Exemption from the mandatory offer in connection with the restructuring of the target company

4 min read

A report about the administrative practice of the German Takeover Panel in the last decade

The exemption from the requirement to launch a mandatory offer based on the restructuring of a target company is the most frequently applied exemption from the mandatory offer procedure in German takeover law. In view of the expected increase of restructuring cases due to the COVID-19 pandemic, it is likely to become even more important.

We have looked into the administrative practice of the German Takeover Panel (Übernahmereferat, BaFin) in the last decade to identify typical constellations and points to consider when filing for such an exemption.

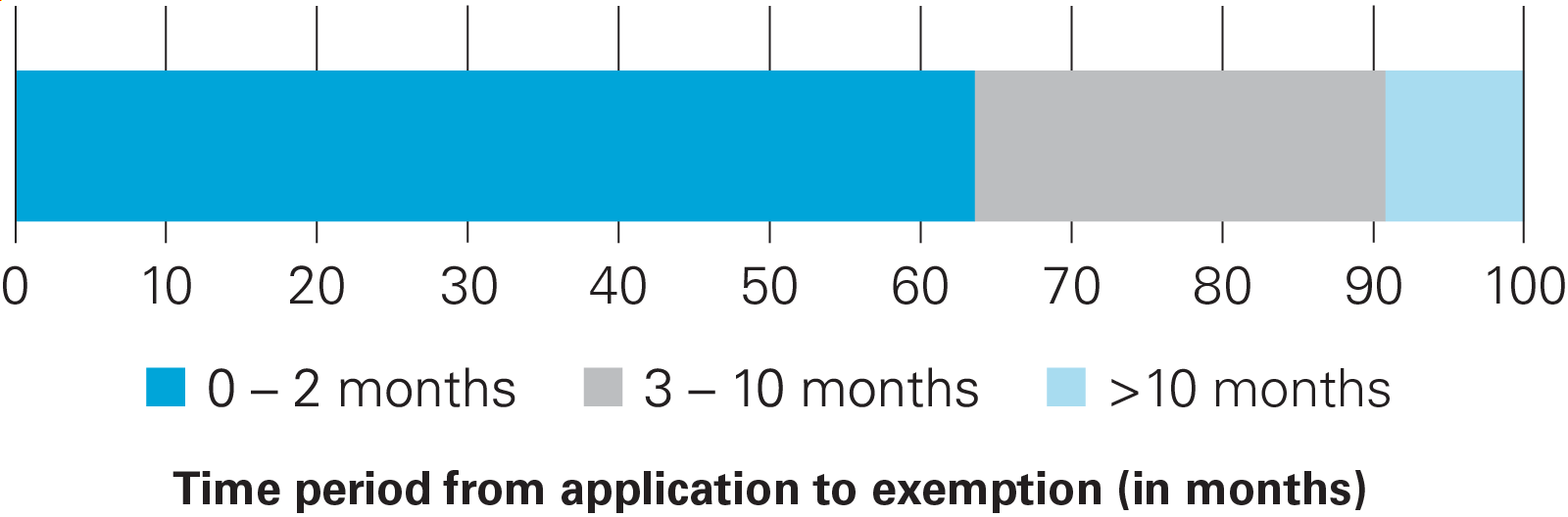

Duration

Proper preparation and alignment with BaFin is key to minimize the time between filing and the exemption decision. BaFin case law shows the time period from filing the application for the restructuring exemption to the BaFin decision varies considerably; it ranges from eight days to almost 19 months (average: approx. four months).

|

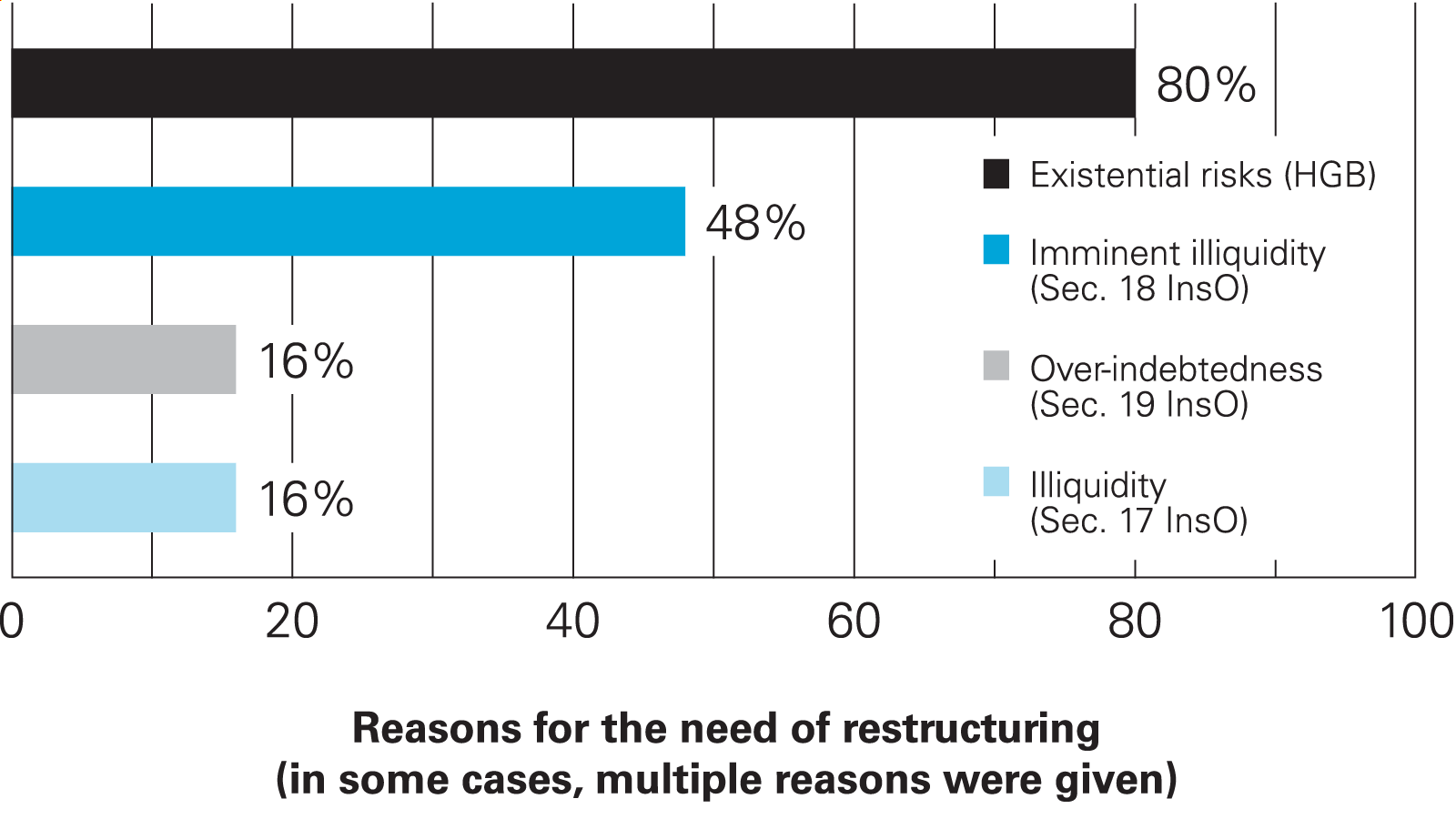

Need for restructuring

First, the bidder needs to establish that the target company has a need for restructuring that fits the exemption criteria under German takeover law.

In this regard, BaFin has most often accepted that risks threatening the existence of the company within the meaning of German GAAP as a need for restructuring (80%) meeting the exemption; another frequently accepted need is imminent illiquidity (drohende Zahlungsunfähigkeit) (48%). In contrast, neither illiquidity (Zahlungsunfähigkeit) nor over-indebtedness (Überschuldung) have been a relevant factor in the decisions published by BaFin.

A bidder needs to provide BaFin with an expert opinion evidencing the need for restructuring. Typically, such expert opinion is rendered by an auditor in accordance with applicable IDW Standards. In one exceptional case, the opinion of an investment bank was accepted by BaFin.

|

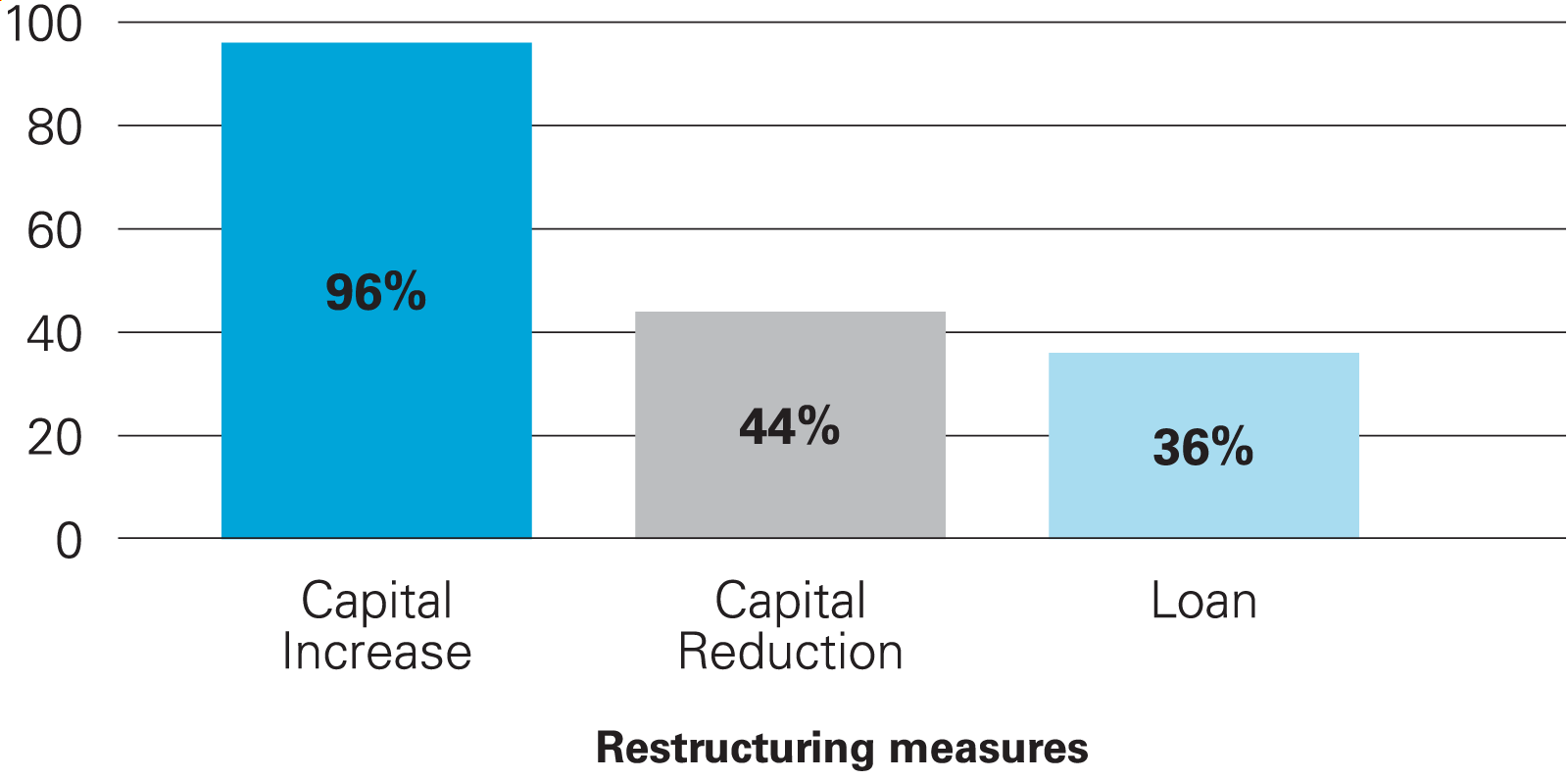

Restructuring capability and restructuring concept

Second, the bidder needs to show that it has a sustainable restructuring concept setting out specific measures to remedy the crisis at the target company, i.e. that the company has a reasonable chance of success.

Capital increases (of all kinds) are the predominant concept, accounting for 96 % of the total measures. In 68% of the cases, the target company was provided with fresh capital by way of a cash capital increase against the issue of new shares; in 20% of the cases by way of a capital increase against contribution in kind and in 8% of the cases by way of a mixed cash and contribution in kind capital increase. The restructuring is often also combined with a capital reduction (44%) or a loan (36%). In this case, the applicants estimated an average time horizon of approx. six months for the implementation of the measures, in their disclosed restructuring concepts.

|

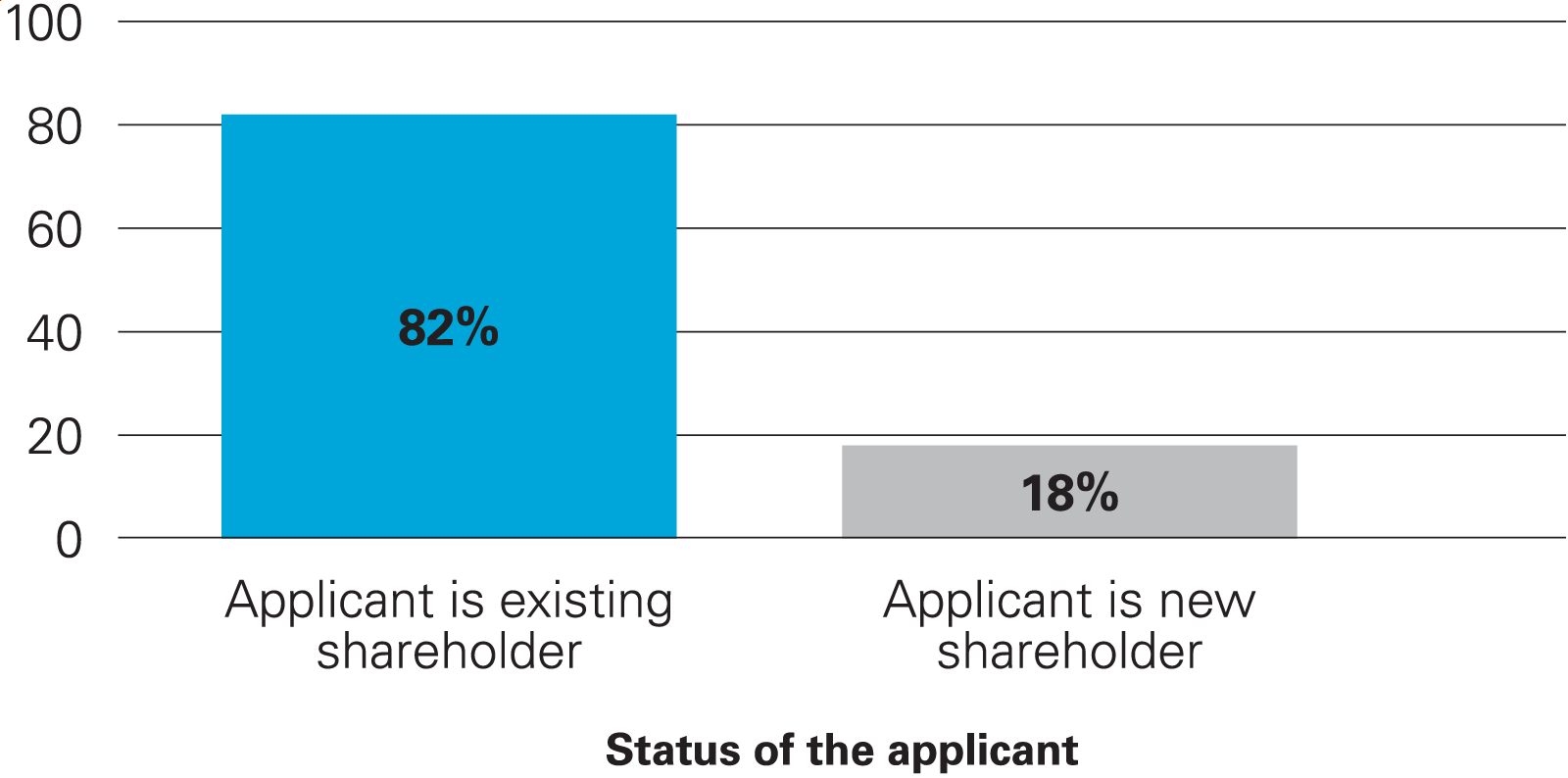

Restructuring contribution

Bidders are predominantly existing shareholders of the target company (82%). In 76% of cases, the restructuring concept and the exemption rely on measures involving contributions from the bidder and third parties (e.g. bond holders or lenders). To benefit from the exemption, the bidder must establish that its contributions account for the vast majority of the financial resources required to restructure the target company.

In addition, the bidder often back-stops the capital increase, i.e. gives an assurance to BaFin that it will acquire all new shares of the target company which are not subscribed by other investors. The contributions of the third parties in some instances take the form of a waiver of claims (or participation in a capital increase).

|

Ancillary provisions

With few exceptions, BaFin has made its decisions subject to ancillary provisions (Nebenbestimmungen), such as conditions or a right of withdrawal. The subject matter of the reservation of withdrawal right and the conditions, respectively, are, in particular, (i) execution and registration of a capital increase intended as a restructuring measure or (ii) acquisition of new shares of the target company or the proof of its execution.

The bidder is typically granted an average of approx. two months to satisfy all such conditions. In individual cases, evidence of satisfaction of the conditions was also to be provided immediately or after 21 months. As evidence of the fulfillment of the ancillary provisions, BaFin has accepted – depending on the type of ancillary provision – an excerpt from the commercial register, a subscription form or a securities account statement.

This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.

© 2021 White & Case LLP