Russia

Protection of the public interest remains a priority for the Federal Antimonopoly Service (FAS), and since merger control is directly interconnected with control of foreign investments, including into "strategic" sectors, strengthening control in this sphere inevitably affects the merger control process and trends

12 min read

Subscribe

Stay current on your favorite topics

While the FAS does not seem to be politically influenced as far as merger control is concerned, public interest is taking on increased importance, and in most cases serves as a trigger for delays in merger reviews

Key developments

There were no specific significant transactions that were reviewed by the Federal Antimonopoly Service (FAS) in 2019, and the FAS did not have a particular focus on any specific spheres, as far as merger control is concerned.

That said, protection of the public interest remains a priority—and since merger control is directly interconnected with control of foreign investments, including into "strategic" sectors—strengthening control and increased activity of the FAS in this sphere inevitably affects the merger control process and trends.

Because of this, the FAS has become more active in the courts, enforcing foreign investment laws. One major development was the confirmation by the Constitutional Court of the FAS's extensive interpretation of one of "strategic" activities—geological studies at, and exploration and extraction of minerals from, subsoil plots of federal significance—which can affect mergers involving foreign investors and Russian targets operating in this sphere.

There was also an increase in the number of referrals of merger filings to the prime minister for his decision on whether or not to conduct a fullscale foreign direct investment (FDI) review of the transaction, a process that was introduced in 2017 Back then, the FAS said that this right would be invoked in rare, exclusive cases only, but in the past year the authority has referred more cases than before to the prime minister.

Otherwise, the FAS continues to develop its digitalization strategy, although the adoption of the fifth "digital" package of amendments to the Competition Law is moving quite slowly. At the time of writing, it is still with the government and has not yet been submitted to the State Duma for review. Similarly, a promised procedure for online submission and review of merger control applications has not yet been adopted.

Impact on merging parties

There is a growing tendency towards (sometimes excessive) formalism by FAS officials, as well as the extension of terms for review of applications. This of course varies according to the specific transaction at hand and on the department at the FAS that is responsible for applications. Some of them are generally slower and reluctant to communicate; some are willing to cooperate and work quickly. However, most of the transactions we filed in 2019 and 2020 did not receive approval within the initial 30-day period.

The COVID-19 pandemic to some extent contributed to this. For one thing, the FAS stopped accepting merger control applications filed in person through its incoming correspondence office. There is now a dedicated drop-box for applications and the registration number for the application would be known the following day, rather than immediately as previously.

Similarly, the FAS stopped handdelivering decisions and said they would be sending these by email, for applications not marked as confidential, or by mail. While the process is smooth for applications not marked as confidential, for confidential ones it can sometimes become complicated.

In the case of confidential applications, the FAS will not provide any information on the status of an application by phone and refuses to send documents by email, even to the authorized representative whose details were provided in the application, so the applicant is effectively put in an information vacuum as to the status of review of its application. Clients are therefore told not to mark applications as confidential unless strictly necessary, or to be prepared for a longer timing for the application review.

Additionally, in the wake of the Bayer-Monsanto merger, the FAS has been trying to investigate the digital aspects of all major transactions. As the FAS clarified following its review of that deal, the pure combination of the market shares of Bayer and Monsanto on the markets of seeds and plant protection products did not give rise to dominance issues. What triggered the FAS's concerns was the parties' combined knowledge and power in technology, digital agriculture platforms and package solutions in the agricultural sector involving a digital aspect.

In cases following the Bayer- Monsanto deal, the FAS has started trying to identify the digital solutions being offered by parties.

99

In 2019, the FAS issued conditional decisions in only 99 cases

Recent changes in priorities

While the FAS does not seem to be politically influenced as far as merger control is concerned, public interest is taking on increased importance, and in most cases serves as a trigger for delays in merger reviews.

It is more difficult to get approval for transactions where a target is in an industry that is of special interest to the state, and which therefore is "on the edge" of merger control and foreign investments regulation—such as pharma, production of equipment or tools and rendering services for the development of subsoil fields, the chemical industry, or IT solutions for state-owned companies.

In these sensitive industries, the review will most likely be extended and merger control approval is highly unlikely to be issued within the 30-day Phase I period, even if the transaction does not pose any competition concerns. This is because the FAS will investigate internally—and possibly with the involvement of other governing bodies, including those that are usually involved in the FDI review process, such as the Federal Security Service—as to whether the transaction poses any sensitivity for the state and requires a full-scale FDI review.

One of the triggers for extended review is the FAS's invoking the prime minister's right as the chairman of the Government Commission on Control over Foreign Investments to decide that the full-scale FDI review is required with respect to any transaction by any foreign investor with regard to any Russian company, if this is needed for the purpose of ensuring national defense and state security.

Recent experience indicates that the FAS has been using this procedure more frequently for transactions that were filed as part of the regular merger procedure. Practically, going through this procedure is extremely time-consuming. The FAS must first receive information on the transaction, conducting at least a preliminary review and assessment of the merger control application; form a position on the transaction's sensitivity, and obtain opinions on this from various governing bodies; and only then send the materials for the prime minister's review. There is no statutory period for this stage.

If the prime minister decides that an FDI review is needed, a full-scale filing needs to be prepared and filed with the FAS, with the review taking not fewer than three, but more often six or more, months. The review of the merger control application is suspended for all these months of the pre-FDI and the FDI review processes.

Also notable is other FAS activity on enforcement of the foreign investment laws, which can affect the merger control process for applications filed with respect to targets not necessarily "strategic" but considered as such by the FAS in the course of review.

In particular, the FAS has been extensively interpreting "geological studies at, and exploration and extraction of minerals from, subsoil blocks of federal importance" as a strategic activity. Following the adoption of the foreign investments regulation back in 2008, only companies with a license for development of subsoil blocks of federal importance, such as oil fields with a certain size of reserves, uranium mines, and subsoil blocks subject to exploration within a defense and security zone, were considered "strategic" companies. Acquisition of control over these by a foreign investor would trigger the FDI review.

Later on, the FAS, while considering merger control applications with respect to specific transactions, established that drilling on subsoil blocks of federal importance, as well as provision of equipment for the purposes of exploration for oil at such subsoil blocks, are also considered strategic activities, so entities involved in these activities should also qualify as strategic.

In one of the 2020 cases the FAS established, and the Constitutional Court confirmed, that oil extraction is a complex process. Accordingly, oilfield services in general, if provided on subsoil blocks of federal importance, and have as their purpose either geological studies or extraction of minerals (meaning, that these would not be completed without such services), are considered strategic activities. Thus, entities providing such services for the purposes of development of such subsoil blocks are also strategic.

Key enforcement trends

Generally, the FAS is not particularly demanding in terms of requesting divestments and other remedies, even for large transactions. Bayer's 2018 Monsanto acquisition remains the unique example of a deal in which the FAS requested serious remedies.

Otherwise, if the aggregate market position of merging entities triggers any competition concerns, the FAS usually issues conditional approvals, for example approvals with attachment of orders on the acquirer and its group (or, more rarely, to the target) listing measures aimed at securing competition on the relevant market.

Such measures typically include an obligation not to terminate contracts with respect to specific products or services or with specific customers; not to increase prices for specific products or services, or report to the FAS on any such increase; or not to discriminate among customers.

There have been several examples of orders that lacked proper justification for their issuance. Instead of itself finding the parties dominant on the market post-transaction, the FAS stated that the order shall be complied with "in case of parties' dominance on the market". Considering that in Russia the FAS has exclusive competence to assess entities' dominance in the market, orders of such kind create extreme uncertainty for their recipients.

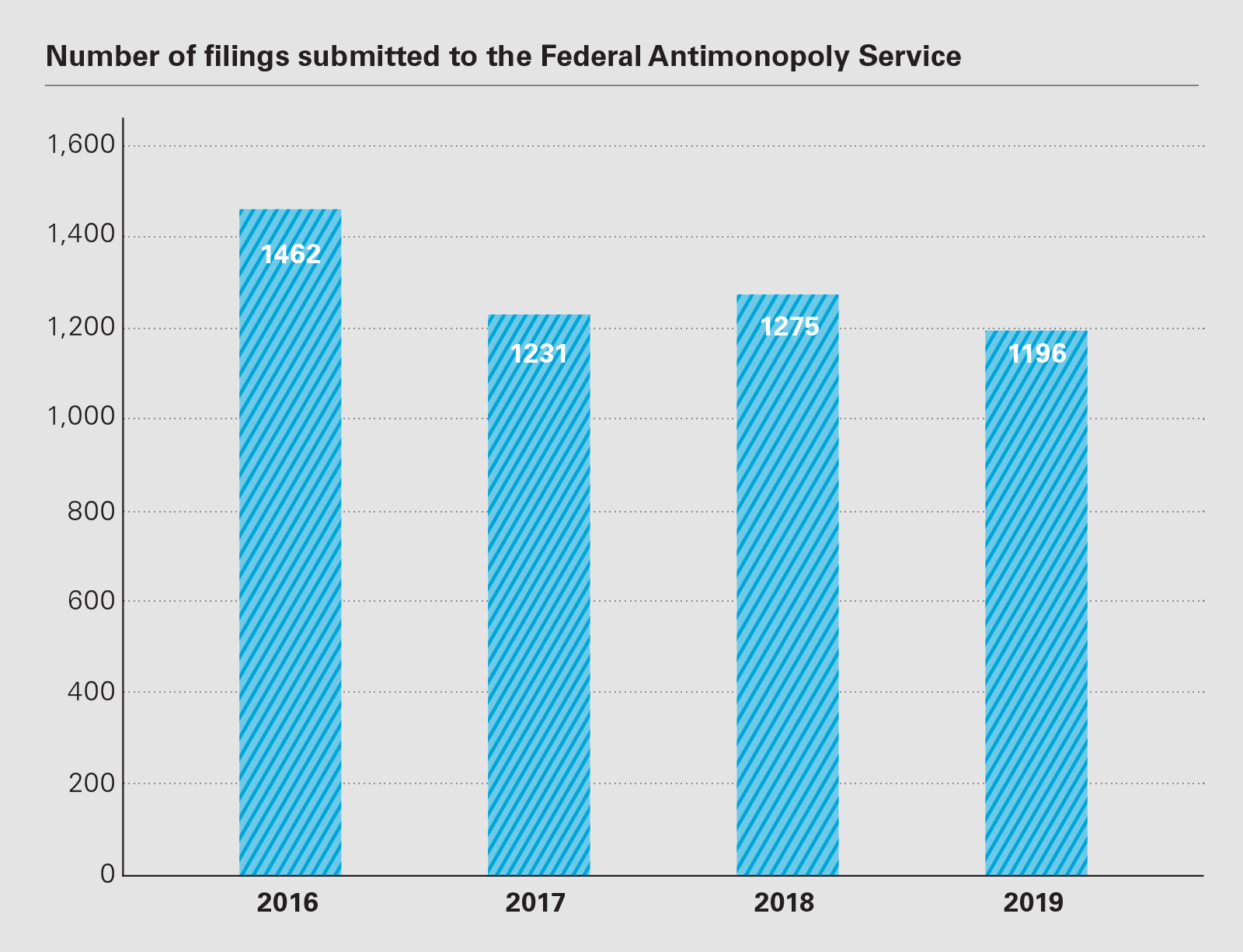

According to FAS statistics, of 1,196 merger control applications filed in 2019, the FAS rejected only 40 (4 percent) and issued conditional decisions in only 99 cases (10 percent). The remaining applications received unconditional approvals.

The highlight of the deals blocked by the FAS is the acquisition by taxi aggregator Yandex.Taxi of Russian taxi provider Vezet, which the FAS refused in June 2020. Back in 2017, the FAS issued a conditional approval of the merger of Yandex.Taxi and Uber, allowing the creation in the market of a powerful combined taxi aggregator.

While reviewing the Yandex.Taxi/Vezet deal, the FAS concluded that the merger would enhance Yandex's dominant position in the market of taxi services. The aggregate market share of the merging companies would amount to 70 percent in the federal Russian market, plus more than 80 percent in 19 local markets, and more than 50 percent in 32 local markets.

Recent studies and guidelines

A remarkable development in the merger control sphere is the joint effort of the FAS and the Association of Antimonopoly Experts (AAE) to draft the full-scale Merger Control Guidelines addressing all aspects of the merger control process, with the aim of clarifying existing controversial issues.

The work started in spring 2019 and is now in its final stage. The FAS has shown great willingness to cooperate and to contribute to the drafting of the voluminous document, and there have been numerous meetings between the AAE working groups and representatives of various departments of the FAS with different levels of seniority.

During these meetings, FAS staff have been open to discussion, devoting considerable time to negotiating controversial issues and trying to form a unified position. The work has been supervised by FAS deputy heads Andrey Tsyganov and Sergey Puzyrevsky, while legal department head Artem Molchanov and deputy head Mariana Matyashevskaya led the drafting work on the FAS side.

In addition to this, the FAS also continued its work on enhancing cooperation with competition authorities in other jurisdictions while reviewing global mergers. For this purpose, the FAS adopted guidelines establishing the procedure for issuance of confidentiality waivers by parties to a transaction that is being reviewed by several competition authorities.

Such waivers would allow the FAS to exchange information on the transaction with other competition authorities and look set to have immediate practical application.

Looking ahead

The introduction of the full-scale online review as announced by the FAS would be welcome. This would facilitate filing preparations and communications with the authority, especially during these times affected by the COVID-19 pandemic. The relevant legal acts, however, have not yet been developed at the time of writing.

No significant changes to merger control regulation and process are expected until the fifth "digital" package of amendments to the Competition Law is adopted. Back in 2018, the FAS expressed a view that the package would be adopted by the end of 2020. However it has not yet been submitted to parliament.

Number of filings submitted to the Federal Antimonopoly Service (PDF)

Number of filings submitted to the Federal Antimonopoly Service (PDF)

THE INSIDE TRACK QUESTIONS

What should a prospective client consider when contemplating a complex, multijurisdictional transaction?

The most critical are timing and process organization. In Russia, filing is quite a formalistic procedure, so the client needs to reserve sufficient time to properly prepare the necessary documents, including those requiring notarization and apostille, as well as other materials, to avoid the package being treated as incomplete and returned to the parties or the review being extended due to bureaucratic reasons.

Other essential aspects are proper multijurisdictional assessment, which is important even for purely Russian deals, as the worldwide activities of a Russian based group can trigger filing requirements outside Russia, and the analysis of the FDI aspects of the planned transaction.

In your experience, what makes a difference in obtaining clearance quickly?

A thoroughly prepared filing and good communication with the FAS during the review are key. The FAS has often attached particular importance to a detailed description of control over the acquirer, including disclosure of ultimate beneficial owners.

It is important to get to the FAS's questions quickly—preferably before or without issuance of a formal request for information—and to answer them quickly. The FAS has its own procedures and timing and, in this sense, parties should be willing to help them complete their review quickly. Here, marking applications as confidential may negatively impact communications with the FAS and timing.

What merger control issues did you observe in the past year that surprised you?

Back in 2013, the FAS adopted guidelines for assessment of joint ventures containing non-compete undertakings. The guidelines, similar to EU practice, allowed such undertakings, subject to certain criteria.

In one of the transactions we worked on in 2020, we saw that certain FAS departments still have a negative approach to such undertakings, and intended to order their removal from transaction documentation, despite their alignment with the guidelines. Such absence of a unified position on the issue FAS itself had clarified was surprising. Fortunately, we managed to persuade the department that the guidelines needed to be followed.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP