European NPLs: Market earns welcome breathing room

What's inside

The ongoing decline in NPL volumes in 2022 and pivot towards smaller disposals leave European lenders well positioned to withstand adverse economic conditions.

Lenders are enjoying the fruits of their labours. Having offloaded their most toxic bad loans, in 2022 banks were instead able to focus on smaller, strategic NPL disposals, even as macroeconomic hardship began to mount.

Europe's banks have been on quite a journey to get their non-performing loans (NPLs) under control through NPL disposal tools including portfolio sales and securitisations. While disposals of toxic debt were interrupted by the COVID-19 crisis, this work has been unrelenting. In last year's edition of this study, we described how NPL sales in Europe in 2021 had bounced back from pandemic disruption; 12 months later, we can report that sales continued in 2022, though at much reduced levels.

That slowdown reflects the extensive progress already made by banks. Most have reached a point where the imperative to further trim their NPL volumes is much diminished—they are free to make disposals according to their strategic and tactical priorities, rather than to avert disaster. That remains true despite the mounting economic and geopolitical volatility that Europe has faced over the past 18 months.

In this year's report, we examine the outlook for Europe's NPL market, including for secondary sales, over the months and years ahead. The first section considers the changing market dynamics, including the latest NPL data and analysis of what is driving activity. The second section offers a deep dive into key markets across Europe.

The future is highly uncertain. There is a case to be made both for a resurgence in NPL volumes and deal activity, and for a continued slowdown. Much will depend on the economic outturn, where uncertainty levels are even more elevated. The good news, however, is that these are precisely the market conditions in which new opportunities abound.

European NPLs: New buyers emerge as disposals shrink

Despite broad economic turmoil, countries across Europe have so far avoided recession. Banks have been able to catch their breath with the NPL market shrinking steadily post-pandemic. But looking forward, Europe is hardly anxiety-free.

Regional spotlight on NPLs: Italy, the UK, Greece and Spain

Total NPL volumes across Europe are down and ratios remain stable, with countries such as Italy and Greece having worked especially hard to deal with toxic assets. Even with economic growth set to slow, banks have reason to be broadly optimistic about their NPL levels.

Declining NPL ratios have put banks in a somewhat more comfortable position than they were this time last year, but the threat of macroeconomic hardship looms over borrowers.

Regional spotlight on NPLs: Italy, the UK, Greece and Spain

Total NPL volumes across Europe are down and ratios remain stable, with countries such as Italy and Greece having worked especially hard to deal with toxic assets. Even with economic growth set to slow, banks have reason to be broadly optimistic about their NPL levels.

The NPL market looks set to remain flat, particularly now that state-backed securitisation schemes in Italy and Greece have run their course.

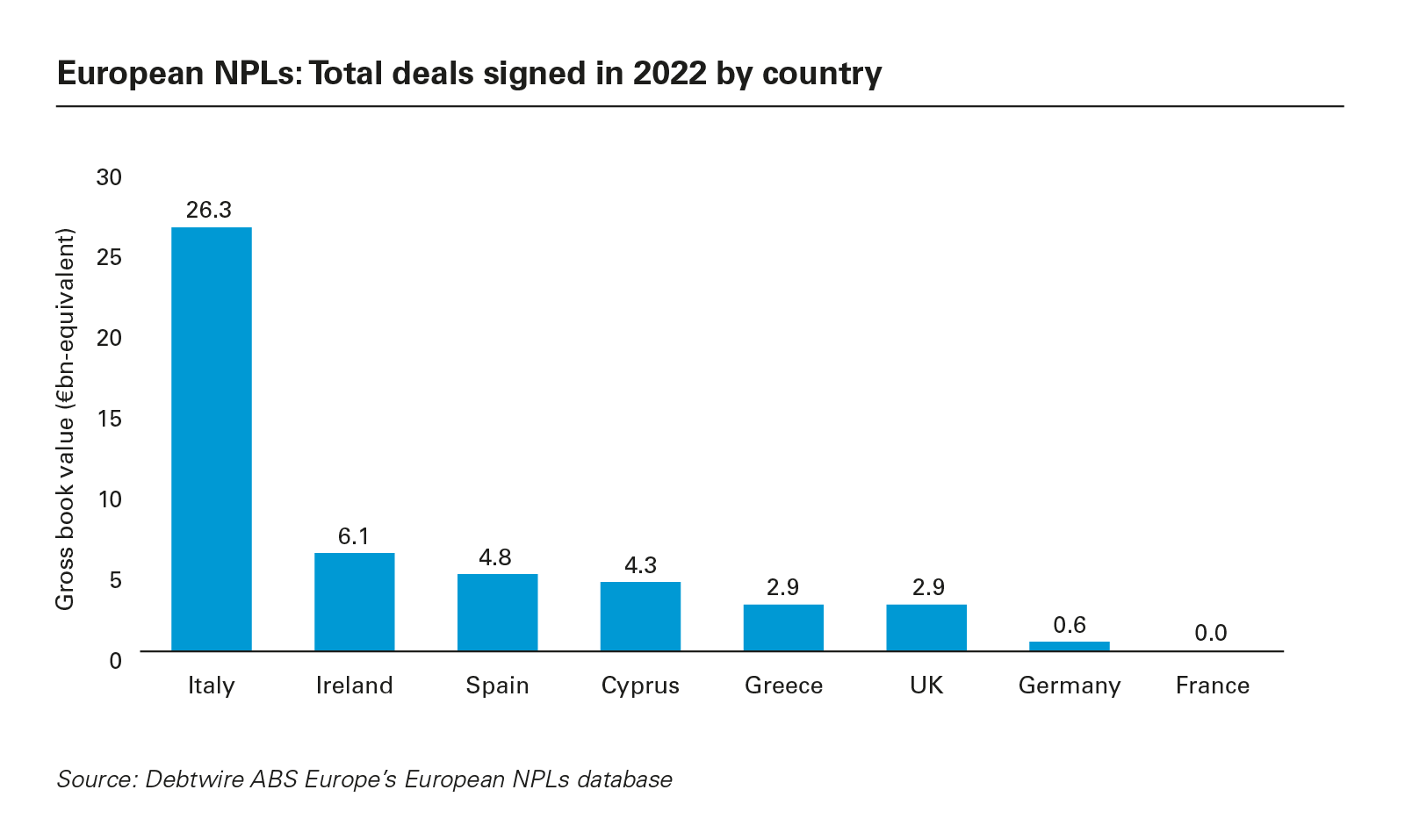

With NPL levels across Europe continuing to fall, the imperative for banks to offload toxic debt has eased. NPL sales fell sharply across much of the continent in 2022, with only Italian banks disposing of more loans than in the preceding 12-month period.

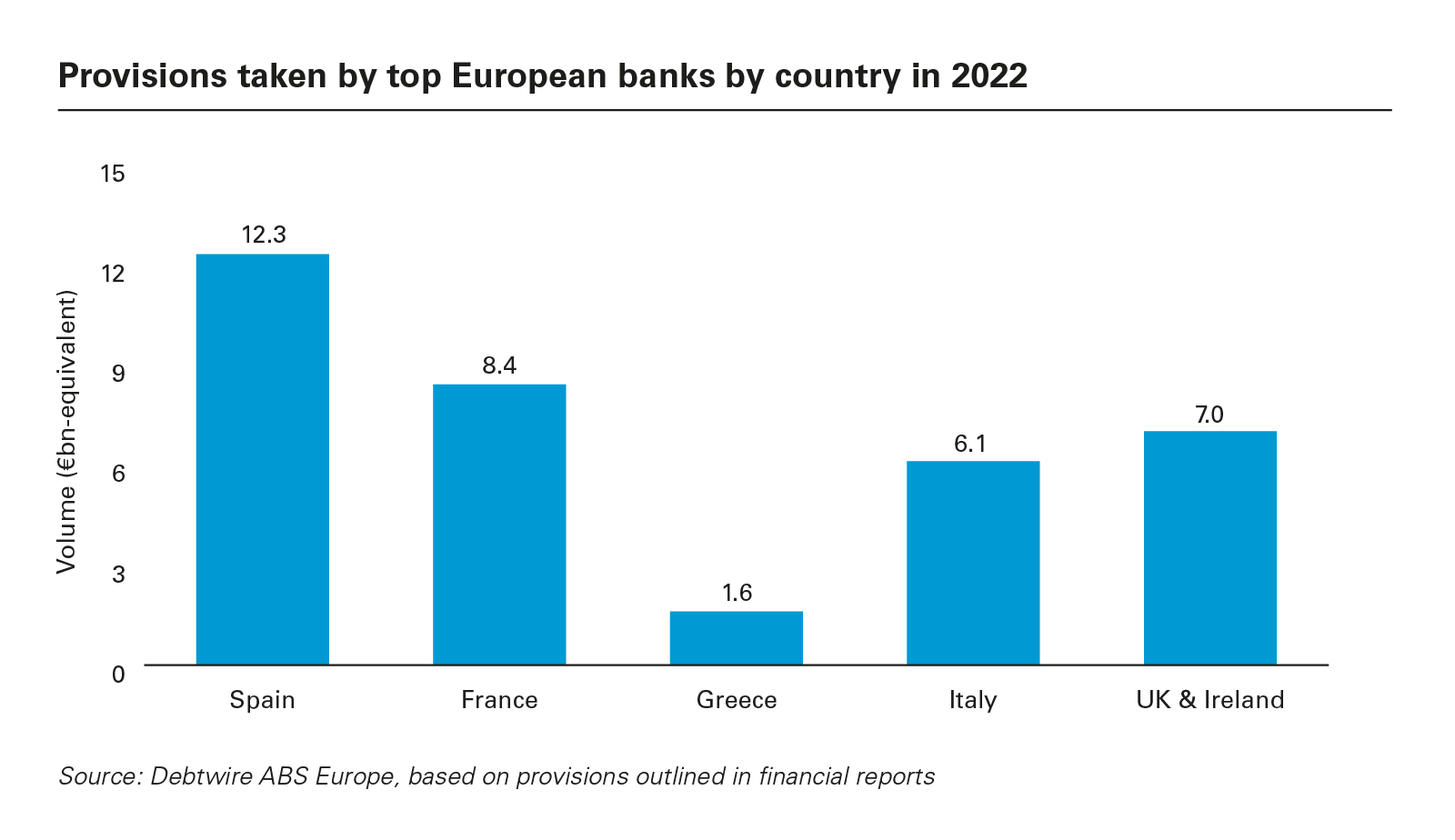

The NPL market looks set to remain flat, particularly now that state-backed securitisation schemes in Italy and Greece have run their course. However, any increase in NPL volumes—perhaps as a result of the cost-of-living crisis and the still-challenged macroeconomic landscape—could presage an increase in activity. In that context, it is notable that banks in much of Europe have increased their provisions compared to 2021.

For now, however, NPLs remain at low levels. The average European Economic Area bank's NPL ratio stood at just 1.8 per cent at end-2022 according to the EBA, unchanged from the previous year.

Italy was the only country in Europe to record a year-to-year increase in NPL sales in 2022.

Italy: Toxic assets offloaded

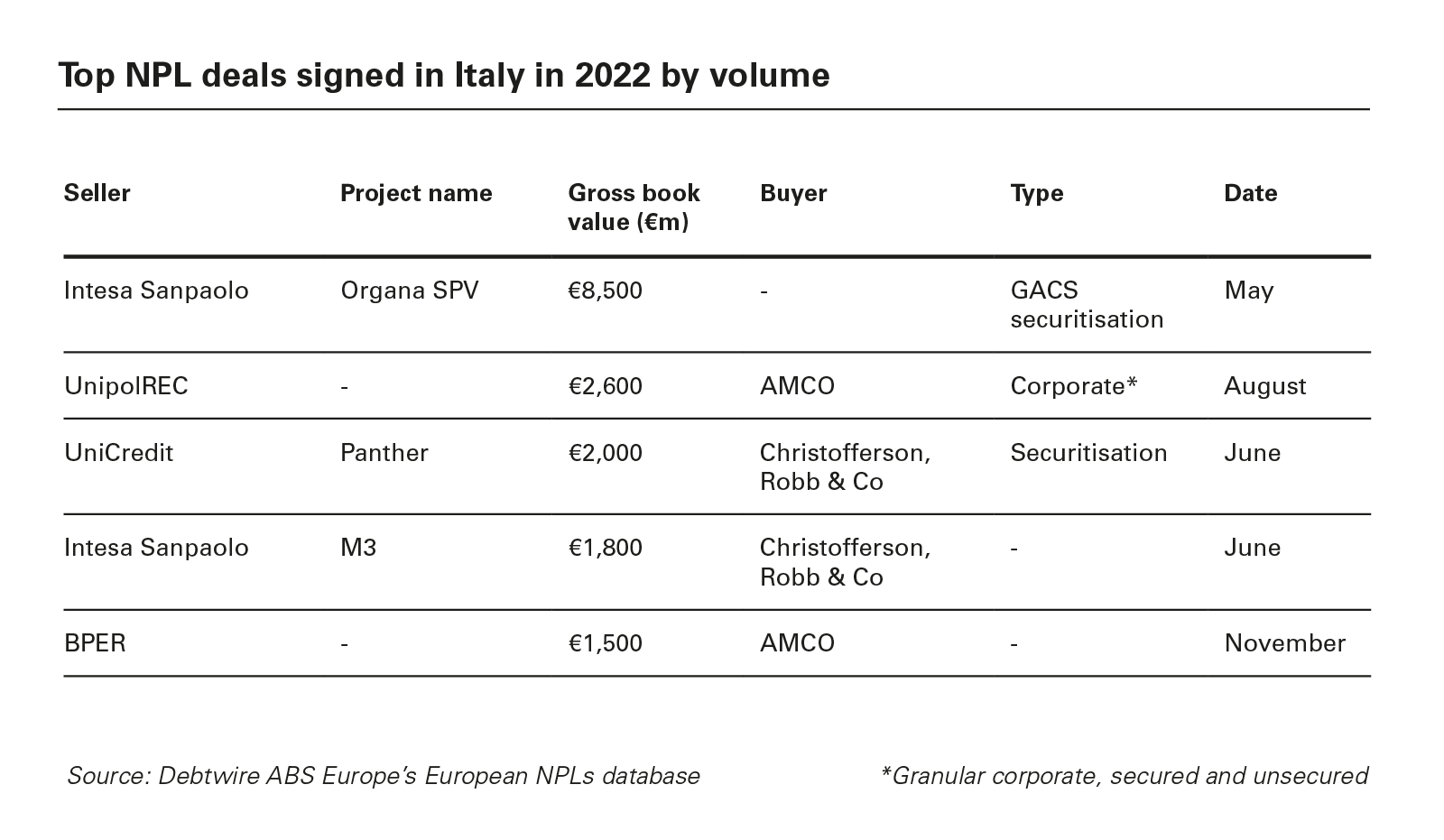

Italy's banks made further reductions to their stock of NPLs over the course of 2022, disposing of more loans than their counterparts in any other European country. NPL sales in Italy totalled just over €26 billion in 2022, up from €19.5 billion the year prior. Indeed, Italy was the only country in Europe to record a year-on-year increase in NPL sales in 2022.

Almost a third of that total came from the largest deal of the year, Intesa Sanpaolo's €8.5 billion securitisation. That transaction was one of the final deals conducted under the state-backed GACS scheme, which came to a close in June 2022. While the Italian government subsequently reached a preliminary agreement with the EU to extend GACS, plans to do so were put on hold.

Nevertheless, the impact of GACS has been substantial. Banks have completed more than 40 securitisations through the scheme over the past five years, offloading more than €100 billion of toxic assets from their collective balance sheets.

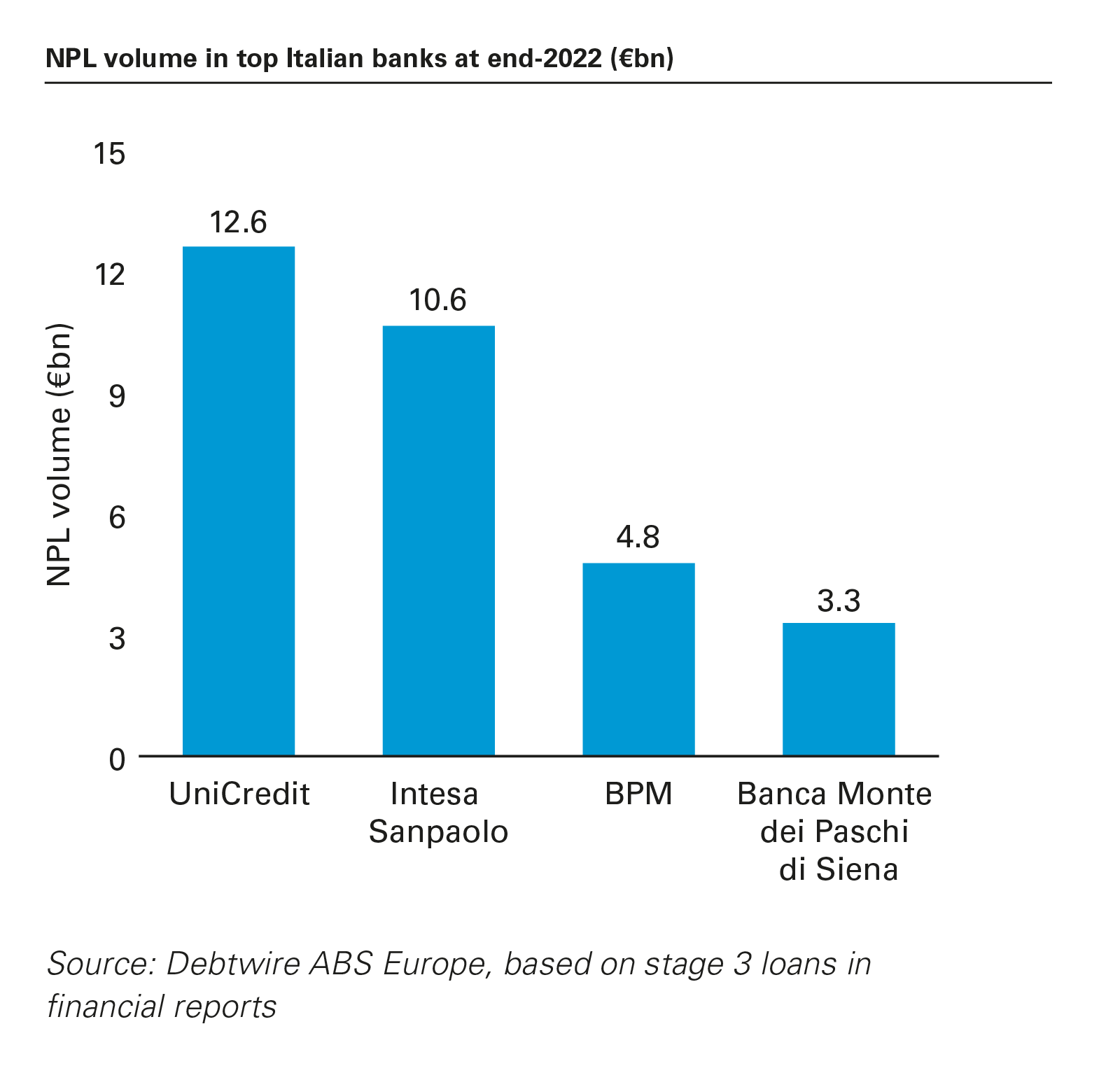

Against that backdrop, and with Italy's NPL ratio down to 2.4 per cent at end-2022 according to the EBA, NPL sales now look set to slow dramatically. Indeed, remaining NPL volumes at leading Italian banks totalled only €31.3 billion by the end of 2022, leaving little room for further substantial disposals.

Instead, Italy's secondary market is beginning to move to centre stage, albeit with much smaller transactions. Some purchasers of NPL portfolios report disappointing collection rates, particularly as they move towards the tail of loans, and are therefore looking to exit. Others are looking to package loans in areas such as real estate to sell to specialist investors.

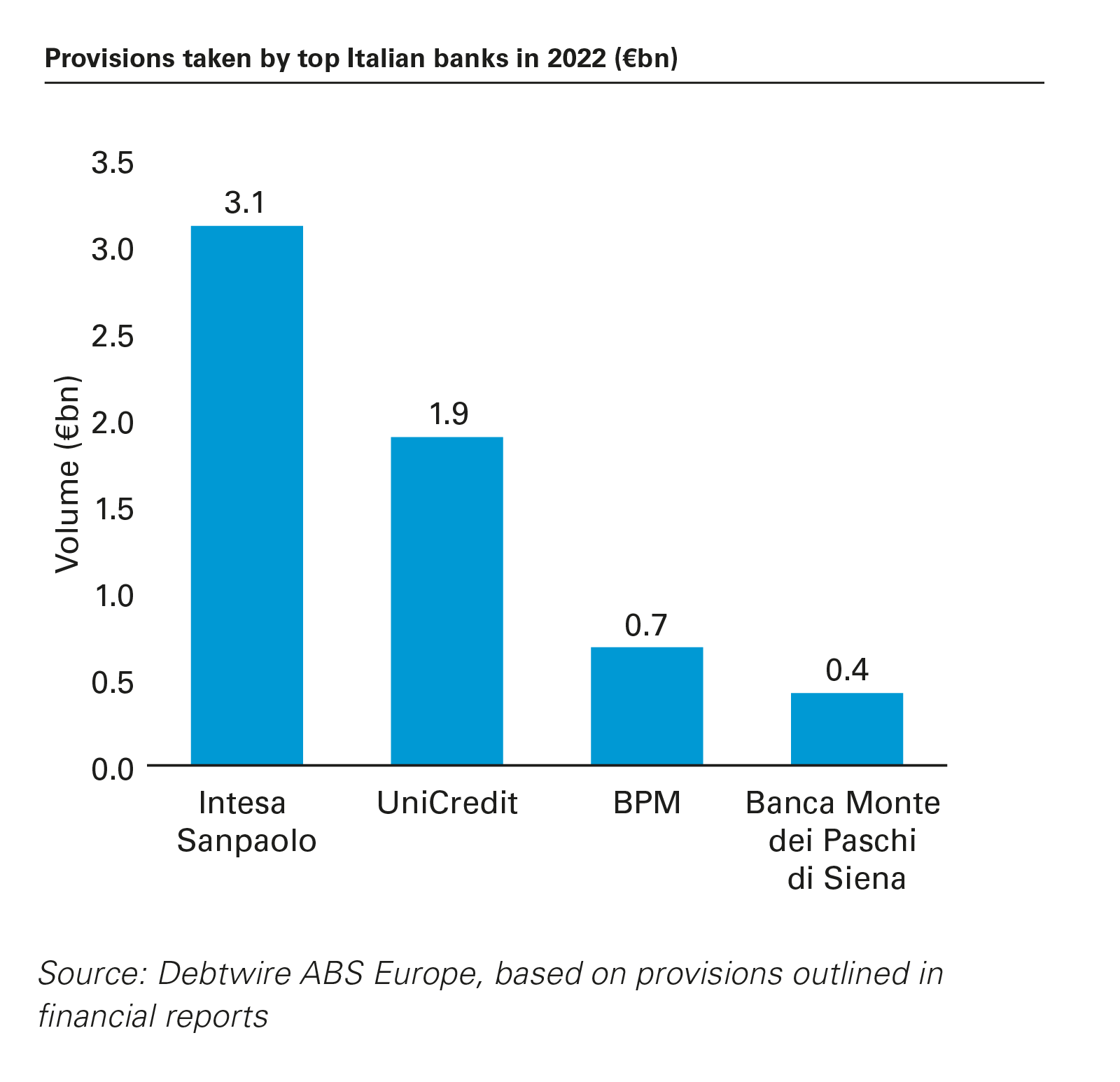

Looking forward, Italy's slowing economy—the IMF is predicting GDP growth of 1.1 per cent for 2023—could see NPLs spike higher once again. Certainly, three of the four biggest banks in the country increased their provisions in 2022 compared to a year prior.

However, while the Italian Banking Association has already asked banks to take a sympathetic approach to customers struggling with debt, there is little sign as yet of a wave of new NPLs. Indeed, stage 2 loan volumes in Italian banks fell by double-digit percentages in 2022.

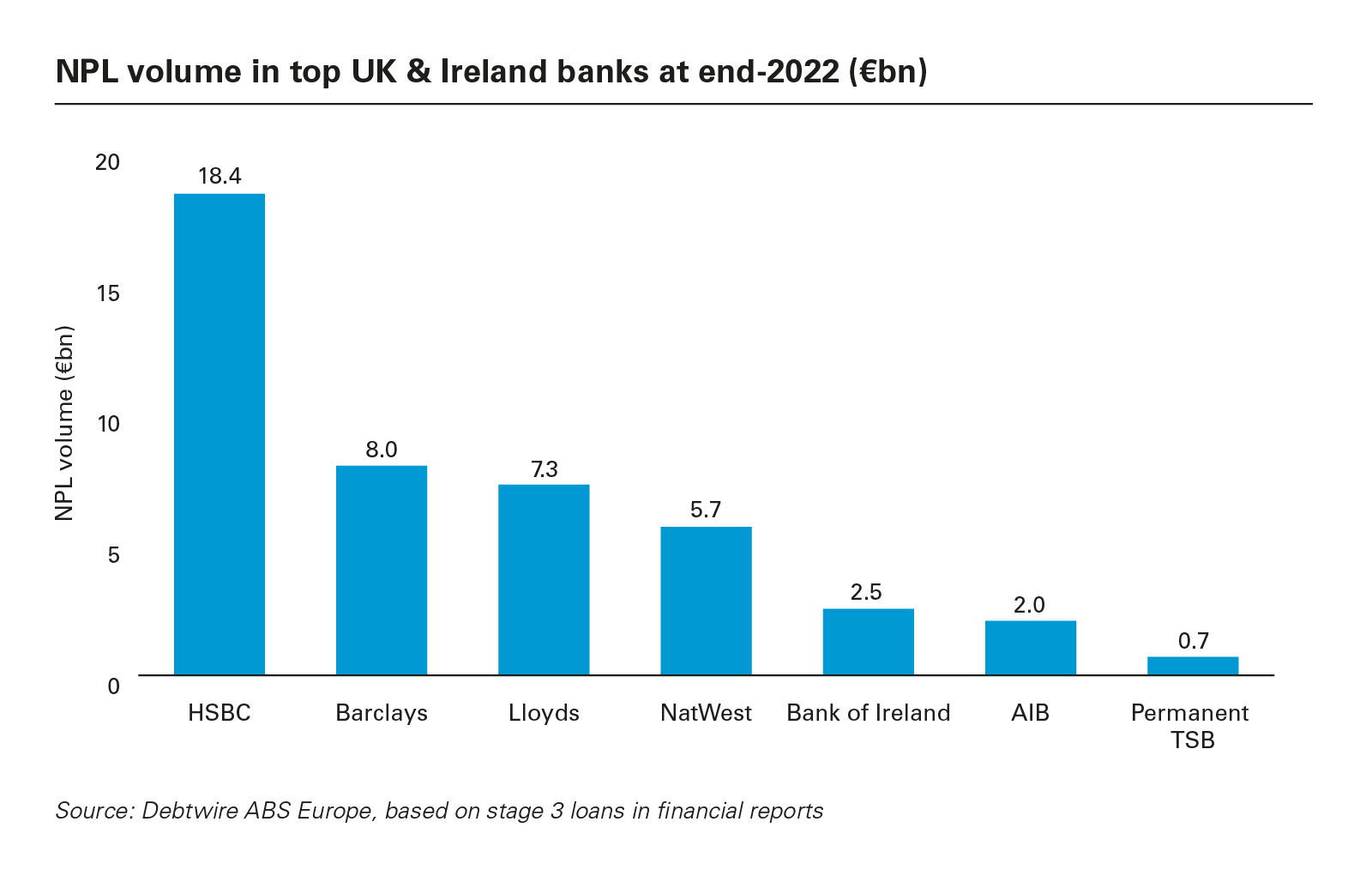

NPL volumes in the UK and Ireland bucked the European trend in 2022, rising slightly to €46 billion by year's end, compared to €44.4 billion at end-2021. That largely reflected higher volumes at two banks, HSBC and Barclays.

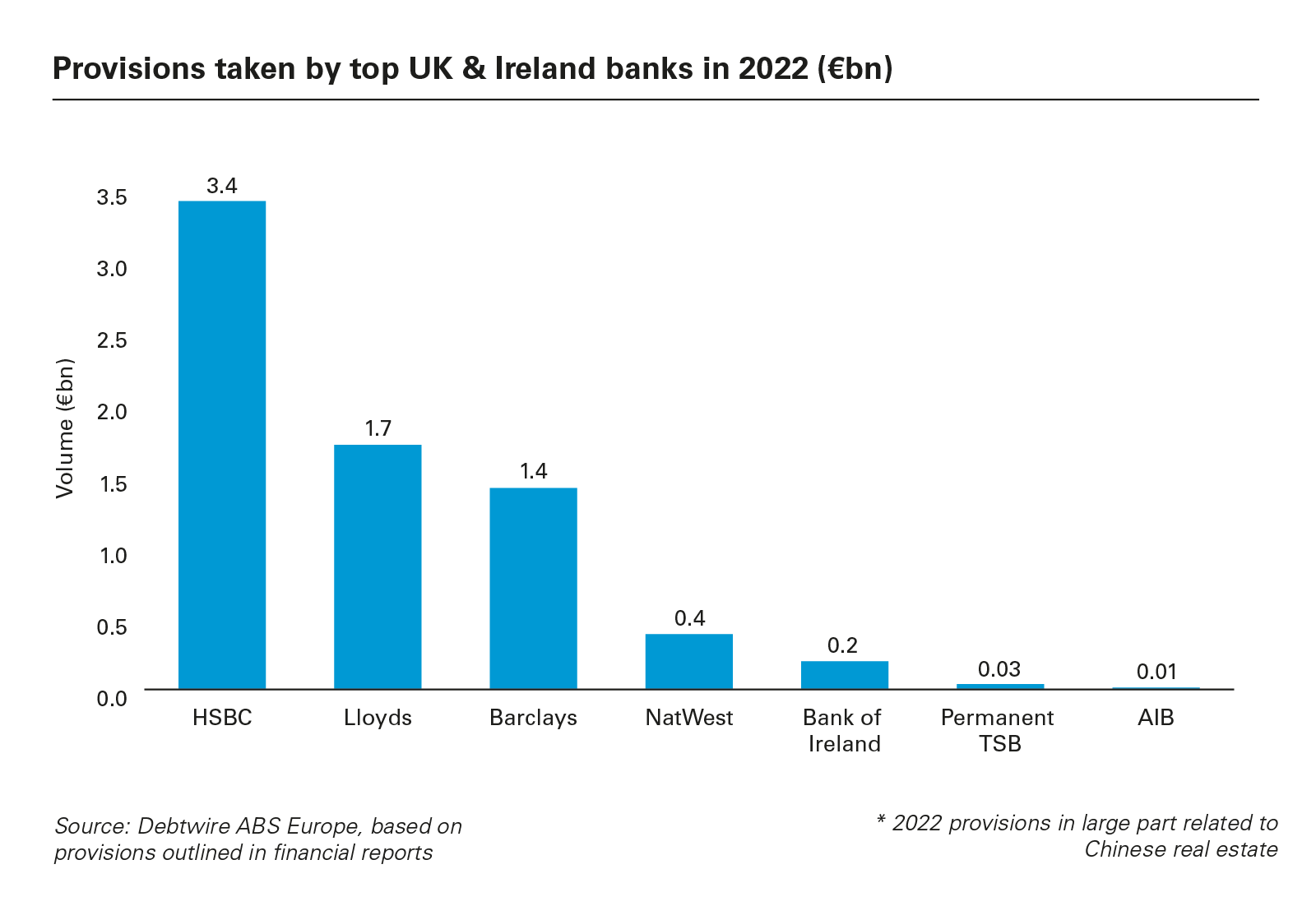

That increase is somewhat surprising in light of IMF analysis that suggests the UK was Europe's fastest-growing major economy in 2022, though the fund also warns that 2023 will see it slow more markedly than any of its rivals. Still, UK banks in particular did record a marked increase in provisions in 2022.

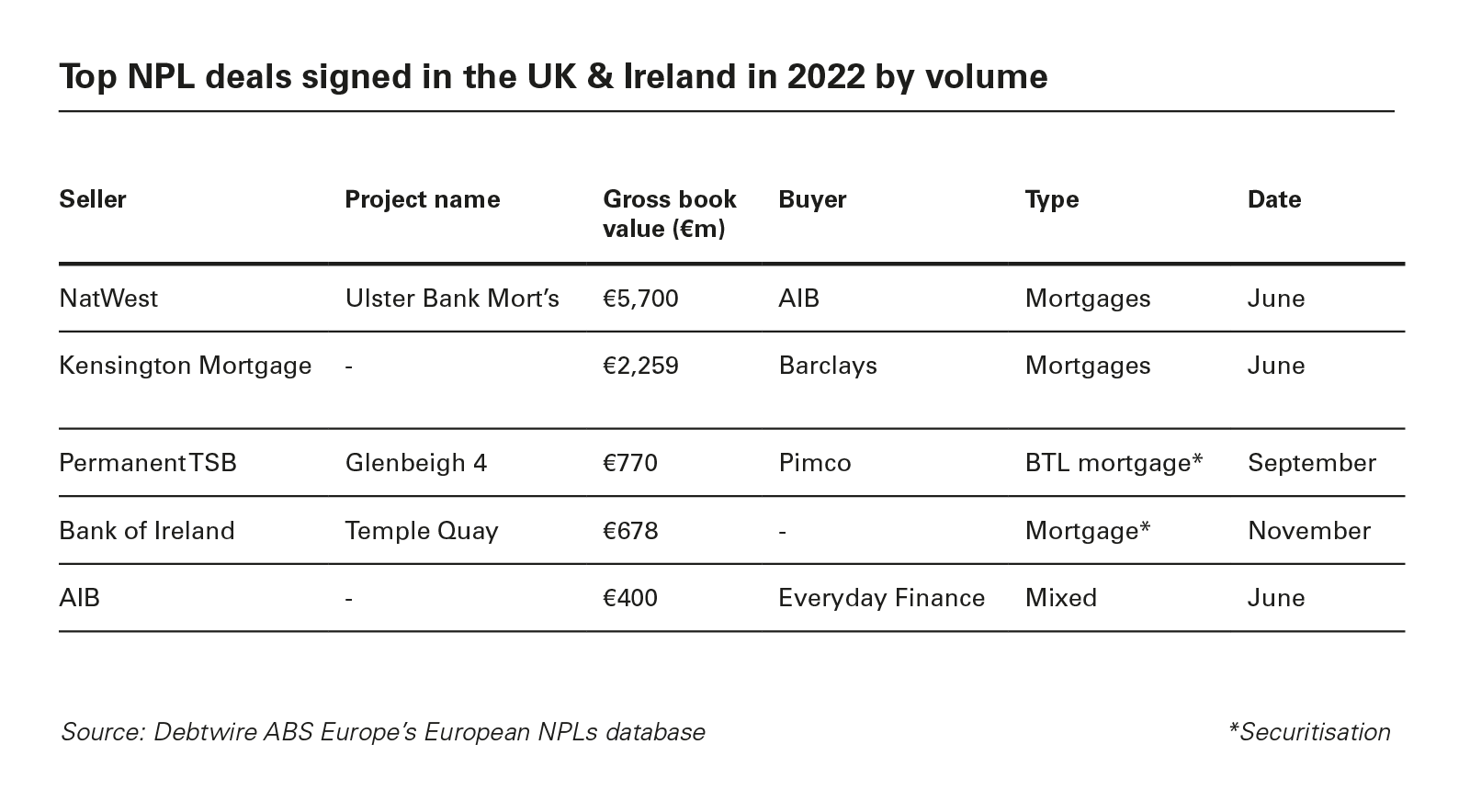

The absence of significant NPL disposals is certainly part of this story, with only five transactions announced by banks in the UK and Ireland in 2022, worth €9 billion in aggregate. While that looks like only a modest decline from the €10 billion of sales recorded in 2021, it is worth noting that more than half of the 2022 total was contributed by a single transaction, the €5.7 billion of NatWest's Ulster Bank NPLs.

Overall, however, NPL exposures look modest. In Ireland, the EBA says the banking sector's NPL ratio fell to 1.8 per cent by the end of 2022, in line with the average across the EU as a whole. In the UK, the comparable figure was 1 per cent, unchanged from a year prior.

Secondary market activity has also been relatively modest, though deals continue to be announced, particularly as PE houses and larger debt servicing companies trade portfolios or individual loans.

Looking forward, the UK's economic difficulties appear particularly pronounced, with core inflation remaining stubbornly high despite more than a year of consecutive interest rate hikes. Capital Economics, the independent think tank, is predicting a surge in business insolvencies over the next 12 to 18 months, potentially hitting a record high by Q2 2024. It will also be important to monitor NPL levels at some of the UK's smaller banks, which are particularly exposed to sectors such as buy-to-let and SME lending.

The Greek market was very quiet in 2022, with banks disposing of just €2.9 billion worth of NPLS.

Greece: Secondary market potential

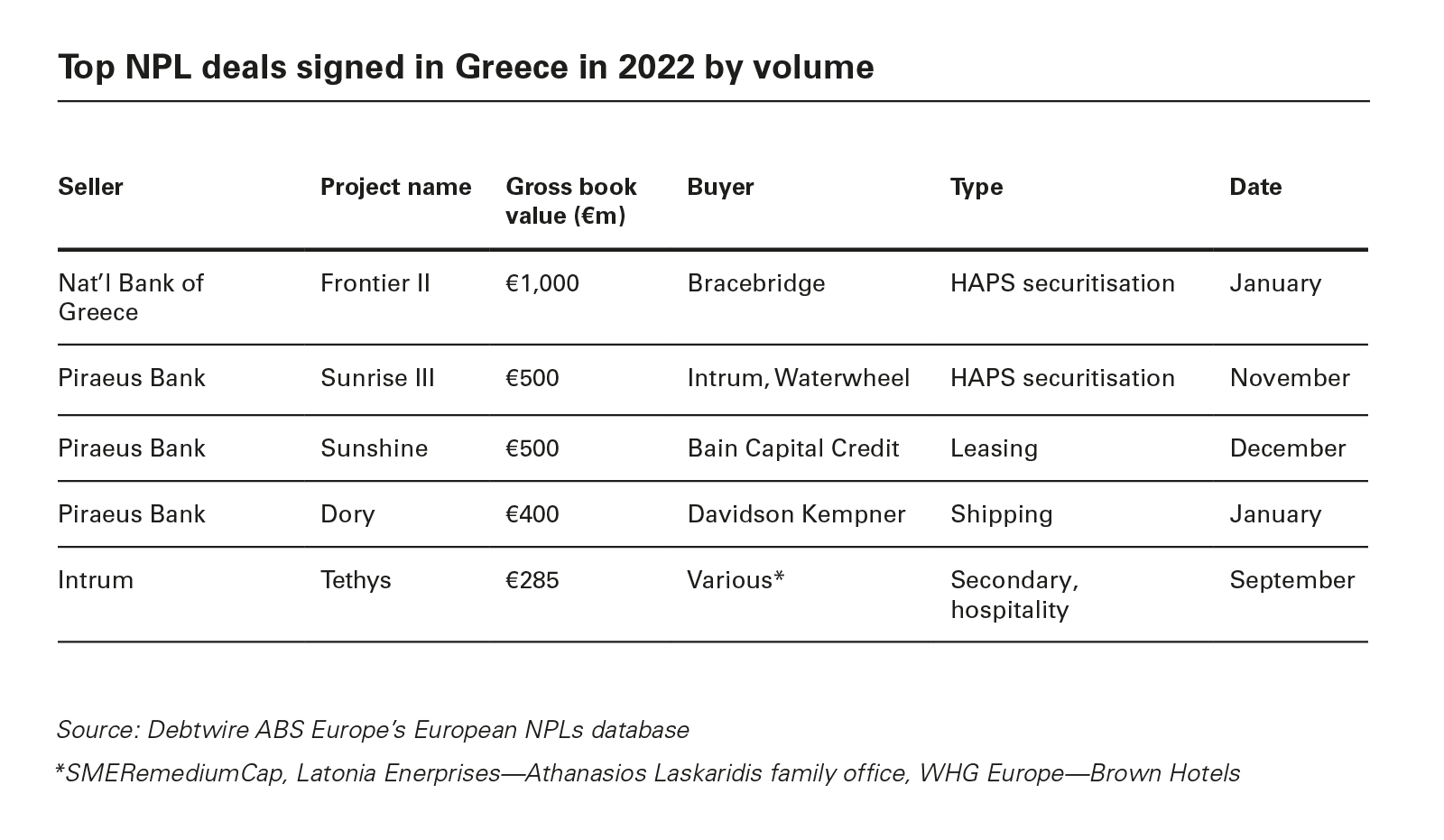

Greece's recovery from financial crisis continues, with the help of the HAPS scheme, which saw the Greek state guarantee senior notes on NPLs while investors took on mezzanine and junior debt and came to an end in October 2022. The Greek government is now discussing the renewal of the HAPS scheme on different terms to the previous programmes (i.e., Hercules I and Hercules II).

The unwinding of HAPS did see a flurry of deals conducted under the scheme over the course of 2022, including the National Bank of Greece's €1 billion Frontier II project, the single largest NPL portfolio sale in the country during the year.

Overall, however, the Greek market was very quiet in 2022, with banks disposing of just €2.9 billion worth of NPLs. That compared with more than €40 billion of transactions in 2021, a year in which Greece saw twice as much NPL deal activity as any other country in Europe.

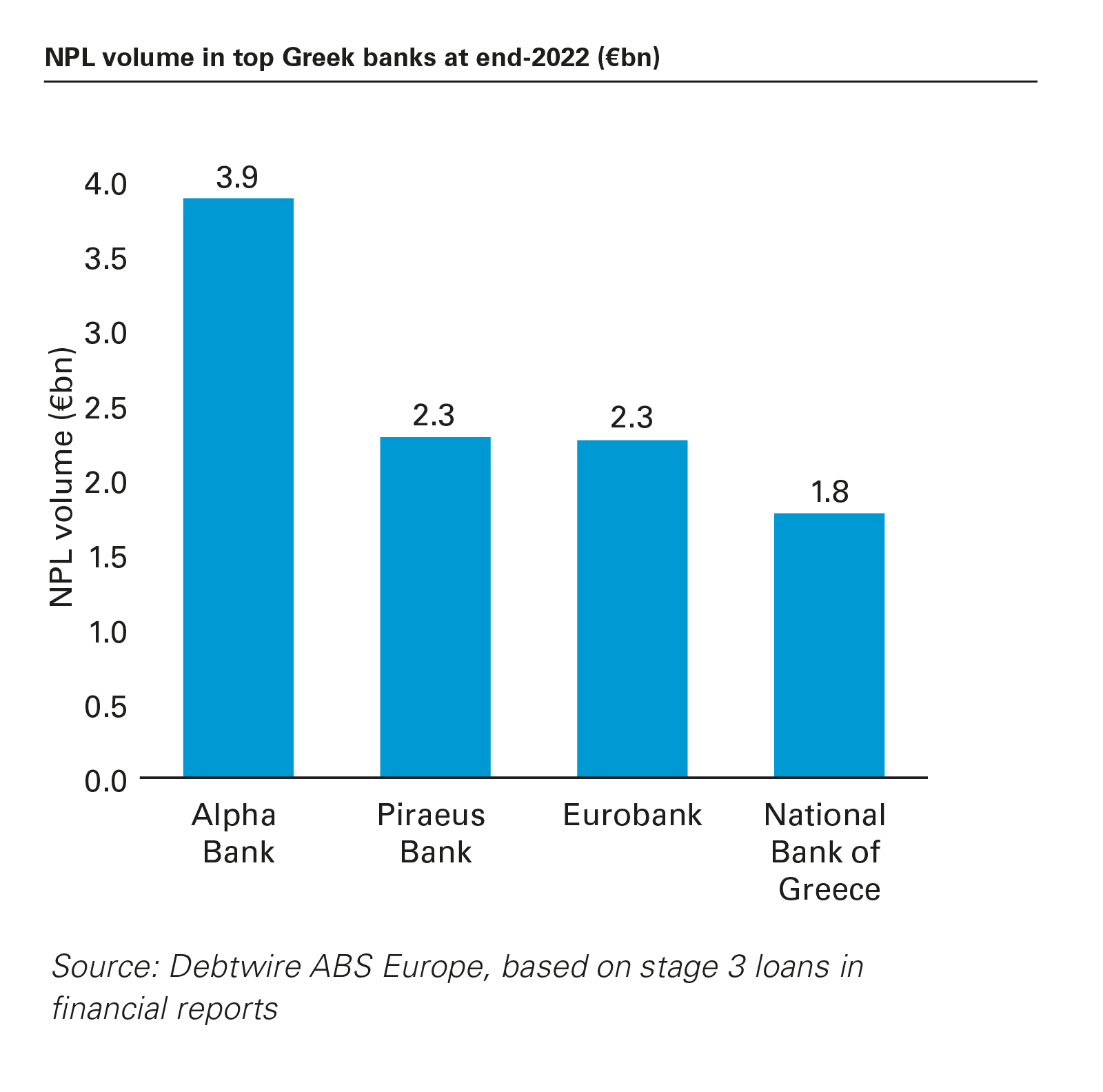

The implication is that the work to right-size Greece's NPL exposure is now more or less complete. NPL volumes at the country's leading banks stood at €10.2 billion at end-2022, down from more than €16 billion a year prior. Alpha Bank and Piraeus Bank have more or less halved their exposure.

There is still some room for improvement—the EBA reported that Greece's NPL ratio stood at 4.6 per cent at end-2022, but that compares favourably to a figure of 7 per cent in December 2021. It is worth remembering that in 2016 the Greek NPL ratio peaked at close to 50 per cent.

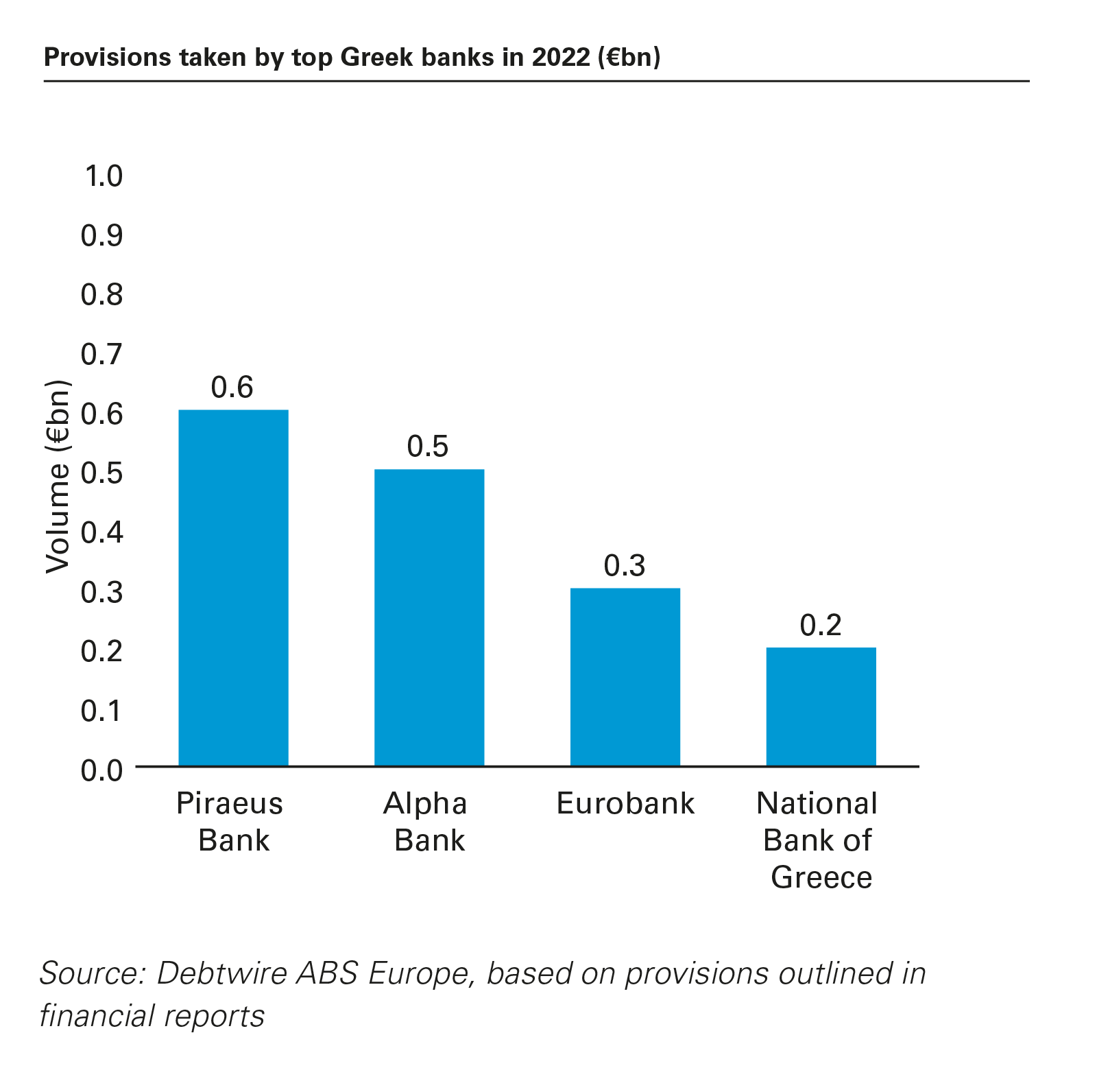

The outlook also feels positive. Greek banks took net provisions of €1.6 billion at the end of 2022, compared to €6.2 billion a year prior.

In that context, NPL deal activity is more likely to be focused on the secondary market going forward, at least in the short term. As investors work through the substantial portfolios acquired over the past few years, there is significant potential for secondary sales, particularly of smaller portfolios or packages of loans. That will include increasing sales of reperforming loans, with Greek borrowers now recovering strongly.

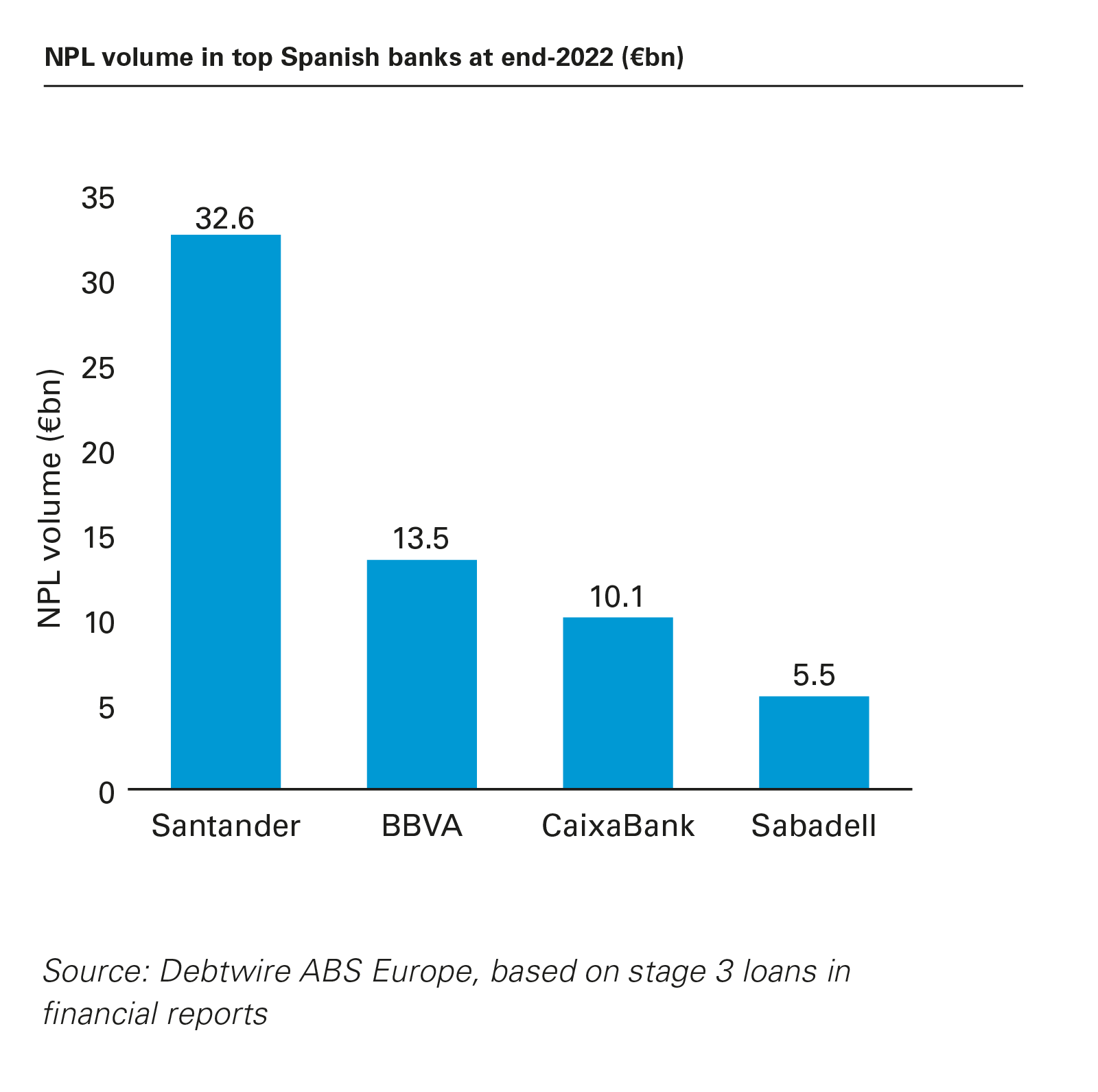

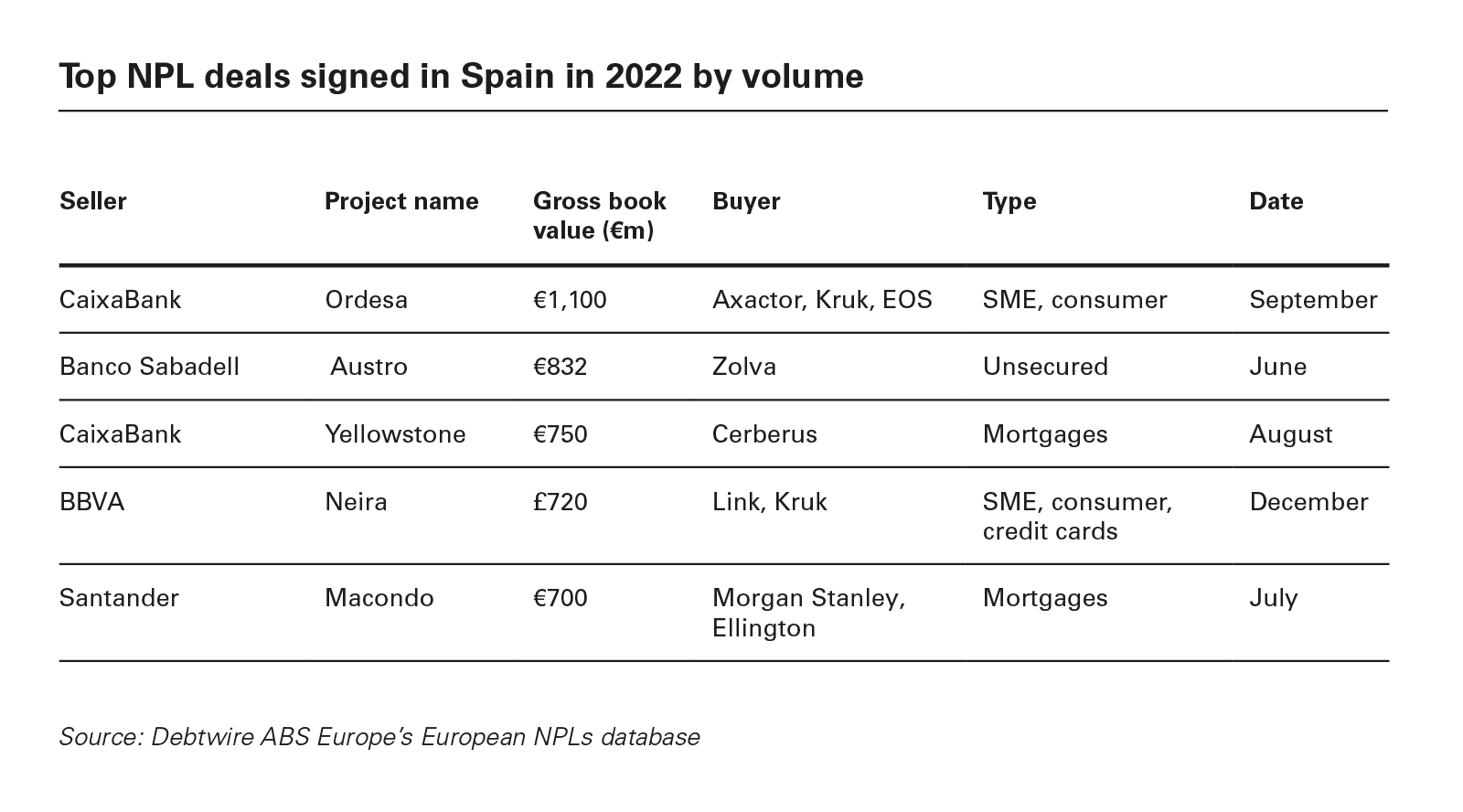

In Spain, NPL volumes at leading banks stood at just under €62 billion at end-2022, down from close to €69 billion a year prior. The decline is partly explained by the fact that Spanish banks disposed of NPLs worth €4.8 billion, though that figure was down from the €7 billion worth of deals seen over the course of 2021.

Two banks dominated proceedings in 2022. Santander completed three disposals worth €1.4 billion combined, and CaixaBank undertook two amounting to €1.85 billion.

Despite these deals, however, Spain still has one of the largest NPL stockpiles in Europe, with only France recording larger totals. The EBA put the average NPL ratio in the Spanish banking sector at 2.8 per cent for end-2022, a modest improvement on the 3 per cent recorded a year prior.

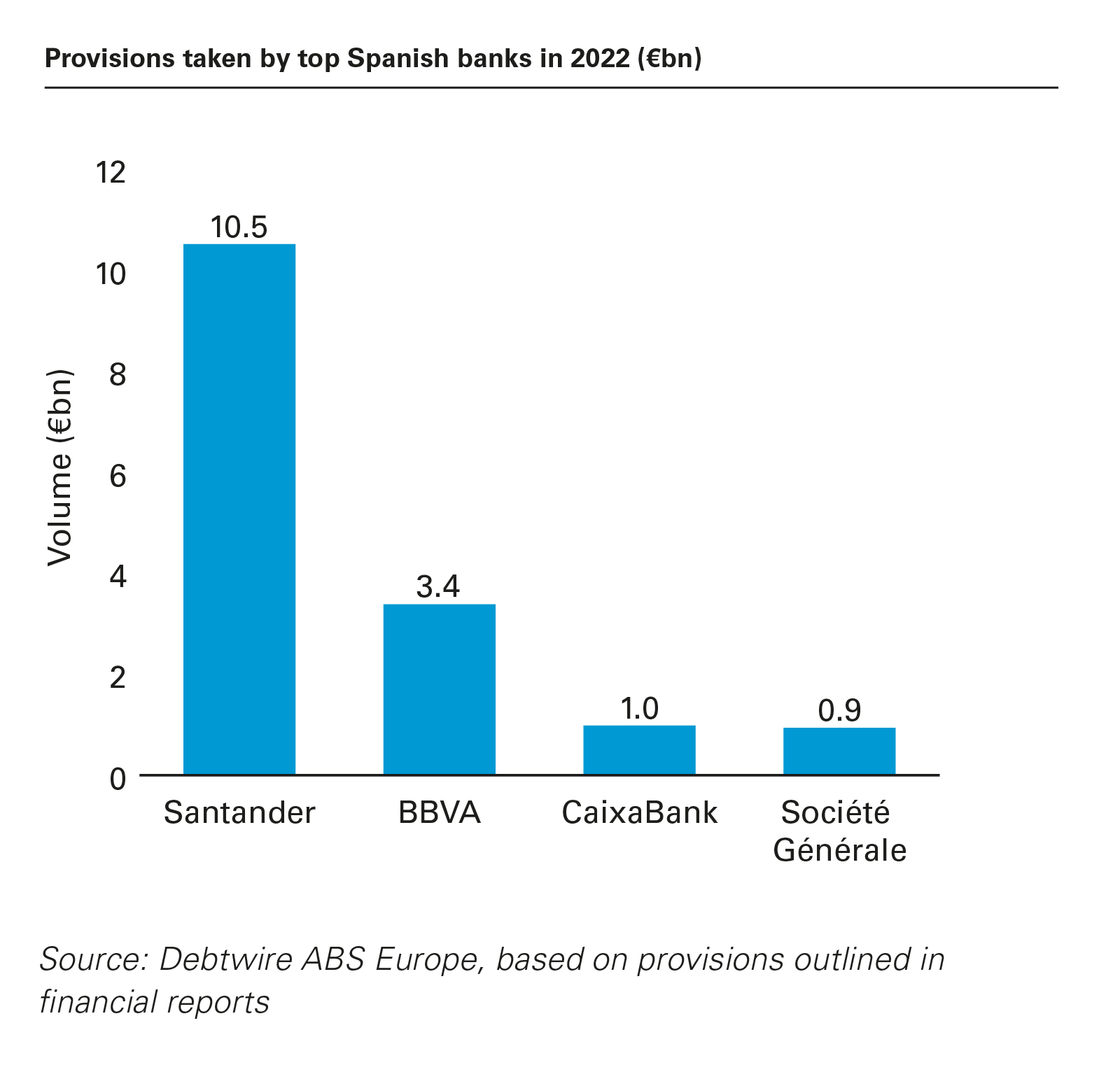

It is also worth noting that Spanish banks are consistently reporting more significant levels of provisions than their peers elsewhere in Europe. At end-2022, provisions at Spain's largest banks totalled €12.3 billion, down only marginally from €12.4 billion figure reported 12 months earlier. That context suggests progress on toxic assets in Spain is slowing, albeit with the country's exposures transformed positively compared to, say, five years ago.

It was reported towards the end of August 2023 that three Spanish banks—CaixaBank, Santander and BBVA—intended to sell a swathe of NPLs worth €1.4 billion in aggregate after the summer. These are composed largely of residential NPLs, with those that BBVA and Santander intend to sell each possessing reported gross book values of at least €400 million, while the portfolio that CaixaBank is looking to move has an unpaid principal balance of €485 million. Disposals such as these will certainly help to keep Spain's average NPL ratio at a modest level.

There is potential, too, for further activity in the secondary market, particularly in sectors such as hotels and leisure, where specialist investors are circling. Reforms to Spain's pre-insolvency regulation, widely perceived as supportive of creditors, as well as plans to streamline the country's insolvency processes, also provide incentives for secondary buyers to focus on the Spanish NPL market.

Still, at a macro level, there are concerns about Spanish economic performance over the course of 2023. The IMF expects GDP growth of 1.1 per cent for the year—down from an estimated 5.2 per cent in 2022—though it points to resilience in the tourism sector as one potential point of optimism.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European NPLs:Total deals signed in 2022 by country (PDF)

View full image: European NPLs:Total deals signed in 2022 by country (PDF)

View full image: Provisions taken by top European banks by country in 2022 (PDF)

View full image: Provisions taken by top European banks by country in 2022 (PDF)

View full image: NPL volume in top Italian banks at end-2022 (€bn) (PDF)

View full image: NPL volume in top Italian banks at end-2022 (€bn) (PDF)

View full image: Provisions taken by top Italian banks in 2022 (€bn) (PDF)

View full image: Provisions taken by top Italian banks in 2022 (€bn) (PDF)

View full image: Top NPL deals signed in Italy in 2022 by volume (PDF)

View full image: Top NPL deals signed in Italy in 2022 by volume (PDF)

View full image: NPL volume in top UK & Ireland banks at end-2022 (€bn) (PDF)

View full image: NPL volume in top UK & Ireland banks at end-2022 (€bn) (PDF)

View full image: Provisions taken by top UK & Ireland banks in 2022 (€bn) (PDF)

View full image: Provisions taken by top UK & Ireland banks in 2022 (€bn) (PDF)

View full image: Top NPL deals signed in the UK & Ireland in 2022 by volume (PDF)

View full image: Top NPL deals signed in the UK & Ireland in 2022 by volume (PDF)

View full image: NPL volume in top Greek banks at end-2022 (€bn) (PDF)

View full image: NPL volume in top Greek banks at end-2022 (€bn) (PDF)

View full image: Provisions taken by top Greek banks in 2022 (€bn) (PDF)

View full image: Provisions taken by top Greek banks in 2022 (€bn) (PDF)

View full image: Top NPL deals signed in Greece in 2022 by volume (PDF)

View full image: Top NPL deals signed in Greece in 2022 by volume (PDF)

View full image: NPL volume in top Spanish banks at end-2022 (€bn) (PDF)

View full image: NPL volume in top Spanish banks at end-2022 (€bn) (PDF)

View full image: Provisions taken by top Spanish banks in 2022 (€bn) (PDF)

View full image: Provisions taken by top Spanish banks in 2022 (€bn) (PDF)

View full image: Top NPL deals signed in Spain in 2022 by volume (PDF)

View full image: Top NPL deals signed in Spain in 2022 by volume (PDF)