In November of 2021, President Biden signed the Bipartisan Infrastructure Law (BIL), which established the Regional Clean Hydrogen Hubs (H2Hubs) program. Under the authority of the US Department of Energy (DoE), six to ten hydrogen hub projects — eligible for up to $1.25 billion in federal funding, respectively — were to be selected. The formal application process closed on April 7, 2023, and on October 13, 2023, President Biden announced the awardees.

Federal policy objectives & resource overview

The BIL authorized a total of $8 billion in federal funding for hydrogen development, with the bulk allocated to the H2Hubs program. Under the new Section 813 of Title VIII of the Energy Policy Act of 2005, the program is envisioned to create a network of clean hydrogen producers, potential clean hydrogen consumers, and connective infrastructure located in close proximity. While the program is intended to stimulate the development of the entire hydrogen value chain, the H2Hubs program is intended to substantially reduce costs associated with the production, distribution and consumption of green hydrogen, which dovetails with the targets set by DoE for 10 million metric tons of clean hydrogen by 2030, 20 million by 2040, and 50 million by 2050.

To support the proliferation of hydrogen as a critical component of the energy industry, the Inflation Reduction Act of 2022 (IRA) also included tax credits for new investments in hydrogen production capacity. Most recently, in September of 2023, DoE issued a request for proposals (RFP) for an independent entity to administer a demand-side initiative to work with the H2Hubs awardees in order to reach efficient operation and cooperation between producers and end users. DoE will provide $500 million to $1 billion to the selected entity; applications for the RFP are due on October 26, 2023.

From a market perspective, hydrogen is not yet fully competitive relative to other fuels due to its complex supply chain — including nascent segments such as liquefaction and transportation. While the density of the energy potential of Hydrogen is readily apparent, the market requires substantial investment and growth until it can be competitive with oil and gas. The current state of the market is relatively similar to the early stages of the liquefied natural gas (LNG) market, with industry participants working to determine the most efficient technologies for liquefaction, uncertainty about the supply chain, and competing opinions about the most efficient methodology for long-distance transportation and the development of an eventual spot market. For now, it seems as if the conversion of hydrogen into ammonia for long-haul shipping is the leading technology, and offtake for use as a blending fuel with natural gas for power generation and development of fertilizer are early demand centers for the future hydrogen that will be produced.

To achieve early synergy with clean hydrogen goals while green hydrogen continues to move towards competitiveness and scale over the longer term, hydrogen hubs may incorporate fuel blending. By adding hydrogen to existing natural gas supply, the hubs may be able to reduce the carbon intensity of existing production facilities (such as oil refineries, ammonia production for fertilizer manufacturing, and steelmaking) and, accordingly, act in pursuit of the overarching climate goals of the Bipartisan Infrastructure Law. This will require infrastructure improvements beyond production of hydrogen, and the H2Hubs program could also stimulate the development of technology to enable hydrogen to utilize existing natural gas midstream assets. In the coming years, green hydrogen may be able to replace blended fuels in a wider range of applications at production facilities.

As it stands, blue hydrogen is generally the most cost-competitive with other fuels, and is the leading hydrogen source for use in refineries and for production of ammonia and methanol. Green hydrogen may become more competitive in future years due to expected technological advancements and supply chain efficiencies spurred by programs such as H2Hubs and other policies incentivizing production technologies beyond steam-methane reformation into areas such as renewable electrolysis, biomass gasification and methane pyrolysis.

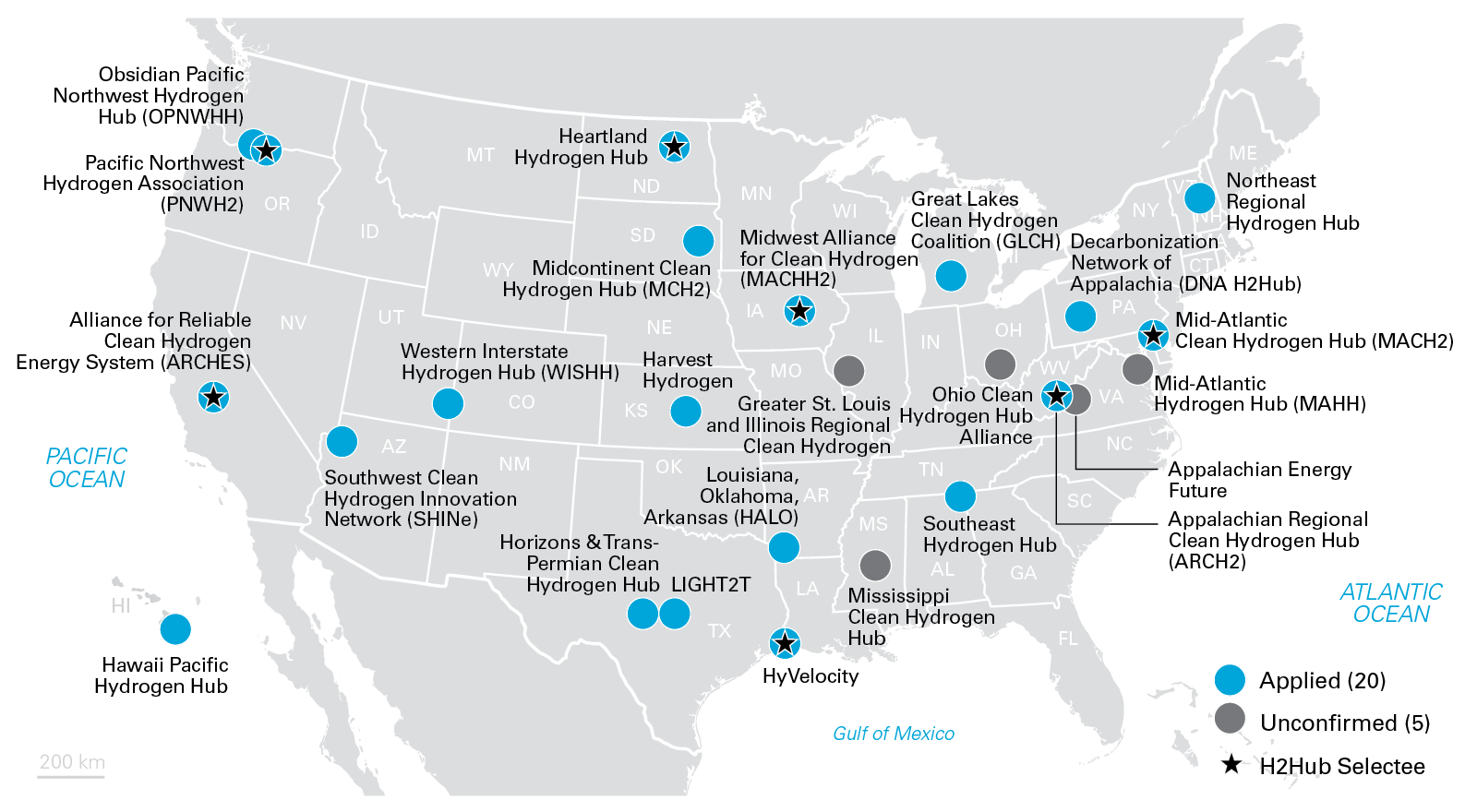

Profile of applicants & proposed hubs

Following the passage of the Bipartisan Infrastructure Law, and corresponding federal funding allocated to hydrogen development, 79 applicants submitted concept papers to the federal government regarding potential hubs. On December 27, 2022, DoE issued notices of encouragement to 33 of those projects. Based on publicly-available information — such as press releases or responses to media inquiries — 20 of those proposed hubs confirmed that applications had been submitted to the DoE Office of Clean Energy Demonstrations (OCED) prior to the April deadline, two hubs indicated that they had merged, two hubs did not respond to inquiries, and the status of the remainder are yet unknown. DoE stated that prospective applicants that had not been expressly encouraged were not barred from submitting their own applications, however.

View full image (PDF)

View full image (PDF)

The range of location, capacity, feedstock, and end use varies significantly among the known applicants. According to the submissions, proposed hubs would produce anywhere from 1,900 to 9,000 metric tons of hydrogen per day. With regard to feedstock, the majority of the proposed hubs would use renewable energy resources, but several would use fossil fuels (namely, the Appalachian Regional Clean Energy Hub in West Virginia and the Heartland Hydrogen Hub in North Dakota, Minnesota, Montana, and Wisconsin). Notably, DoE stated that at least two of its selections would be situated in regions with high natural gas resources; in addition to the two hubs mentioned prior, there were other applicants in Texas and the Appalachian region (six in total, three for each) that sought to leverage their respective abundant shale reserves. DoE also indicated that it would prioritize hubs using steam reformation in order to capture carbon dioxide, with flexible use cases ranging from underground injection or for industrial and manufacturing purposes.

The public-private teams are comprised of entities across the energy sector, from utility companies to oil and gas majors. Additionally, many of the projects would be led by state governmental bodies or agencies as well as supported by educational institutions, including the University of Texas for the proposed HyVelocity Hub, which sought to partner with several oil and gas companies. The Western Interstate Hydrogen Hub was to be located in Colorado, New Mexico, Utah, and Wyoming would include the DoE’s own National Renewable Energy Lab and Sandia National Laboratories as well as a number of energy companies and public utilities.

Other submissions included an expansive collaboration between government partners and corporate partners across the energy, manufacturing, and technology sectors in the Alliance for Renewable Clean Hydrogen Energy Systems hub to be located in California. This project purported to prioritize the use of hydrogen — derived from renewable feedstock — for heavy transportation and power generation. Similarly, the Northeast Clean Hydrogen Hub to be located in New York, Connecticut, New Jersey, Massachusetts, Rhode Island, Maine, and Vermont would use renewable and nuclear feedstock to produce hydrogen for the same use cases as well as industrial decarbonization of heat processing.

Applicants commonly cited logistical constraints in preparing fulsome application materials due to the fairly compressed timeframe — approximately four months from issuance of the encouragement notices to the submission deadline. DoE evaluated the proposed hubs in accordance with technical and economic modeling requirements as well as furnished information relating to governance and management structures, especially relevant due to the variety of participants. H2Hubs applicants were required to address potential safety concerns specific to hydrogen, such as potential leakage during transport and storage. Further, the proposed hub submissions were required to demonstrate compliance with key priorities for the current administration, including community benefits planning, environmental justice and equity considerations, inclusive workforce development, consent-based siting, and contributions to the broader long-term national buildout of hydrogen infrastructure.

Hub awards & future outlook

On October 13, 2023, it was announced that the H2Hubs program awardees were as follows:

| Hydrogen hub | Funding amount | Geographic location | Feedstock | Production capacity | Notable corporate partners |

| Appalachian Regional Clean Hydrogen Hub (ARCH2) | $925 million | West Virginia, Ohio, Pennsylvania, Kentucky | Natural gas | Unknown | EQT Corporation, Battelle, GTI Energy, Allegheny Science & Technology |

| California Hydrogen Hub (ARCHES) | $1.2 billion | California | Renewables, biomass | 500 mt/day by 2030; 45,000 mt/day by 2045 | Amazon, Brookfield Renewable, EDP Renewables, Hyundai, Pacific Gas & Electric |

|

Gulf Coast Hydrogen Hub (HyVelocity) |

$1.2 billion |

Texas | Natural gas, renewables | 9,000 mt/day | Chevron, ExxonMobil, Fortescue Future Industries, Invenergy, Orsted, Shell |

| Heartland Hydrogen Hub (HH2H) | $925 million | Minnesota, North Dakota, South Dakota | Natural gas, nuclear | Unknown | Xcel Energy, Marathon Petroleum Corporation, TC Energy, Bakken Energy |

| Mid-Atlantic Clean Hydrogen Hub (MACH2) | $750 million | Delaware, New Jersey, Pennsylvania | Renewables, nuclear | 85 mt/day to 600 mt/day | Monroe Energy, PBF Energy, Southeastern Pennsylvania Transportation Authority |

| Midwest Alliance for Clean Hydrogen (MachH2) | $1 billion | Illinois, Indiana, Michigan | Natural gas, renewables, nuclear | Unknown | Invenergy, AirLiquide, Exelon, ArcelorMittal, bp America, Constellation Energy |

| Pacific Northwest Hydrogen Hub (PNW H2) | $1 billion | Washington, Oregon, Montana | Renewables | 50 mt/day to 100 mt/day | bp America, Amazon, Puget Sound Energy, Plug Power |

DoE reiterated in its award notification that these selections do not a represent commitment by DoE to ultimately issue an award or provide funding. Before funding is issued, DoE and the applicants will undergo a negotiation process, and DOE may cancel negotiations and rescind the selection for any reason during that time. OCED will manage the H2Hubs program, providing project management oversight for the awardees.

This first phase for awardees only provides a small amount of the total funding — up to $20 million, with a 50 percent minimum cost matching requirement — and will span 12 to 18 months.

DoE will release the balance of program funding to awardees and monitor implementation and operations during subsequent phases in the ensuing years. The second phase will comprise analysis and negotiations to determine if each project is technologically and commercially viable and, if so, DoE will then release up to 15 percent of funding for each hub. The third phase will constitute implementation of the project — including the engineering design, labor agreements and related contractual and construction arrangements — and the release of remaining 85 percent of funding. DoE currently estimates that the third phase will take two to four years.

At this juncture, it is anticipated that the H2Hubs program will have fulfilled its objective of initially deploying an operational network of domestic hydrogen infrastructure, at scale, by the end of the decade. Synergizing this momentum with other federal incentives, such as the new IRA production tax credits and increased Section 45Q credits may also bolster the long-term prospects of domestic hydrogen. Given the ambitious climate goals of the Biden administration — a 50 percent reduction in greenhouse gas emissions (GHG) by 2030, a carbon-pollution-free power sector by 2035, and a net-zero GHG emissions economy by 2050 — it is evident that a robust hydrogen sector, with strong market signals to participants and investors as well as regulatory certainty, can contribute to an increasingly integrated and dynamic energy economy.

While there remains a substantial amount of work to be done, the H2Hubs program is an extremely exciting driver in the market, allowing the accelerated development of the industry that would be challenged to proceed apace solely on a traditional project finance or corporate balance sheet model. White & Case is honored to have a number of clients that are H2Hubs program awardees, and we sincerely appreciate the opportunity to partner with them in the development of hydrogen as a vital component of the global energy mix.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP