What will drive issuance in a post-COVID-19 world?

Foreword

Halfway through 2021, we take stock of leveraged finance in the United States and consider the road ahead for both borrowers and lenders. After more than a year of COVID-19, are things returning to normal? Or are we just starting a whole new journey?

In many ways, COVID-19 had far less of an impact on leveraged finance markets than expected. Activity dropped in the second quarter of 2020, primarily in leveraged loan issuance, but a year later numbers returned to pre-pandemic levels. In fact, leveraged loan and high yield bond values reached record highs by the end of Q1 2021—the highest quarter since Q2 2018 and the second-highest quarter, respectively, on Debtwire Par record going back to 2015.

What drove this relatively high-speed recovery? First, the Coronavirus Aid, Relief and Economic Security (CARES) Act, signed into law in March 2020, protected many businesses from the full brunt of the pandemic. At the same time, many businesses shored up their finances, taking on debt to ensure liquidity as lockdown measures continued to have an impact through the second half of 2020. Issuances rose and that upward trajectory carried on into 2021.

By the end of Q1 2021, the picture had changed once again. Vaccines were being distributed quickly and efficiently, raising hopes for a post-COVID-19 future. The economy was also improving, as various states began to open up and a year of pent-up consumer demand was released. By May, core retail sales in the US had reached levels typically only seen over the Christmas period, according to the National Retail Federation. An air of optimism crept into the market, with lenders increasingly willing to take more risks on borrowers in their pursuit of yield. Financing earmarked for M&A and buyout activity also began to climb, hinting at growth plans for the months ahead. Perhaps most significantly, the low interest rate environment gave businesses an opportunity to reprice and refinance their maturing debt in droves.

What's next for 2021?

While these are all very positive signs for lenders in the leveraged finance space, there are still a few red flags on the horizon. First is inflation—in July, the Bureau of Labor Statistics reported that the US consumer price index had climbed 5.4 percent in the 12 months to June, a level not seen in 13 years. These growing inflationary pressures are part of the rush to reprice and refinance existing debt, as businesses try to avoid any unpleasant surprises if interest rates begin to climb as well.

Second, companies in robust sectors that enjoyed a degree of preferential treatment from lenders during the pandemic may find that sentiment shifting in the months ahead as other sectors begin to recover. The "flight to quality" witnessed in the early days of the pandemic will likely return to a more evenly balanced state of affairs. Documentation may also go through some changes in the coming months, as adjustments brought in during COVID-19 are phased out.

Finally, as the dust settles in debt markets, issues that were gaining ground before the pandemic will return in force, especially environmental, social and governance factors, which continue to take on increasing importance among borrowers and lenders alike.

All of which means the road ahead is not quite as clear as many would like, but there will be fewer obstacles blocking the path.

The US leveraged finance story so far

Leveraged loan issuance reached US$763.5 billion in the first half of 2021, up 60 percent from US$478.1 billion in the same period in 2020

High yield bond market issuance also rose 22 percent year-on-year, from US$219.6 billion to US$267.1 billion

Refinancings and repricing deals accounted for 62 percent of overall loan issuance in H1 2021

How distressed companies are avoiding full-blown bankruptcies

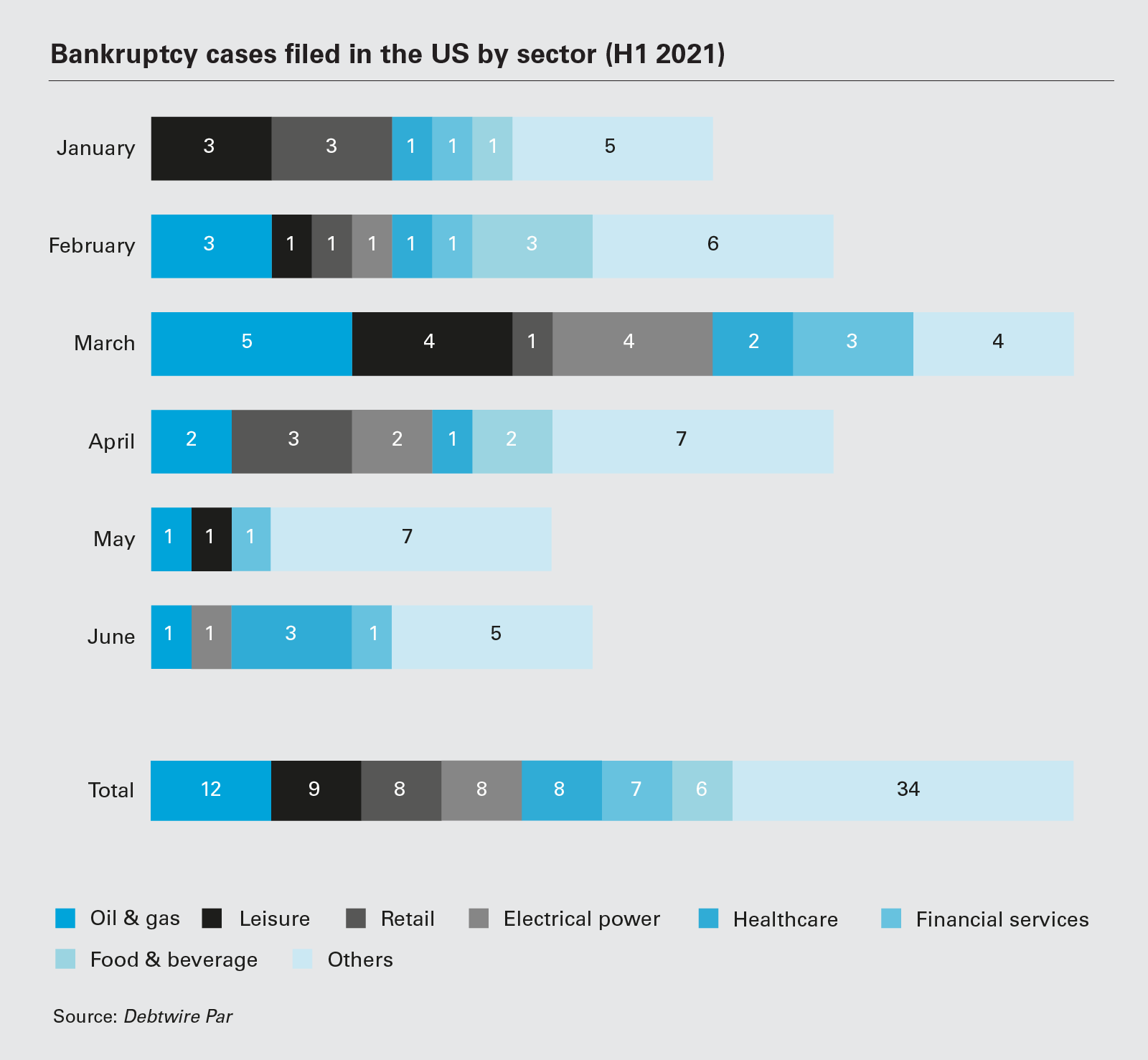

Announced US corporate bankruptcies climbed to 630 cases in 2020, according to Standard & Poor's—up from 2019 levels, but still lower than expected

Bankruptcies ticked higher early in 2021—from 14 cases in January to 23 cases in March, before dropping to 11 in June—but are still well below 2020 levels according to Debtwire Par

Covenant relief and uptiering, as well as drop down deals and other liability management structures have offered companies a variety of levers to pull to avoid entering bankruptcy situations

Refinancing, repricing, M&A and buyout activity all surged in the early months of 2021, but then lenders shifted gears in pursuit of yield and borrowers realized they could tap the market for more than just liquidity. Where will this fork in the road lead for the rest of 2021?

Announced US corporate bankruptcies climbed to 630 cases in 2020, according to Standard & Poor's—up from 2019 levels, but still lower than expected

Bankruptcies ticked higher early in 2021—from 14 cases in January to 23 cases in March, before dropping to 11 in June—but are still well below 2020 levels according to Debtwire Par

Covenant relief and uptiering, as well as drop down deals and other liability management structures have offered companies a variety of levers to pull to avoid entering bankruptcy situations

23 Bankruptcies in the US climbed from 14 cases in January 2021 to 23 in March, but are still below the levels seen in 2020

Management teams and private equity (PE) sponsors have successfully deployed a range of liability management tools to steer companies through the COVID-19 downturn and avoid both bankruptcies and full-blown restructurings.

According to Standard & Poor's, US corporate bankruptcies climbed from 580 in 2019 to 630 in 2020. Although volumes did rise, the number of bankruptcies came in significantly lower than anticipated, and well down from the 819 recorded in 2010 in the aftermath of the global financial crisis.

Although Debtwire Par figures show an uptick in bankruptcy filings from 14 cases in January to 23 in March 2021, volumes are still low year-on-year. Monthly bankruptcy totals consistently exceeded 25 in the first half of 2020, pushing to as high as 40 cases in July 2020 and 37 cases in May 2020.

The relatively benign levels of bankruptcies reflect a combination of factors that have favored distressed companies, giving them time to manage their liabilities without resorting to bankruptcy.

One major factor that has helped borrowers navigate COVID-19 volatility is that the lion's share of outstanding debt has been issued with covenant-lite terms. A covenant-lite loan has fewer covenants to protect the lender and fewer restrictions on the borrower regarding payment terms, income restrictions and collateral (e.g., no maintenance covenants that default due to deterioration of financial performance alone).

According to Standard & Poor's, more than 80 percent of the S&P/LSTA Leveraged Loan Index (which tracks the performance of the largest US institutional leveraged loans) is composed of covenant-lite loans—compared to a share of just 15.5 percent at the end of 2008. This offered much-needed breathing room to companies that saw earnings flatline and leverage multiples mushroom during the pandemic, developments that would have tripped financial maintenance covenants if not for covenant-lite terms.

Even debt instruments that continue to have financial maintenance covenants—primarily pro rata revolving credit facilities and amortizing loans that are held by banks post-syndication—have been able to obtain covenant relief from lenders to help them through this volatile period. But this relief has often come at a cost.

According to Standard & Poor's, by the end of April 2021, there were 15 covenant relief deals, which is consistent with pre-pandemic levels. Although less than half the number of covenant relief deals observed over the same period last year, the option has remained open for borrowers even as capital markets have rebounded and, in fact, thrived post-pandemic.

When borrowers have pushed up against potential breaches of financial maintenance covenants, lenders that agreed to offer covenant relief typically did so in return for newly inserted liquidity-based covenants that required borrowers to share cash-flow projections of up to 13 weeks with lenders, as well as hold lender calls to outline financial performance expectations, and maintain certain minimum liquidity levels.

Even borrowers that have been running out of cash and have not been positioned to raise additional capital have used innovative tools to avoid bankruptices, de-lever their balance sheets, reduce their overall interest expense and extend their debt maturity profiles

Dropping down and uptiering

Even borrowers that have been running out of cash and have not been positioned to raise additional capital have used innovative tools to avoid bankruptices, de-lever their balance sheets, reduce their overall interest expense and extend their debt maturity profiles.

Companies facing various pandemic, industry and other headwinds have taken advantage of flexibility in documentation through so-called "asset drop down" and "uptiering" deals.

Asset drop down transactions (which often use flexibility found through using unrestricted subsidiaries) have seen borrowers use flexibility present in their existing debt documentation to transfer valuable assets and collateral out of the restricted group that benefits the senior secured creditors. In these deals, assets (often intellectual property) have been transferred into new "unrestricted" subsidiaries that can raise additional debt using those assets as collateral, or can be sold without the restrictions imposed by existing debt documentation.

Lenders have been moving, as and when opportunities arise, to shut down this flexibility through unrestricted subsidiary blocker terms, which provide that certain "core" assets are prohibited from being transferred to unrestricted subsidiaries. But, over the past 12 months, borrowers have nonetheless been able to bring in additional liquidity by using drop down flexibility.

In uptiering deals, meanwhile, borrowers have structured transactions pursuant to which they offer certain existing senior creditors the opportunity to exchange some debt instruments (often at a discount to par) for new instruments that layer into new structurally senior positions in the capital structure. This has proven an effective way for borrowers to reduce leverage and improve their liquidity profiles by reducing debt service, while also extending their debt maturity profiles to provide additional runway to navigate challenging industry landscapes. However, in some instances, this has triggered litigation in US courts by lenders that were excluded from this uptiering.

As has been the case with asset drop down deals, lenders are zeroing in on terms in new deals, and in the context of amendment and waiver discussions, to block uptiering.

Uptiering and drop down deals have proven valuable tools for borrowers but, as capital markets have recovered, borrowers have not had to turn to these options as frequently. Borrowers that have not benefited from this recovery, but whose tools have been locked away through blocker provisions, continue to seek ever-more creative options to raise liquidity—which may account for the recent rise in interest for preferred equity structures.

A big rebound in secondary prices for debt has reduced the opportunity to capture discount through uptier transactions.

In June 2020, the average price for debt in the secondary loan market was trading at 85.51 percent of par. In June 2021, prices averaged 97.95 percent of par. High volumes of refinancing activity have also given borrowers greater flexibility to extend maturities and lower financing costs.

Innovative structures that use the flexibility found in debt documentation have provided, and will continue to provide, valuable tools that distressed companies can deploy to manage their balance sheets through challenging market backdrops.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image 'Bankruptcy cases filed in the US sector (H1 2021)' PDF

View full image 'Bankruptcy cases filed in the US sector (H1 2021)' PDF