Two years ago, the FSR arrived as the new kid on the block in Brussels. Today, it is one of the EU's sharpest enforcement tools, and one that is only gaining prominence as geopolitical tensions reshape global investment and trade. We take stock of the FSR's first two years, sharing the latest statistics, practical lessons and policy developments from our experience with the European Commission. We also look ahead, offering insights on how this regime is likely to evolve and what it means for investors navigating the EU market.

M&A activity under the FSR: a statistical overview

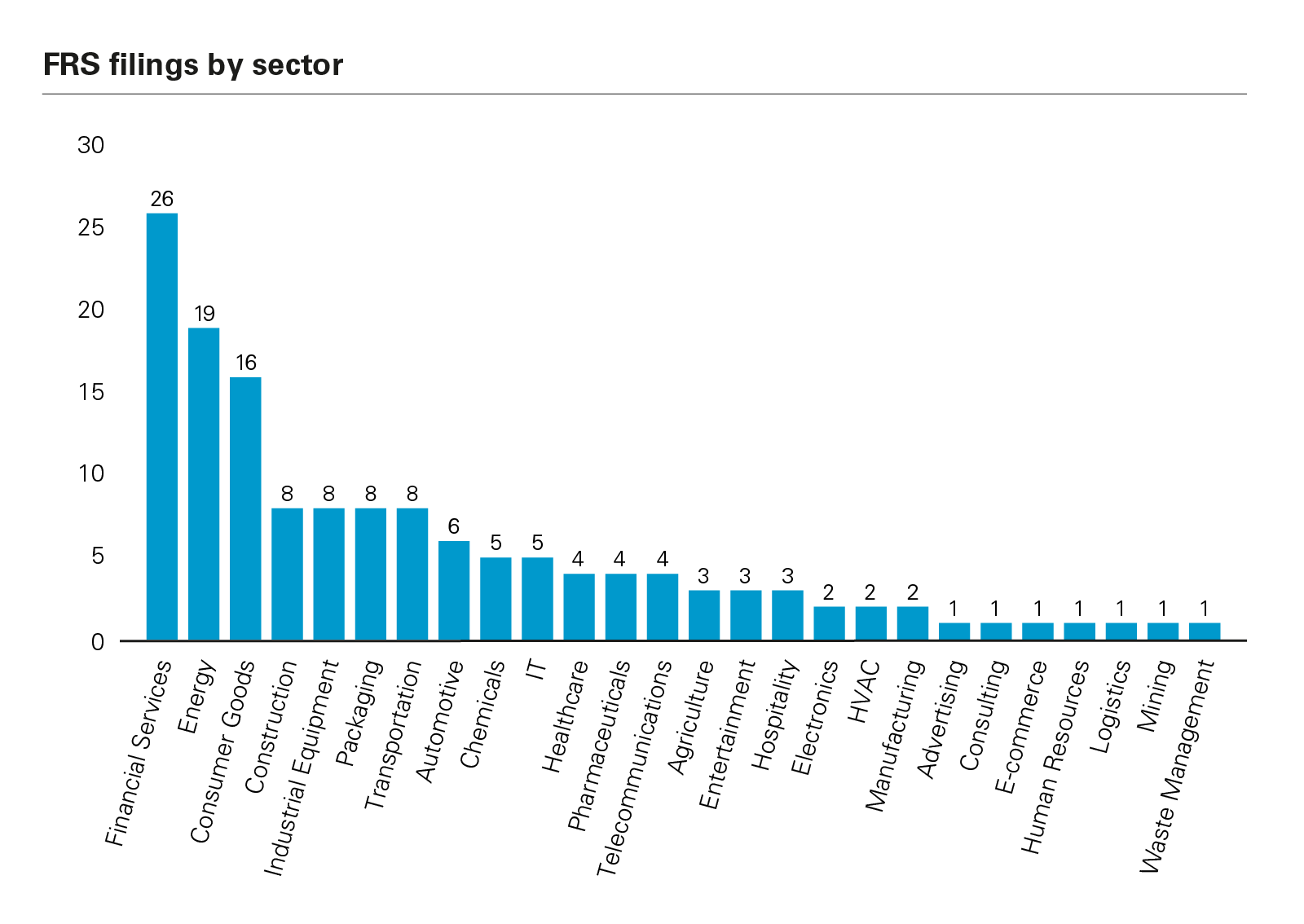

To date1, the European Commission ("EC") has received 179 FSR filings, with an average of eight notifications per month. Private equity (PE) sponsors account for roughly a third of these notifications – making them the largest category of notifying parties. While filings span a range of different sectors, they are primarily concentrated in financial services, energy and consumer goods.

View full image: FSR Filings by Sector (PDF)

View full image: FSR Filings by Sector (PDF)

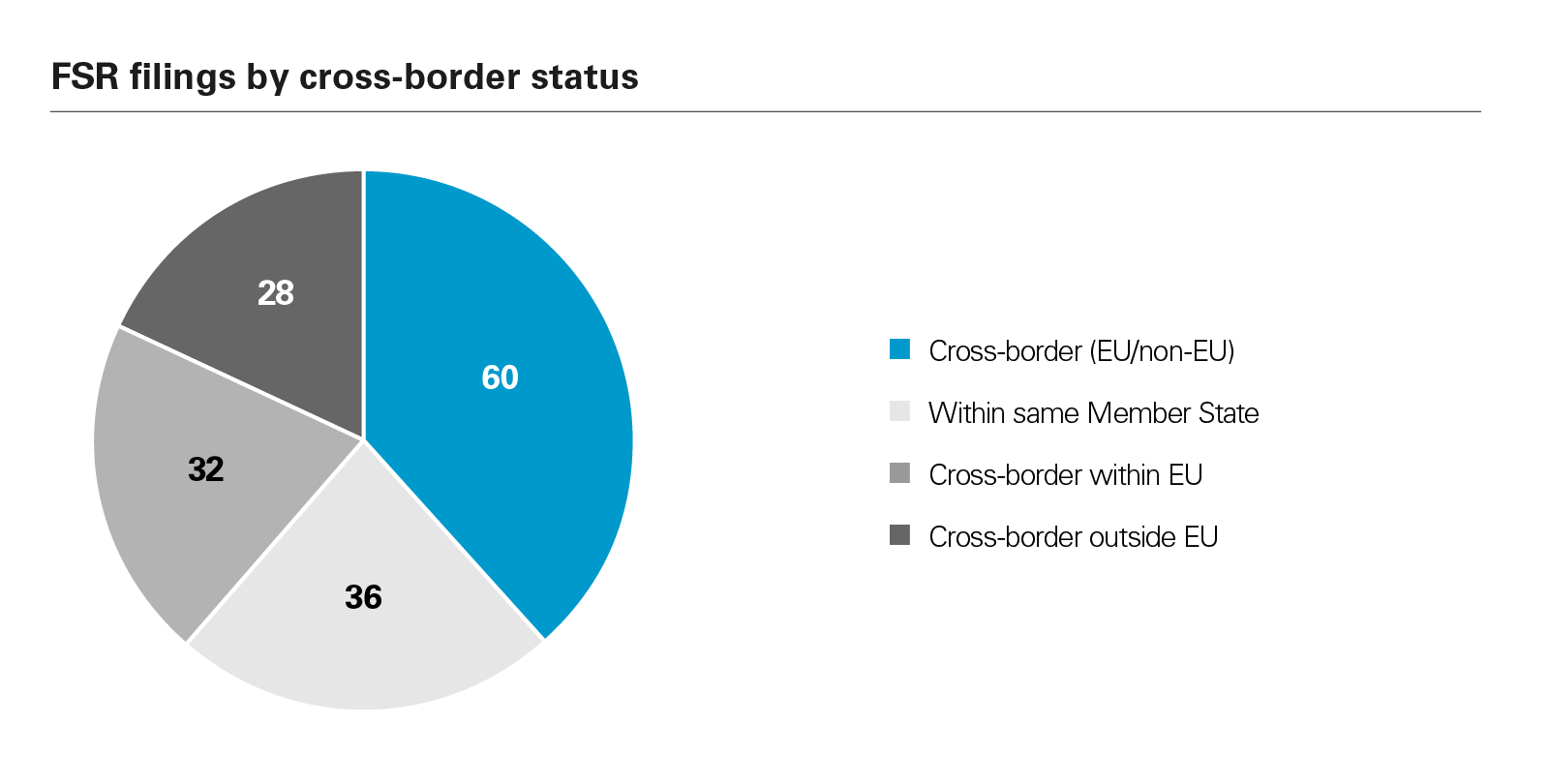

More than 60% of transactions reviewed under the FSR are cross-border in nature, half of which involve one EU and one non-EU party.

View full image: FSR Filings by Cross-Border Status (PDF)

View full image: FSR Filings by Cross-Border Status (PDF)

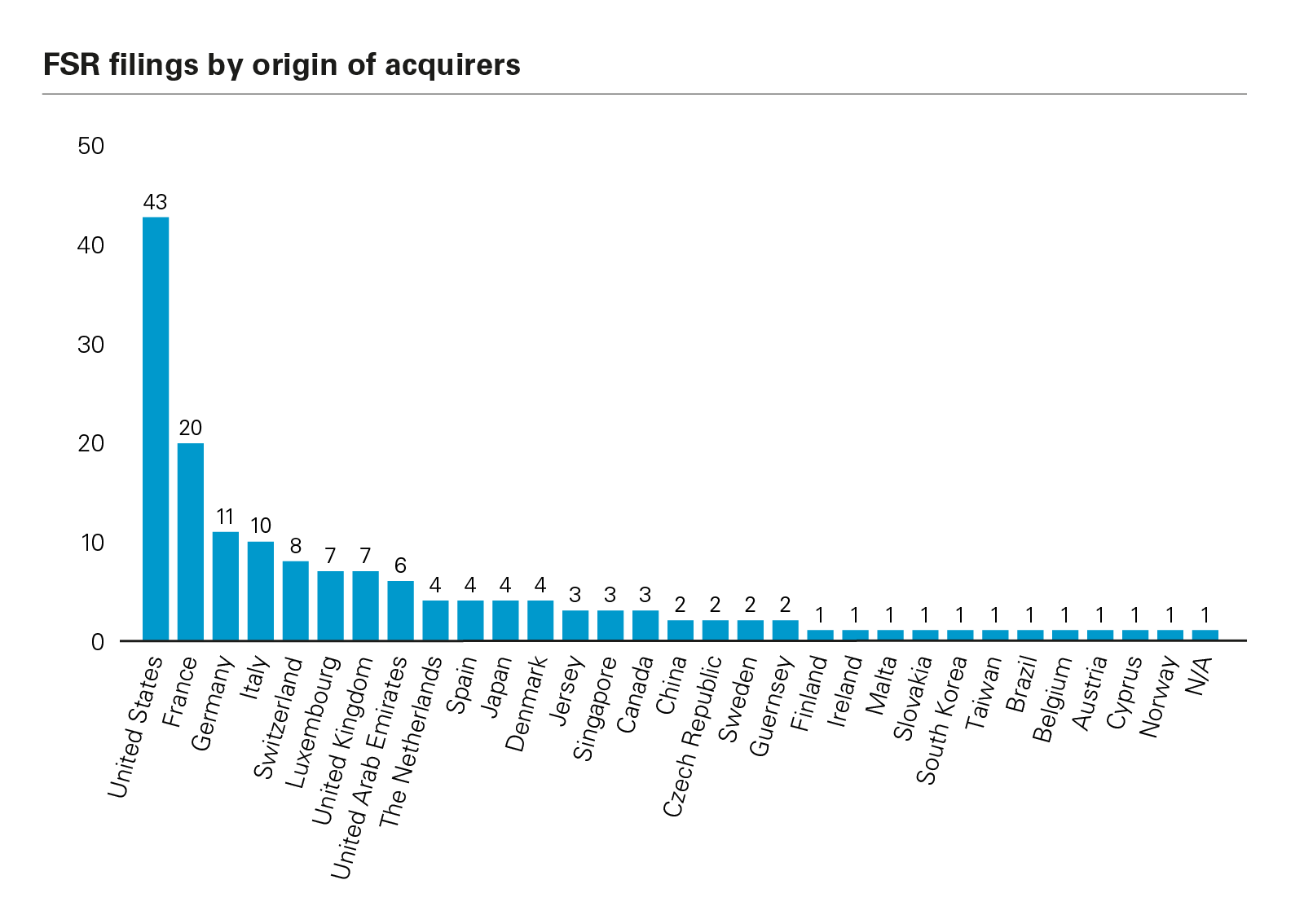

Acquirers come from a broad mix of jurisdictions, with the United States, France and Germany leading the pack.

View full image: FSR Filings by Origin of Acquirers (PDF)

View full image: FSR Filings by Origin of Acquirers (PDF)

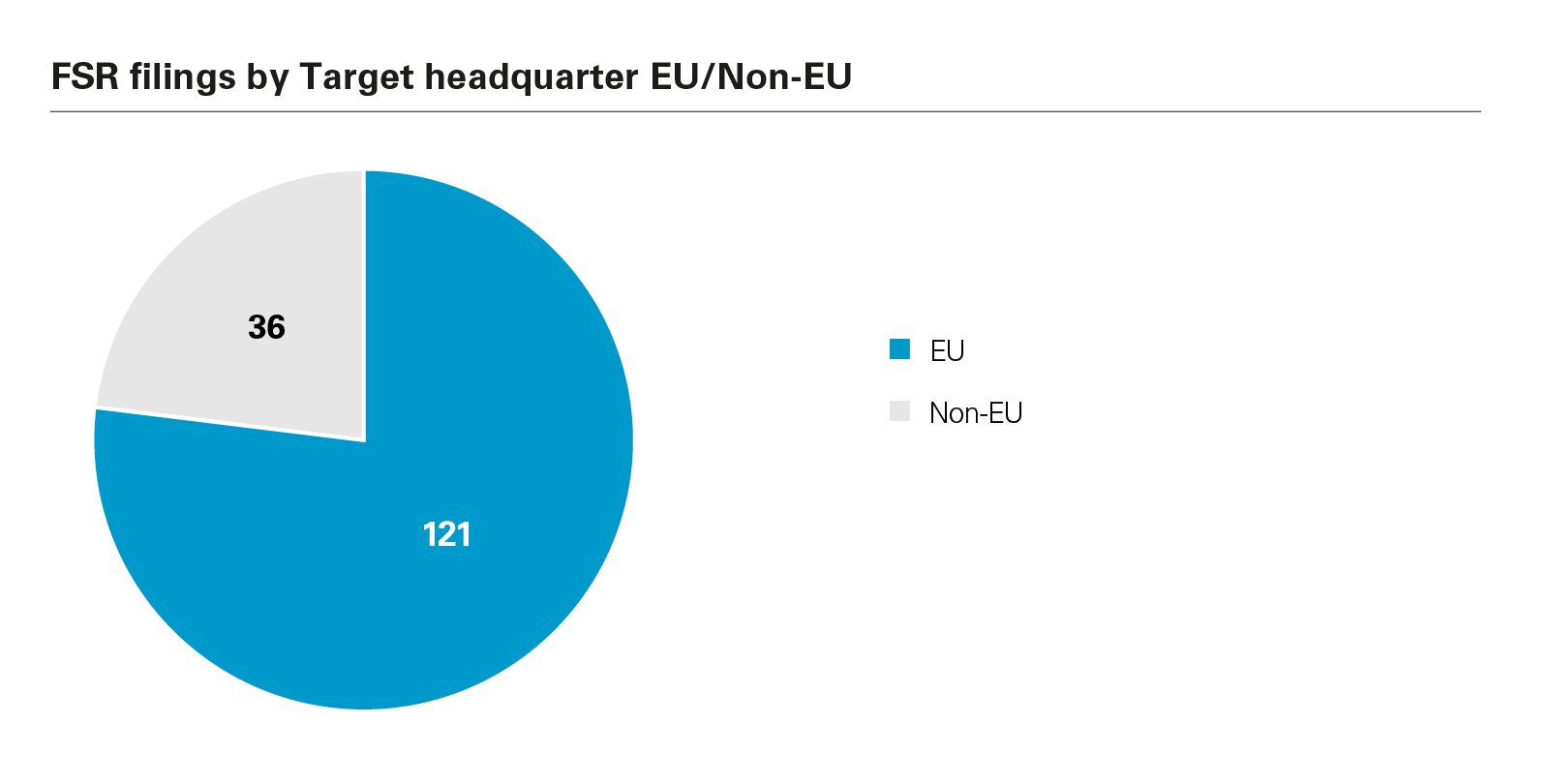

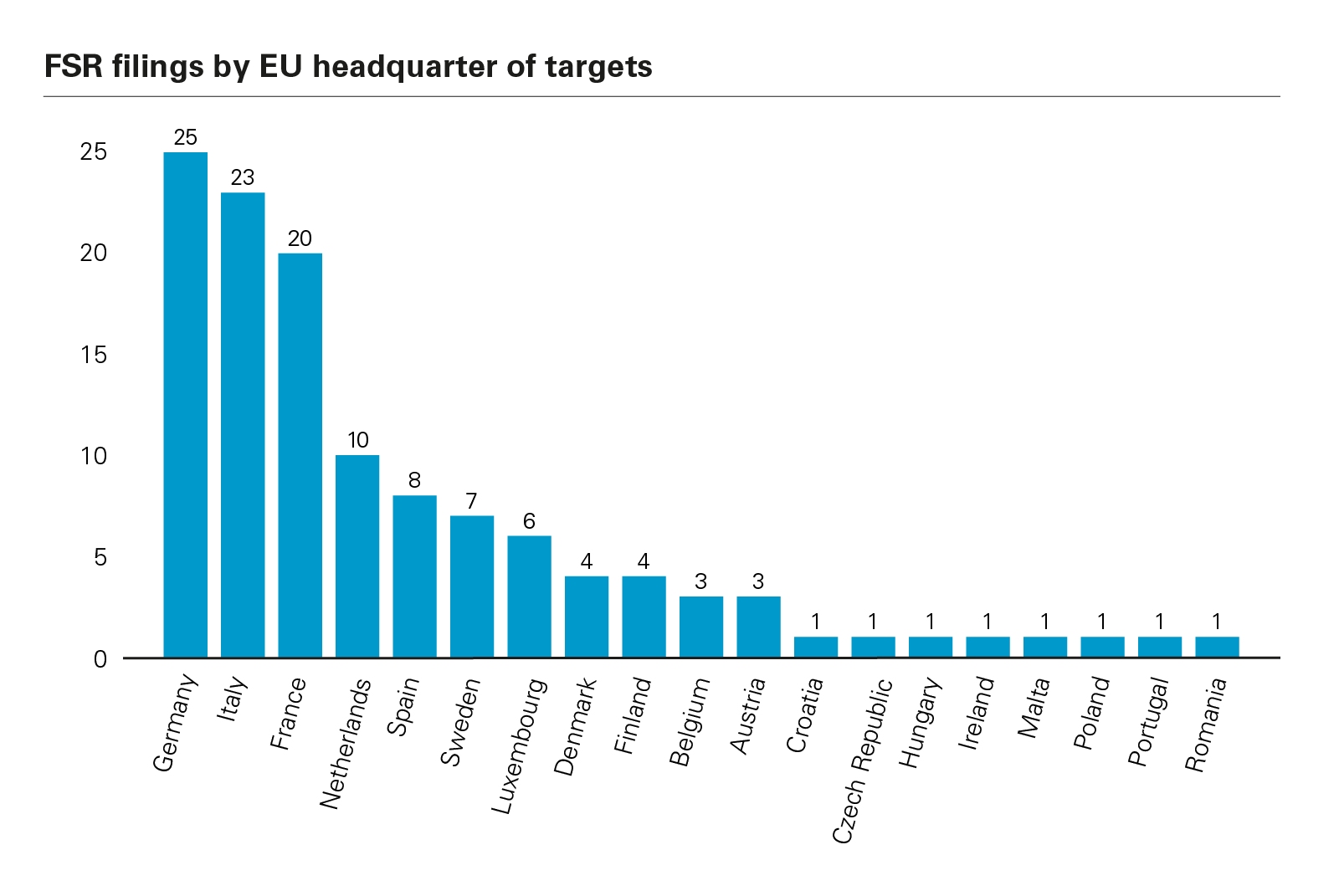

Around 77% of targets are headquartered in the EU, mostly located in Germany, Italy, and France.

View full image: FSR Filings by Target Headquarter EU / Non-EU (PDF)

View full image: FSR Filings by Target Headquarter EU / Non-EU (PDF)

View full image: FSR Filings by EU Headquarter of Targets (PDF)

View full image: FSR Filings by EU Headquarter of Targets (PDF)

In June 2024, the EC opened its first (and so far only) Phase II investigation in Case FS.100011 – Emirates Telecommunications Group ("e&")/PPF Telecom Group ("PPF"). This concerned the acquisition of PPF's telecoms operations in several EU Member States by e&, a telecommunications operator based in the United Arab Emirates ("UAE"), controlled by the Emirates Investment Authority. The transaction was cleared in September 2024 with behavioural remedies, including, inter alia, a commitment that e&'s articles of association do not deviate from ordinary UAE bankruptcy law and that no funding would be provided to the Target group in the EU.

Key policy and organisational developments

The EC is expected to "vigorously enforce" the FSR in support of Europe's long-term competitiveness, as is evident from both the Draghi Report2 and President von der Leyen's Mission Letter to Commissioner Ribera3.

At the same time, enforcement of the FSR must be carefully balanced with the need to maintain the EU's attractiveness to foreign investors. While the EC emphasized the EU's commitment to a balanced approach, compliance with the FSR places a substantial burden on companies' internal resources, particularly in identifying foreign financial contributions (so-called FFCs). The broad scope of notification requirements has frequently been criticized for potentially discouraging foreign investors from pursuing opportunities in the EU.

Yet the high volume of FSR notifications also reflects strong investor appetite in sectors seen as strategic to the EU's competitiveness, including clean tech (such as wind, solar power, electric trains), telecommunications and security equipment.

To cope with the unexpectedly high number of notifications, on 1 March 2024, the EC established a FSR Directorate — 'Directorate K' — within DG COMP. The FSR Directorate now comprises three operational units and around 40 officials.

Key takeaways from the last two years

- The FSR remains a heavy compliance obligation for companies. While the value-based threshold is high (the Target must have an EU turnover of at least 500 million), the scope of reporting is broad. Notifying parties must disclose FFCs received by all controlled subsidiaries, even those with no link to the deal. Some exemptions (such as the fund-to-fund exemption for PE sponsors and the exemption for contracts on market terms) help limit the reporting in certain cases. But in practice, the data collection process is complex and time-consuming — tax measures in particular often require significant work. For example, if a Canadian pharma portfolio company of an investment fund acquires an EU target, the group may need to report FFCs received by unrelated portfolio companies, such as a Malaysian mining business. The EC takes this broad approach because it views money as fungible: a subsidy anywhere in the group could strengthen its position in the EU. That said, in practice, the EC focuses on overlaps or interactions with the acquirer and is often prepared to grant waivers when no such link exists.

- Notifications have far exceeded expectations. Despite the high threshold, the EC initially forecast around 30 filings per year for both M&A and procurement cases. Actual numbers have been much higher (see section above).

- The EC monitors below-the-threshold deals. While the EC has powers to call-in below-the-threshold cases, it has not used them yet. The EC reportedly came close in a building technologies deal involving a Chinese investor and has sent RFIs in other deals that were not made public.

- The EC's first Phase II decision in e&/PPF sheds light on how it assesses distortion. The decision shows how foreign subsidies, such as unlimited guarantees, can be considered distortive. While the case confirms that FSR clearance is possible even in complex scenarios, the EC took a formalistic approach to several concepts. The remedies may also be hard to replicate in other contexts — particularly where the target needs investment. While many transactions are caught by the FSR, e&/PPF also remains the only decision to date where the EC found distortive subsidies. The case is expected to shape the EC's upcoming guidelines on distortion under the FSR. The ADNOC/Covestro deal, which involves the potential acquisition of a German chemicals group by the Abu Dhabi based energy group, is expected to give further guidance on this topic.

- Ex officio enforcement is gaining momentum. The EC has the power to launch ex-officio investigations into potentially distortive foreign subsidies on its own initiative (or based on information from Member States or complainants), including but not limited to M&A deals and public tenders. The first two cases (in security equipment and wind power) in which it did so are already underway, reportedly focusing on Chinese players. We can expect more active FSR enforcement in this area, particularly in sectors seen as sensitive or critical to EU competitiveness. However, more resources will be needed for this to happen at speed.

- Practical tips – what we've seen in practice:

- Pre-notification can be long, but things are improving. The EC's information requests remain burdensome and time-consuming, but we are seeing more flexibility. In sectors the EC now understands better, such as PE, the EC is becoming more open to granting waivers and streamlining reviews.

- Disclosure obligations depend on the type of acquirer. Acquirers must disclose FFCs received by any entities the group controls (typically >50% of voting rights or veto rights over key decisions like budget, business plan, or senior management). PE sponsors may benefit from the fund-by-fund exemption (see our previous alert), limiting disclosure to only the acquiring fund. This exemption does not apply to sovereign wealth funds or corporates, but waivers can still help carve out parts of the group that have no link to the deal.

- Cooperation matters. If parties do not cooperate, the EC can base its findings solely on information available and we understand that this may be applied in ex-officio investigations. That is what appears to have happened in e&/PPF, where the EC inferred subsidies to the parent company (EIA) from financial and public sources.

- Remedies under the FSR are still uncharted territory. Unlike merger control, remedies can only be accepted in Phase II (though discussions can start earlier). In e&/PPF, far-reaching behavioural commitments were accepted. This raises open questions on how far remedies must go, and whether restrictions on future funding qualify as merger-specific. These issues will likely shape the future distortion guidelines and the EC's practice.

Looking ahead – key enforcement trends and priorities:

- The EC is learning by doing. As its experience grows, the EC is becoming more targeted in its questions and increasingly open to granting waivers, particularly where the information is not essential to assess the transaction.

- More flexibility, guidance and simplification ahead. A formal enforcement report is due in July 2026 and may propose simplification measures, including a fast-track procedure for certain cases. By January 2026, the EC must also adopt distortion guidelines on the substantive tests under the FSR. A public consultation has been launched, and a draft text is expected to be published in July 2025.

- Call-in powers are under close watch. The EC is actively tracking below-threshold acquisitions and may intervene where deals appear to be part of a broader acquisition strategy. With the creation of a dedicated FSR directorate, the EC now has greater resources and is expected to start using its call-in powers.

- Origin of funds remains a key focus. The EC is likely to continue scrutinising deal financing structures, with particular attention to state-backed guarantees or other non-commercial funding.

- Consolidation with other regulatory regimes remains unlikely. While there is growing overlap in enforcement tools, the EC sees FSR and FDI as serving distinct purposes and has pushed back on calls for a single "super" M&A screening mechanism.

Anastasios Tsochatzidis (White & Case, Trainee, Brussels) contributed to the development of this publication.

1 All statistics in this alert are updated as of 10 June 2025.

2 "It is of paramount importance for the EU that [FSR] rules are applied effectively and result in the intended benefits for EU consumers and businesses", Draghi report – Part B, The future of European competitiveness, September 2024, available here.

3 "You will work with other Members of College to vigorously enforce the Foreign Subsidies Regulation, including by proactively mapping the most problematic practices that could lead to competition distortions", President von der Leyen's Mission Letter to Teresa Ribera Rodriguez, 17 September 2024, available here.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP