NAV and Holdco back leverage facilities: balancing stakeholder interests to maximise value creation

9 min read

Key Points

- Limited partners are increasingly scrutinising the fund's ability to enter into new or amended facilities to understand the impact on the fund's risk and return profile.

- Enforcement can be complex for portfolios with many non-syndicated assets.

- Success in Net Asset Value and Holdco financings depends on early engagement, tailored documentation, and ongoing dialogue among limited partners, general partners and lenders.

The rapid evolution of fund finance has propelled Net Asset Value and Holdco back leverage facilities (that is, facilities in which one or more holding companies below the fund enter the financing) to the forefront of liquidity and portfolio management for funds across asset classes. These facilities, which allow funds to borrow against the value of their underlying investments, have become increasingly sophisticated and prevalent. As the market matures, both limited partners and lenders are sharpening their focus on transparency, risk management and enforceability. This article explores the practical realities of collateral enforcement, the legal guardrails being adopted, and the value these facilities can unlock; balancing the perspectives and interests of limited partners, general partners, and lenders.

The Rise of NAV and Holdco Back Leverage Facilities

Net Asset Value (NAV) and Holdco facilities have emerged as essential tools for funds seeking to optimise liquidity, accelerate distributions and enhance returns. By borrowing against the value of their portfolios, funds can access capital without the need for immediate asset sales, providing flexibility to support portfolio companies, pursue add-on acquisitions, or manage market volatility.

The structures of these facilities vary widely by asset class. Credit funds, secondaries, private equity and infrastructure funds each present unique collateral and enforcement considerations. For lenders, understanding the nuances of each structure is critical to managing risk and maximising recoveries. For limited partners (LPs), clarity on how these facilities impact fund leverage and risk profile is paramount.

LP Concerns: Transparency, Governance and Risk

When it comes to general partners' (GPs) borrowing practices, LP focus has moved on from subscription lines to NAV and Holdco facilities. Whilst it is customary for the fund limited partnership agreements (LPAs) to include parameters on the scope and size of subscription lines, the provisions around NAV and Holdco facilities, particularly in older vintage funds, tend to say little, if anything. In a muted exit environment where LPs are starved of distributions from funds, the core investor concern is that GPs could be using NAV facilities to make distributions to make up for the lack of genuine portfolio realisations. All of this has therefore given rise to a range of LP concerns around transparency, governance and liability management.

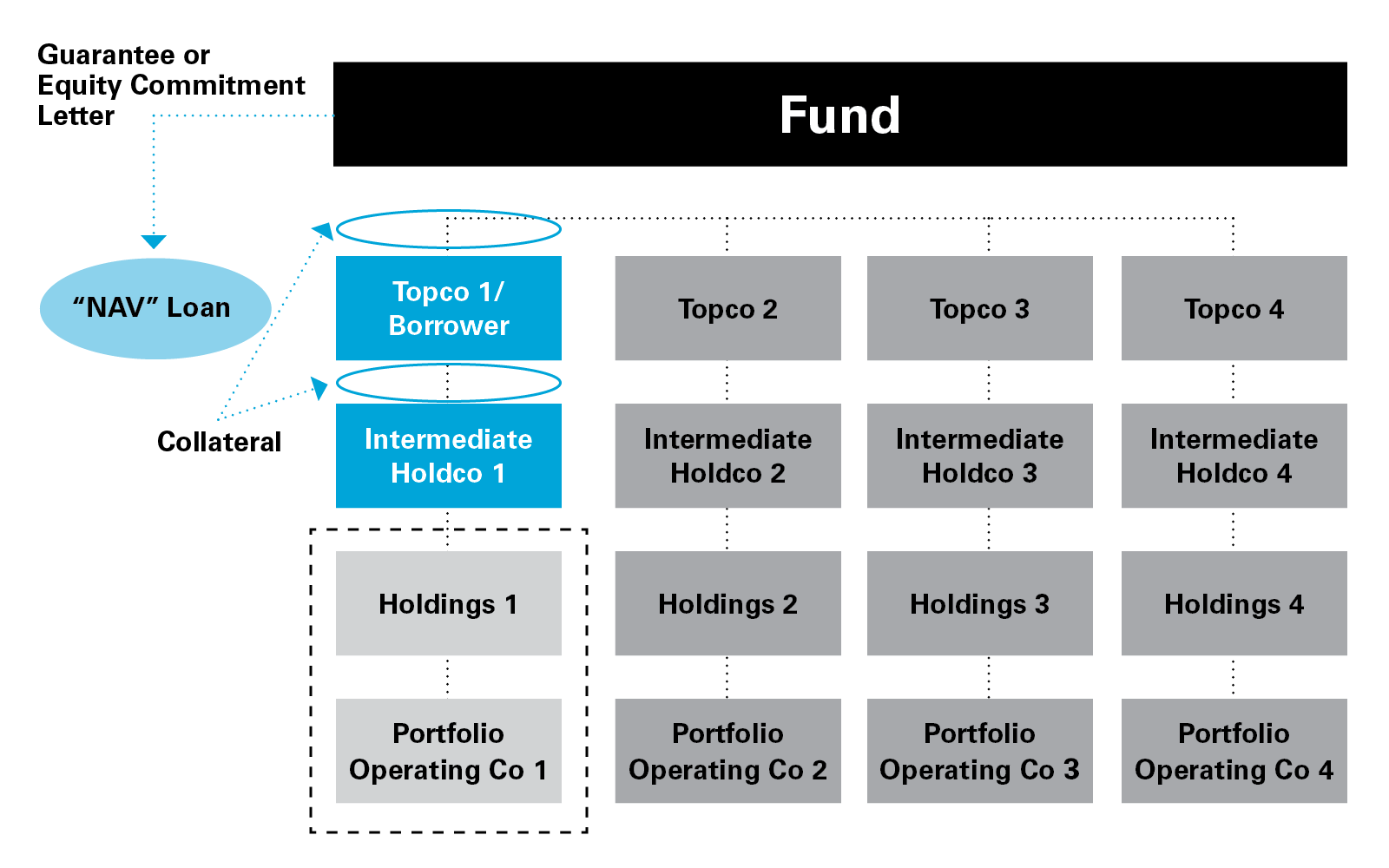

View full image

View full image

Transparency and disclosure

A recurring theme among LPs is the need for greater transparency from GPs on a range of matters and metrics, particularly on matters that could affect their risk or return profile. LPs often express concern about not being notified when such facilities are established or amended, and about insufficient detail regarding terms, collateral and the impact on fund metrics. This opacity can obscure the true leverage and risk profile of the fund, undermining LPs' ability to assess their exposure and make informed decisions. To address these concerns, LPs are increasingly demanding regular, detailed reporting and advance notice of new or amended facilities. For lenders, supporting transparency can foster trust and streamline enforcement by reducing disputes and aligning expectations. Enhanced disclosure expectations from LPs are becoming standard, including requirements for advance notice, detailed reporting and an overview of the intended usage and terms of the proposed facilities.

Recallable capital and recycling

Recallable capital and recycling provisions are key considerations for GPs when funds utilise NAV or Holdco leverage. Recallable capital allows GPs to call back distributions (already returned to LPs) to meet any purpose permitted under the LPA, while recycling enables amounts that would otherwise be distributed to LPs to be retained and reused for new investments or debt repayment. When NAV facility proceeds are distributed and then recalled, this can impact unfunded commitments, management fees and carried interest, potentially increasing LP exposure without a corresponding rise in asset value. LPs are concerned that leverage could facilitate "synthetic" recycling, complicating their true obligations and risk profile. For lenders, clarity on these provisions is essential to assess fund cash flows and repayment prospects. Best practices for fund documentation that address investor concerns include setting limits on recycling, ensuring transparent reporting, requiring advance notice or consent for recycling linked to NAV facilities, and specifying how recycled capital affects fees and carry. These measures help maintain transparency and alignment, supporting both fund performance and effective risk management.

Tax considerations

Leverage at the fund or Holdco level can trigger adverse tax consequences for certain LPs. Structures such as preferred equity interests or blocker entities (intermediate corporations that act as a tax shielding layer for other investors) can help mitigate these risks, benefiting both LPs and lenders by ensuring enforcement remains efficient and tax neutral. The specifics of these issues are beyond the scope of this article, but should be taken into account, along with any mitigation strategies, by relevant funds in deciding how to structure a proposed NAV or Holdco facility.

Cross-collateralisation and enforcement risk

LPs are concerned that there is potential for the use of NAV financing to counteract one of the key advantages of investing in a blind-pool fund (a fund that does not specify the assets to be purchased before raising capital from investors), i.e. portfolio diversification. In a situation where the NAV leverage is used with respect to an underperforming investment, cross-collateralisation (where one investment serves as collateral for obligations of other investments) could expose otherwise unrelated assets to enforcement actions, increasing risk in the event of a default and the likelihood for unintended consequences for other investments. Lenders, meanwhile, seek robust collateral packages to secure their position. Solutions include targeted collateral pools, carve- outs and the right to substitute additional assets, as well as controlled asset sale provisions that dictate the process and timeline for asset sales in a manner designed to balance the interests of all parties. Controlled sale provisions, in particular, are increasingly used to provide a clear framework for asset monetisation, ensuring that enforcement is commercially reasonable and protects both lender recoveries and LP interests.

Clearer limitations

LPs are increasingly seeking disclosure around the purpose of proposed NAV facilities and limitations, particularly in quantum, around the extent of incurrence of such indebtedness. While this adds a layer of governance and can be more involved for GPs from an investor relations perspective, it can also benefit lenders by reducing the risk of challenge and facilitating smoother enforcement processes.

Enforcement Realities: Asset Class Matters

Credit fund

Enforcement is relatively straightforward for syndicated loans, as these can be sold in the secondary market following customary assignment procedures. However, enforcement can be complex for portfolios with many non-syndicated assets due to transfer restrictions and consent requirements. Bankruptcy-remote SPVs and pledges of bank accounts are common features that protect both lenders and LPs.

Secondaries

In the case of secondaries LP-led transactions where fund interests are sold by an existing LP to a third-party investor, it is common for purchasers of fund interests to incur asset- based leverage to fund the purchase price for such interests. Where leverage is incurred, it will usually be taken by an SPV sitting below the secondary fund level, for a couple of reasons, including risk isolation and to avoid triggering GP secondary fund consent requirements. However, indirect transfer restrictions in LPAs may still apply, requiring careful structuring. Lenders can enforce by foreclosing on the SPV but must navigate consent requirements for asset sales. The use of bifurcated SPVs, one holding interests subject to indirect transfer restrictions and another holding the remainder, can help manage these risks.

Private equity and infrastructure

Enforcement of NAVs and Holdco back leverage facilities is complicated by portfolio company-level leverage, change of control provisions, potential regulatory consent requirements, and shareholder agreements. Pledging only economic interests (the rights to profit) without transferring associated voting or management rights on the shares may avoid triggering certain restrictions but can limit the lender's ability to monetise assets and may increase risks in insolvency when enforcement is most important. Controlled sale provisions and preferred equity structures (that subordinate repayment) may be used to balance these challenges.

Holdco back-levering/ margin loans

The equity interests in the underlying portfolio companies pledged as collateral for these loans often involve minority interests which are subject to broad transfer restrictions and rights of first refusal and/ or tag-along provisions. Lenders must conduct thorough diligence on shareholder agreements and be prepared for constrained enforcement options. The use of fund-level guarantees, or equity commitment letters can enhance lender protections.

Mitigation Strategies: Legal Guardrails and Practical Solutions

- Advance disclosure and reporting: Regular, detailed reporting and advance notice requirements benefit both LPs and lenders by reducing uncertainty and aligning interests.

- Controlled sale provisions: These provisions require the fund to monetise assets in a commercially reasonable manner, providing a clear framework for enforcement that protects both lender recoveries and LP interests.

- Jurisdictional analysis: Out-of- court enforcement procedures and careful selection of governing law can streamline enforcement and maximise recoveries.

- Tax and regulatory structuring: Preferred equity interests, blocker entities and other structures can mitigate tax and regulatory risks for all parties.

Value Accretion: Why These Facilities Matter

When properly structured and managed, NAV and Holdco back leverage facilities deliver significant value:

- For LPs: Improved liquidity, accelerated distributions and enhanced IRR, provided risks are managed and impact on returns are disclosed;

- For lenders: Secure, asset-backed lending opportunities with robust legal protections and clear enforcement pathways; and

- For GPs: Strategic flexibility to support portfolio companies, pursue add-on acquisitions and manage market volatility.

The key is alignment. Parties must balance robust lender protections with transparency and governance for LPs and leveraging creative structuring to address enforcement and regulatory challenges.

Negotiation and Collaboration: The Path Forward

Success in NAV and Holdco financings depends on early engagement, tailored documentation and ongoing dialogue among LPs, GPs and lenders. By working collaboratively to address concerns and structure practical solutions, all parties can unlock the full value of these facilities while managing risk and ensuring enforceability.

Conclusion

NAV and Holdco back leverage facilities are powerful instruments for unlocking liquidity and supporting portfolio strategies, provided that the risks are properly managed. The key to successful transactions lies in rigorous due diligence, clear documentation and robust legal protections that anticipate enforcement challenges and align lender interests with those of the fund and its LPs. By insisting on transparency, enforceable collateral structures and practical reporting mechanisms, lenders can confidently deploy capital while mitigating downside risk. In a market defined by complexity and innovation, lenders who prioritise disciplined structuring and proactive risk management will be best positioned to realise the full potential of these facilities and safeguard their investments.

Sherri Snelson is a partner in White & Case's debt finance practice in New York.

Email: sherri.snelson@whitecase.com

Lavanya Raghavan is a funds and investment management partner in White & Case's global Private Equity practice in London.

Email: lavanya.raghavan@whitecase.com

Emma Russell is a partner in White & Case's debt finance in London.

Email: emma.russell@whitecase.com

Alice Wight is an associate in White & Case's debt finance practice in London.

Email: alice.wight@whitecase.com

Further Reading:

- NAV facilities to PERE funds (2025) 9 JIBFL 664.

- Hybrid facilities: the promise, the reality and the hope (2023) 10 JIBFL 691.

- Lexis+® UK: LexisPSL Banking & Finance Practical Guidance: Practice Note: Fund finance.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2026 White & Case LLP