Germany

The COVID-19 pandemic has not had a significant impact on the work of the Federal Cartel Office (FCO). For 2021 and going forward, the 10th amendment of the ARC that just came into force will bring the most substantial overhaul of competition law in a long time.

29 min read

Subscribe

Stay current on your favorite topics

Key developments

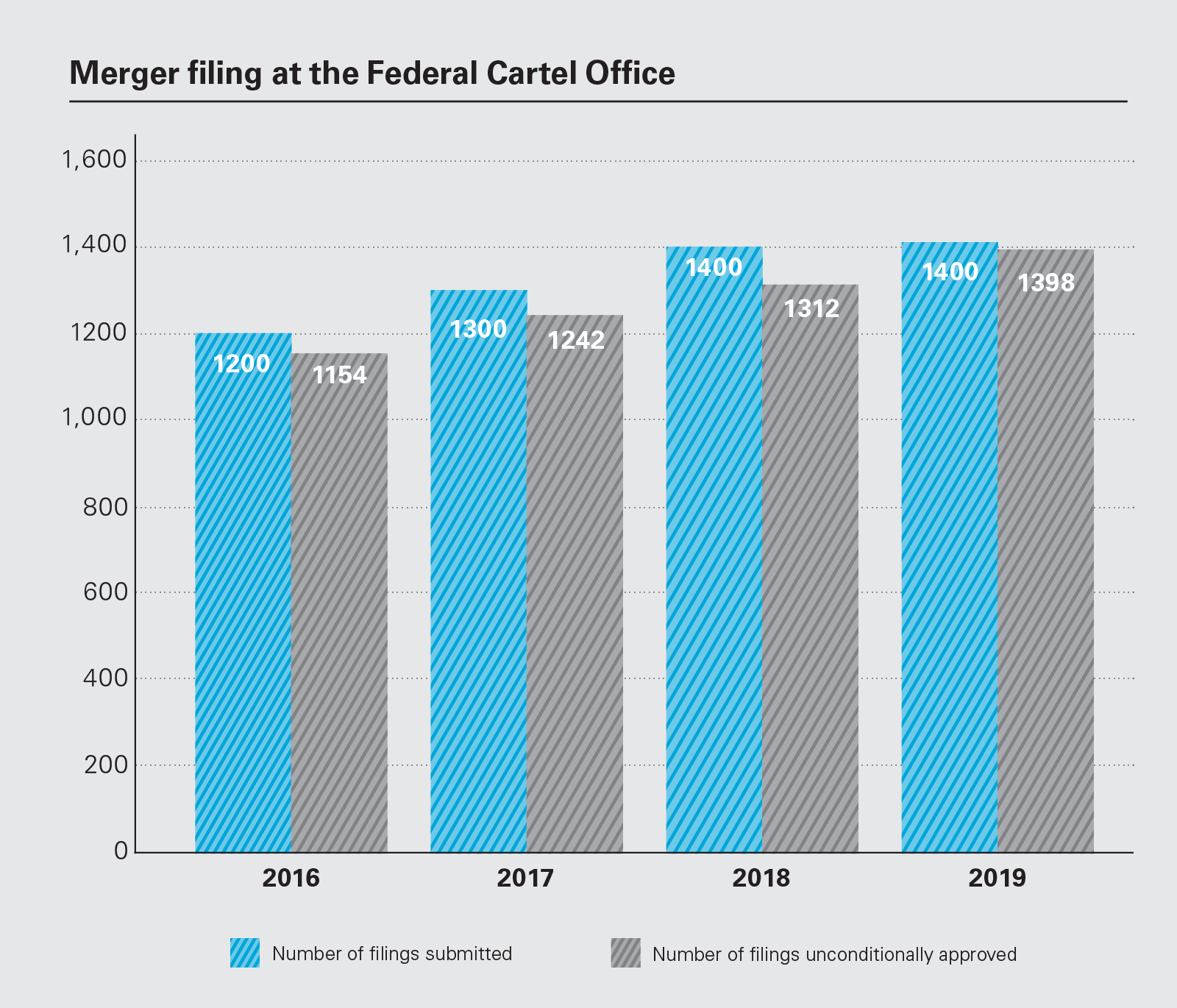

The Federal Cartel Office (FCO) reviewed approximately 1,200 transactions in 2020 – slightly less than in 2019 (approximately 1,400 transactions) – and entered into in-depth or Phase II investigations in only 8 cases (14 in 2019).

4

The FCO blocked four transactions in 2019 ; no transaction blocked in 2020

The year saw less interventions than the previous year. In 2020, the FCO did not block any transaction. In two cases, the parties withdrew their filing in Phase II based on the FCO's objections and abandoned the transaction; four cases were cleared without remedies after a Phase II review.

In 2019, there were six withdrawals, and four transactions were blocked.

Prohibitions/Withdrawals

In 2019/2020, the FCO reviewed a number of "three-to-two" mergers, one of which was withdrawn in early 2020, and another prohibited in late 2019. In February 2020, the FCO raised objections to a deal based on a noteworthy distinction between branded and private label personal care goods. Edgewell Personal Care Company's planned acquisition of Harry's Inc. was abandoned after the FCO expressed concerns that the merger would impede competition on the national market for private-label wet-shaving razors.

The review of a competitor cooperation can raise questions under the cartel prohibition clauses of the ARC: They cannot be reviewed as part of merger control proceedings, so it is common practice to review such questions in parallel but separate proceedings

The US Federal Trade Commission had also raised concerns about the merger of the two US-based companies. Edgewell sells its shaving products under the Wilkinson Sword brand and as private-label products to retailers, which resell them under their own brands. Harry's traditionally manufactured and sold wet-shaving private-label products, but recently established and expanded the sale of branded products.

While from a customer perspective, private-label and branded goods may well be interchangeable, the FCO's preliminary view was that there is a separate market for private-label products due to significant differences in the market characteristics, including distribution channels, availability, procurement factors and prices.

The FCO found that the parties' combined market share for private label wet-shaving products would have significantly exceeded 40 percent, exceeding the statutory dominance presumption threshold.

With only one other major competitor left, the FCO was concerned that this merger would have likely created both unilateral and coordinated effects. It also said that the statutory presumption for collective dominance was met, since the merging parties were close competitors, and the number of significant competitors left was limited.

In December 2019, the FCO reviewed—and ultimately prohibited— another three-to-two merger. The deal concerned the provision of cash for business and banks. Sweden's Loomis, a company providing cash-handling services in northern and western Germany, planned to acquire Ziemann Sicherheit Holding, the second-largest cash-handling services provider in Germany.

According to the FCO, Loomis's acquisition would have been part of a continuous consolidation process in the market. The FCO found that Prosegur was the only other relevant competitor active in many highly concentrated regional markets that the merger would have affected, and the merged company and Prosegur would have had a combined market share of between 60 percent and more than 85 percent in these regions.

The FCO was concerned that the transaction would have likely created unilateral effects. It said the company would have had strong incentives post-merger to increase prices or otherwise adversely change business terms, especially because there were considerable price increases even before the transaction.

8

In 2020, the Federal Cartel Office (FCO) entered into in-depth or Phase II investigations in only 8 cases

In July 2019, the FCO blocked the proposed acquisition by Remondis, Germany's largest waste disposal company, of Duales System Holding (DSD), active in the collection and recycling of packing waste. According to the FCO, the vertical integration of the companies would have impeded DSD's competitors both downstream and upstream.

The merger would also have paved the way for competitor foreclosure towards competing waste disposal companies, resulting in additional price increases for DSD's competitors. The Düsseldorf Court of Appeal (DCA) rejected Remondis's appeal against the prohibition decision in April 2020.

In March 2019, the FCO continued a series of decisions concerning the petrol station segment. The FCO's objections induced Total Deutschland to abandon its proposed acquisition of 11 petrol stations in the Trier area.

The FCO found that the deal would increase the likelihood of coordinated effects, since the joint dominant position of the leading petrol providers in the region would have been further strengthened.

The FCO works under the presumption that the "big five" mineral oil companies—BP, Jet, ExxonMobil, Total and Shell—form an oligopoly without active competition. Remarkably, according to its case summary, the FCO still considers Esso to be part of the oligopoly, despite the fact that Exxon sold the operation of its Esso gas stations in 2018.

For the affected Trier area, the three largest petrol station operators—BP, Shell and Total—would have jointly had a market share of more than 80 percent post-transaction. Additionally, the FCO also found that the petrol station operators set prices very uniformly, and gas prices in Trier were already way above average.

In 2020 and 2019, the FCO also reviewed an unusually large number of hospital mergers. Two notifications were withdrawn (Cellitinnen Nord/Cellitinnen Süd and Ameos/Sana Kliniken) after the FCO voiced concerns in Phase II proceedings.

Ameos and Sana Kliniken's largest competitor, Schön Klinik, are portfolio companies of investment funds operated and controlled by The Carlyle Group. If the Ameos/Sana Kliniken merger had been implemented, the latter's controlling shareholder would have at least co-controlled all somatic hospitals in the Ostholstein region.

In both cases, the FCO found that the acquisitions would have created or strengthened a dominant position in very narrow regional markets.

In contrast, in August 2020 the FCO cleared the merger of two hospital operators in north Germany, Diakonissenanstalt and Malteser Norddeutschland. The two hospitals operated by the merging parties in Flensburg were to be replaced by a new building and the FCO found that the remaining hospitals in the region had sufficient capacity to maintain competition.

The COVID-19 pandemic has not had a significant impact on the FCO’s work: it kept on with business as usual, adopting a professional and accessible “no-frills” approach towards ongoing and new cases

Between March and June 2020, the FCO also cleared the acquisition of the Malteser Hospital in Bonn by Helios Kliniken, the purchase of Rhön Klinikum by Asklepios Kliniken, and SRH Kliniken's purchase of Klinikum Burgenlandkreis. Another hospital merger in the Allgäu region was cleared in 2019.

In early 2019, another peculiarity of the German merger control regime came into play again after the FCO had blocked a joint venture between Miba and Zollern in the sphere of engine and industrial bearings: the ministerial authorization.

Since the market was already highly concentrated, and the merging parties were the two major suppliers and very close competitors, the FCO found the deal would further reduce competition. However, the German Federal Minister of Economic Affairs overruled the FCO's prohibition by way of a ministerial authorization, despite the fact that the Monopolies Commission (an advisory body to the Federal Government) had issued a recommendation to reject the request.

The Minister found that public interests, such as safeguarding know-how and innovation, outweighed competitive concerns. The decision was unusual as ministerial authorizations typically focus more on public interests other than know-how or innovation, such as preserving jobs.

Surprisingly, Miba and Zollern still applied for an annulment of the FCO's prohibition decision before the DCA, despite their joint venture already having been implemented after the ministerial authorization. The companies claimed that a commitment to invest €50 million into research and development over the next eight years was an undue burden, especially during the pandemic, so they were looking for an unconditional clearance.

The move to challenge the FCO decision despite a ministerial authorization is uncommon, and the DCA dismissed the application in late August 2020. The DCA found that the appeal was inadmissible since the FCO's prohibition decision became groundless after the ministerial authorization, and so there was no "commendable interest" in reviewing it.

Clearances

The FCO has also issued a number of noteworthy conditional clearance decisions. In late 2019, joint venture partners Telekom Deutschland and EWE committed to extensive remedies that could be perceived as market development or even market opening measures.

The two companies are major suppliers of gigabit-ready broadband access in north-west Germany, and the FCO expressed doubts about whether they were willing to make the necessary significant investments in building fiber-optic networks. The two companies committed to building at least 300,000 gigabit-ready broadband connections, which exceeds the number they originally planned to build and that would have been expected had they carried out the development independently.

In addition, Telekom and EWE will have to concentrate on rural areas to build new connections, and to refrain from strategic defense measures towards competitors in order to uphold competition for gigabit technology. The commitments were made not to address an SIEC, but to resolve concerns under Section 1 of the German Act Against Restraints of Competition (ARC), which the FCO carried out in parallel to the merger review.

Such a large package of commitments was crucial for the FCO, although the joint venture covers less than 10 percent of all German households and businesses. The FCO said the clearance could be a potential model for network expansion in other parts of Germany.

It is crucial to have transparent and early communication with the case team about the timing, before formally notifying the merger; the parties can also accelerate the review process by providing extensive information upfront, rather than providing information bit by bit

Another conditional clearance decision related to the cinema sector. In March 2020, the FCO cleared the merger of two major cinema operators in Germany. The acquirer, Vue Nederland, operates cinemas under the CinemaxX brand, while the target companies operate cinemas under the Cinestar brand.

The FCO found that the merger would create a leading cinema operator in Germany in terms of turnover and number of cinemas. Similar to cases in the food retail sector, the FCO assessed narrow regional markets based on the cinemas' actual catchment areas and, in order to clear the merger, the parties committed to divest one cinema in each of the six regions that would otherwise be adversely affected.

Although the merger created a significant position in other regions as well, the FCO found that competition was still guaranteed through large rival cinema operators in those areas. The case is also remarkable due to its extensive review process, which lasted about one year, an extraordinarily long time period for the FCO.

The FCO has also made a number of unconditional clearances, for example in the online dating platform market. While the FCO has suggested that digital and platform cases will have a review and enforcement focus, and they certainly do in behavioral cases, the FCO's merger control enforcement in this area has been limited.

The ProSiebenSat.1 group with platforms Parship and ElitePartner took over control of the Meet Group, which operates several online dating platforms, and is active in the German market with its Lovoo app. Despite the platforms' relatively high market shares, the FCO did not expect any competitive harm, since users still have sufficient alternative dating platforms to choose from, are often using several different platforms at once, and there are only low barriers for market entries.

The FCO also cleared the merger between Papyrus Deutschland and Papier Union despite the high combined market shares in the market for printing paper (40 to 45 percent), which exceeded the statutory threshold for a rebuttable single-dominance presumption. This was because their main competitor, Igepa Group, had an even higher market share.

Additionally, multi-sourcing practices, customers' ease of switching suppliers, and spare capacity among competitors led the FCO to find that the single dominance presumption was rebutted. According to the FCO, it could not be assumed with certainty that any unilateral and coordinated effects resulting from the merger would reach the threshold for a prohibition, in particular due to the market structure and the competitive landscape— including new competitive pressure arising from new distribution channels.

After having cleared mergers in the food wholesale sector, the FCO continued rigorous reviews in the food retail sector. In December 2020, the FCO conditionally cleared Kaufland's acquisition of up to 92 Real stores from SCP Retail, a Russian investment company, which had acquired all of the approximately 270 Real stores from Metro. Kaufland had originally notified the acquisition of up to 101 Real stores. At the same time, Globus can acquire up to 24 Real stores from SCP.

The European Commission had referred the case to the FCO. Kaufland is part of the Schwarz Group, which is the largest food retailer in Europe. In food retailer concentrations, the FCO traditionally focuses on buyer power. In particular, the FCO found that the transaction would have expanded the Schwarz Group's distribution network significantly and increased Kaufland's sales and procurement volume within a very short time, while the RTG procurement cooperation, of which Real was a significant member at the time, would have lost a large part of its procurement volume. RTG is a significant alternative for manufacturers on the procurement side: Thus SCP committed to sell Real stores with a purchase volume of € 200 million to medium-sized food retailers (including Globus). In the same vein, in March 2021, the FCO only partly cleared the acquisition of Real stores by Edeka. Edeka planned to acquire up to 72 real stores from SCP, but the FCO only cleared the acquisition of 45 stores; Edeka committed not to acquire 21 stores and for six other stores committed to carve out retail space to competitors or to close stores.

Similarly, the FCO conditionally cleared the acquisition of 50 percent of the shares and joint control of Roller and other companies of the Tessner Group by XXXLutz KG in November 2020. The clearance decision was subject to the commitment to sell 23 locations to third parties. Notably, due to the Parties revenues, the transaction was notifiable to the European Commission, but the Parties requested a referral to the FCO. However, as the procurement markets were likely wider than national, the European Commission's referral to the FCO was limited to the furniture retail markets. In late November 2020, the European Commission (unconditionally) cleared the transaction regarding the procurement side. For the retail side, the FCO assessed the transaction with regard to the overall market for the retail of basic furniture products and various sub-segments, such as stationary discount retailing and furniture stores. For the geographic market definition, the FCO relied on its standard practice of identifying "catchment areas" on the basis of post codes (i.e., post codes that relate to customers accounting for c. 90% of the sales) and areas within a radius of 30km around a store.

