Real estate 2023: Into the headwinds

The sector's ability to adapt to changing circumstances underlines positivity and upbeat sentiment about the future—particularly in the longer term

14 min read

The findings reveal an industry in a period of instability and disruption, with investors, lenders, operators, and advisers cautious and taking pause to reset expectations and risk appetites in response to a rapidly changing macro-economic landscape.

While real estate stakeholders may be concerned about the challenges posed by short-term volatility, over the long term, most respondents remain positive about the sector's prospects and continue to have conviction in the relevance of their strategies and the ability of the real estate sector to adapt to changing circumstances.

Real estate M&A: A waiting game with a positive horizon

M&A: Key findings

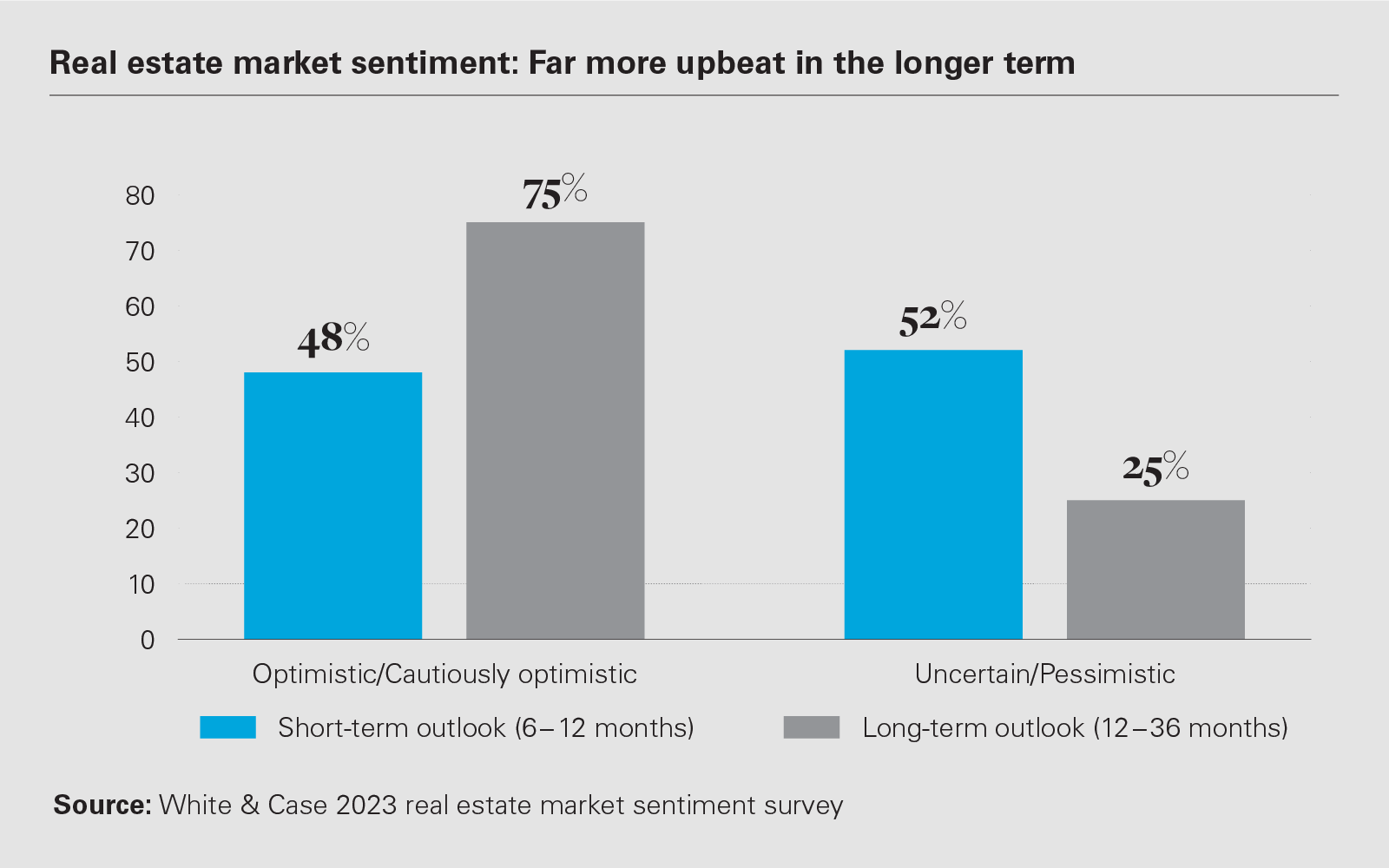

- The respondents are almost evenly split in their short-term assessment of the market: some 52% are uncertain or pessimistic about real estate deal-making opportunities while 48% are more upbeat about the outlook.

- Sentiment much more positive over the longer term, with 75% of those polled cautiously optimistic or optimistic about M&A over the 12 – 36 month horizon.

- Current choppy markets will see real estate dealmakers focus predominantly on off-market deals (28%) and distressed/ restructuring opportunities (26%).

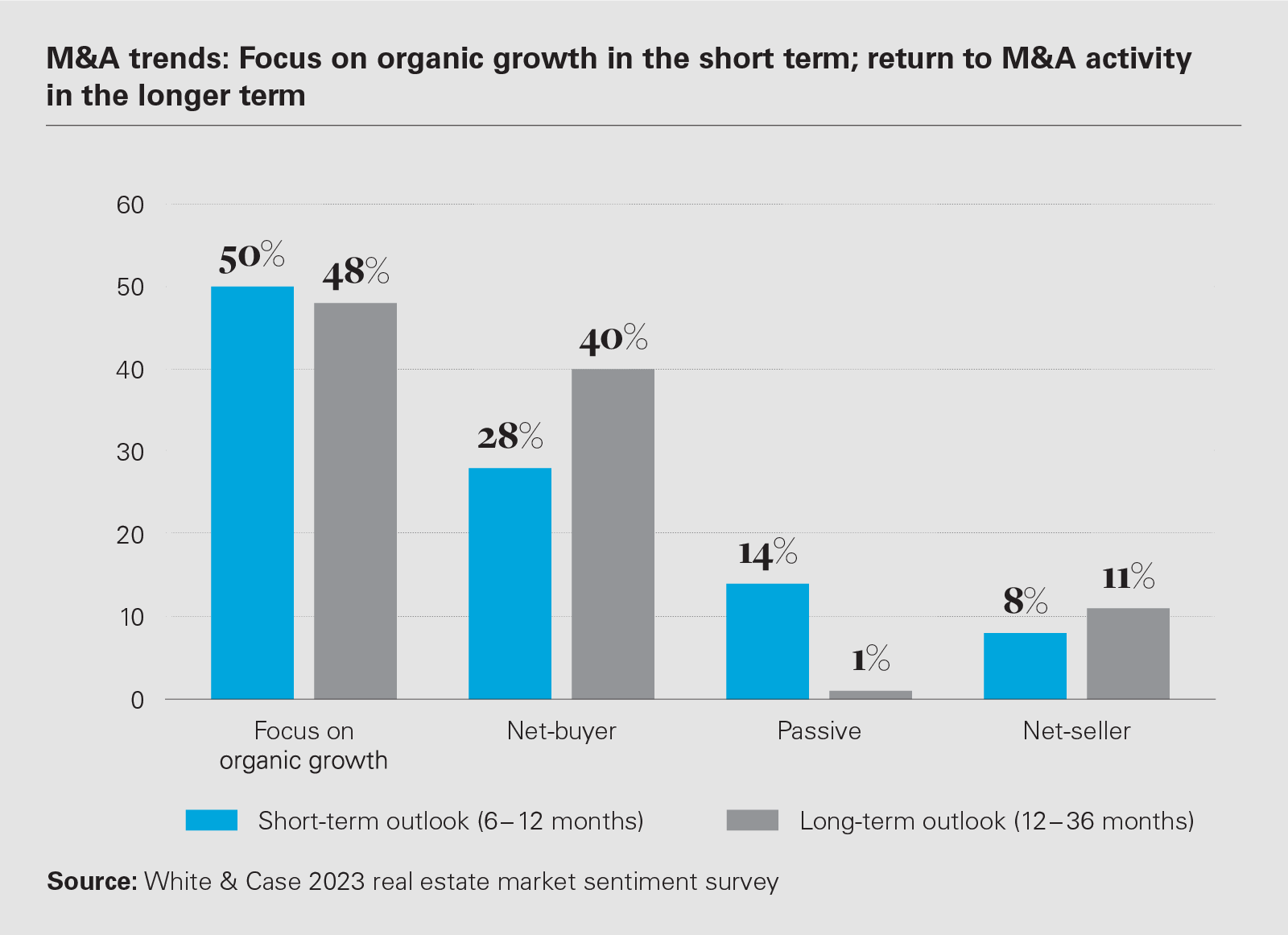

- Over the next 12 months, most respondents expect to tap the brakes on M&A to focus on organic growth or simply sit out the current period of market flux. Over the longer-term horizon, more respondents expect to return to M&A activity.

75%

of respondents are positive about M&A activity in the longer term (12 – 36 months) vs 48% in the next 6 – 12 months

Rising interest rates, volatile asset valuations and fears of housing market corrections have taken their toll on global real estate activity through the course of 2022.

After reaching record highs in 2021, global real estate deal value has tailed off this year with the deal value of US$191.53 billion secured over the first nine months of 2022, down 13% year-on-year, according to White & Case's M&A Explorer.

Deal value for 2022 is down despite a solid first six months of 2022 and without the uplift of a cluster of jumbo real estate deals closed in the first half—including warehouse operator Prologis's US$26 billion bid for Duke Realty and Blackstone's US$13.1 billion acquisition of student housing business American Campus Communities—year-on-year comparisons would have been even less flattering.

Indeed, real estate activity has dropped off materially in Q3 as the impact of rising interest rates in the US and Europe knocked sentiment. Q3 2022 real estate M&A value totalled US$22.9 billion, less than a quarter of the US$87.51 billion posted in Q2 2022 and the lowest quarterly total posted since the first COVID-19 lockdown in 2022.

Against this challenging backdrop for deals, half of respondents (52%) said they were either uncertain or pessimistic about real estate deal-making opportunities in the short term, and 48% were cautiously optimistic or optimistic.

View full image: Real estate market sentiment: Far more upbeat in the longer term (PDF)

View full image: Real estate market sentiment: Far more upbeat in the longer term (PDF)

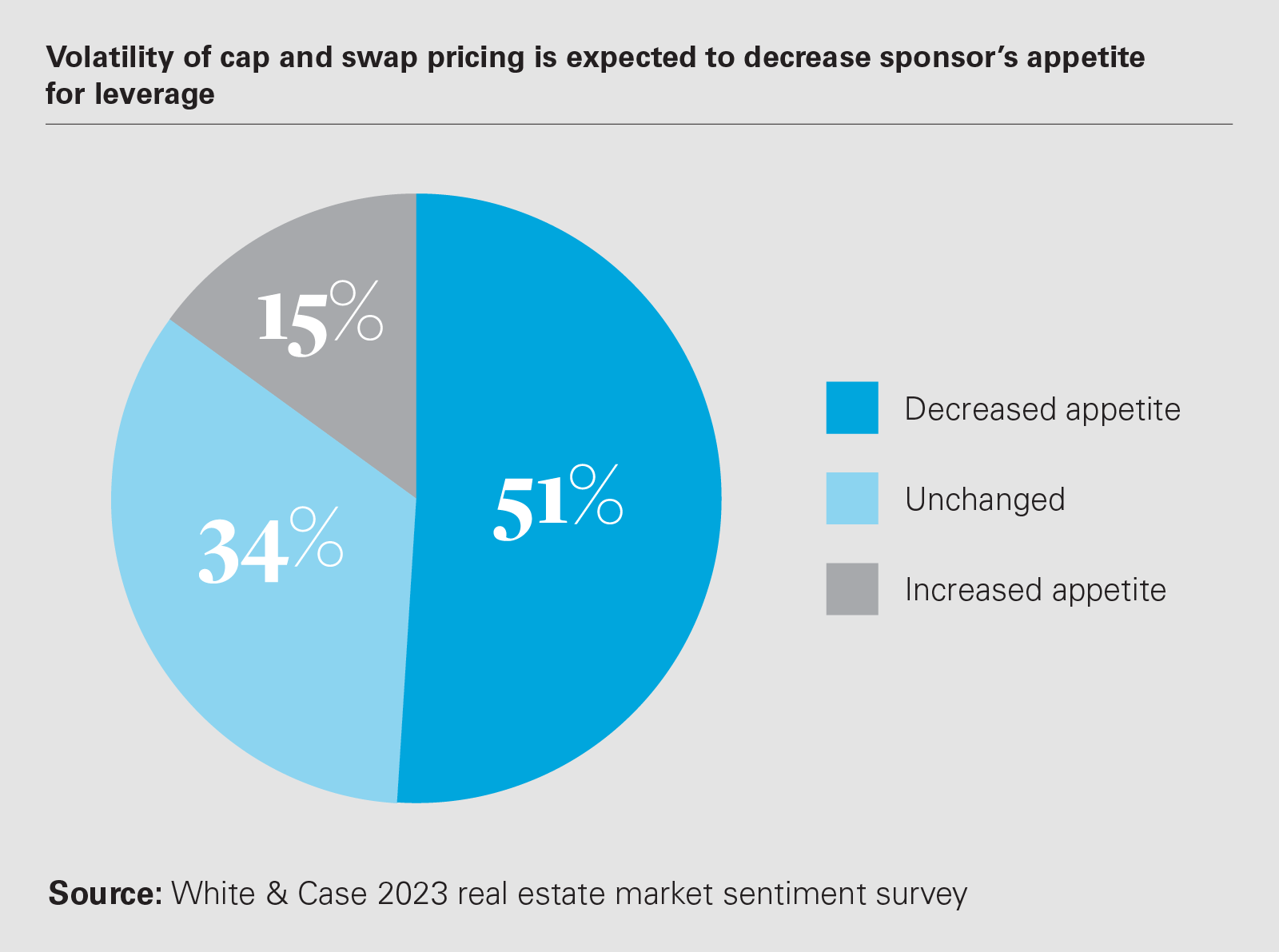

51%

of respondents expect debt cap and swap pricing volatility to decrease sponsor appetite for leverage

For deals that progress over the next 12 months, distressed deals and off-market transactions are expected to account for the bulk of activity.

Approximately a third of survey respondents (28%) expect off-market deals to dominate, reflecting a focus on deliverability and buyer reliability in an uncertain market.

For 26%, distressed deals are expected to increase as the pressure builds on real estate balance sheets— because of rising interest rates. Single asset deals (15%) and platform deals (13%) are selected as the next busiest pipelines for deals, reflecting a more cautious outlook and focus on smaller deals and bolt-on acquisitions rather than big ticket transactions.

For most respondents, M&A will be down the list of priorities, with 50% focusing on organic growth and 14% taking a passive stance towards transactions. Nearly a third of respondents expect to be net buyers during the next 12 months.

In the long term, however, sentiment is more upbeat. Over a 12 – 36 month horizon the percentage of respondents who expect to be net buyers of assets rises to 40% with only 1% expecting to retain a passive position. A vast majority (75%), meanwhile, are optimistic or cautiously optimistic about the outlook for deals in their respective real estate sub-sectors over a 12 – 36 month period.

View full image: M&A trends: Focus on organic growth in the short term; return to M&A activity in the longer term (PDF)

View full image: M&A trends: Focus on organic growth in the short term; return to M&A activity in the longer term (PDF)

Real estate fundraising in flux

Fundraising: Key findings

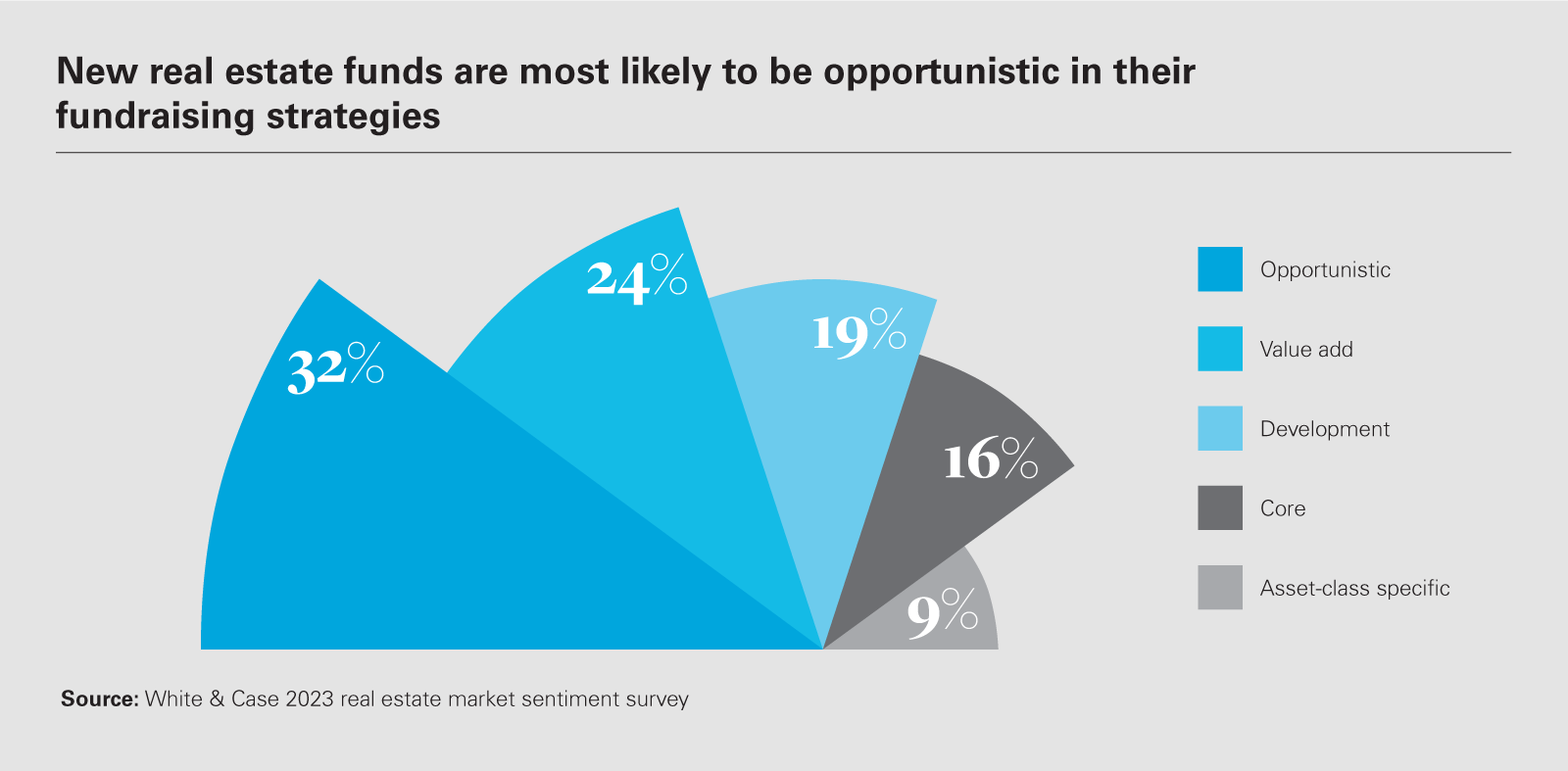

- A third of respondents (32%) expect opportunistic strategies to be the most pursued, 24% citing value-add strategies.

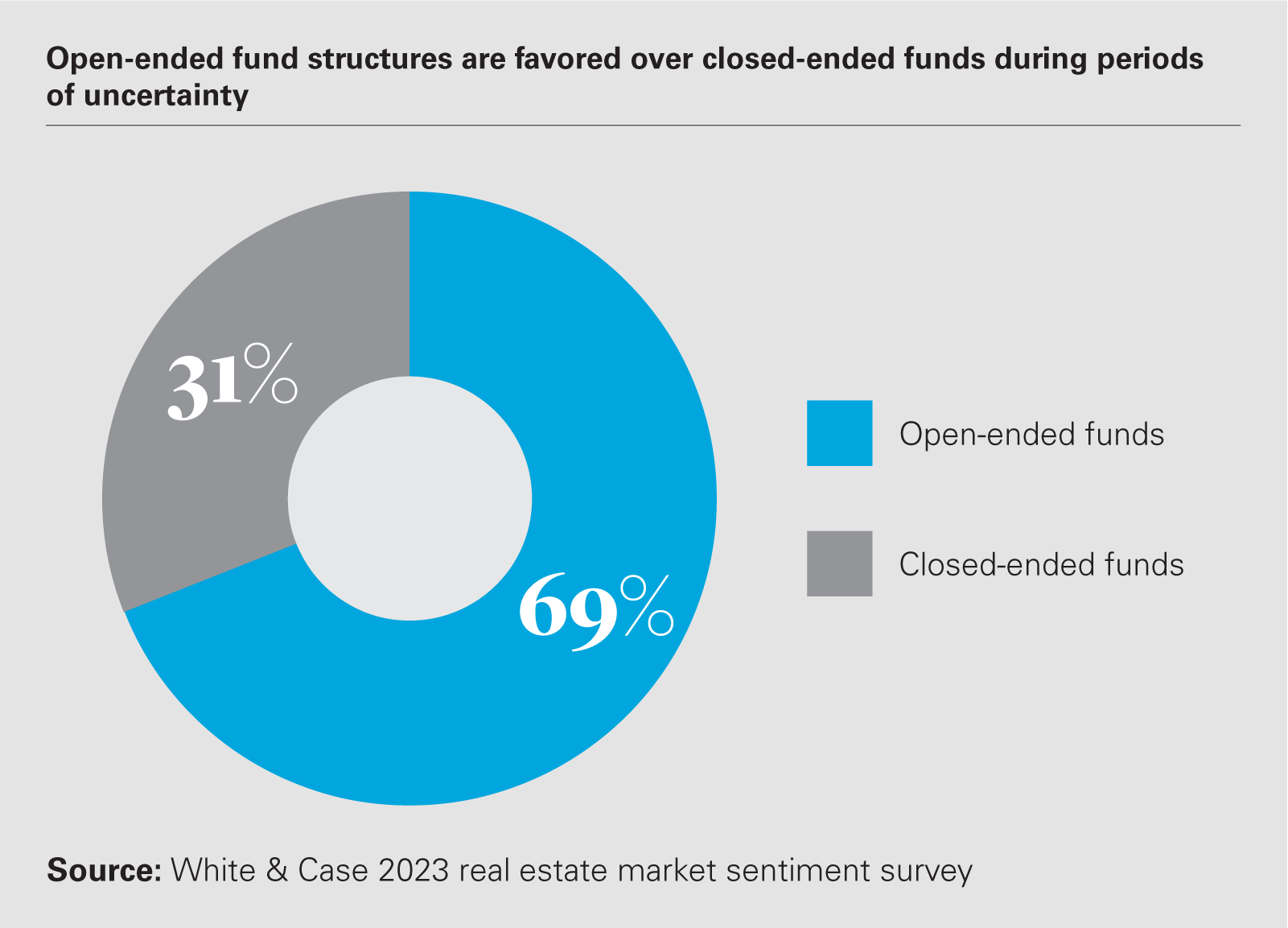

- The use of open-ended funds is in the spotlight. Two-thirds of respondents (69%) believe real estate managers should be considering the use of open-ended fund structures.

- Managers are open to all options that will enable them to extend hold periods rather than sell assets in a falling market.

33%

of respondents said that their companies are incorporating or considering incorporating data analytics into their business operations

Real estate fundraising has cooled in 2022, with investors becoming increasingly risk averse and holding off on making commitments to real estate investment vehicles until there is more visibility on how the industry will navigate current economic turbulence.

According to Private Equity Real Estate (PERE) figures private markets real estate fundraising for the year to the end of Q3 2022 came in at just over US$107 billion, the lowest total for the first nine months of a year since 2013.

The market has not shuttered altogether and large, established managers have still been able to close new vehicles. TPG raised US$6.8 billion for its Real Estate Partners IV vehicle, with LaSalle Investment Management closing an Asia-focused fund on US$2.2 billion and Aermont Capital securing US$3.72 billion for its new real estate fund. For most managers, however, fundraising has become more challenging—in particular, those who are seeking to raise funds as a first-time sponsor, as part of the launch of a new product line, or in the context of new investor relationships.

Looking ahead, survey respondents expect opportunistic strategies and value-add fund strategies (32% and 24%, respectively) to gain the most traction in the next 12 months. Value-add funds that focus on improving existing assets that managers and investors are close to will present lower perceived risk. Lower risk appetite is also evidenced by the finding that the third-most popular fund strategy is expected to be lower risk and have a lower return on core real estate.

View full image: New real estate funds are most likely be opportunistic in their fundraising strategies (PDF)

View full image: New real estate funds are most likely be opportunistic in their fundraising strategies (PDF)

Opportunistic strategies, meanwhile, will see managers attempt to take advantage of market dislocation and lower asset prices to buy good assets at lower valuations. The MSCI World Real Estate Index is trading at a deep discount to levels observed at the end of 2021, shedding more than 27% of its value for the year to the end of October 2022.

For managers across all strategies, a key priority is finding pathways to extend asset hold periods and avoid having to sell assets when valuations are in decline.

Two-thirds of respondents (69%) think real estate fund managers should consider the use of open-ended fund structures in the current economic cycle.

Open-ended funds, however, have not been without their challenges in volatile periods. The illiquid characteristics of real estate assets have meant that managers have often found it difficult to source sufficient liquidity when investor redemption rates rise, forcing managers to gate funds when redemptions start increasing. In addition to this, the calculation of fees on a net asset value basis is substantially less appealing for fund sponsors in times of significant market volatility.

Managers, in order to prolong hold periods, are evenly split between transferring assets into continuation funds (49%), or seeding new vehicles with legacy assets (51%).

View full image: Open-ended fund structures are favoured over closed-ended funds during periods of uncertainty (PDF)

View full image: Open-ended fund structures are favoured over closed-ended funds during periods of uncertainty (PDF)

Real estate financing: feeling the squeeze as liquidity tightens

Financing: Key findings

- Half of the respondents (51%) expect debt cap and swap pricing volatility to decrease sponsor appetite for leverage, with 15% predicting increased appetite.

- A vast majority of respondents (79%) expect to see an uptick in non-performing loans secured by real estate in the next 12 months.

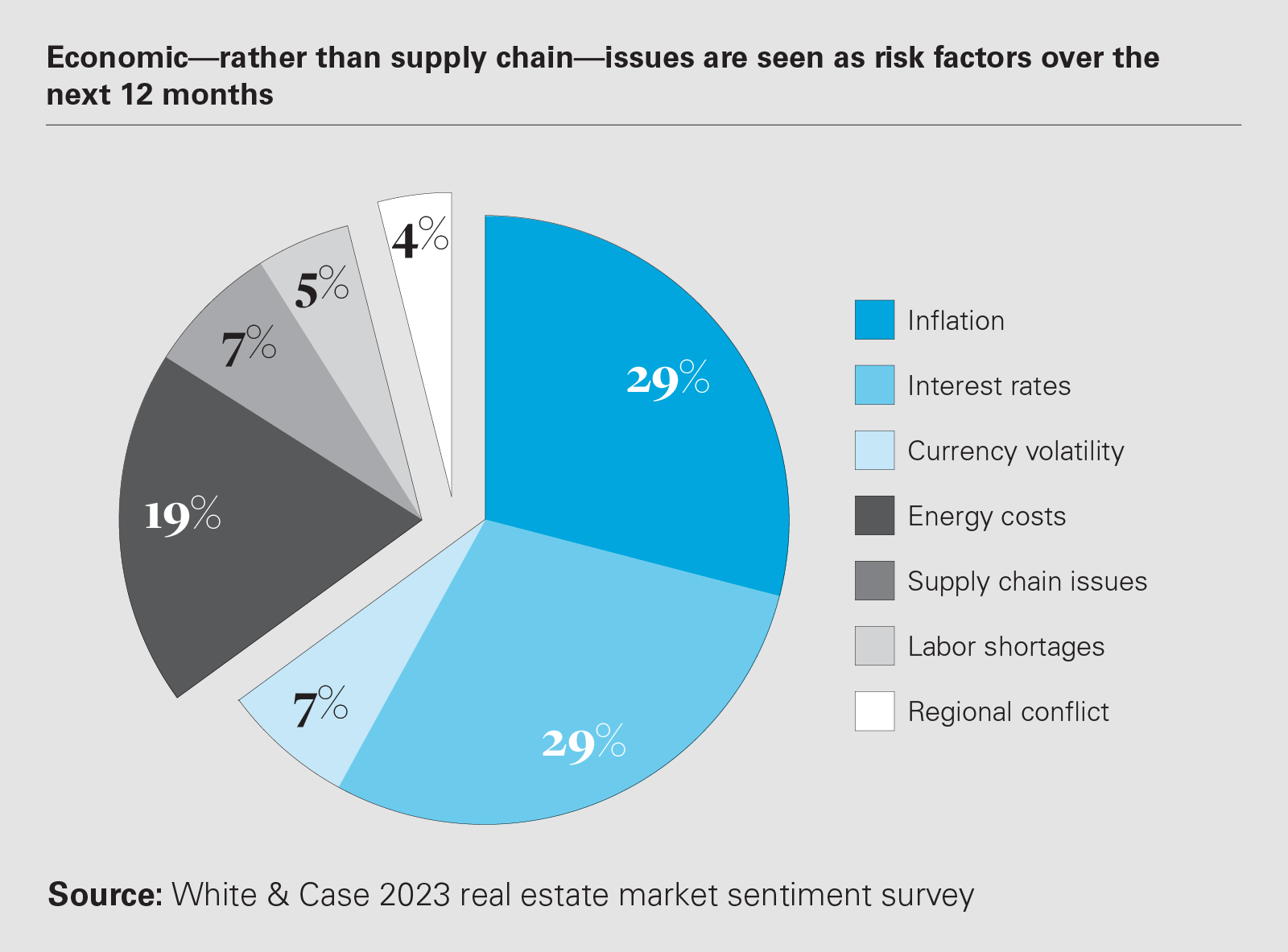

- Inflation and interest rates ranked as the biggest macro-economic risks facing respondents (29% each).

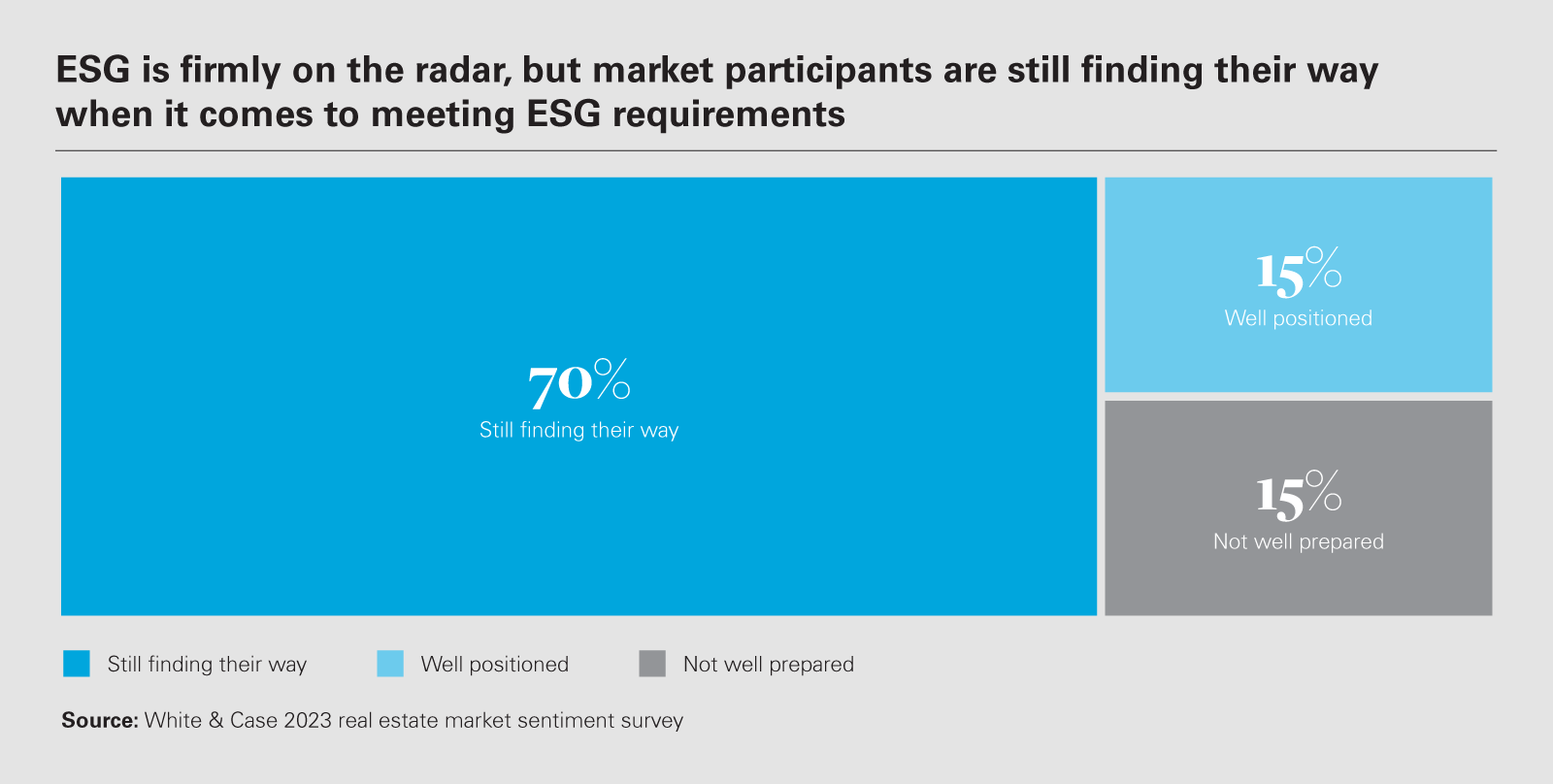

70%

of respondents believe that market participants are still finding their way when it comes to ESG

After enjoying access to abundant liquidity on favorable terms in 2021, the real estate industry has had to adjust to rising financing costs and constrained debt availability through the course of 2022.

As interest rates have increased on both sides of the Atlantic, financing costs are up and debt for real estate has been harder to come by. This has decreased appetite for debt and put existing real estate capital under pressure.

"Limited cash flow will be a challenge for property developers, who have to deal with high interest rates, expensive building materials and lack of mortgage availability," one survey respondent said.

According to research from Moody's Analytics, the cost of debt on commercial property has climbed at such a pace that real estate deal financing costs now exceed earnings from rents for many property owners. Moody's figures show that more than a quarter (28%) for new commercial mortgage-backed securities have negative leverage, where the cost of debt exceeds projected return on their investment. The percentage was sitting at only 8% as recently as Q2 2022 and only 2% in Q3 2021.

"With a hiatus in debt availability some entities will need deep pockets and wise calculus of alternative uses to prevail. Many will simply opt to sell off market," a real estate consultant said.

It comes as no surprise, then, that half of respondents (51%) expect debt cap and swap pricing volatility to decrease sponsor appetite for leverage, with a vast majority of respondents (79%) expecting an uptick in nonperforming loans secured by real estate in the next 12 months.

When questioned on the biggest macro-economic risks facing real estate during the next year, inflation and interest rates— which determine debt pricing and availability—topped the ranking with 29% each, while 27% highlighted availability and pricing of debt as the biggest operational risk during the next 12 months, with only construction costs and resources (30%) ranking higher.

"Construction costs are very volatile. When underwriting you cannot just simply assume a large safety buffer," a survey participant said.

Indeed, the shifts in debt markets, coupled with economic activity, have already had an impact on underwriting with the vast majority of respondents (83%) expecting to see a significant or moderate change in underwriting.

"Property values depend on a market having broad consensus. Presently all variables—including rents, yields, operational costs, construction costs, regulation, and energy—are in flux, and highly unpredictable. Coupled with a slowdown in transaction activity, real estate valuers are exposed to subjectivity and intensified pressure," one survey respondent said.

View full image: Volatility of cap and swap pricing is expected to decrease sponsor's appetite for leverage (PDF)

View full image: Volatility of cap and swap pricing is expected to decrease sponsor's appetite for leverage (PDF)

View full image: Economic—rather than supply chain—issues are seen as risk factors over the next 12 months (PDF)

View full image: Economic—rather than supply chain—issues are seen as risk factors over the next 12 months (PDF)

Challenges & opportunities: Adapting to new demands

Challenges & opportunities: Key findings

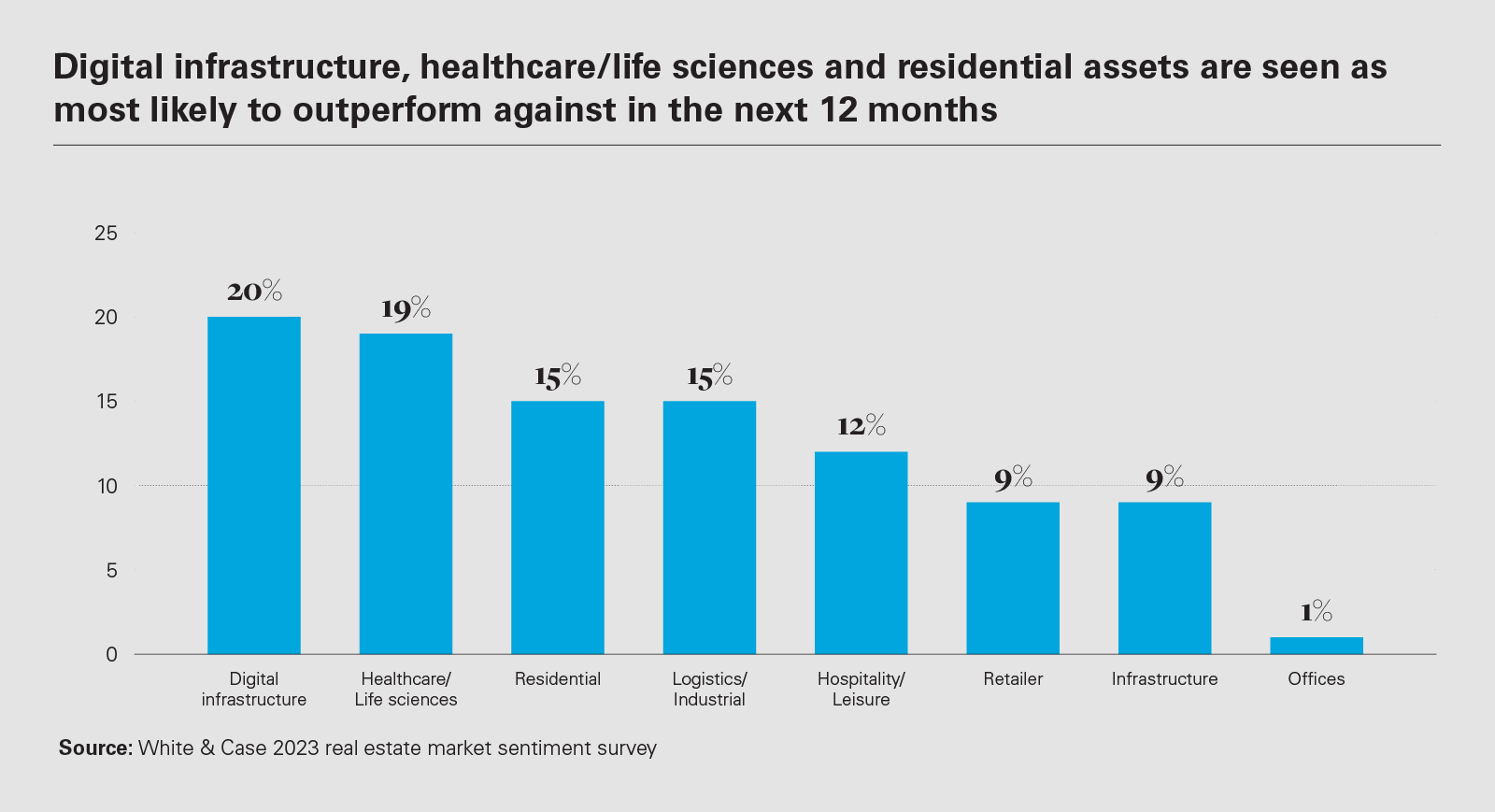

- Digital (20%) and healthcare (19%) assets highlighted as the real estate sectors most likely to outperform.

- Some 37% agree that CVAs, restructuring plans and other insolvency events will have a material impact on business in the next 12 months.

- Technology and digital integration are key to a vast majority of respondents (86%), with data analytics the focus for a third of respondents (33%).

- ESG is firmly on the radar of respondents, although 70% believe market participants are still finding their way when it comes to meeting ESG requirements.

In this undoubtedly difficult time, the operators and managers who are flexible and able to adapt to changing circumstances will continue to strengthen their operations and find opportunities to invest in high-quality real estate assets

Navigating the current volatility in markets will present challenges for real estate operators, but opportunities will also emerge through this period. Organizations with the flexibility to pivot and respond to shifting market dynamics will be the best placed to see out current headwinds and emerge as stronger businesses.

Respondents see digital infrastructure (20%) and healthcare/ life sciences (19%) as areas of sustained growth that are likely to outperform value expectations in the next 12 months.

Indeed, data center M&A activity has proven robust through the course of 2022, according to figures from Synergy Research, with a number of jumbo transactions progressing through the year as dealmakers look to build exposure to the rapid growth in demand for cloud computing and data-hungry digital services. Deal highlights in 2022 have included KKR and Global Investment Partners lining up a US$15 billion acquisition of CyrusOne and the US$11 billion acquisition of Switch by DigitalBridge and IFM Investors. In healthcare real estate, meanwhile, large deals, such as Healthcare Realty Trust's acquisition of Healthcare Trust of America for US$11.2 billion, have also progressed, signalling the sub-sector's resilience.

There is evidence, however, that the market is delineating with other areas of real estate expected to underperform. Slightly more than one quarter (28%) of respondents expect office space to come in below expectations during the next 12 months as the market deals with the ongoing fallout from lockdowns and the growth in home working. Approximately one-fifth are also bearish on retail real estate (22%), which has been squeezed by the secular shift to online shopping and the squeeze on consumer spending in the face of rising inflation.

View full image: Digital infrastructure, healthcare/life sciences and residential assets are seen as most likely to outperform against in the next 12 months (PDF)

View full image: Digital infrastructure, healthcare/life sciences and residential assets are seen as most likely to outperform against in the next 12 months (PDF)

86%

of respondents say technology and digital integration is important or very important for future-proofing their organizations

"This property cycle has a dynamic absent in previous cycles: chronic oversupply in two major asset classes, namely office and retail," a real estate consultant said. "As the paradigm shifts of a significant uptick in online retail and hybrid working coalesce, successful repurposing will be a defining feature of survival for many market participants."

The outlook for the residential and living space sector is also downbeat, with a quarter of respondents expecting residential and living real estate to underperform.

"In living, underwritings would have been done based on very high residential rentals. I expect these will start dropping in the mid-term, making a lot of projects unprofitable," one survey respondent said. "Also, a lot of developers are building private rental sector projects with very small units which will become unpopular with tenants in the mid-term."

The financial pressure that is building on particular pockets of real estate has raised the prospect of restructurings. A quarter of respondents agree that CVAs, restructuring plans and other insolvency events will have a material impact on business in the next 12 months, with nearly half (45%) neutral but aware that risk of restructuring is higher than a year ago.

In addition to steering through an uncertain time in the market cycle, real estate companies are also having to keep apace with digitalizing their own businesses and responding to investor focus on ESG.

Our research reveals an industry in a period of instability and disruption, cautious and taking pause to reset expectations and risk appetites in response to a rapidly changing macro-economic landscape, with brighter times expected ahead

A vast majority of respondents (86%) say technology and digital integration is important or very important for future-proofing their organizations. Data analytics is the technology focus for a third of respondents (33%), reflecting the growing importance of data in the planning, development, and operation of real estate assets, with automation and upgraded hardware also ranking highly (17% and 16%, respectively).

On the ESG front, although there is a recognition of the higher priority investors in real estate are placing on ESG, the survey findings show that the real estate industry is still grappling with how to embed ESG into operations and reporting. More than two-thirds (70%) of respondents say the sector is still finding its way, with another 15% saying that the real estate industry is not well prepared.

ESG, however, is not exclusively a matter of compliance, with survey participants noting the potential upsides of ESG implementation when it comes to saving energy and space costs in real estate sub-sectors such as data centers.

"New server and cloud computing technology reduces energy consumption and makes the real estate in which it is located much more efficient, and thus reduces the overall requirement for space," one respondent said.

Another participant saw ESG opening up new potential business lines thanks to convergence between real estate and energy transition.

"We will see the photovoltaic market develop with substantial upside potential for warehouse roof areas being leased to third parties," the survey respondent said.

View full image: ESG is firmly on the radar, but market participants are still finding their ways when it comes to meet ESG requirements (PDF)

View full image: ESG is firmly on the radar, but market participants are still finding their ways when it comes to meet ESG requirements (PDF)

Outlook for 2023: Recalibrating expectations

After delivering record M&A and investment activity in 2021, spurred by abundant liquidity and low financing costs, real estate stakeholders have to recalibrate expectations as rising inflation and interest rates impact valuations, underwriting and risk appetite.

The survey shows that respondents have taken the opportunity to pause for breath, put M&A programs on hold and reassess debt structures across existing portfolios. Real estate fundraising has been similarly slowed.

In the midst of market uncertainty, however, the survey does reveal that there are still opportunities to invest and deliver value.

Respondents are focusing on investment in existing portfolios of assets they know well, to protect and enhance value. Some are leaning into current headwinds and see a window to tap investors for opportunistic funds that can take advantage of a correction in valuations and support assets faced with potential restructuring. Real estate subsectors, such as data centers and healthcare, meanwhile, continue to grow and present compelling long-term investment targets. Respondents are also taking the time to upgrade their digital and technology capabilities and implement ESG best practice across their organizations and property portfolios.

This is undoubtedly a difficult time in the real estate space, but operators and managers who are flexible and able to adapt to changing circumstances will continue to strengthen their operations and find opportunities to invest in high-quality real estate assets.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP