The 'Taskforce on Scaling Voluntary Carbon Markets' (the "Taskforce") is a private sector initiative working to scale an effective and efficient voluntary carbon credit market to help meet the goals of the Paris Agreement.

On 10 November 2020, the Taskforce published a blueprint for a voluntary greenhouse gas or carbon market, (the "Consultation Document"), which was summarised in our 13 November 2020 alert here (Voluntary Carbon Markets: A Blueprint). The Taskforce has now published its final report (the "Final Report") following a public consultation throughout November and December 2020 in which the Taskforce received more than 160 responses via the consultation survey, and more than 25 letters written directly to it. The Taskforce's Final Report includes 20 recommended actions under six key topics for the scaling of existing voluntary carbon markets. The Taskforce believes publishing this blueprint can guide companies to increase their emissions-reduction goals and finance climate action. If you wish to read more about why a widely accepted blueprint is important in establishing and scaling a voluntary carbon market, please see our November 2020 client alert (see Background).

The Taskforce is spearheaded by Mark Carney, UN Special Envoy for Climate Action and Finance Advisor to UK Prime Minister Boris Johnson for the 26th meeting of the Conference of the Parties to the United Nations Framework Convention on Climate Change (UNFCCC) ("COP26"). The Taskforce is chaired by Bill Winters, Group Chief Executive, Standard Chartered, and sponsored by the Institute of International Finance ("IIF") under the leadership of IIF President and CEO Tim Adams. It is made up of more than 50 members globally, representing buyers and sellers of carbon credits, standard setters, the financial sector and market infrastructure providers including Ingrid York of White & Case, and is supported by a consultation group composed of subject-matter experts from approximately 120 institutions and relevant sector trade associations. The Final Report of the Taskforce was introduced by Bill Gates, Mark Carney, Bill Winters and Annette Nazareth at the Davos Agenda 2021.

Key guiding principles

The Taskforce has developed this blueprint according to four key principles:

- Producing open-source solutions for private-sector organisations to take forward. The Taskforce hopes the solutions suggested in the Final Report can work alongside other initiatives to scale up voluntary carbon markets globally.

- Voluntary carbon markets must have high environmental integrity and seek to do no harm. In the past, carbon markets have occasionally allowed projects that generate carbon credits to cause harm to local communities and ecosystems. The Taskforce argues carbon markets should be designed to ensure emissions-reductions projects benefit local communities, preserve or strengthen ecosystems and avoid doing harm.

- Amplify existing and ongoing work of parallel initiatives. The Taskforce membership includes players from many ongoing related initiatives and incorporates lessons learned from these efforts into the Final Report. Future efforts arising from the Final Report need to be carried out in tandem with parallel initiatives to ensure emissions-reduction efforts learn from and support one another.

- Avoid disincentivising emissions reduction efforts. Carbon markets need to be designed in a way that does not reduce the incentive for businesses to reduce their own emissions. The Taskforce recognises that to meet the Paris Agreement targets, all sectors must reduce their absolute emissions and carbon markets must also enable companies to become carbon-negative.

Recommendations

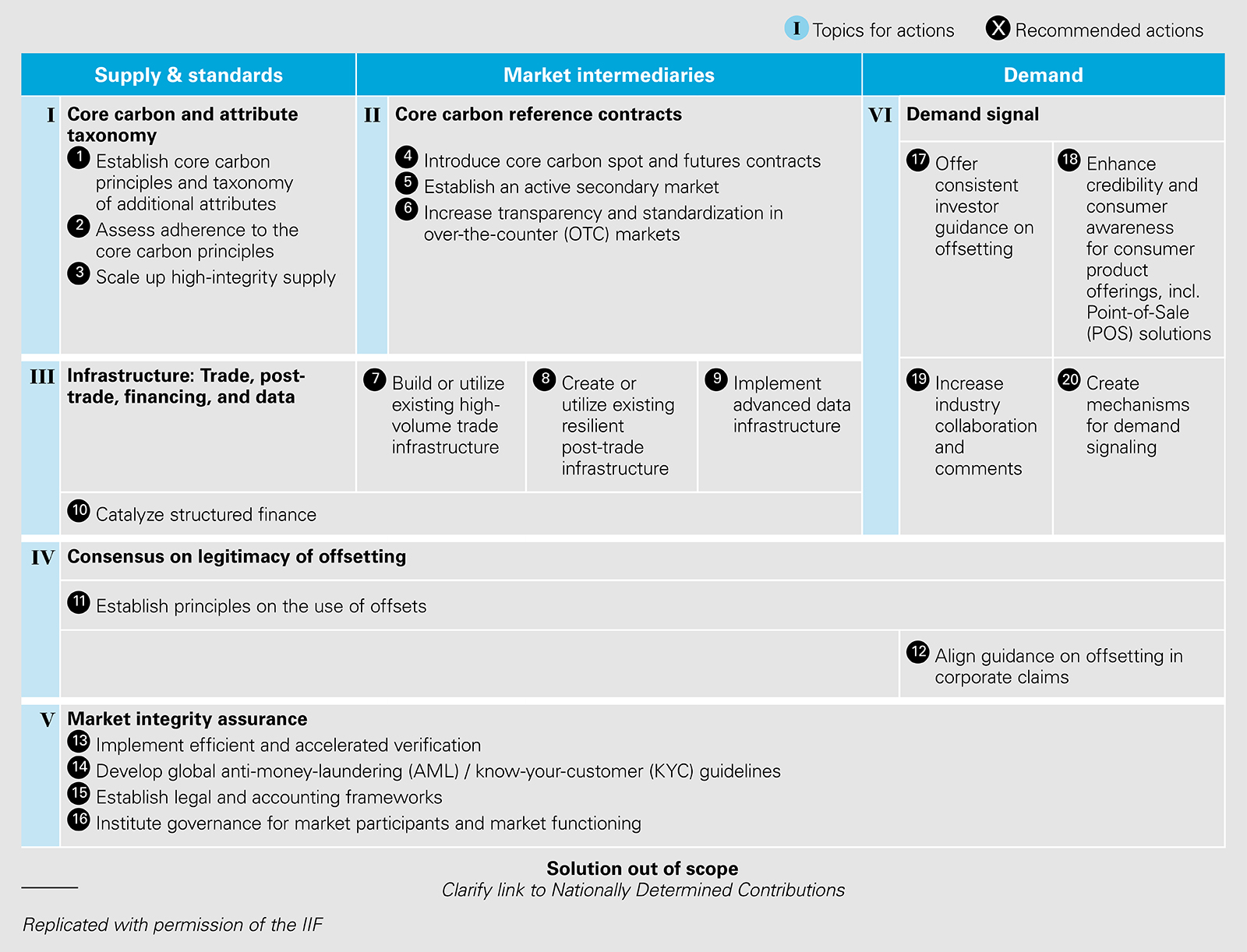

To support the scaling-up of voluntary carbon markets, the Taskforce has developed 20 underlying recommended actions, grouped under six topics, for action across the value chain (including supply and standards, market intermediaries and demand), as summarised below. Note that there remain open items for further consideration and several important questions that will be part of the Taskforce's "Roadmap for Implementation" over the next 12 months.

Topic One: Core carbon principles and attribute taxonomy

- Establish core carbon principles and taxonomy of additional attributes. The Taskforce is focused on creating a market with both integrity and liquidity. It accordingly recommends the establishment and maintenance of core carbon principles ("CCPs") by an independent third party which would set out threshold quality criteria against which carbon credits and their supporting standards and methodology can be assessed. The Implementation Roadmap in the Final Report, as further outlined below, sets out the organisational steps required to establish the correct body for CCP governance. The independent third party would also define a set of additional attributes, e.g. vintage, project type (i.e. avoidance / reduction, nature-based removal, technology-based removal), additional benefits beyond emissions reductions (i.e. co-benefits), location and inclusion of corresponding adjustments. The Taskforce believes establishment of CCPs in such a manner would build confidence and credibility in voluntary carbon markets, allowing the market to develop more successfully.

- Assess adherence to the CCPs. The Taskforce also recommends the need for an independent third party organisation to be tasked with assessing carbon credit standards and methodologies for validation against the CCPs and additional attributes. While it is noted that it may be possible for this to be carried out by the same body hosting the CCPs, the recommendation is for separate expert verification agencies (accredited by the International Accreditation Forum) to undertake this role. Ideally, all relevant carbon-market standards entities would adopt the taxonomy and make clear whether their methodologies are certified. The clear challenge will be to balance the level of detail needed for methodology assessments against the administrative burden. However, this is clearly key to address significant quality concerns that exist across the value chain.

- Scale-up high integrity supply. The Taskforce recommends rapid market upscaling (15 fold by 2030) but with a focus on ensuring market integrity and project local community impact. The impetus for such scale-up will need to derive from smaller-scale project developers as well as large multinationals and technology projects (in particular, new technologies being brought to market). To help achieve this and support small-scale developers, the Taskforce recommends a supplier to financier matching platform for proposed projects. Ideally, this platform would allow for the upload of suppliers' previous project development history and credit score for buyers to conduct due diligence and be subject to the same standards and controls as would apply to any other voluntary carbon market infrastructure. For negative emissions technology and other maturing climate technologies, the Taskforce encourages the development of new methodologies in a timely and robust manner.

Topic Two: Core carbon reference contracts

- Introduce core carbon spot and futures contracts. Development and listing of standardised spot and futures core (physically delivered) carbon contracts is seen as vital by the Taskforce in order to match suppliers' products and buyers' preferences more efficiently and, critically, provide a daily reference carbon price for standardised products.

- These contracts would be physically settled, traded on exchange and cleared via clearing houses. Futures contracts should be fungible to allow for trading across all markets and multiple platforms and could potentially also be cash settled. Over time, the Taskforce envisages that exchanges could also develop reference contracts which combine the core carbon contract with additional attributes that are separately priced. The Taskforce also encourages large buyers to purchase a share of their voluntary credits on exchange, through reference contracts, to encourage the development of liquidity. This would also reinforce the efficacy of the published carbon price. There is also discussion regarding the development of a separate and complementary over-the-counter (off exchange) market for carbon contracts in both standardised and bespoke format, which will benefit from the establishment of a reference contract.

- Establish an active secondary market. This will be core to the success of voluntary carbon markets by providing a number of benefits across the value chain, such as:

- increasing the transparency and reducing the volatility of pricing;

- allowing market participants to manage and hedge risks that can arise from, for example, carbon projects or carbon reduction commitments;

- increasing flexibility such that firms are able to change their strategy more efficiently. This is likely to increase the number of firms committing to voluntary carbon markets given they know they can exit a carbon credit position if their circumstances change;

- increasing access to carbon markets for those participants who would not traditionally be present in financial markets and/or may not be able to easily access exchanges or clearing houses; and

- increasing investor attraction and liquidity, thereby tightening the bid-ask spread.

Additional services in the secondary market may also arise such as the development of indices, which would facilitate longer term hedging and financial investment.

- Increase transparency and standardisation in over-the-counter (OTC) markets. The Taskforce argues OTC markets will benefit from the development of reference contracts given they will be tightly linked to them. It is posited that, when negotiating OTC contracts, parties can use the price of the liquid core carbon contracts, as well as the price signal, as a starting point; this can assist in forming a more general consensus in the market. Upgraded contracts (based on currently existing agreements such as the emissions trading annex published by the International Swaps and Derivatives Association, Inc.) are needed to help facilitate negotiations, and enable more efficient trading of credits, in primary and secondary OTC markets (see further discussion of this in Topic Five: Market integrity assurance). Other items are noted which will be beneficial to this market such as further digitisation of voice-brokered OTC services, the use of post-trade risk reduction services (e.g. trade compression) and increased transparency through the use of, e.g. price reporting agencies.

Topic Three: Infrastructure: Trade, post-trade, financing and data

The Taskforce recommends that a set of infrastructure components must be in place that is resilient, flexible and able to handle large scale trading of core carbon reference contracts. The recommended actions to develop the target infrastructure are:

- Build or utilise existing high-volume trade infrastructure. Exchanges should provide market participants with access to market data and adhere to suitable cybersecurity standards. Likewise, OTC brokers should provide enhanced transparency through market data access to market participants.

- Create or utilise existing resilient post-trade infrastructure. Clearing houses should be used to facilitate an exchange traded market, provide counterparty default protection and offer access to relevant data. Meta-registries should be established to provide custodian-like services and generate standardised issuance numbers for projects across existing registries (similar to the ISIN concept). This would allow for more project transparency and market participants to conduct due diligence on certain projects. If possible, the meta-registry should connect to international registries as well as the voluntary independent registries to maximise the use of the data. As with exchanges, meta-registries and the underlying registries should adhere to suitable cybersecurity standards. The infrastructure should be aligned to the Committee on Payments and Market Infrastructures – International Organization of Securities Commissions (CPMI-IOSCO) Principles for Financial Market Infrastructures.

- Implement advanced data infrastructure. Data providers and meta-registries should work together to offer transparent reference and market data, as well as historic carbon project or project developer performance and risk data. Intermediaries (such as exchanges and clearing houses) should include trading information in their existing data flows.

- Catalyse structured finance. Banks and other supply chain financiers should examine potential lending facilities for project development, which could be collateralised by the right to generate carbon credits. This should be supported by various measures including, e.g., establishing a robust recognition system for banks that finance such projects. In the medium to long term, a carbon credits spot and futures market would provide a suitable foundation for a structured finance market to develop as it would provide clarity on pricing and facilitate risk transfer.

Topic Four: Consensus on the legitimacy of offsetting

- Establish principles on the use of offsets. The Taskforce asserts that there is a lack of shared vision on the role of carbon offsets in achieving net zero goals, with many stakeholders having legitimate concerns about carbon offsetting crowding out other decarbonisation efforts (for example, reduction of a company's own emission levels). With this in mind, the Taskforce proposes two new sets of principles.

- It firstly wishes to establish 'Principles for Net Zero-Aligned Corporate Claims and Use of Offsets'. These principles are:

- Reduce: companies should publicly disclose commitments and detail transition plans and annual progress to decarbonise their own operations and value chains to limit warming to 1.5 degrees Celsius in line with the Paris Agreement, using the best available data. Companies should prioritise implementing these commitments and make public the basis on which the claims are made;

- Report: companies should measure and report Scope 1, Scope 2 and, where possible, Scope 3 greenhouse gas emissions on an annual basis using third party standards for corporate greenhouse gas accounting and reporting; and

- Offset: during the transition to net zero, companies should purchase and retire carbon credits generated under credible third party standards.

- The Taskforce also proposes 'Principles for Credible Use of Offsets in Products or at Point of Sale'. Most notably, these principles require companies to provide more pricing and product transparency for customers by being clear about profits they make from offset products, disclose whether the carbon offset has any co-benefits and allow end-consumers to access data that validates the retirement of the purchased credits (or they obtain third party validation and auditing of point of sale products to demonstrate use of funds to purchase and receive carbon credits).

- The Taskforce recommends that these principles should be further developed, hosted and curated by an independent body and the Final Report states an "independent High Ambition Demand Accelerator for the Voluntary Carbon Market" will take on this role.

- Align guidance on offsetting in corporate claims. The Taskforce also acknowledges that there is some inconsistency in the treatment of carbon credits with regard to corporate commitments on climate action that needs to be addressed. For example, offsetting is not counted towards science-based emissions reduction targets but the Science-Based Targets Initiative does recognise the role of offsetting towards net-zero claims. It is also recommended that harmonisation of guidance is achieved in respect of both carbon accounting and corporate claims standards. Ideally, the harmonised offsetting reporting guidance will be in line with broader national and international frameworks.

Topic Five: Market integrity assurance

Growth of voluntary carbon markets can increase the risk of errors, fraud and money laundering between market participants. To create and protect market integrity, the Taskforce therefore recommends:

- Institute efficient and accelerated verification. The development of a shared digital data protocol across standards and registries. This system would allow for project data to be captured, protected and continuously monitored on a higher frequency basis and validated as projects are being developed. This will allow for an efficient, effective and secure verification system. The Taskforce encourages rapid innovation and continued testing and evolution of related technological solutions.

- Develop 'anti-money laundering (AML)' and 'know your customer (KYC)' guidelines. The development and implementation of AML and KYC guidelines for voluntary carbon markets will help minimise the risk of fraud or money laundering as the market develops. A governance body should coordinate this process in line with existing regulatory regimes at the international level (such as the Financial Action Task Force ("FATF")).

- Establish legal and accounting frameworks. Further coordination and support of legal and accounting frameworks is required to underpin the legitimacy and efficacy of voluntary carbon markets. The Taskforce accordingly recommends the need for standardised contractual documentation across primary and secondary markets to allow for a robust exchange and OTC market, with such documentation underpinned by appropriate legal opinions.

- The Taskforce also highlights the need for further clarity from international accounting agencies like the IFRS and GAAP on how carbon credits ought to be treated from an accounting standpoint (e.g. as an asset or an expense). The Taskforce encourages organisations such as the Greenhouse Gas Protocol to provide clarity as to how removal offsets are to be counted against a company's carbon footprint.

- Further to its other statements on governance, the Taskforce acknowledges that appropriate governance is required to host and curate standard contracts, financial accounting guidance and carbon accounting guidance.

- Institute governance for market participants and market functioning. Strong governance should be established to ensure there is the high level of environmental and market integrity needed for the voluntary carbon market to be successful. The three key areas of focus in which governance is required are:

- participant eligibility;

- participant oversight; and

- market functioning oversight.

- For example, if the use of carbon credits may disincentivise alternative climate action (such as companies reducing their own emissions), governance is needed around the identification and principles-based mitigation of this risk.

- Participant eligibility could involve establishing a set of principles to be followed by buyers, suppliers and intermediaries if they wish to participate in voluntary carbon markets. Participant oversight could include the development of a new process for accrediting the validation and verification bodies that assess projects and methodologies and authorise issuance of carbon credits (with the aim being that this would also involve auditing and conducting spot checks of those bodies).

- Oversight of market functioning could include developing principles to prevent fraud across the market value chain, including by ensuring appropriate anti-money laundering practices (as mentioned above). It would also include the establishing, hosting and curating of principles for the use of offsetting, as mentioned above (see Topic Four: Consensus on the legitimacy of offsetting) and consideration of how long investors can retain carbon credits.

Need for end-to-end market governance:

- In connection with its recommendations on governance, the Taskforce believes governance structures will be needed in three areas:

- overseeing the hosting, the curation and the assessment of CCPs;

- the market principles; and

- legal and accounting rules.

- Existing and newly established governance bodies must interact to ensure governance in these areas is as comprehensive as possible. Whilst existing bodies like the CFTC (for financial instruments), the IAF (for accreditation and verification) or the IFRS and GAAP (for financial accounting) are able to fulfil some of the governance needs for an effective voluntary carbon market, the Taskforce acknowledges that not all needs can be currently met by these bodies. It is therefore a specific undertaking of the Taskforce's Implementation Roadmap to take steps to address gaps in governance needs. This could potentially involve the development of an umbrella governance body, which could carry out particular governance needs not suited to existing bodies (such as hosting and curating the CCPs).

Topic Six: Demand signals

The Taskforce is of the view that a clear demand signal from buyers could increase liquidity in carbon markets and scale up supply. The Taskforce accordingly recommends a number of ways to increase demand for carbon credits, including:

- Offer consistent investor guidance on offsetting. Key investor bodies should work with reporting protocol bodies to provide clear and consistent guidance on the appropriate use of offsetting for buyers.

- Enhance credibility and consumer awareness for consumer offerings, including point-of-sale solutions. The ability for consumers to purchase carbon credits should be increased, allowing them to make more informed choices as to what they are purchasing. This would include the following steps:

- requiring clear and consistent carbon claims;

- encouraging clear carbon labelling and continuing to improve consumer education regarding the environmental and economic benefits of carbon offset in everyday life;

- expanding existing point-of-sale carbon offsetting offerings; and

- creating digital functionality to enable point-of-sale offset purchases.

- Increase industry collaboration and commitments. Further collaboration in key sectors, particularly oil and gas, would lead to significant carbon reduction activity and an increase in the demand for carbon offsets in the process. The Taskforce states in particular that tailored sector-wide standards on the use of offsets can improve industry best practices and aid buyers' transition to net zero.

- Create mechanisms for demand signalling. Companies sending long-term demand signals (for example, through long term agreements with suppliers or reduction commitments) in order to scale credit supply. These demand signals could be aggregated through a buyer commitment registry.

Commentary – why is this important right now?

The Taskforce argues that the global climate change mitigation goals simply cannot be achieved by way of emissions reductions alone. Instead, the Taskforce advocates that carbon offsetting must accordingly be an important part of any such transition. The Taskforce notes that voluntary carbon markets must grow by at least 15 times by 2030 to meet the necessary corporate demand. The intention of the Taskforce's Consultation Document and Final Report is to be a catalyst for such radical change.

This year's COP26 will focus investors' minds on the sustainability strategies of the companies and institutions in which they invest across the globe. Carbon credits are a key tool for boards to ensure relevant sustainability targets are met, corporate resilience is sustained and the goals of the Paris Agreement are achieved. But the usefulness of carbon credits depends on the liquidity and consistent price generation of the markets on which they are traded. This in turn depends on reliable and consistent data, taxonomies and benchmarks. The Taskforce has set out concrete steps to accelerate and scale up the development of these markets as the axis for generating liquidity, pricing, data, taxonomies and benchmarks – ultimately achieving real and swift mitigation of climate change.

Conclusion

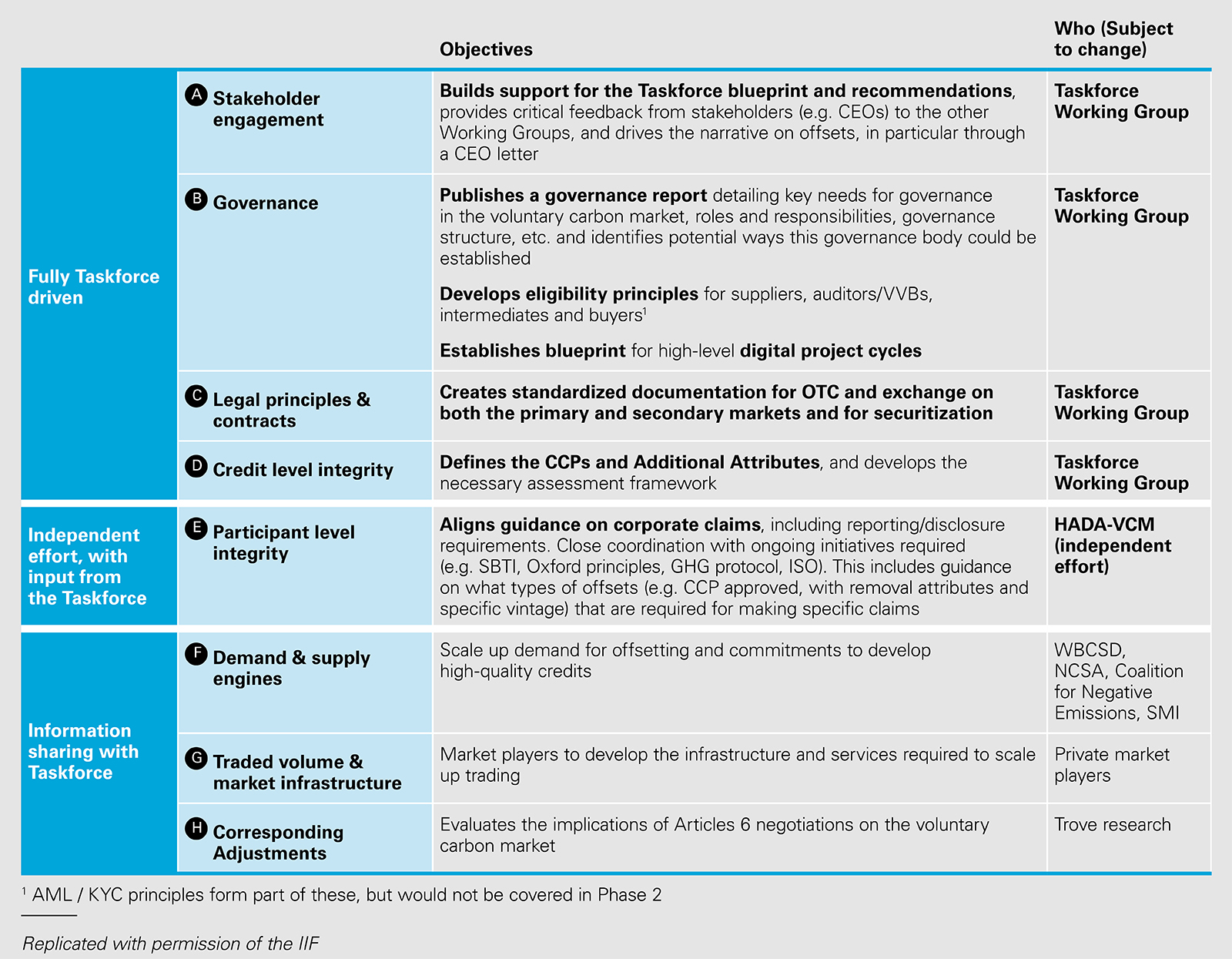

The work of the Taskforce will now turn to implementation and the establishment of a pilot market within the next 12 months. The Taskforce's Implementation Roadmap builds directly on the 20 recommended actions summarised in this alert. The graphic above highlights the eight areas of work the Taskforce will target to capture the 20 recommended actions, and sets out the objectives to be achieved within each one.

It is made clear in the Final Report that the Taskforce considers this a highly collaborative process and invites parties interested in leading or driving key action items to make themselves known. Clearly the ambition and scale of the proposal is great and will require participation of all relevant stakeholders to ensure its success. This is a global Taskforce seeking global private sector solutions for a problem which needs global cooperation; it would be a great shame if it were to be stymied by national barriers or balkanised rules and regulations. The work of the Taskforce in this next phase will be critical for the initiative as the nascent market takes shape and key positions on principles, rules, governance and infrastructure evolve.

Further details regarding the Taskforce can be located here.

The Final Report can be located here.

Connor Gray (Trainee Solicitor, White & Case, London) contributed to the development of this publication.

This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.

© 2021 White & Case LLP