In December 2020, the FCO cleared Carglass GmbH's acquisition of A.T.U Auto-Teile Unger GmbH's glass business in Phase II. The transaction included a purchase agreement regarding ATU's "controlled business" (i.e, commercial customers with framework agreements and insurance holders with fixed workshop clauses) and a long-term cooperation agreement regarding the "uncontrolled business" (e.g., drive-in customers). Therefore, the FCO assessed the case under merger control law regarding the controlled business and under antitrust law regarding the uncontrolled business. For the controlled business, the parties' combined shares were below the statutory threshold for a rebuttable single-dominance presumption. Also, during the course of the proceeding and upon discussion with the FCO, the parties limited the scope of the cooperation agreement both in terms of content and duration.

In April 2020, the FCO cleared the purchase of Vossloh Locomotives GmbH ("Vossloh") by Chinese stateowned company CRRC Zhuzhou Locomotives Co., Ltd. ("CRRC"). After the German Ministry for Economic Affairs had already granted a certificate of non-objection under the German foreign direct investment rules, the FCO had to deal with two particularities: (i) the foreseeable change of the parties' market shares during the forecast period (which was extended to five to ten years rather than the traditional three to five years), and (ii) particularities associated with the acquisition by a Chinese stateowned company. The FCO found that the historical market share data could not provide a robust picture of the parties' actual market positions in the future. The FCO found, based on the development of Vossloh's market position in recent years that Vossloh's market position was expected to decrease, while CRRC was expected to increase its share. Further, the FCO faced the challenge to assess an acquisition by a Chinese state-owned company, which according to the FCO, is a subject of public debate. In particular, with a view to its pricing strategy, the FCO assessed CRRC's access to financial resources, such as subsidies, which according to the FCO can considerably distort competition. Ultimately, the Bundeskartellamt was not able to issue a robust forecast whether the merger will result in a dominant market position and cleared the deal, since it expected competitors to gain stronger positions despite the risk that CRRC will implement a lowprice strategy. Notably, even though the European Commission's prohibition decision in the Siemens/Alstom case lead to strong voices claiming that Chinese state-owned enterprises should be treated as strongest future competitors due to their access to state funding and subsidies, such concerns were not strong enough for the FCO to block the deal.

Also, in February 2021, the FCO cleared Taiwanese company GlobalWafers's acquisition of German competitor Siltronic unconditionally in Phase I. The Parties are active in the manufacture and supply of silicon wafers, which are an essential input product for the semiconductor industry. They mainly compete against large Japanese competitors ShinEtsu and SUMCO and Korean manufacturer SK Siltron. The FCO found that the parties' combined shares were below the thresholds for the presumption of single dominance (Section 18(4) GWB), but found that pre- and post-Transaction, the thresholds for collective dominance under Section 18(6) GWB were met. However, the FCO ruled out concerns related to unilateral and coordinated effects, inter alia, due to strong countervailing buyer power that the parties face from large semiconductor customers.

Another notable clearance decision in Phase I related to SAP's acquisition of Signavio in February 2021. SAP is a major supplier of enterprise application software (EAS) with a strong position in enterprise resource management software (ERP); Signavio provides B2B software solutions for process management. The parties' products do not overlap and the FCO could also rule out any vertical effects, as their products were mainly complementary. The FCO further assessed whether tying or bundling SAP's ERP with Signavio's process management software could impede effective competition. However, the FCO found that the parties' products were typically not requested as a bundle and Signavio's software did not meet all customer requirements, so it was unlikely for SAP to attempt bundling strategies by preventing customers from using other software.

Also in February 2021, the FCO cleared salesforce.com's acquisition of Slack Technologies Inc. in Phase I. Salesforce offers customer relationship management software, while Slack is active in enterprise collaboration software (such as group messages, document sharing, voice and video calls).

The FCO also cleared transactions that featured interesting procedural questions. In late 2019, the FCO faced a transaction that was only notifiable due to the new "consideration" threshold introduced in the previous ARC amendment. That states that, if the turnover thresholds are not met, a substantial purchase price may still trigger a filing requirement.

The target, Honey Science, mainly operates a browser add-on, which searches for and applies vouchers and rebate offers during online purchase check-outs. Although Honey had 17 million monthly active users, its turnover in Germany was below €5 million and it did not meet German filing thresholds.

Online payment services giant PayPal acquired Honey for approximately €3.6 billion, exceeding the new consideration threshold of €400 million. The FCO found that despite its low domestic turnover, Honey was able to generate a high number of users in Germany. Therefore, its activities were not just marginal (which could have been a factor to exclude a filing obligation under the new threshold). The merger was cleared unconditionally in Phase I.

The FCO also faced the question of whether a minority acquisition establishes a notifiable transaction under the merger control regime and, in particular, whether it confers a "competitively significant influence" over the target, which is a peculiarity of the German merger control regime.

As part of a complex asset and share swap, energy company RWE acquired a minority stake of 16.67 percent in rival E.ON. The merger notified to the FCO was part of a larger transaction, parts of which were assessed by the European Commission.

The FCO found that the minority stake, through which RWE became the largest single shareholder, together with the right to appoint a member of E.ON's supervisory board, led to corporate influence by RWE. This is also competitively significant, because the parties will continue to operate similar businesses, albeit with diverging industry focuses.

In May 2020, the FCO assessed – and did not have objections against – the B2B online platform for the distribution of petroleum products, which is currently in trial operation and operated by a joint venture between OnlineFuels Limited and Shell Deutschland Oil GmbH (the establishment of which was not subject to merger control). The platform shall be used for the short-term spot trade of petroleum products at the wholesale level. The FCO had to assess whether the increase in transparency could be detrimental to competition, but ultimately found that the JV had taken precautions to limit the risk, e.g., as suppliers and customers have to register and set up a user account and the data (prices, quantities, availability, etc.) are mostly displayed on an anonymous basis.

In November 2020, the FCO cleared the Thalia/Osiander merger. Thalia is German's largest stationary book retailer with more than 300 bookstores and an online shop. Osiander is mainly active in southern Germany and operates more than 70 bookstores. Notably, for the product market definition, the FCO did nt limit its assessment to the stationary stores, but also included the online and mail-order business when determining market volumes and shares. The FCO noted that links between online and stationary sales are increasing as, e.g., stationary shops offer clickand- collect services and overnight delivery, while online retailers such as Amazon try to get closer to stationary book experiences with services such as "book sneak peeks". Despite the parties' high combined shares on the retail side, the FCO found that market entry barriers were relatively low and due to the national statutory obligation to sell books at a fixed price, smaller retailer were protected from price competition. The FCO further assessed the purchase side and despite concerns from publishers and book wholesalers, did not find an impediment to effective competition, particularly due to the parties' low combined shares and alternative sales opportunities to other retailers and online shops.

Merger filing at the Federal Cartel Office (PDF)

Merger filing at the Federal Cartel Office (PDF)

Pending Phase II proceedings

The FCO continues its reviews in the waste disposal/recycling sector with currently two pending phase II proceedings related to scrap metal trade.

Appeals

In the market for concert and event tickets, the DCA took an important decision concerning markets involving multi-sided platforms, leading the way for Germany's new rules on the assessment of market power on multisided markets, which entered into force in mid-2017.

CTS Eventim's planned acquisition of Four Artists Booking Agentur GmbH (Four Artists) was squashed by the FCO in 2017, since it would have strengthened the already strong market position of CTS for ticketing services, given that CTS allegedly held a dominant position. Remarkably, the DCA confirmed the FCO decision and underlined that German merger control (still) deviates from EU merger control when it comes to the assessment of whether a transaction leads to a significant impediment of effective competition (SIEC), which is also the substantive test under the EU Merger Regulation: although Four Artists's market share amounted to only 1.5 per cent of all tickets sold in Germany, even such minimal increment of market share is sufficient to establish the strengthening of a dominant position. The DCA made clear that even under the SIEC test, German law does not require a 'significant' strengthening of a dominant position.

In March 2020, the Federal Court of Justice accepted to hear the case concerning the question of whether any de minimis increase of a dominant position fulfils the prohibition criterion of an SIEC under section 36, paragraph 1 of the ARC.

An unusual appeal against a clearance decision by the FCO was still pending at the time of writing, after the DCA upheld EnBW Energie Baden-Wurttemberg's acquisition of a minority shareholding of 6.28 percent in competitor MVV Energie, raising its total stake to 28.76 percent.

The acquisition triggered a notification under the ARC, as acquisitions that bring the buyer's aggregate stake to at least 25 percent are treated as a concentration under German merger control rules (even where the buyer does not obtain control).

MVV challenged the increase before the DCA, trying to get rid of EnBW's blocking minority gained by the transaction. The court, however, in line with previous case law, said MVV was unable to challenge the FCO's unconditional clearance of the deal, since only third parties can be adversely affected by a clearance decision.

According to the DCA, any adverse effects, to the detriment of the parties to the transaction, do not result from the clearance decision itself, but from the private law agreement underlying the transaction. MVV has appealed to the Federal Court of Justice.

Impact on merging parties

The COVID-19 pandemic has not had a significant impact on the FCO's work. Despite the short period when review periods were extended, the FCO kept on with business as usual, adopting a professional and accessible "no-frills" approach toward ongoing and new cases. In particular, the FCO continued to engage in informal pre-filing contacts and applied a flexible approach to help companies hold to their timetable, where possible.

The FCO's general practice is that it does not expect any pre-filing discussions in straightforward cases, while more complex cases can be presented on a draft basis in order to enable substantive discussions with the case team—without starting the clock. When it comes to the timing of FCO proceedings, recent practice has shown a trend to extend Phase II proceedings, in some cases even more than once, leading to a significantly longer total review period than the four to five months German law stipulates.

For example, in the Loomis/Ziemann case, the parties agreed to at least four extensions, leading to a total review period of more than nine months from the notification date to the final decision. Taking into account that the 2020 decision in the CinemaxX/Cinestar case was based on an even longer review period of about one year, this trend is likely to continue in the future.

However, the recent amendments to the ARC aim at addressing these de facto prolonged review periods by extending the review deadlines. Going forward, we believe the DCA's and the Federal Court of Justice's future decisions related to the question of whether any de minimis share increment can fulfill the significant impediment of effective competition (SIEC) test will have a significant impact on the FCO's decisions.

Also, it will be worth keeping an eye on how the European General Court's judgment on the European Commission's 2016 prohibition of the UK merger between Hutchison 3G and Telefonica UK will influence German merger control practice, especially regarding the analysis of the closeness of competition between the parties, whether at least one of them is an important competitive force, and regarding the treatment of efficiencies.

Recent changes in priorities

The FCO is taking cases as they come. It has not been faced with headline end-game mergers, but its decisional practice focuses on narrow and mature markets with high market shares, such as hospitals and retail, as well as platform markets.

Although the FCO said it planned to focus on the technology giants collectively known as GAFA (Google, Amazon, Facebook and Apple), and has issued antitrust decisions against some of them merger control practice in 2020 has not followed this path.

Additionally, although the "new" consideration/transaction value threshold has now been in place for more than three years and was designed to capture critical digital and pharmaceutical mergers that would otherwise fly under the radar, there has not been the expected wave of new cases, let alone interventions.

In particular, the FCO has not reviewed any cases raising substantive concerns that could be reviewed only under this new threshold. The deals captured by the threshold, such as the PayPal/Honey deal, have been cleared without remedies.

Key enforcement trends

A classical remedies case is the CinemaxX/Cinestar case mentioned earlier. By way of a package of regional divestitures, business overlaps have been completely neutralized in geographic markets with both high combined market shares and a significant increment.

The Telekom/EWE joint venture cleared by the FCO in late 2019 is an illustrative example of parallel Article 101, Section 1 ARC, and merger control proceedings. The extensive remedy package the companies committed to will likely affect the FCO's future policy in this sector.

Since the review of a competitor cooperation can also raise questions under the cartel prohibition clauses of the ARC, which cannot be reviewed as part of merger control proceedings, it is common practice to review such questions in parallel but separate proceedings. As the parties' commitments go even further than what they originally planned to do under their cooperation, this appears to be the FCO's way of shaping and opening the market.

The FCO's decision in the PayPal/Honey deal provides helpful clarification with regard to the relatively new consideration value threshold. In particular, the FCO sheds more light on the question of whether and when a target's activities in Germany are only "marginal", which can be a factor in excluding a filing obligation under this threshold.

Finally, the DCA's confirmation in the CTS Eventim/Four Artists deal that even minimal market share increments can be sufficient to strengthen a dominant position will affect the application of the SIEC test under German law, pending the Federal Court of Justice's decision and a possible referral to the European Court of Justice.

Recent studies and guidelines

Apart from the recent 10th amendments to the ARC, no significant changes to German merger control rules are currently expected.

Looking ahead

The FCO takes the view that it is reviewing too many unproblematic cases, but also still misses out on problematic cases below the current thresholds.

The 10th amendment of the ARC that just came into force, and which includes the most substantial overhaul of German competition law in a long time, is trying to square these two contradictory observations.

First, it has increased the domestic turnover thresholds from €25 million to €50 million and €5 million to €17.5 million with the aim of reducing the number of filings significantly. The exemption that transactions do not need to be filed if one of two parties involved has worldwide consolidated revenues of less than €10 million has been eliminated. The additional de minimis market exemption has been extended to markets with a total national sales volume of up to €20 million (whereas the cumulative requirement of relevant products being offered since at least 5 years has remained unchanged).

The FCO, however, has also obtained new powers to review transactions that it could not investigate previously with the socalled 'Remondis' clause. It allows the FCO to capture successive acquisitions of smaller companies. The FCO can order a company to notify all acquisitions in certain sectors (following a previous FCO sector inquiry), provided that the acquirer's worldwide revenues exceed €500 million and its domestic market share exceeds 15% and provided there are objective reasons to be concerned that the acquisition will significantly impede effective competition in Germany in the sector concerned. The duty to notify only applies to transactions where the target company's worldwide revenues exceed €2 million and if at least 66% of the target's worldwide revenues are realized in Germany. While this amendment is most likely based on German waste disposal company Remondis's acquisitions of small regional targets that did not trigger a filing obligation with the FCO, it can also apply to other sectors and enable the FCO to capture deals perceived as potential ‘killer acquisitions'.

The review period has been extended. German law stipulates that Phase I lasts up to one month, and Phase II proceeding shall now be concluded within five months from the filing date. Thus, with the 10th amendment the Phase II review period has been increased by one month. This period is automatically extended by one month in case the parties offer remedies, and the FCO can further extend it multiple times (without any limitation, but only with the parties' consent). Contrary to an original proposal, there will be no limit to the sum of further extensions.

Finally, merger control related wrongdoings, in particular wrong or incomplete filings or non-compliance with FCO's requests for market data, revenues or other information can now be penalized with fines up to one per cent of the annual group turnover (from prior maximum €100,000).

THE INSIDE TRACK

What should a prospective client consider when contemplating a complex, multijurisdictional transaction?

In terms of timing, the basic rule is to do the German notification first, since the FCO generally acts as a "lighthouse" authority, whose decisions pave the way for other regulators. Austria's Federal Cartel Authority in particular agrees with the FCO in many cases.

As to the procedural side, the filing is typically not particularly burdensome. In expected Phase II cases, the procedure is far less tedious than a filing with the European Commission, with less focus on sophisticated economics and limited requests for internal documents. As a downside, pure behavioral remedies are not possible under the German merger regime.

In your experience, what makes a difference in obtaining clearance quickly?

It is crucial to have transparent and early communication with the case team about the timing, before formally notifying the merger. Also, the parties can accelerate the review process by providing extensive information upfront, rather than providing information bit by bit.

What merger control issues did you observe in the past year that surprised you?

Despite public focus on platforms and digital mergers, and the introduction of the new consideration threshold, there was no intensification in these sectors.

On substance, the DCA's decision in CTS Eventim/Four Artists will lead the way for Germany's rules on the assessment of market power on multi-sided markets and the application of the SIEC test.

Finally, on the remedies side, the extensive market opening and development remedies the parties to the Telekom/EWE joint venture committed to will likely affect future deals in this sector.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP