Pivot potential: A deep dive into offshore wind in the Gulf of Mexico

After years of blunted growth and false starts, the US is finally scaling up offshore wind, with the Gulf of Mexico as the potential new setting.

17 min read

After years of blunted growth and false starts, the US is finally scaling up offshore wind. While most progress had been spurred by state policies incenting projects in the Atlantic Ocean off the East Coast, the federal government recently announced the first-ever lease sale in the Gulf of Mexico, historically dotted with oil rigs and conventional energy infrastructure. By capitalizing on regional supply chains, underutilized labor, and robust technical expertise in the domestic oil and gas industry, there may be significant returns in leveraging these competitive advantages and high resource quality for a rapidly growing segment of the domestic energy industry.

Market update: First-ever GoM lease sale announced for August 2023

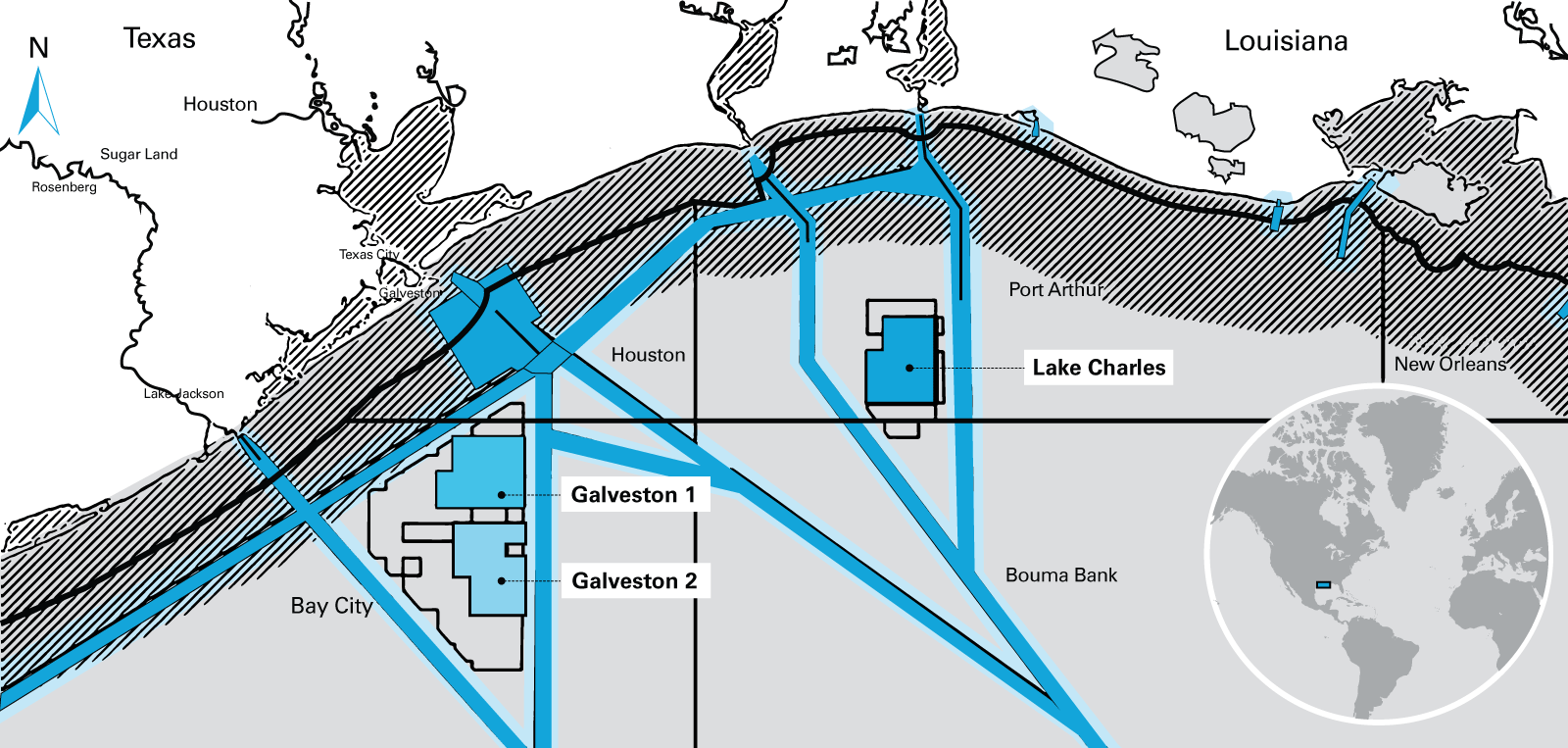

Building on the Final Environmental Assessment issued by the Bureau of Ocean Energy Management (BOEM) on May 26, 2023, the US Department of the Interior (DOI) will auction off commercial wind energy leasing rights for three areas in the GoM: two parcels offshore Galveston, Texas (totaling nearly 200,000 acres) and one parcel offshore Lake Charles, Louisiana (just over 100,000 acres). According to DOI, the auction sites have the potential to generate a total of 3.7 GW from offshore wind.1

In the official lease document published by DOI (the Final Sale Notice),2 a number of new and modified lease stipulations will be incorporated into the GoM auction, largely based on comments submitted to BOEM during the Proposed Sale Notice proceeding initiated in February of 2023. These stipulations may affect corporate strategy and stakeholder engagement for the companies selected in order to receive approval for any proposed project. The new and modified lease stipulations focus on the following issues:

- Tribal engagement and increased reporting requirements: Lessees must furnish semi-annual progress reports to BOEM relating to activities that potentially affect cultural and historical ties to lease areas by Tribes. Additionally, lessees are required to engage in ways that minimize linguistic, technical, cultural, capacity, or other obstacles, and are encouraged to work collaboratively with governments, community leadership and organizations, and Tribes3 and to develop specific frameworks for capacity building.

- Commercial fisheries: Lessees will provide a Fisheries Communication Plan related to anticipated project activities as well as coordinate with commercial and recreational fishing industries and stakeholders during construction and operation in order to minimize localized economic impacts.

- Protected species: Pursuant to section 7(a)(2) of the Endangered Species Act, lessees must coordinate with BOEM, the National Marine Fisheries Service, and the US Fish and Wildlife Service in order to design and conduct biological surveys in order to assess the potential intersection of new offshore wind generation with protected species located in the GoM. Lessees may also be required to obtain an authorization pursuant to section 101(a)(5) of the Marine Mammal Protection Act.

- Project Labor Agreements and supply chains: Lessees will be compelled to make "every reasonable effort" to enter into a Project Labor Agreement for the construction stage of the project. Further, lessees are required to produce an initial statement of goals and recurring progress updates on the achievement of those goals — to be publicly disclosed — on the lessee's plans for contributing to the creation of a robust and resilient domestic offshore wind industry supply chain that would facilitate this or other renewable energy projects permitted by BOEM.

- Research Site Access: This stipulation makes explicit that BOEM, its designated representatives, and certain designees all retain the right to access the leased areas for purposes of further research, without limiting BOEM's authority to access the lease for other purposes as well.

- Archaeological Survey Requirements: Lessees will be required to describe to BOEM in writing the methods they will use to conduct archaeological surveys in support of plans, and to coordinate a Tribal pre-survey meeting with Tribes that have cultural and/or historical ties to the leased areas. Furthermore, in the event of an unanticipated discovery, lessees must immediately halt bottom-disturbing activities within the area of discovery.

- Foreign interests: The US Department of Defense (DoD) requested that lessees provide specific information relating to the personnel to be allowed access the wind turbine structures — and associated data systems — as well as information pertaining to the ownership interests of the facility. Lessees must also preemptively receive clearance from DoD in order to allow access to the project site by foreign representatives of foreign entities of which the DoD has previously raised concerns.

- Committee on Foreign Investment in the United States: In accordance with CFIUS, lessees must be designated as one of the following: (1) a citizen or national of the United States; (2) an alien lawfully admitted for permanent residence in the United States; (3) a private, public, or municipal corporation organized under the laws of any State of the United States, the District of Columbia, or any territory or insular possession subject to U.S. jurisdiction; (4) an association of such citizens, nationals, resident aliens, or corporations; (5) an Executive Agency of the United States; (6) a State of the United States; or (7) a political subdivision of States of the United States. Furthermore, any proposed lessee that is a foreign-controlled business entity must provide joint notice, with BOEM, to CFIUS of the proposed leasing transaction and provide a copy of the notice to DoD. Approval of any assignment of lease interest to a foreign-controlled business entity is also subject to this CFIUS notice stipulation.

- Transmission planning: In tandem with the new provision of project coordination with Tribes and other local stakeholders that may implicate land use concerns, lessees must account for the use of cable corridors, regional transmission systems, meshed systems, or other large-scale transmission facilities and mechanisms as is technically and/or economically feasible.

In the Final Sale Notice, BOEM listed the companies that are legally, technically, and financially qualified to bid on the available lease sites (any entity may only bid for, at most, one of the offered leases at a time and, if successful, can only acquire one lease of the three). As discussed at length in the original piece attached, several of the eligible entities are renewable business units of oil and gas companies. The participation of these entities underscores our view that traditional fossil fuel companies can easily leverage their comparative strength and experience in risk management in new market entry to increasingly position themselves to capture these benefits, and we anticipate continued and increased participation by similar entities in future GoM auctions and opportunities.

The map of the three lease sites is included for reference, per the official BOEM documentation:

View full image (PDF)

View full image (PDF)

For most of the millennium, Europe has outpaced the US in constructing and installing offshore wind projects but the US is now rapidly accelerating its pace in adopting offshore wind

40GWs

The US has pledged to procure a collective 40 gigawatts (GWs) of offshore wind capacity in the Atlantic Ocean by 2040

For most of the millennium, Europe has outpaced the US in constructing and installing offshore wind projects. But the tables are turning: The US has pledged to procure a collective 40 gigawatts (GWs) of offshore wind capacity in the Atlantic Ocean by 2040.

On a shorter timescale, the Biden administration announced a 30 GW offshore wind target by 2030, the first such federal goal for this technology. According to the White House, if the industry reaches the 30 GW target, offshore wind projects could generate upwards of US$12 billion in capital investments annually over the next decade. In the Inflation Reduction Act of 2022, Congress appropriated US$100 million in funds through fiscal year 2031 to the Department of Energy (DOE) for interregional and offshore wind transmission planning, modeling and analysis.

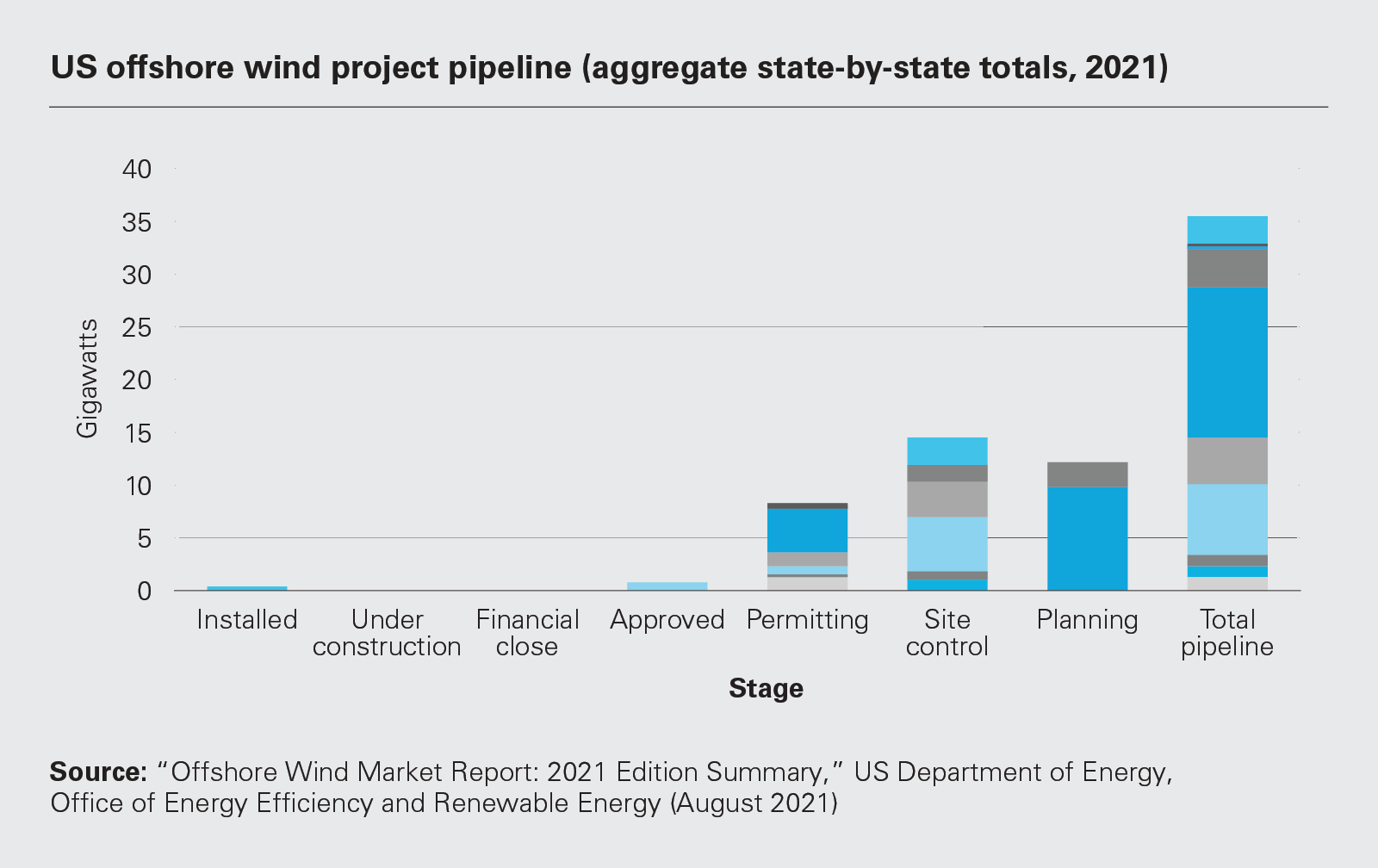

In 2020, the overall US offshore wind pipeline of projects—either proposed or in development—grew by 24 percent year-over-year (from 28.5 GWs in 2020 to 35.3 GWs in 2021). Currently, there are only two operational utility-scale projects, which together comprise 42 megawatts (MWs) (Block Island Wind Farm and Coastal Virginia Offshore Wind), with another 800 MW project (Vineyard Wind I) commencing construction in the near future. The recent approval of the larger project, Vineyard Wind I, should beget insight to both regulators and developers alike, and ensuing proposals will likely hew closer to the 800 MW size of that project rather than the smaller 42 MW size of Block Island and Coastal Virginia.

Nearly 10 GWs of other projects are in phases approaching installation and commercial operation in the near- to medium-term—the "permitting" and "approved" designations.

Technological advancements in platform and turbine engineering should also generate additional revenue-additive opportunities. Deeper foundations can yield more favorable outcomes for projects broadly, as the installation could be placed further out from land—thereby alleviating possible concerns about competition with other ocean industrial activities and reducing visibility from shore for aesthetic reasons. Capacity factors of wind facilities have also increased steadily due to larger blade sizes, taller towers and more optimal placement relative to resource availability.

On a cost basis, offshore wind is competing adeptly with other energy resources. Since 2012, the levelized cost of energy (LCOE) for offshore wind has plummeted by 67 percent. Financial instruments deployed in offshore wind investments across the world have evolved in concert with technology, including competition in international markets and reduced lending rates for project development. In the first half of 2020 alone, firms invested US$35 billion in offshore wind, eclipsing the entire total for 2019 and setting a torrid pace for the industry.

View full image: US offshore wind project pipeline (aggregate state-by-state totals, 2021) (PDF)

View full image: US offshore wind project pipeline (aggregate state-by-state totals, 2021) (PDF)

The GoM enjoys many unique advantages compared to other regions active in offshore wind development —not least of them is its lower labor costs

US$12bn

"The Gulf of Mexico is poised for a wind energy boom. 'The only question is when.'" Tristan Baurick, The Times-Picayune (November 24, 2021) If the US reaches its 30 GW target, offshore wind projects could generate upwards of US$12 billion in capital investments annually over the next decade

Resource quantity & quality

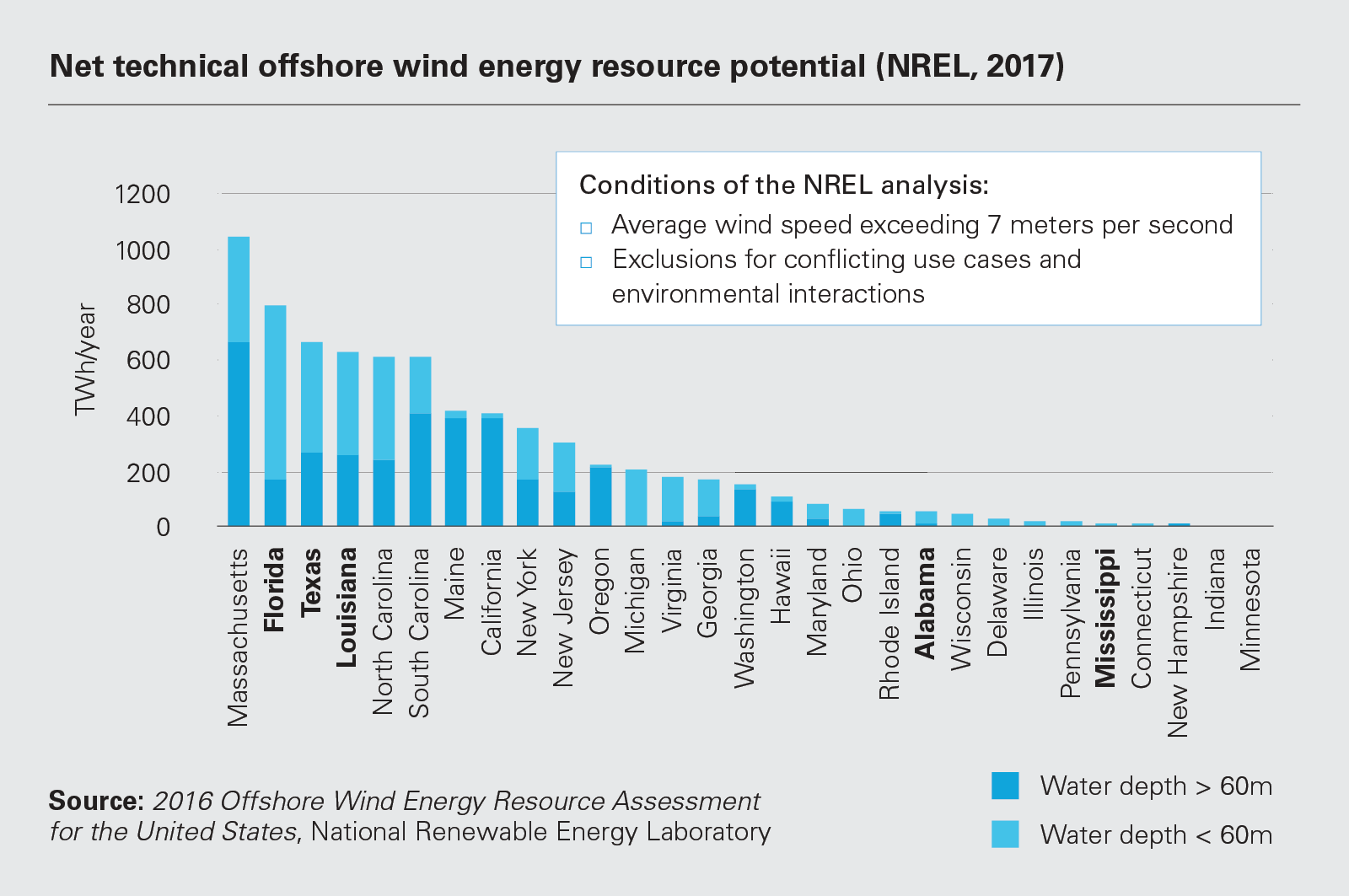

While the US has rapidly accelerated its pace in adopting offshore wind, primarily in the Atlantic Ocean, no projects have yet been proposed or constructed in the Gulf of Mexico (GoM). However, the technical resource potential in the GoM is estimated at 508 GWs.

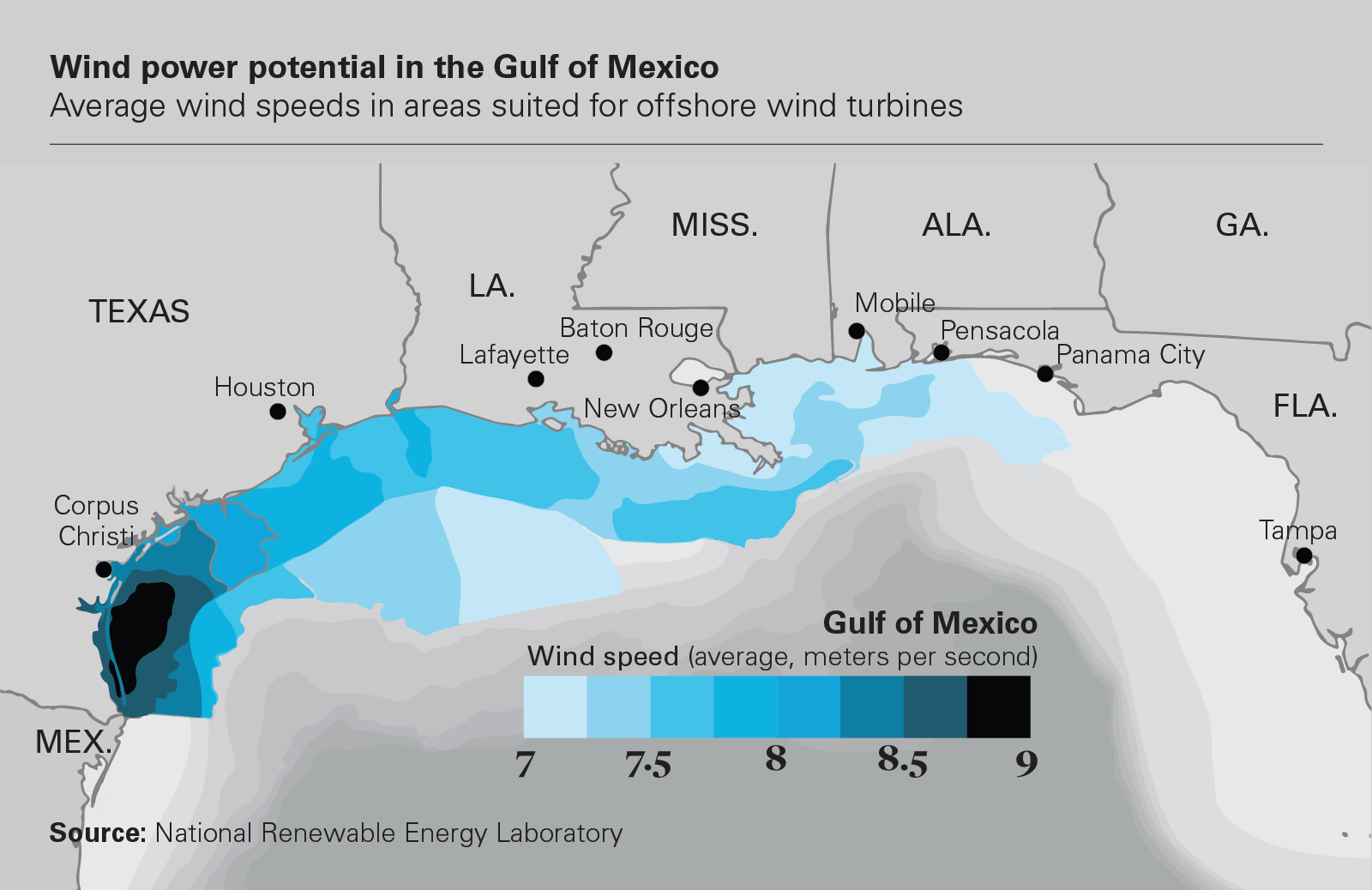

However, most feasible areas of development in the GoM would yield relatively low wind speeds. If projects used current turbine designs and technology, sites with low wind speeds of seven to eight meters per second may only yield a net capacity factor of 30 to 40 percent. Developers can circumvent this natural limitation by increasing the size of rotors, as that practice has been proven viable for onshore wind facilities.

Current projections ascribe the highest resource potential to the coastal waters of Texas and Louisiana, respectively. Newer studies with increased precision may yield additional opportunities for nearby GoM states such as Alabama, Florida and Mississippi. In any case, offshore wind projects could spur significant economic activity for the region. Further, states could emulate the approach in the Northeast and Mid-Atlantic regions in setting robust targets for offshore wind while gleaning lessons from nearby proposal processes and competitive bid solicitations.

Offshore wind development could generate positive, long-term returns for an array of participants and bolster grid reliability in the states bordering the GoM.

Overlaps and synergies with existing energy infrastructure in the GoM

Dating back several years ago, pilot research and development programs in the US have deployed prototype floating foundations. Traditionally used in the offshore oil & gas industry, floating sub-substructures would enable developers to site wind turbines in deepwater areas while accommodating the unique technical characteristics—namely the dynamic nature and sheer scale and height of blades, rotors and turbines, along with the weight distribution needed to stay afloat, particularly when subjected to storms and hostile weather.

Inversely, the shallow waters off the coasts of Texas and Louisiana present several drivers of overall project cost reduction when compared to other offshore projects located in the Atlantic Ocean, including comparatively warmer water and closer proximity to local and regional supply chains, which all collectively improve access to the technical features of an offshore wind-generating facility.

Even though the GoM is yet to host an offshore wind installation, a number of manufacturers in the region—those typically serving the offshore oil & gas industry—have already produced components and foundations for offshore wind projects in other regions as part of a strategic pivot toward the renewable energy sector.

The GoM enjoys a further unique advantage relative to Northeast and Pacific states: Lower labor costs compared to other regions active in offshore wind development.

View full image: Wind power potential in the Gulf of Mexico (PDF)

View full image: Wind power potential in the Gulf of Mexico (PDF)

Of the GoM states, Texas and Louisiana are most optimally positioned to readily embrace offshore wind as a new segment within their energy mix

US$20m

As part of its Inflation Reduction Act of 2022, Congress appropriated US$20 million to hiring additional permitting personnel at the National Oceanic and Atmospheric Administration (NOAA)

Permitting pathways

The offshore wind industry in the US is still in its nascent stages. In no aspect is this more apparent than the lack of regulatory certainty and clarity on time frames for project approval. In March 2021, the Bureau of Ocean Energy Management (BOEM) issued its first environmental impact statement (EIS) for a utility-scale offshore wind project that was initiated in December of 2017.

While it is highly unlikely that subsequent project applications will necessitate such a lengthy environmental review, the BOEM has yet to establish a demonstrable track record in providing a clear roadmap going forward. In the meantime, developers have to contend with a complex web of federal statues and regulations, and also account for a host of jurisdictional issues at the state level for any prospective offshore project.

This federal-state nexus has been a matter of contention in many other arenas of the domestic energy sector, and is poised to cause similar issues as offshore wind deployment scales up. If there is wisdom to be gleaned from other resources, the primary question will be centered around when state-level jurisdiction or authority will supersede that of a federal agency, or simply delay the process enough to effectively halt application approvals altogether.

As part of its Inflation Reduction Act of 2022, Congress appropriated US$20 million to hiring additional permitting personnel at the National Oceanic and Atmospheric Administration (NOAA). Since the NOAA plays a crucial role in reviewing and approving components of offshore wind regulatory applications, increasing permitting staff will hopefully keep pace and improve efficiency of a historically fragmented process.

Extreme weather risks

The warm waters of the GoM bolster hurricane strength and pose significant risks to offshore and onshore infrastructure, and unlike offshore wind facilities on the East Coast, GoM developers will need to address technical considerations stemming from extreme weather events.

To some extent, offshore wind developers may be able to learn from the offshore oil & gas industry, which has endured decades of hurricanes in GoM waters. However, the core aspects of wind turbines—height and profile—differ dramatically from oil rigs and associated platforms: Taller turbines are more susceptible to swaying if the foundation is not also proportionately constructed. The offshore wind sector needs to research and develop specific standards to withstand hurricanes. Site-specific studies and risk assessments will be necessary to design foundations and turbines, particularly if alternative load mitigation may be critical to maintaining movement of the axis so that turbine rotors and blades do not shift direction inadvertently during periods of extreme weather.

Project developers and regulators will need to take that and other regional differences into account when evaluating the robustness and strength of turbines sited in the GoM, especially given the fact that such turbines will invariably be in the direct path of strong storm systems or hurricanes.

View full image: Net technical offshore wind energy resource potential (NREL, 2017) (PDF)

View full image: Net technical offshore wind energy resource potential (NREL, 2017) (PDF)

Offshore wind development in the GoM is an untapped opportunity for large-scale renewable generation

Jan 2022

In January of 2022, the BOEM initiated a monumental step in unleashing the GoM’s potential for offshore wind by announcing it was conducting an Environmental Assessment to evaluate prospective Wind Energy Areas (WEAs) in the region

State and federal nexus

Of the GoM states, Texas and Louisiana are most optimally positioned to readily embrace offshore wind as a new segment within their energy mix. Texas, for example, boasts the strongest quality of offshore wind resources due to having the highest average wind speed, bolstered by plentiful and advanced energy infrastructure both onshore and offshore. Additionally, Texas can draw from its lessons and best practices as a national leader in renewable energy; in 2021, Texas led the US with more than 7,300 MWs in new renewable capacity additions and nearly 20,000 MWs in future projects in the pipeline.

Louisiana, on the other hand, is pursuing renewable energy through policy mechanisms. In fact, Louisiana is the only GoM state that has prioritized climate change goals and recognized that offshore wind can be a key part of meeting such milestones. At the time of publication, Louisiana was the only GoM state with a formalized strategy to reduce greenhouse gas emissions. Louisiana is pursuing a 25 to 28 percent reduction in emissions by 2025 and carbon neutrality by 2050. The Louisiana Climate Initiative Task Force revealed in its draft final report that planning to construct and bring into commercial operation 5,000 MWs of offshore wind will be necessary to meet the statewide goal of carbon neutrality by 2050.

In 2021, the BOEM established the Gulf of Mexico Intergovernmental Renewable Energy Task Force, which includes the states of Alabama, Louisiana, Mississippi and Texas, to share insights and collaborate during the incipient stages of building out a new energy sector in the region.

In January of 2022, the BOEM initiated a monumental step in unleashing the GoM’s potential for offshore wind by announcing it was conducting an Environmental Assessment to evaluate prospective Wind Energy Areas (WEAs) in the region. If the GoM WEAs yield a favorable outcome, then certain WEAs will be auctioned for leasing to project developers.

Oil majors shifting focus

The GoM is the birthplace of offshore energy development: the global, multibillion-dollar offshore oil & gas industry. The energy supermajors, who started out as oil & gas companies, are now diversified and sophisticated energy companies actively pursuing opportunities in the growing development of US offshore wind.

Industry observers expect that oil & gas companies will participate heavily in upcoming seabed lease and subsidy auctions. In 2022, these auctions will exceed 20 GWs of offshore wind-generation capacity, posing a significant opportunity for new market entrants. Large oil & gas companies, with their drive for innovation and the balance sheets to back it up, will be optimally positioned to bolster their odds of winning BOEM auctions. Energy supermajors will have a natural advantage in the offshore arena—particularly in the GoM—over emerging renewable energy-focused companies.

Oil & gas majors will not be deterred by the uncertainty inherent in such projects: A typical exploration venture into oil & gas will encompass similar, if not greater, risks. Incorporating new and emerging renewable assets, such as offshore wind, is now increasingly perceived by these companies as a viable business case both in terms of economic returns and allaying public concerns about environmental impacts.

BP, TotalEnergies, Shell, Equinor and other leading oil & gas companies have already committed substantial financial resources to offshore wind in European waters. Shell, for instance, intends to allocate more investment toward two offshore wind projects (proposed to be sited off Scotland) by 2030 than toward its entire oil & gas segment in the same period.

Untapped potential

Offshore wind development in the GoM is an untapped opportunity for large-scale renewable generation. Renewable developers may have an initial head start in forecasting resource potential and facility design, but fossil fuel stalwarts can easily leverage their strength and experience to their advantage in the long-term.

1 Biden-Harris Administration Announces First Ever Offshore Wind Lease Sale in the Gulf of Mexico, US DEPARTMENT OF THE INTERIOR (press release issued on July 20, 2023). Located at: https://www.doi.gov/pressreleases/biden-harris-administration-announces-first-ever-offshore-wind-lease-sale-gulf-mexico.

2 Final Sale Notice (FSN) for Commercial Leasing for Wind Power Development on the Outer Continental Shelf in the Gulf of Mexico (GOMW-1), BUREAU OF OCEAN ENERGY MANAGEMENT, US DEPARTMENT OF THE INTERIOR, Docket No. BOEM-2023-0021 (published on July 20, 2023), available at: https://www.federalregister.gov/documents/2023/07/21/2023-15501/final-sale-notice-fsn-for-commercial-leasing-for-wind-power-development-on-the-outer-continental.

3 Although used but not defined in the Final Sale Notice, we believe "Tribes" has the corresponding meaning given to "Indian tribe" in Executive Order 13175, which is referenced in the Final Sale Notice when discussing this consultation requirement. Section 1(B) of that Executive Order defines "Indian tribe" as any "Indian or Alaska Native tribe, band, nation, pueblo, village, or community that the Secretary of the Interior acknowledges to exist as an Indian tribe pursuant to the Federally Recognized Indian Tribe List Act of 1994, 25 U.S.C. 479a." Consultation and Coordination With Indian Tribal Governments, EXECUTIVE ORDER 13175 at § 1(b) (Nov. 6, 2000), available at: https://www.federalregister.gov/documents/2000/11/09/00-29003/consultation-and-coordination-with-indian-tribal-governments.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP