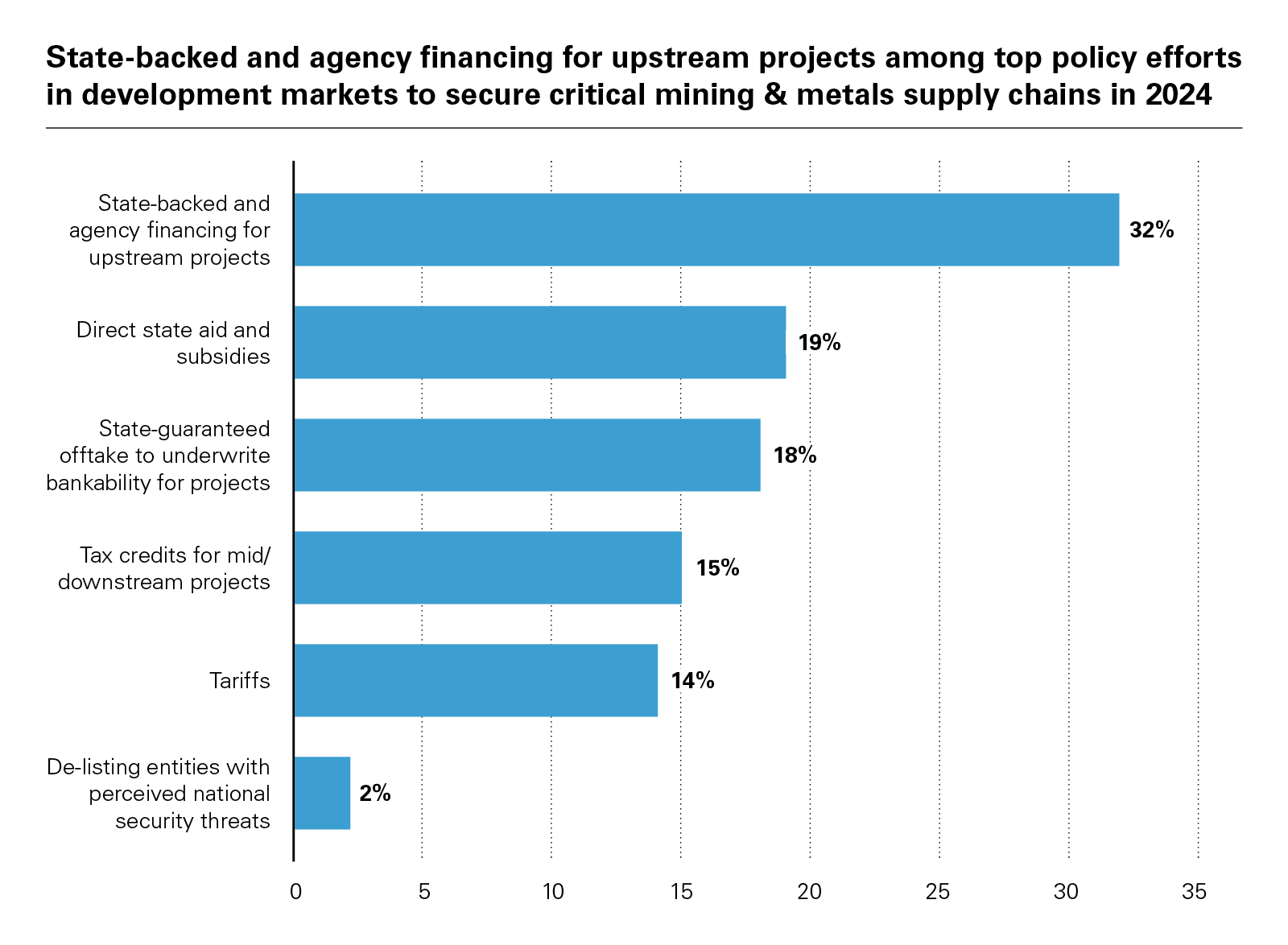

A likely neutral price environment will disproportionately affect junior miners despite the expanded provision of targeted financing from export credit agencies, development institutions, and national policy lenders tasked with securing critical mineral supply chains. Weaker price upside and renewed interest rate volatility from an expected loosening of monetary conditions will, as one respondent put it, contribute to "mismatches in the valuation of assets under consideration for M&A." 32% of respondents see state-backed and agency financing as the most common policy effort to support sector investment, followed by 19% citing state aid and 18% citing state-guaranteed offtake.

View full image: State-backed and agency financing for upstream projects among top policy efforts in development markets to secure critical mining & metals supply chains in 2024 (PDF)

View full image: State-backed and agency financing for upstream projects among top policy efforts in development markets to secure critical mining & metals supply chains in 2024 (PDF)

The upswing for mining & metals firms that took off during 2023 is unlikely to abate, but the rate and nature of growth and investment will evolve and mature over the year ahead. Costs and disruptions still weigh on sector participants as end-users maintain a more prominent role going forward. Future uncertainty may drive more activity in the short-term as windows of opportunity may close. 2024 will undoubtedly have surprises in store.

Percentages in graphs may not sum up to 100% due to rounding

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2024 White & Case LLP