Senior unsecured trust certificates (commonly known as sukuk) are now regularly issued in the capital markets. Most commonly, these are issued by Shari'a compliant companies to raise funds in international capital markets in the form of trust certificates. The Global Islamic finance industry grew by 10.6% in 20241 and is expected to grow to US$6.67 trillion by 20272. Although, Islamic finance still represents a small percentage of global finance and capital markets, there is continued appetite from investors for such products with total trust certificate issuances amounting to US$193.4 billion in 2024, slightly down from $197.8 billion a year earlier but with a significant increase in foreign currency-denominated issuances.

Trust certificates adopt novel structures and in this client briefing we discuss a variation of trust certificates that could be utilised by issuers with listed or unlisted shares. These are "Exchangeable Trust Certificates" which adopt and combine the existing structure of trust certificates and exchangeable bonds.

Key Concepts: Trust Certificates and Exchangeable Bonds

To understand the concept of an Exchangeable Trust Certificate, it is important to first understand the following:

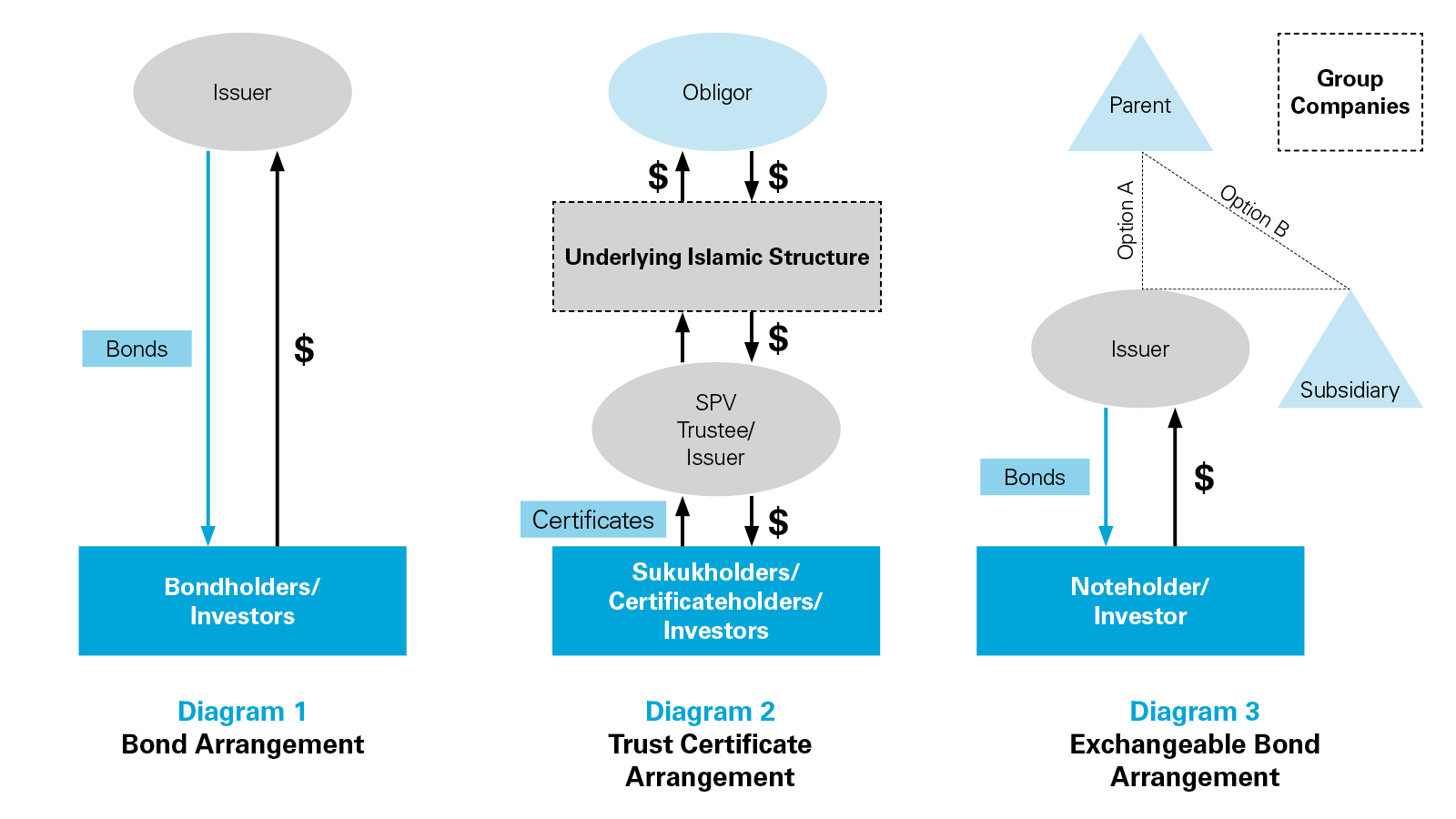

What are Trust Certificates?

A trust certificate is an Islamically compliant bond which returns profit, rather than interest, to investors (who are known as the "Certificateholders"). Trust certificates put investors in the same economic position as investors under a conventional bond and can be listed and are tradeable. However, due to various Shari'a and structuring considerations there is one key distinction to note: the issuer of the trust certificates will be a special purpose vehicle ("SPV"), which is usually incorporated in a tax-free jurisdiction (such as the Cayman Islands) with its shares held on trust for charitable purposes.

It is called a trust certificate because the issuer SPV (also known as the "trustee"), declares a trust over the proceeds raised by the issuance and the Certificateholders have an entitlement interest in such proceeds and the assets of the trust. The proceeds raised from the issuance are then used by the trustee to enter into various Shari'a compliant transactions with an obligor. The obligor will be bound by payment obligations to the trustee under such Shari'a compliant transactions, which will then be used to repay the profit under the trust certificate along with the "Dissolution Amount" (known as the principal under a conventional bond). Under a trust certificate, the ultimate credit of the transaction is in respect of the obligor and its ability to fulfil its payment obligations.

What are Exchangeable Bonds?

An exchangeable bond is a hybrid debt security which may be issued in the form of a conventional bond. At either a) maturity, or b) the exercise of an option or put (known as the "Exchange Date"), the bond is exchanged for shares in a third party or an affiliate company of the issuer (the "Affiliate Company"), such as the issuer's parent or subsidiary. This is presented as Option A and Option B under Diagram 3 below.

Under a mandatory conversion, the bonds will be exchanged for shares on the Exchange Date. Alternatively, the issuers or the bondholders may have a contractual right, known as an "option" in respect of the issuer and a "put" in respect of the bondholder, to determine whether they wish to exercise the exchange of the bonds into shares. In the case of a contractual right to exchange, any bonds in respect of which such option or put is not exercised, will be redeemed for the principal.

(This is not to be confused with convertible bonds, under which the bonds are converted into shares of the issuer itself rather than an Affiliate Company. An investor's assessment of the viability of the investment in an exchangeable bond will be based on the quality and performance of the Affiliate Company, while under a convertible bond, the assessment will remain on the issuing company on the Exchange Date and beyond.)

Key elements of an exchangeable bond are the "Exchange Price" (i.e., the pre-determined price at which the bond can be exchanged for the shares of the Affiliate Company) and the "Exchange Ratio" (the ratio setting out the number of shares exchanged for each bond) which are specified in the terms and conditions.

Having considered this product, our view at White & Case is that an exchangeable bond is adaptable to the structure of trust certificates

What is the connection between a Trust Certificate and an Exchangeable Bond?

Upon the maturity date of trust certificates, the Certificateholders will be repaid the initial price they paid for the purchase of the trust certificates i.e., the Dissolution Amount. This Dissolution Amount is paid by the obligor to the trustee pursuant to the underlying Islamic structure. The trustee will then use the funds to pay the Certificateholders (and the trust is dissolved).

As discussed above, upon the maturity date of an exchangeable bond, the investors will receive shares in an Affiliate Company of the issuer. While the relationship between the trustee and the obligor under a trust certificate is not a parent-subsidiary or affiliate relationship, the transaction could be structured so that upon the maturity date, the payment obligation of the obligor to pay cash proceeds to the trustee is replaced with an obligation by the obligor to deliver shares within itself, or another group company of the obligor to the trustee. The trustee can then use such shares to redeem the trust certificates.

View full image: Exchangeable Sukuk (PDF)

View full image: Exchangeable Sukuk (PDF)

Key Considerations for Exchangeable Trust Certificates

Listed Shares? – In the context of an international issuance of Exchangeable Trust Certificates, investors will most likely want any shares they receive to be liquid (i.e., tradeable for cash) as well as being easily and freely transferable. This is to avoid investors holding shares which will be difficult to dispose. Consequently, listed shares which are to be exchanged for the trust certificates may be more desirable.

Exchangeable Trust Certificates issued by the holding companies of start-ups, which have potential for future initial public offerings ("IPO"), may also prove popular for such securities. Investors are likely to be drawn by the idea of receiving shares in a company pre-IPO at a lower price than the market value of the shares upon or after an IPO.

Origination of Shares – The shares which will be exchanged for the trust certificates must be available at the Exchange Date

- Issuance of New Shares and EGM Approval – The company, whose shares will be offered for exchange (the "Exchanging Company"), may issue shares in advance of the Exchange Date so they are readily available for the exchange. For such company to issue shares, it may be required to obtain approval from existing shareholders, pursuant to applicable laws and regulations and its constitutional documents. This may require the Exchanging Company to put such issuance to a vote at an "Extraordinary General Meeting" (which will need to be coordinated in advance as it is a lengthy process). The Exchanging Company will also have to consider whether it has sufficient shares to issue new shares and consider whether there will be any risk of dilution for existing shareholders, which may make the proposal less attractive to voting shareholders.

- What about Reserves? – Any shares held by a) the Exchanging Company in itself, or b) a shareholder willing to sell and offer such shares for the purpose of the exchange, in the context of international transactions will need to be made public and listed, which, as discussed, adds additional time to the transaction. Furthermore, issuing new shares or using privately held shares and bringing them to the public market may be classified as an IPO, which will bring even greater complexity.

Global Master Repurchase Agreement ("GMRA") – Investors in the international capital markets may typically require shares to be in existence and available for the exchange at the outset of the transaction to avoid any complications or delay at the Exchange Date. This can be achieved through a repo transaction, under which a large shareholder of the Exchanging Company will lend the shares to an arranger under the transaction. Pursuant to this, investors can have assurance that the shares their trust certificates will be exchanged for have been set aside and are available for exchange at the Exchange Date. Upon the Exchange Date:

- The arranger delivers the required number of shares to the Certificateholders in exchange for the Exchangeable Trust Certificate.

- Once the Certificateholders have received the shares, the Exchangeable Trust Certificates are effectively cancelled as specified in their terms and conditions.

- The arranger will need to return an equivalent number of shares to the original shareholder at the end of the lending period specified in the GMRA.

- If the exchange does not occur (applicable under non-mandatory exchange transactions) i.e., where the Certificateholders do not exercise their exchange right under the put or the trustee does not exercise its option, the arranger returns the borrowed shares to the original shareholder at the end of the lending period.

This mechanism ensures that the shares are available for exchange, thereby providing confidence to international investors in the integrity of the Exchangeable Trust Certificates. To determine whether this is a viable route, the following must be considered:

- Are there any shareholders who have shares available to be lent under the GMRA?

- Is this permitted under the regulation and rules of the applicable listing authority and stock exchange?

- How to transfer the shares away from the shareholder and under the control of the arranger?

- Pre-Emption Rights – If the Exchangeable Trust Certificates are to be settled using newly issued shares, then this may trigger pre-emption rights of existing shareholders. This will need to be considered on a case-by-case basis and will necessitate reviewing the Exchanging Company's constitutional documents, the requirements of any stock exchanges where the shares are listed and applicable laws and regulations to determine if this will be an issue. There may be exemptions to the pre-emption rights or structures, such as a cashbox structure, which can be used to circumvent the application of pre-emption rights.

- Anti-Dilution and Takeovers – The terms and conditions of the Exchangeable Trust Certificates may contain anti-dilution provisions which result in adjustments to the Exchange Ratio if the Exchanging Company undergoes corporate actions such as stock splits, bonus issues, or rights offerings. The Exchange Ratio will be adjusted accordingly and aims to maintain the Certificateholders value and equity stake despite changes in the share structure. Additionally, in the event of a takeover or merger, these provisions may also provide for modifications to the exchange terms to protect Certificateholders from adverse impacts, ensuring they receive equivalent value in the newly structured company.

Regulation – The laws and regulations of the jurisdiction of the Exchanging Company will need to be reviewed and assessed to determine whether an exchange is permitted. It would need to be considered whether there is an existing legislative framework which regulates exchangeable securities or whether there is an analogous regime that is applicable. A review of the applicable equity offering rules will also be required. The relevant regulator for the Kingdom of Saudi Arabia ("KSA") would be the Capital Markets Authority ("CMA") and for onshore United Arab Emirates ("UAE") it would be the Securities and Commodities Authority ("SCA").

Shareholder Approval – The Exchanging Company must ensure they hold the required shareholder approvals under the applicable companies laws and regulations for the transaction and the issuance of shares.

An Exchanging Company in the UAE will need to take into consideration the UAE Companies Law (Federal Decree-Law No. 32/2021 on Commercial Companies) and any regulations issued by the SCA. By the Exchange Date, a special resolution is required to have been passed by the shareholders of an Exchanging Company which is a joint-stock company. This requires shareholders holding at least three-quarters of the shares represented in a general assembly meeting to have approved the issuance of any shares. If such shares are to be listed, an application will also need to be made to the SCA.

An Exchanging Company in the KSA will need to take into consideration the KSA Companies Law (Royal Decree No. (M/132) of 1443) and any regulations issued by the CMA. In particular, the CMA's Rules of the Offer of Securities and Continuing Obligations (Issued by the Board of the Capital Market Authority pursuant to its Resolution Number 3-123-2017 dated 9/4/1439 corresponding to 27/12/2017 as amended from time to time). By the Exchange Date, an extraordinary general assembly of the Exchanging Company will be required to have approved the issuance of the shares. This will require a three-quarters majority of the voting shares represented at the meeting of the extraordinary general meeting to approve the issuance. If such shares are to be listed, an application will also need to be made to the CMA.

Other jurisdictions may have different requirements which will need to be assessed on jurisdiction-specific and a deal-by-deal basis.

Exchange Ratio – The Exchanging Company and issuer will need to consider the Exchange Ratio upon which the trust certificates will be exchanged for shares i.e., for each dollar of the trust certificate, how many shares or fractional shares would an investor receive following the exchange? This Exchange Ratio may be fixed at the outset of the issuance of the trust certificates under the terms and conditions or it may be floating and subject to commercial and market considerations.

Shari'a Compliance? – As Shari'a compliance is likely to be a key consideration for investors in such securities, the trust certificates should be exchanged for shares in an Exchanging Company which is Shari'a compliant. Where the Exchanging Company is the obligor, this would not be a point of concern, as non-Shari'a compliant entities cannot act as obligors under trust certificates. However, if the Exchanging Company is not the obligor, investors may have greater scrutiny to ensure the shares they obtain do not raise any issues from a Shari'a perspective.

What are the Benefits?

Investors – Investing in Exchangeable Trust Certificates mitigates the risk of non-payment and provides investors with a layer of protection from total loss, while also allowing them to benefit from capital appreciation if the underlying shares perform well and increase in value.

Issuers

- Cost effective borrowing, as the profit rate for Exchangeable Trust Certificates may be lower than a standard trust certificate (which may be the expectation for conventional bonds compared to exchangeable bonds).

- Flexibility in terms, as Exchangeable Trust Certificates may have a longer maturity and optionality of not repaying the debt.

- Wider investor base, this instrument may introduce the issuer, obligor and Affiliate Company to investors outside its domestic or usual base of investors and will diversify its source of funding.

- Better treatment of equity, enabling an issuer to raise funding at a more appropriate price where the Exchanging Company's shares are undervalued in the market. Furthermore, on the Exchange Date, the shares may be exchanged at a premium, resulting in fewer shares being offered or having to be issued as compared to the market price (although this will be transaction specific).

Are Exchangeable Trust Certificates ready for market adoption?

As Islamic finance expands and proves to be a stable source of funding for issuers in the region, new innovative structured instruments, like Exchangeable Trust Certificates, have potential in this environment. The demand for such products may be across both the domestic capital markets, as well as international capital markets. The structure of Exchangeable Trust Certificates, which provides the option to exchange debt for equity, can be highly advantageous for issuers seeking effective liability management. This exchange option offers flexibility, enabling issuers to optimise their capital structure based on market conditions and strategic objectives.

1 htps://www.spglobal.com/ratings/en/research/articles/250417-islamic-finance-2025-2026-resilient-growth-amid-upcoming-headwinds-13453768

2 https://www.lseg.com/en/insights/data-analytics/islamic-finance-global-industry-on-track-towards-projected-growth

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP