What will drive issuance in a post-COVID-19 world?

Foreword

Halfway through 2021, we take stock of leveraged finance in the United States and consider the road ahead for both borrowers and lenders. After more than a year of COVID-19, are things returning to normal? Or are we just starting a whole new journey?

In many ways, COVID-19 had far less of an impact on leveraged finance markets than expected. Activity dropped in the second quarter of 2020, primarily in leveraged loan issuance, but a year later numbers returned to pre-pandemic levels. In fact, leveraged loan and high yield bond values reached record highs by the end of Q1 2021—the highest quarter since Q2 2018 and the second-highest quarter, respectively, on Debtwire Par record going back to 2015.

What drove this relatively high-speed recovery? First, the Coronavirus Aid, Relief and Economic Security (CARES) Act, signed into law in March 2020, protected many businesses from the full brunt of the pandemic. At the same time, many businesses shored up their finances, taking on debt to ensure liquidity as lockdown measures continued to have an impact through the second half of 2020. Issuances rose and that upward trajectory carried on into 2021.

By the end of Q1 2021, the picture had changed once again. Vaccines were being distributed quickly and efficiently, raising hopes for a post-COVID-19 future. The economy was also improving, as various states began to open up and a year of pent-up consumer demand was released. By May, core retail sales in the US had reached levels typically only seen over the Christmas period, according to the National Retail Federation. An air of optimism crept into the market, with lenders increasingly willing to take more risks on borrowers in their pursuit of yield. Financing earmarked for M&A and buyout activity also began to climb, hinting at growth plans for the months ahead. Perhaps most significantly, the low interest rate environment gave businesses an opportunity to reprice and refinance their maturing debt in droves.

What's next for 2021?

While these are all very positive signs for lenders in the leveraged finance space, there are still a few red flags on the horizon. First is inflation—in July, the Bureau of Labor Statistics reported that the US consumer price index had climbed 5.4 percent in the 12 months to June, a level not seen in 13 years. These growing inflationary pressures are part of the rush to reprice and refinance existing debt, as businesses try to avoid any unpleasant surprises if interest rates begin to climb as well.

Second, companies in robust sectors that enjoyed a degree of preferential treatment from lenders during the pandemic may find that sentiment shifting in the months ahead as other sectors begin to recover. The "flight to quality" witnessed in the early days of the pandemic will likely return to a more evenly balanced state of affairs. Documentation may also go through some changes in the coming months, as adjustments brought in during COVID-19 are phased out.

Finally, as the dust settles in debt markets, issues that were gaining ground before the pandemic will return in force, especially environmental, social and governance factors, which continue to take on increasing importance among borrowers and lenders alike.

All of which means the road ahead is not quite as clear as many would like, but there will be fewer obstacles blocking the path.

The US leveraged finance story so far

Leveraged loan issuance reached US$763.5 billion in the first half of 2021, up 60 percent from US$478.1 billion in the same period in 2020

High yield bond market issuance also rose 22 percent year-on-year, from US$219.6 billion to US$267.1 billion

Refinancings and repricing deals accounted for 62 percent of overall loan issuance in H1 2021

How distressed companies are avoiding full-blown bankruptcies

Announced US corporate bankruptcies climbed to 630 cases in 2020, according to Standard & Poor's—up from 2019 levels, but still lower than expected

Bankruptcies ticked higher early in 2021—from 14 cases in January to 23 cases in March, before dropping to 11 in June—but are still well below 2020 levels according to Debtwire Par

Covenant relief and uptiering, as well as drop down deals and other liability management structures have offered companies a variety of levers to pull to avoid entering bankruptcy situations

Refinancing, repricing, M&A and buyout activity all surged in the early months of 2021, but then lenders shifted gears in pursuit of yield and borrowers realized they could tap the market for more than just liquidity. Where will this fork in the road lead for the rest of 2021?

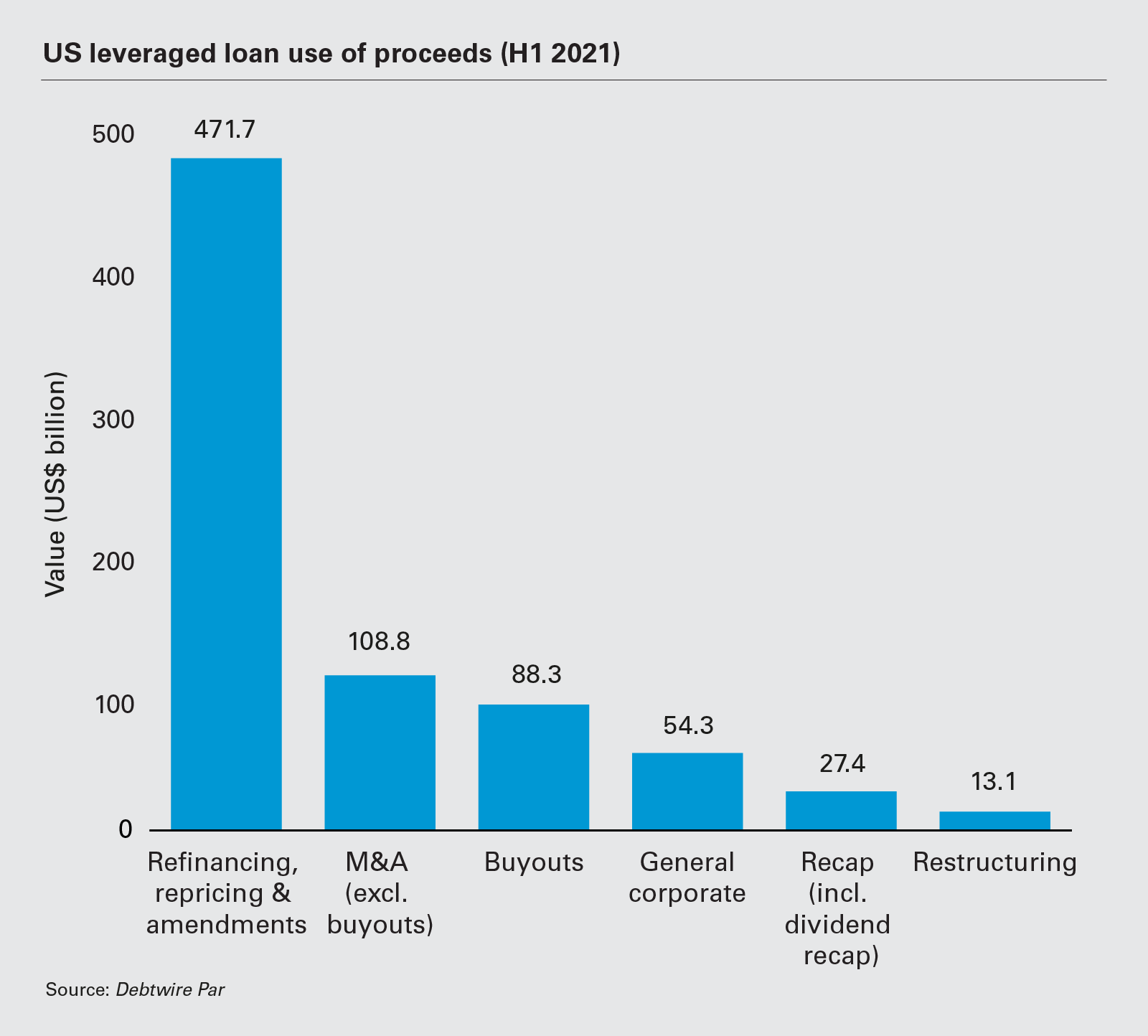

Refinancing and repricing in US leveraged loan markets surged to US$471.7 billion over the first six months of 2021

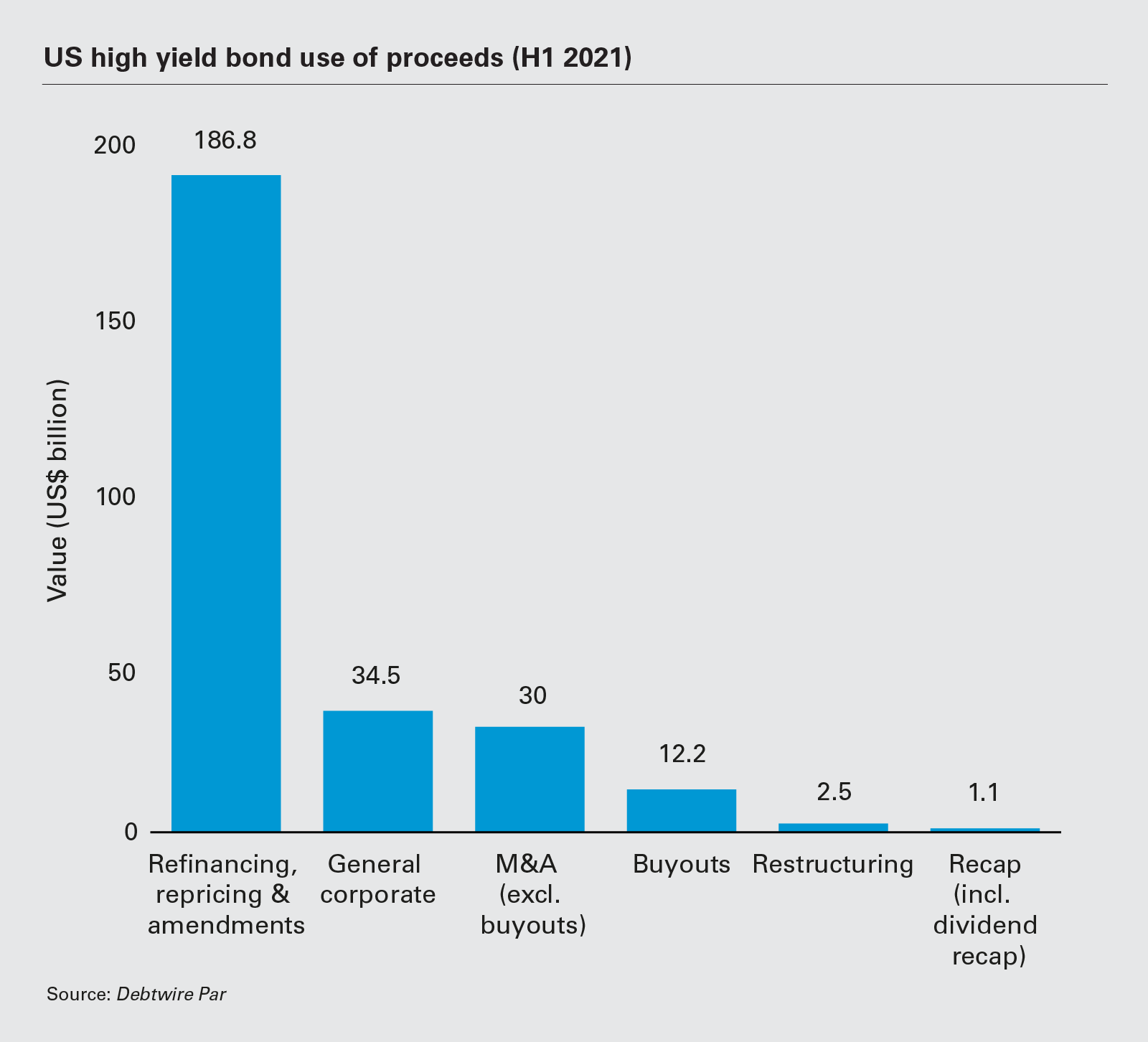

US high yield bond refinancing accounted for 70 percent of total high yield issuance

Amend-and-extend deals give borrowers further breathing room

The extension of maturities has reduced near-term risk of default and limited the number of borrowers running out of cash and facing bankruptcy

Abundant liquidity, a red-hot refinancing market and improving credit ratings combined through the first half of 2021 to limit defaults and ease any near-term pressure on the balance sheets of US borrowers.

Borrowers have found lenders open and amenable to refinancing existing loans and bonds. Refinancing and repricing in US leveraged loan markets totaled US$471.7 billion over the first six months of 2021, a 79 percent year-on-year rise that represents almost two-thirds of total issuance for the year. US high yield bond refinancing accounted for 70 percent of total high yield issuance, climbing 48 percent year-on-year to US$186.8 billion by the end of June 2021.

79% Refinancing and repricing in US leveraged loan markets totaled US$471.7 billion over the first six months of 2021, up 79% year-on-year

The high levels of refinancing activity have strengthened the underlying credit fundamentals of borrowers, who have been able to extend maturities and either lock in lower pricing or increase the size of borrowing facilities.

Atlanta-based payments company Fleetcor Technologies, for example, refinanced its securitization term loan B facilities to lock in close to US$2 billion of liquidity at lower rates and with longer maturities.

Borrowers have also had the option to amend-and-extend the terms on their loans to push out any imminent maturity cliff edges. According to ratings agency Standard & Poor's, US$41 billion in amend-and-extend deals were secured for the year to the end of April 2021—up year-on-year and already more than half of the annual amend-and-extend activity posted in all of 2018 and 2020.

The capacity in the market to either amend-and-extend terms or refinance deals in such high volumes has all but removed the risk of defaults for borrowers that were running low on liquidity due to COVID-19 lockdowns and approaching maturity walls.

According to Standard & Poor's, the volume of loans falling due between 2021 and 2023 was reduced by US$198.3 billion between the end of 2019 and the end of April 2021. The volume of loans falling due in 2024 and 2025 dropped by US$135.1 billion over the same period. Longer-dated maturities due in 2026 or later, meanwhile, have swelled to US$348.4 billion as maturities have been pushed out and borrowers kick the can down the road.

With the threat of a maturity cliff edge effectively averted, default rates have decreased and credit ratings have improved. In June, ratings agency Fitch lowered its leveraged loan and high yield bond default rates forecasts for 2021 to 1.5 percent and 1 percent respectively. And as corporate balance sheets stabilized and company earnings improved, the credit ratings environment is looking far healthier—according to Debtwire Par's Ratings Tracker, in the last two weeks of June, out of the 153 actions taken for 137 companies, just six percent were changed to "negative"ratings.

The benign default rates and improving credit ratings observed so far in 2021 stand in stark contrast to the distress and volatility seen a year ago. In the first half of 2020, ratings downgrades became a feature of the market: 101 companies downgraded in June following 121 downgrades in May, 230 downgrades in April and 169 downgrades in the second half of March, according to the Debtwire Par Ratings Tracker.

The wave of downgrades was accompanied by a spike in default rates, which climbed to 4.5 percent among institutional loans in 2020, up from 1.7 percent in 2019, representing the highest levels observed since 2009 in the aftermath of the global financial crisis. High yield bond default rates, meanwhile, spiked from approximately 3 percent in January 2020 to close to 6 percent by the middle of the year.

The surge in default rates and ratings downgrades never led to the anticipated levels of deep financial distress and restructurings, as borrowers refinanced or amended-and-extended their loans and bonds. Cases where companies ran out of cash and faced chapter 11 bankruptcy were kept to a minimum as a result. The rising number of credit ratings upgrades is expected to keep this supportive backdrop in place through the rest of 2021, especially as it will encourage sustained demand from collateralized loan obligation (CLO) managers, whose targets are linked to ratings.

With ratings improving, CLOs will have a significant influence on the levels of liquidity available in the market—new CLO issuance over the first six months of 2021 was up 140 percent year-on-year at US$80.56 billion, supported by this trend of improved ratings.

The wave of US debt restructurings anticipated during the depths of the COVID-19 debt crisis appear to have been put on hold—at least for now.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image 'US leveraged loan use of proceeds (H1 2021)' PDF

View full image 'US leveraged loan use of proceeds (H1 2021)' PDF

View full image 'US high yield bond use of proceeds' (PDF)

View full image 'US high yield bond use of proceeds' (PDF)