Poland

The most important development at the Office of Competition and Consumer Protection is its increased focus on procedural infringements, a trend that has also been visible in other jurisdictions and the EU

17 min read

Subscribe

Stay current on your favorite topics

€50 million

A statutory fine of up to €50 million can be imposed for failure to provide requested information or for providing incorrect or misleading information

Key developments

The most important development is the increased focus on procedural infringements, a trend that has also been visible in other jurisdictions and the EU.

First, in November 2019, the Office of Competition and Consumer Protection (Urząd Ochrony Konkurencji i Konsumentów, or UOKiK) fined Engie Energy PLN 172 million (€40 million) for refusing to provide information to the UOKiK for its probe into alleged gun-jumping in relation to the financing of the construction of the Nord Stream 2 pipeline. This was followed, in July 2020, by a PLN 213 million fine for Gazprom for failing to cooperate in the same probe.

While there are particular circumstances related to the UOKiK's investigation into the Nord Stream 2 project, this is a strong indication that the UOKiK is likely to impose substantial fines for failure to provide requested information or for providing incorrect or misleading information. A statutory fine of up to €50 million can be imposed for this type of infringement.

Second, in October 2020, the UOKiK imposed the record fines for alleged gun-jumping of PLN 29 billion on Gazprom, and of over PLN 234 million on five remaining companies participating in the construction of the Nord Stream 2 pipeline. To be clear, the circumstances of this case were quite specific: the parties initially submitted a merger filing concerning the establishment of a JV, but withdrew it when it became clear that the UOKiK was likely to oppose the deal. The parties then restructured the deal and proceeded on the basis that a notification was no longer required. The UOKiK asserted that a joint undertaking may be established when two or more entities unite their economic interests (even if a separate entity is not created). In the Nord Stream case, this has been achieved by signing a financing agreement, which according to the UOKiK was key to the execution of the project, and led de facto to a creation of a joint undertaking.

In September 2020, the UOKiK has imposed another fine for alleged gun-jumping of PLN 0.7 million on AmeriGas Polska, which according to the UOKiK, took over control of Gas Distribution Center without required merger clearance. Once again it was not a straightforward case. The companies entered into a lien agreement that guaranteed AmeriGas additional powers to influence key management decisions of Gas Distribution Center. Under Polish law, conclusion of a lien agreement on shares or stocks does not require the consent of the UOKiK, provided that the entrepreneur does not exercise the rights arising from those shares or stocks (except for the right to sell them). In the case at hand, the UOKiK considered that AmeriGas exercised these rights, e.g. by blocking the sales of an organized part of the assets of Gas Distribution Center, and therefore, a notification was required.

After submitting a notification, it is crucial to be proactively involved in the proceedings, establish a good working relationship with the case handler, and promptly reply to all queries raised by UOKiK

In December 2019, the UOKiK also issued two decisions imposing fines for alleged gun-jumping. Both cases were local: one concerned a deal between a local supermarket chain and its franchisee; the other, Polish state-owned companies. The fines were quite small, particularly when compared to the fines imposed in the Nord Stream cases.

The first case involved controversial questions relating to the interpretation of the notion of a notifiable concentration, and is relevant for transactions involving acquisition of assets and staggered acquisition of control.

The owner of supermarket chain Dino acquired land on which retail outlets had been built, as well as certain contracts and assets from its franchisee. The transaction was notified to the UOKiK, but the authority adopted an expansive interpretation of the notion of "concentration." It found that the transaction had already been implemented when Dino acquired the land, reasoning that the land was the key asset in the supermarket business. The UOKiK cleared the acquisition and fined Dino PLN 100,000 for this infringement.

Earlier in 2019, the UOKiK also launched an investigation into the acquisition of a 40 percent stake in Eurozet, the owner of several Polish radio stations, by Polish media conglomerate Agora. The remaining 60 percent was acquired by a Czech investment fund.

The UOKiK is investigating whether Agora obtained control over Eurozet as a result of this transaction. In October 2019, Agora notified the UOKiK of the proposed acquisition of a remaining 60 percent stake in Eurozet, which would lead to its sole control of the company. The UOKiK launched a Phase II investigation into this transaction in November. In January 2021, the UOKiK has issued a blocking decision and prohibited the acquisition of Eurozet by Agora. According to the UOKiK, the concentration would have resulted in the development of a powerful radio group that would be able to limit competition on the market for radio advertising and broadcasting of radio programmes.

The UOKiK has also recently become very active in requesting Article 9 referrals in cases with a strong Polish element that are reviewed at the EU level. This is something that companies should keep in mind when notifying a deal with a strong Polish element in Brussels.

In the past couple of years, the UOKiK has submitted four referral requests under Article 9, three of which were granted. Notably, two of the Article 9 requests concerned the media sector, which, together with the Agora case, could suggest a particular focus on this market.

Impact on merging parties

Aside from the increased focus on procedural infringements, 2020 has largely been defined by the COVID-19 crisis, which has generally delayed merger control proceedings in Poland. During the spring, the deadlines for the UOKiK to issue decisions were suspended.

The authority has continued to accept merger control filings for review, but there were delays in obtaining clearance. Although deadlines were resumed in May 2020, some delays should still be expected.

130 days

The shortest duration of merger control proceedings completed in Phase II in 2019

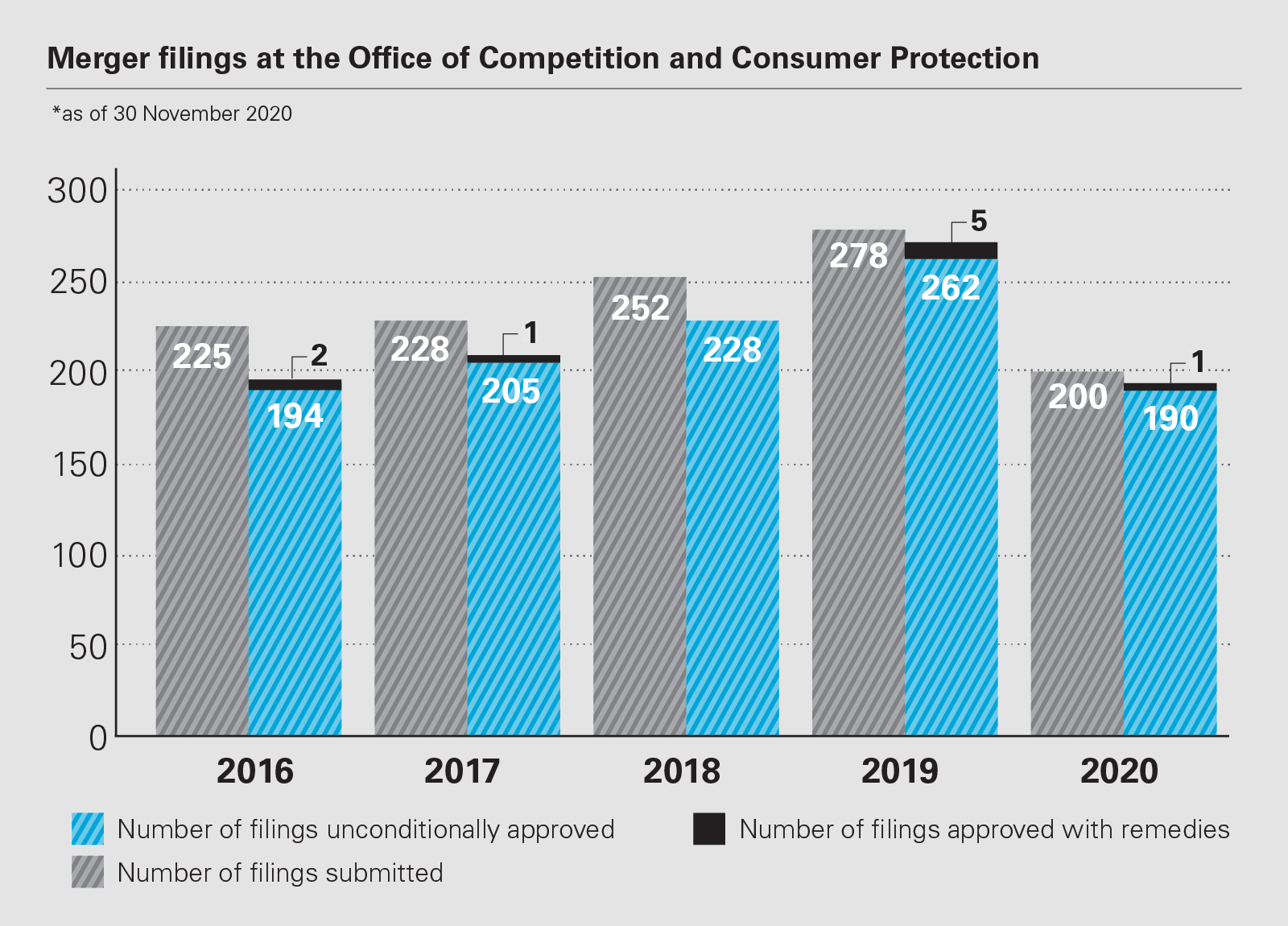

Prior to the COVID-19 crisis, the pace of the UOKiK's work was satisfactory. Last year was a record year in terms of the number of merger notifications, with 278 notifications and 267 decisions issued.

Despite the increase in workload, the average duration of merger control proceedings completed in Phase I was 33 calendar days: the statutory Phase I deadline for the UOKiK to issue a decision is one month, but the clock is stopped each time the UOKiK issues a request for information (RFI), which may significantly extend the proceedings. For example, the longest Phase I case in 2019 lasted 202 days.

Phase II proceedings, by contrast, are significantly longer than the statutory review period, with the average duration of a Phase II case being 266 calendar days. Last year, the shortest Phase II case was 130 days, and the longest 381 days. As in other jurisdictions, the number of merger notifications in the last few months fell due to COVID-19 leading to fewer transactions.

The timeframe in which the UOKiK issues a decision heavily depends on the quality of a merger filing. Parties planning a notification should consider what types of issues the authority will have questions about, what elements should be explained in more detail, and what are the potential "grey areas" that have to be addressed.

There are certain important points that should be always kept in mind when drafting a filing. It should be clear and understandable to avoid potential information requests from the authority. In some instances, the case handlers have limited experience in dealing with a particular market or business sector and can ask additional questions if something is unclear, especially when the transaction concerns new or emerging markets that have not previously been analyzed by the European Commission or the UOKiK.

Some procedural changes to merger control will likely be adopted in the future, as the UOKiK is currently in the process of preparing the implementation of the ECN+ Directive

Gaps in documentation provided should be avoided, as the UOKiK takes a formal approach to filing. Parties should also be responsive to any RFIs and try to resolve as many issues as possible by email or phone.

Communication with the UOKiK is generally smooth, and direct contact with the case handler is possible by phone or email. However, when it comes to obtaining the UOKiK's official standpoint, for instance, with respect to the anticipated time for completing the merger review or potential queries, the authority is reluctant to provide information by email or phone. Instead, it sends official letters, which typically significantly prolongs the proceedings.

As a result of the COVID-19 outbreak, new foreign direct investment (FDI) rules were adopted in June 2020 and became effective on July 24, 2020. In addition to merger control, merging parties now need to take into account the new FDI rules each time they contemplate a transaction with a Polish element.

The new rules tightly regulate major acquisitions by foreign investors without a registered office in the European Economic Area or Organisation for Economic Cooperation and Development countries for at least the past two years.

The UOKiK will apply the new FDI rules, in addition to potential merger control rules, to transactions that involve the acquisition of control or a qualifying holding in a protected entity by a foreign investor. The new FDI rules protect companies registered in Poland, fulfilling one or more of several criteria.

These criteria include generating income in Poland of at least €10 million in at least one of the two preceding financial years; being publicly listed in Poland; holding assets classified as parts of critical infrastructure; being involved in the development or modification of important software; or operating in strategic sectors.

The new FDI law is supposed to remain in force until July 2022, although it could be extended beyond that.

After submitting a notification, it is crucial to be proactively involved in the proceedings, establish a good working relationship with the case handler, and promptly reply to all queries raised by the antitrust authority

The UOKiK is responsible for the enforcement of the new FDI rules and because there is an overlap between the monetary thresholds included in the new FDI rules and the merger control thresholds, the majority of cases requiring an FDI clearance would also be caught under the merger control rules. The UOKiK suggested that there would be close coordination between the two sets of proceedings, so there are likely to be longer waiting periods in cases requiring both merger control and FDI clearance, in particular before the UOKiK becomes more experienced in processing FDI notifications.

The FDI rules adopted in 2020 make the UOKiK's FDI clearance dependent on public interest issues, such as the impact of affected transactions on the public order, public security or public health in Poland.

FDI and merger control proceedings will both be handled by the UOKiK, and UOKiK officials have indicated that there would be close coordination between the two procedures, potentially even putting the same case handlers in charge of both processes. It would therefore not be surprising if cases requiring an FDI approval had a strong political dimension.

Recent changes in priorities

Unfortunately, only a handful of the UOKiK's merger decisions each year are accompanied by a detailed justification, making it hard to deduce any clear-cut trends or enforcement priorities. The UOKiK's decisional practice indicates that it is particularly cautious when reviewing cases on highly concentrated markets, in particular where the transaction results in a high combined share.

If there is a focus on specific industries, it is on sectors that are traditionally close to consumers, such as media, retailing, financial and insurance services and telecoms.

Most cases in 2020 show that the UOKiK is particularly focused on deals involving local markets such as retail markets for daily consumer goods or pharmaceutical products, or emerging markets that were not previously analyzed, such as e-commerce.

Similar to the national competition authorities in other EU Member States, the UOKiK frequently relies on European Commission decisions in determining the relevant markets in its merger proceedings. That said, the UOKiK is not bound by the market definitions established by the European Commission and, even in cases where the geographic market is eventually defined as broader than the national market, the UOKiK usually requests the notifying parties to provide separate data on areas like market share and competitors for Poland.

In several cases, such as the market for commercial real estate rental, the UOKiK decided to delineate the relevant market in a way that clearly diverged from the established line of European Commission decisions, arguing that unique, specific conditions justified a different approach.

Key enforcement trends

As in previous years, the vast majority of cases decided in 2019 were unproblematic. The UOKiK initiated Phase II procedure in only 11 cases. Five conditional clearance decisions were issued in 2019 and one in 2020.

The number of conditional clearance decisions increased, compared with previous years—no conditional clearance decisions were issued in 2018, one conditional clearance decision was issued in 2017, and two conditional clearance decisions were issued in 2016—which may suggest that the UOKiK is more open to finding a solution. Blocking decisions are very rare and there have been no such decisions in 2019 or 2020. One blocking decision was issued in 2021 so far (see the Eurozet/Agora case).

Like other enforcers, the UOKiK prefers structural over behavioral remedies. Many of the transactions conditionally approved by the UOKiK in 2019 and 2020 involved local markets and the remedies were divestments in local markets with the largest combined share.

An interesting example is the Vectra/Multimedia Polska case, cleared conditionally by the UOKiK in January 2020. The case involved the acquisition of fixed-line telecoms provider Multimedia Polska by its competitor Vectra. Remedies imposed involved the sale of overlapping operations in eight towns. In another 13 municipalities, Vectra agreed to allow the customers of the merged entity to change operators before the expiry of their existing contracts.

But the UOKiK can be creative in remedies cases. For instance, in 2019, the UOKiK conditionally cleared a merger between multiplex cinema operators Multikino and Cinema 3D. To address the UOKiK's concerns regarding one local market, Multikino committed not only to selling one 3D multiplex cinema to a suitable purchaser, but also to ensure contractually (subject to the UOKiK's approval) that the buyer would run the cinema at least until 2026.

The remedy accordingly went beyond a divestment and obliged Multikino to contractually warrant future conduct. Such interference in the independence of the remedy taker post-divestment will inevitably complicate the remedy implementation.

Another noteworthy case concerned the acquisition of ACP Europe and Eurocylinder by Air Products & Chemicals, which was cleared subject to behavioral and structural commitments. Interestingly, one of the commitments requires the purchaser not to charge Polish wholesale customers prices for liquid CO2 higher than the maximum prices set according to a specific algorithm. The remedy is effectively a form of price regulation.

Remedy cases typically involve a very lengthy review. For example, in the Vectra/Multimedia Polska case, the review process lasted close to one-and-a-half years. Unlike in the EU and in some other jurisdictions, there is virtually no scope for obtaining a conditional clearance in a Phase I review in Poland.

Recent studies and guidelines

The UOKiK had not, at the time of writing, published any studies or guidelines that directly concern merger control. The authority is now also in charge of processing FDI notifications and it has issued guidelines that aim to clarify the FDI rules adopted in 2020.

Last year was also marked by the resignation of UOKiK president Marek Niechciat in December 2019 after three-and-a-half years in the role. He was replaced by former UOKiK vice-president responsible for consumer protection, Tomasz Chrostny, who joined the authority in August 2019 from the Ministry of Entrepreneurship and Technology, where he served as director of the Department of Economic Analysis.

It remains to be seen whether this will lead to any changes in the UOKiK's review of merger cases.

Looking ahead

The UOKiK has not announced any expected changes to merger control rules for the near future. However, some procedural changes will likely be adopted, as the UOKiK is currently in the process of preparing the implementation of the ECN+ Directive.

Broadly, it would be good to see the UOKiK providing greater clarity in relation to best practices with respect to pre-notification and consultations in cases where it is not entirely clear whether the transaction is caught under the merger control rules.

There is currently no guidance on the pre-notification phase in Poland and it is also difficult to obtain any guidance from the authority as to whether the transaction is notifiable. While certain informal consultations with the UOKiK are possible before submitting a notification, this method of cooperation has limited efficiency.

The UOKiK is rather reluctant to take any decisive approach before a filing, especially in borderline cases. Therefore, at the end of the day, it is often up to the notifying party and its counsel to decide whether a notification is required.

Another problem that would be good to solve is jurisdictional thresholds, in particular as applied to extraterritorial joint ventures (JVs). Under Polish merger control rules, both full-function JVs and non-full-function JVs must be notified to the UOKiK.

Jointly established undertakings might be subject to notification even if they are solely controlled by one of the parent companies. Additionally, according to the UOKiK's merger control guidelines, a JV transaction could be caught under Polish merger control rules if at least one of the parent companies generates turnover in excess of €10 million in Poland.

In consequence, transactions that have no meaningful nexus to the Polish market, such as the establishment of a JV responsible for the construction of an electric plant in Japan, may require Polish clearance.

It would be helpful to adjust the thresholds to consider the geographic scope of the JV's activity. It would also be desirable to bring the approach to non-full-function JVs and JV transactions that do not involve the acquisition of joint control more in line with the rules applicable at the EU level and other European jurisdiction.

Merger filings at the Office of Competition and Consumer Protection (PDF)

Merger filings at the Office of Competition and Consumer Protection (PDF)

THE INSIDE TRACK QUESTIONS

What should a prospective client consider when contemplating a complex, multijurisdictional transaction?

Such transactions often require the assistance of a skilled team of antitrust advisers. This ensures that the client is properly advised and assisted in the conduct and coordination

of a detailed and timely review of merger control issues in various jurisdictions.

The adviser's local footprint also ensures that the client is smoothly guided through and alerted to antitrust risks that may jeopardize the completion of the transaction. It is important to ensure coherence between filings in various jurisdictions, while taking into account local differences and the fact that national competition authorities might communicate with each other in ongoing proceedings.

In your experience, what makes a difference in obtaining clearance quickly?

Achieving quick clearance requires a clear and informative merger notification that is supported with convincing evidence proving that the transaction would not lead to competition concerns. This requires not only an in-depth knowledge of the transaction dynamics, but also efficient cooperation between different teams of advisers and smooth communication with the client.

After submitting a notification, it is crucial to be proactively involved in the proceedings, establish a good working relationship with the case handler, and promptly reply to all queries raised by the antitrust authority.

What merger control issues did you observe in the past year that surprised you?

The very high fines imposed in the Nord Stream 2 case, both for procedural violations on Engie and Gazprom, and for gun-jumping on all members of the Nord Stream 2 investment, were surprising. It is worth noting that the fines for gun-jumping imposed in the Nord Stream 2 case were the highest financial sanctions available to the UOKiK, equaling, in case of each undertaking, 10 per cent of its annual turnover (a fine of more than PLN 29 billion was imposed on Gazprom). The fines imposed in the Nord Stream 2 case were also the highest individual fines in the UOKiK's history for both procedural and substantive infringements.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP