With the urgent need to address climate change universally expressed at the COP26 United Nations Climate Change Conference, many wonder how can we accelerate the path to net-zero? The answer may lie beneath our feet – with geothermal. Geothermal is the heat produced by the earth's subsurface (the term comes from the Greek words geo (for earth) and therme (for heat)). Our planet's core is as hot as the surface of the sun,1 and there are estimates that just 0.1% of its heat content could supply humanity's total energy needs for millions of years.2

Although geothermal power has not experienced the growth of other renewables,3 a constellation of factors suggests that this sector is poised to break out of the shadows and into the limelight of the energy transition. Recent technological progress, such as enhanced geothermal systems, are facilitating commercial developments.4 Oil and gas companies are investing in the industry, as part of their strategy to diversify from fossil fuels and leverage their transferrable drilling expertise. In several countries with an abundance of this green energy, policy makers have passed legislation to encourage investment. In Indonesia, the government has committed to absorbing exploration risk by underwriting the exploitation of prospective fields and selling "proven" reservoirs to the private sector.5 Lawmakers in the Philippines have allowed large-scale projects to be wholly owned by foreign developers, as an exception to domestic ownership requirements.6

And why should we care about geothermal power? It has key advantages over other renewables. Unlike solar and rain-dependent hydropower, it provides around-the-clock, weather-independent electricity.7 Boasting an average capacity factor of approximately 70% (i.e., the ratio of actual energy output over a period to the maximum possible energy output over that period), geothermal is exempt from the perennial "intermittency" criticism directed at other clean energies. Developments have small land footprints, as most of their key components are underground. According to estimates by National Geographic, a geothermal plant capable of producing 1GWh would require only 17% of the land required for a similar sized solar farm.8

In light of this optimism in geothermal's starring role in our carbon-free future, this article spotlights the Asia Pacific countries that will provide the stage for this growth and discusses challenges inherent to its development.

Geothermal projects – key Asia Pacific jurisdictions

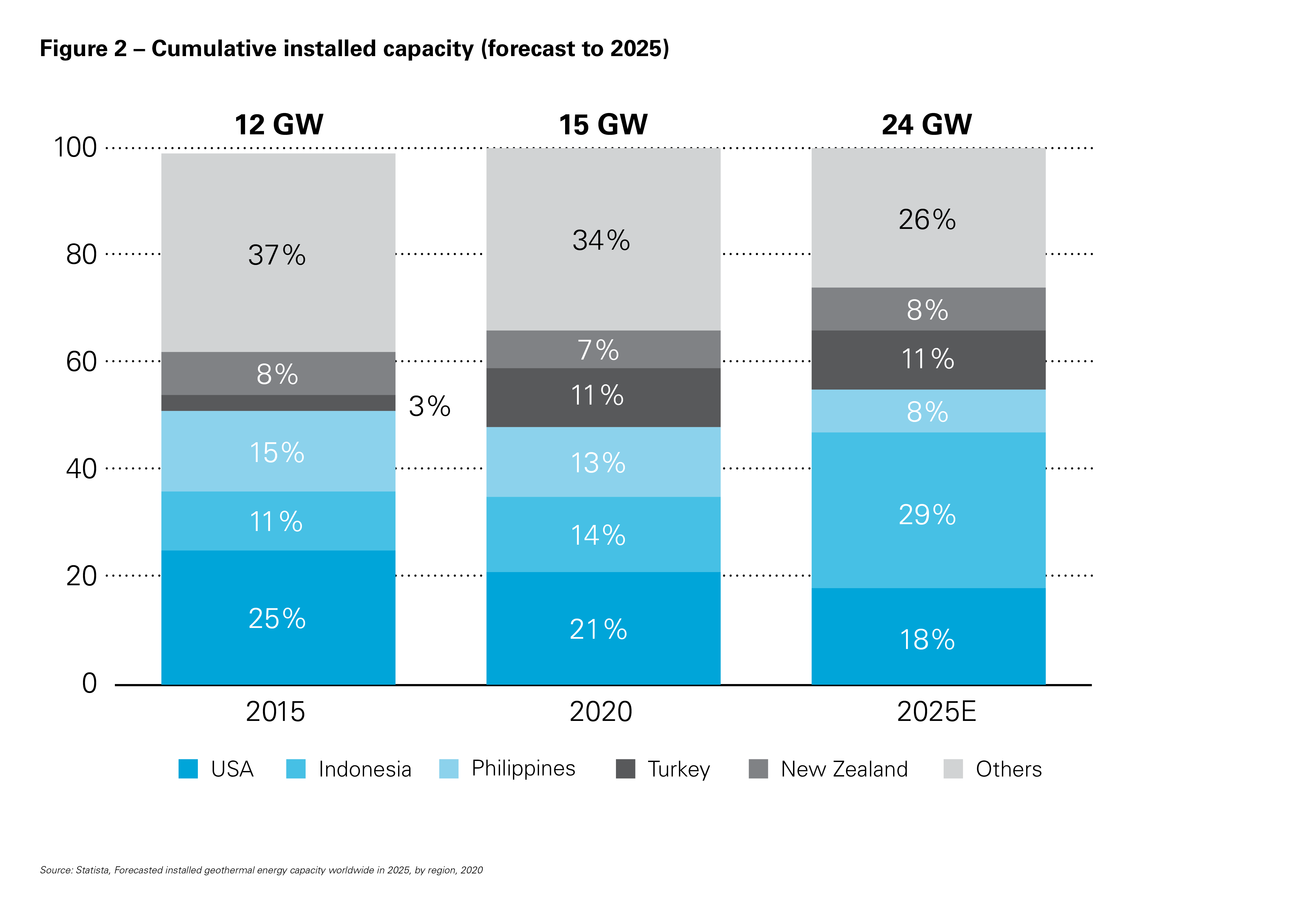

Indonesia, the Philippines and New Zealand are the largest geothermal-producing countries in the Asia Pacific region, accounting for 34% of the approximate global installed capacity of 15GW in 2020.

According to recent forecasts, by 2025, these island nations will collectively increase their market share to 45% of the global installed capacity.

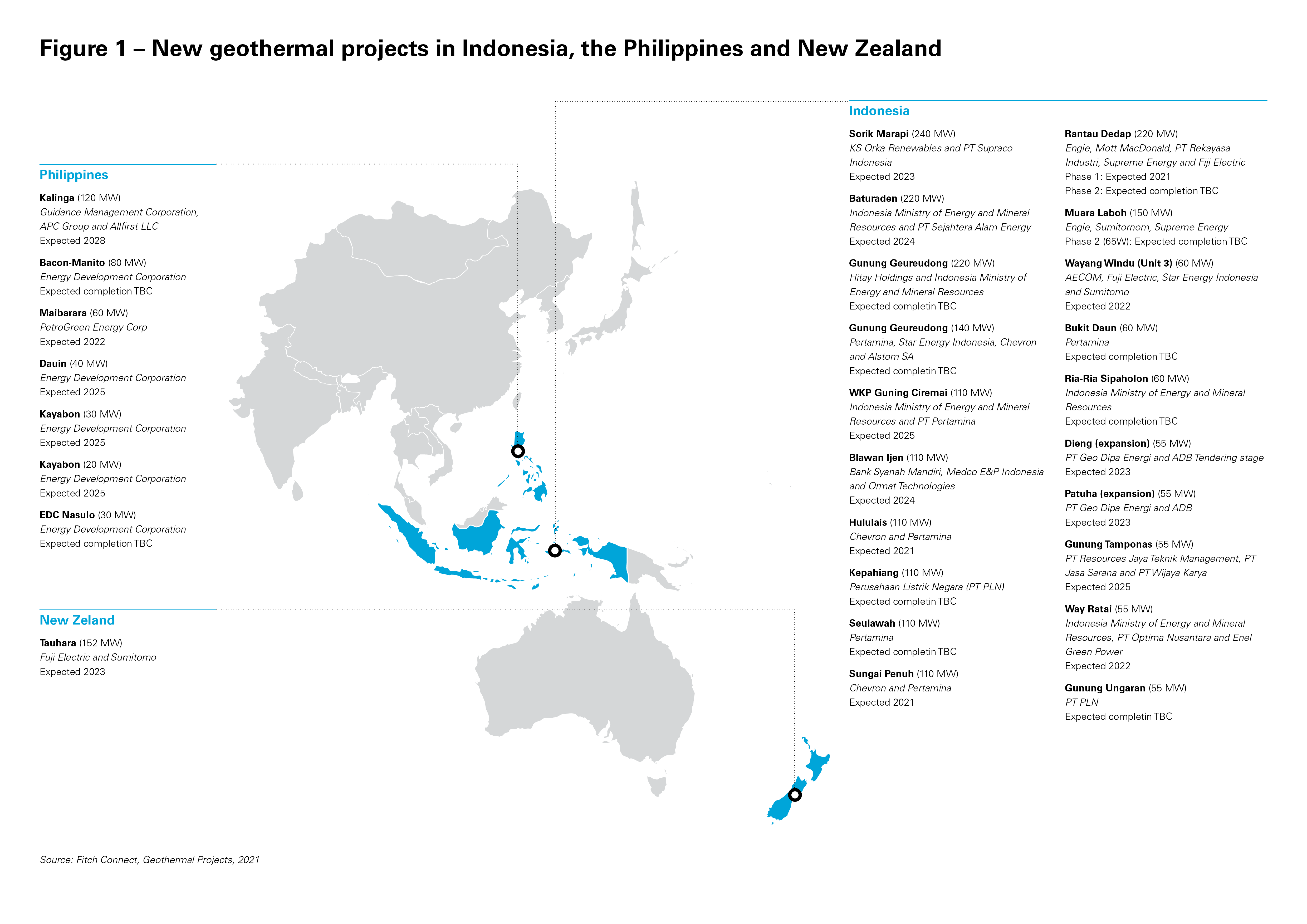

View full image: New geothermal projects in Indonesia, the Philippines and New Zealand (PDF)

View full image: New geothermal projects in Indonesia, the Philippines and New Zealand (PDF)

Indonesia

Due to Indonesia's tilting on the "ring of fire" formed by the confluence of three tectonic plates, this island nation is reported to have the greatest amount of geothermal potential in the world – around 28.5GW, which, if fully used, would account for over 40% of its current electricity generation capacity. As of 2020, the country is the world's second largest geothermal power producer after the United States of America (USA), with a total installed capacity of approximately 2.1GW.9 It has four of the world's top ten geothermal projects, including the two biggest plants by active capacity: the 375MW Gunung Salak facility and the 330MW Sarulla facility.10

Indonesia is aiming to use this renewable power for at least 12% of its electricity requirements, with the installation of approximately 7GW of projects.11 To promote investment in the sector, it has recently passed policies to "de-risk" projects, including the provision of fiscal incentives, value added tax exemptions on imports and property tax reductions during resource exploration. It has implemented exploration-phase risk mitigation measures pursuant to which government-backed entities are to explore prospective fields and tender them to developers for exploitation once proven.

These policies have poised the industry for growth. According to Fitch Solutions, by the turn of the decade, Indonesia will likely claim the number one spot for installed geothermal power capacity, and this green energy will account for approximately 75% of the archipelago's total renewables electricity generation.

The Philippines

As of 2020, the Philippines is the world's third largest geothermal electricity producer after the USA and Indonesia. It has a total installed capacity of approximately 1.9GW, fulfilling over 10% of its power requirements.12 Projects under development include the 120MW Kalinga and the 60MW Maibarara facilities, which are expected to become operational in 2026 and 2022, respectively. The Bacon-Manito facility is slated to be expanded by 80MW, with the initial 29MW expansion scheduled for completion in 2022.13

The geothermal industry in this island nation is not without challenges. Experts no longer anticipate significant domestic discoveries of high-enthalpy resources (i.e., high temperature resources, which facilitate the generation of electricity with a high efficiency factor). And the risk-return ratio of exploiting the remaining low-enthalpy resources has discouraged recent material investment into the sector.14 Developers have been reportedly impeded by the country's stringent environmental protection regulatory framework, which complicates the obtainment of permits.15

That said, the Philippines government is implementing pro-development policies. In 2020, it allowed complete foreign ownership of geothermal projects requiring initial capital of US$50 million or more, as an exception to its domestic ownership requirements.16

New Zealand

New Zealand remains fertile ground for geothermal projects. This renewable energy accounts for approximately 18% of the national electricity supply (which is more than wind and solar combined).17 The 181MW Wairakei plant is the country's largest geothermal facility.18 The 100MW Ngatamariki facility, completed by Ormat Technologies in 2013, remains the largest singular binary power plant in the world.19

Domestic demand for this renewables is expected to increase in the near term.20 This expectation is predicated on the government's commitment to 100% renewable electricity generation by 2030 and the anticipated increase in power demand from transport and industry.21 In 2019, the government committed to spending NZ$10.7 million over a 5-year period to identify new geothermal resources.22 Recently, the feasibility of the 152MW Tauhara plant was confirmed following the appraisal of the adjacent field with commissioning scheduled for 2023.23 In 2026, a 32MW generating unit is expected to be added to the 28MW Northland facility.24

View full image: Cumulative installed capacity (forecast to 2025) (PDF)

View full image: Cumulative installed capacity (forecast to 2025) (PDF)

Key challenges for geothermal projects

Although geothermal power shows great promise in the Asia Pacific region, it poses unique challenges. In this section, we discuss risks inherent to the exploitation of this resource and how such risks are typically mitigated contractually.

Geothermal development differs from other green energy resource development. It harvests the heat beneath the earth's surface through extractive drilling. In contrast, solar, wind and hydropower projects do not require resource extraction, but rather "catchment" of their respective resource (i.e., solar irradiance, wind and water).

Data on resource potential for geothermal is relatively thin. Historical records on wind speeds, solar irradiance and rainfall may provide a reasonable degree of certainty regarding the future availability of such resources. No comparable historical records exist for geothermal, and substantiating the potential of a prospective site requires expensive exploration drilling. Several developers have invested tens of millions of dollars in exploring potential fields in Indonesia and the region without discovering viable resources.25

Drilling and well maintenance costs risk

Once exploratory drilling has confirmed the existence of resources, drilling is required to harvest a geothermal field. Due to the unpredictability of the subsurface, it is difficult to forecast the investment required to access this resource (drilling contractors do not guarantee resource access). On certain projects, drilling and well maintenance costs have exceeded EPC costs and constituted around 40% of their total capital costs.26

Project finance lenders seek to mitigate this heightened risk of budget overruns. During construction, lenders may require that the borrower design and implement an approved well drilling program, satisfy drilling milestones and seek lender consent over drilling contract change orders. During operation, the borrower may be required to develop well maintenance and drilling projections for lender approval and incur expenses in accordance with these approved projections. Project financiers may also insist that the borrower procure well equipment insurance and drilling operator's extra expenses insurance to insure against well equipment damage, or the costs of controlling an unstable well and cleaning up contamination from drilling.

Reservoir depletion risk

If improperly managed, geothermal fields may deplete faster than originally anticipated. The three oldest projects in Italy, New Zealand and the USA, have operated at reduced output because heat and water were extracted from their reservoirs faster than they were replenished.27 Any such unanticipated depletion can reduce a project's generation capacity and adversely affect its economics.

Project investors will seek to manage reservoir depletion risk. They may require close and regular monitoring of reservoirs for signs of thermal depletion by their reserves consultant and impose obligations on developers to commit to drill "make-up" wells to maintain consistent steam production. Project lenders may also require an update to the financial model once signs of reservoir depletion emerge, to ensure that dividend payment conditions are evaluated against current economic and technical assumptions.

Safety risks

Geothermal development is risky, and the fracking process typically used has been associated with well blowouts.28 Fracking involves the injection of high-pressure fluid into wells to crack the subsurface and release resources. In April 2020, a well blowout was reported at the Blawan Ijen project in East Java, Indonesia,29 and widely reported blowouts have occurred in Australia,30 Chile31 and Japan.32 Blowouts have resulted in worker injury and death and property damage. In January 2021, a poisonous gas leak from a project in Indonesia resulted in several civilian fatalities and injured dozens of others.33

Project financiers will typically mitigate this heightened safety risks by requiring strict safety-related representations and undertakings, including the requirement that the borrower provide regular, detailed reports on project safety statistics and proposed remedial measures.

The "Sun Beneath our Feet"

Although geothermal development poses exceptional challenges, careful structuring may sufficiently de-risk projects and facilitate investment into this promising sector. Combined with recent technological and legislative advances, geothermal's advantage as a baseload source of clean power with high energy density has provided grounds for optimism about its future in the Asia Pacific region. The earth is offering support in our struggle against climate change. It is up to us whether we care to accept it, and tap the "sun beneath our feet".

1 https://www.bbc.com/news/science-environment-22297915.

2 https://www.cnbc.com/2021/05/07/why-oil-giants-like-chevron-and-bp-are-investing-in-geothermal-energy.html.

3 Between 2000 and 2018, geothermal energy capacity registered a compound annual growth rate (CAGR) of 3.2% compared to a CAGR of 22% for the onshore wind segment and a CAGR of 42% for the solar power segment: https://www.nsenergybusiness.com/news/geothermal-indonesia/; https://www.windpowerengineering.com/renewables-to-double-in-total-installed-capacity-in-the-u-s-by-2030-finds globaldata/#:~:text=The%20onshore%20wind%20segment%2C%20which,compared%20to%208%25%20in%202018; https://www.seia.org/solar-industry-research-data.

4 https://www.greentechmedia.com/articles/read/enhanced-geothermal-systems-technology-advances.

5 https://www.ren21.net/wp-content/uploads/2019/05/GSR2021_Full_Report.pdf, page 102.

6 https://www.thinkgeoenergy.com/philippines-allows-100-foreign-ownership-in-large-scale-geothermal-projects/.

7 Geothermal power has an average capacity factor of approximately 70% whilst the average capacity factors of wind and solar are estimated at 25% and 35%, respectively. https://e360.yale.edu/features/can-geothermal-power-play-a-key-role-in-the-energy-transition; https://www.eia.gov/electricity/monthly/epm_table_grapher.php?t=epmt_6_07_b.

8 https://www.energysage.com/about-clean-energy/geothermal/pros-cons-geothermal-energy/.

9 https://www.esdm.go.id/assets/media/content/content-capaian-kinerja-tahun-2020-dan-program-kerja-tahun-2021-sektor-esdm.pdf.

10 https://www.nsenergybusiness.com/features/top-geothermal-power-producing-countries/.

11 https://www.geothermal-energy.org/pdf/IGAstandard/WGC/2020/01073.pdf, page 2.

12 https://www.geothermal-energy.org/pdf/IGAstandard/WGC/2020/01017.pdf, page 11.

13 https://www.turboden.com/upload/blocchi/X40167allegato1-2X_31626_POWER_PHILPPINES_press-release-EDC-by-MHI.pdf.

14 https://mb.com.ph/2021/01/19/geothermal-investors-seek-risk-insurance-perks-for-new-projects.

15 https://www.ren21.net/wp-content/uploads/2019/05/GSR2021_Full_Report.pdf, page 102.

16 https://mb.com.ph/2020/12/22/no-foreign-firm-takers-of-ph-geothermal-blocksyet.

17 https://www.mbie.govt.nz/building-andenergy/energy-and-natural-resources/energy-statistics-andmodelling/energy-statistics/electricity-statistics.

18 https://www.nsenergybusiness.com/features/geothermal-power-stations-new-zealand/.

19 http://worldkings.org/news/australia-records-institute/worldkings-worldkings-news-australia-records-institute-auri-ngatamariki-power-station-world-s-largest-singular-binary-power-plant.

20 https://theconversation.com/as-nz-gets-serious-about-climate-change-can-electricity-replace-fossil-fuels-in-time-155123.

21 https://theconversation.com/as-nz-gets-serious-about-climate-change-can-electricity-replace-fossil-fuels-in-time-155123.

22 https://www.stuff.co.nz/national/117860027/searching-for-new-zealands-electricity-future-in-the-deep-heat.

23 https://www.ren21.net/wp-content/uploads/2019/05/GSR2021_Full_Report.pdf, page 102.

24 https://www.mbie.govt.nz/dmsdocument/11679-energy-in-new-zealand-2020.

25 https://www.thinkgeoenergy.com/chevron-abandons-lampung-geothermal-project-in-indonesia/.

26 https://pangea.stanford.edu/ERE/pdf/IGAstandard/SGW/2018/Gul.pdf, page 3.

27 https://www.energy.gov/eere/geothermal/geothermal-faqs#environmental_impacts_of_geothermal_energy.

28 https://www.lexology.com/library/detail.aspx?g=9ab6ec95-683e-49b3-966c-be3dd2140d84.

29 https://www.thinkgeoenergy.com/steam-kick-from-geothermal-exploration-well-at-blawan-ijen-geothermal-project/.

30 https://www.thinkgeoenergy.com/geodynamics-habanero-project-back-on-track/.

31 https://www.environmentandsociety.org/arcadia/subterranean-invisibilities-traces-underground-water-and-thermal-flows-el-tatio-geyser-field.

32 https://publications.mygeoenergynow.org/grc/1030551.pdf.

33 https://go.kompas.com/read/2021/01/26/161149774/five-dead-24-receiving-intensive-treatment-after-gas-well-burst-on-indonesias.

Shafinas Djuanda (White & Case, Associate, Singapore) contributed to the development of this publication.

This article was first published in PFI magazine (December edition).

This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.