UK FDI Year in Review: a look at the first year of the National Security and Investment Act

6 min read

4 January 2023 marked the one-year anniversary of the coming into force of the UK's National Security and Investment Act. We take a look at decisional practice to date and the lessons learned from the regime so far.

Overview: the NSIA in brief

The National Security and Investment Act 2021 (NSIA) became operational on 4 January 2022 and has since become a regular feature of transactions. The regime is administered by the Investment Security Unit (ISU) within the Department of Business, Energy and Industrial Strategy (BEIS), with the Secretary of State (SoS) exercising final decision-making powers.

Qualifying transactions require notification if the Target carries on specified activities in any one of seventeen "sensitive sectors", and the acquirer proposes to buy 25% or more of shares, or voting rights, in the Target. Our more detailed overview of the NSIA, including notification triggers and timelines is accessible here.

Decisions to Date

Prohibitions

There have been five prohibitions in the first year of the NSIA. These were:

- University of Manchester / Beijing Vision Technology Company Ltd.

- Pulsic Limited / Super Orange HK Holding Limited

- Nexperia / Newport Wafer Fab

- HiLight Research Limited / SiLight (Shanghai) Semiconductor Limited

- Upp Corporation Limited (previously Fibre Me Limited) / L1T FM Holdings UK Limited.

Unusually, the NSIA had retrospective effect from the date the proposed legislation was announced on 12 November 2020. As a result, the final orders issued with respect to two of the blocked transactions – Nexperia / Newport Faber and Upp / L1T – unwound previously concluded deals. Indeed, the Upp transaction was concluded in January 2021, demonstrating the scope of the powers conferred by the NSIA to retroactively "call-in" transactions concluded before its coming into force.

This retroactive power to call-in a transaction for review ordinarily applies for up to five years from the date of the transaction, although this can be reduced to six months if the SoS becomes aware of the transaction. Voluntary notification of transactions not subject to mandatory notification can be used to mitigate this risk but it is also notable that of the prohibited transactions, one, SCAMP, emanated from a voluntary filing, as did at least three of the nine conditional decisions taken to date (see further below).

Of most note in terms of trends in prohibition decision is the relevance of investor origin. Of the five prohibitions, four related to investors from China or Hong Kong, whilst the most recent, the Upp decision, concerned the acquisition of UK broadband firm Upp by a subsidiary of LetterOne, which is Russian-backed.

Conditional Decisions

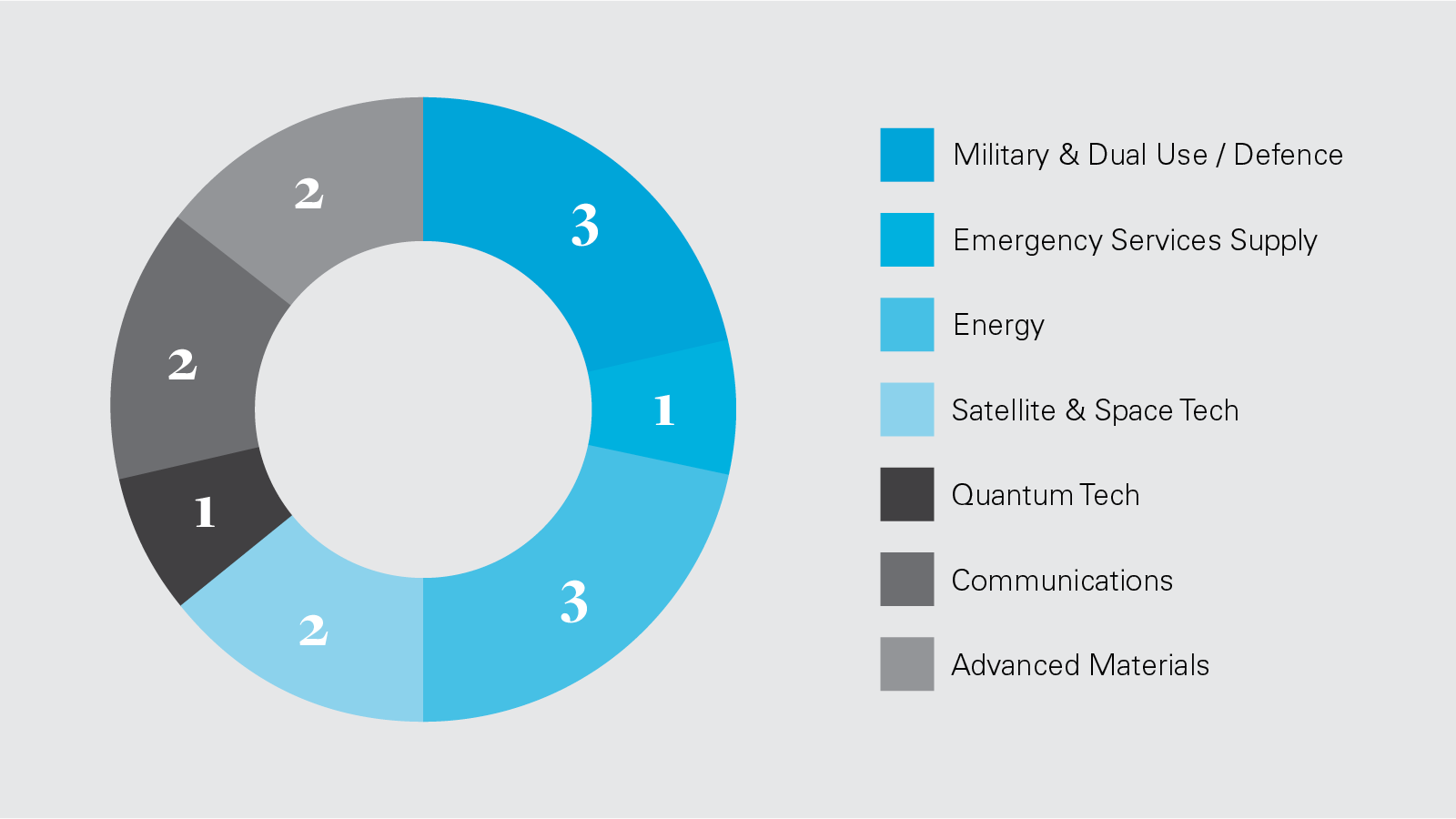

There were nine conditional decisions in 2022. These concerned transactions in energy, satellite & space technology, communications, quantum technology, suppliers to the emergency services and military and dual-use / defence.

Scope of Commitments

The precise scope of the commitments offered is limited, given the ISU's general approach to final orders, which is to publish sparse details. To date, all conditions have been behavioural rather than structural. Several transactions have included general requirements to institute enhanced security controls and put information barriers in place.

In terms of sectoral focus, there have been three conditional decisions in the energy sector: Stonehill asset development project, Electricity Northwest Limited / Redrock Investment Limited and XRE Alpha Power Limited / China International Power Holdings Limited. These have included sector-specific conditions, for example, requirements to:

- Obtain Government approval before appointing a power offtake operator and ancillary service providers; and

- Restrict information flows between a power offtake operator, asset operator and site operator and the acquirer.

Government pre-approval is also a feature of more general conditions, such as the appointment of an approved auditor to carry out a security assessment, requiring that a Government-approved observer be appointed to a target subsidiary board and appointment of a Chief Information Security Officer approved by the SoS.

Investor Origin

The focus on China apparent from the prohibition decisions is also discernible in the conditional decisions, with four of the nine conditional decisions involving investors with links to China. However, acquirers from jurisdictions traditionally considered friendly to the UK have also been subject to conditional approvals: Inmarsat / Viasat, for example, was a US acquisition cleared on condition that information protection protocols are introduced as well as a commitment to ensure that both parties continue to provide strategic capabilities to the UK Government.

Sectoral Focus

The content of final orders is very light with decisions typically not identifying the sensitive sector that has triggered the notification. However, based on the details available, it is possible to extrapolate which sectors are featuring in prohibition and conditional decisions. The sensitive sectors in which prohibition and conditional decisions have thus far been adopted are set out below, along with the corresponding number of final orders.

The NSIA Annual Report, due for publication in spring 2023, should reveal whether these numbers correspond proportionately to the sectors triggering notifications, or represent a particular sectoral focus from BEIS.

Trends: Process and Practice

Before the NSIA entered into force, the ISU was very amenable to consultation on potential transactions, but since it has started receiving formal notifications it is less open to these discussions. The NSIA process can be something of an information vacuum. There is typically no engagement for uncontroversial transactions, but even call-in reviews can, for instance, be conducted without any engagement from the ISU. Nevertheless, it is important for investors to be aware that the NSIA legislation mandates that even unprompted engagement from the parties must be taken into account before a decision is taken.

In terms of timing, early practice saw uncontroversial transactions being cleared quickly, but now the regime is in full swing the ISU will typically take almost the full 30 working days to issue a decision as the volume of notifications received has increased, which is important to factor into transaction timelines. The maximum timeline from the date a notification is confirmed as accepted (which typically takes 3-4 working days) is 105 working days, with a timeline of 75 working days from the date of any call-in notice. However, there is scope for that timeline to be extended with the notifying party's consent. For example, the Nexperia transaction was first called in on 21 May 2022 with no final decision taken until 18 November 2022. This totals 124 working days from the call-in date, and over 18 months from the date of the acquisition.

Outlook and Analysis

As well as the 2023 Annual Report, 2023 looks set to bring us the first appeal of an NSIA final order. Nexperia has been unequivocal about its intentions to appeal the unwinding decision issued with respect to its completed acquisition of Newport Wafer Fab. That appeal will need to take a form of judicial review proceedings. The Nexperia appeal, assuming it goes ahead, should put the ISU's lack of transparency under a spotlight.

Indeed, the Nexperia prohibition is probably the best illustration of how dynamic an instrument the NSIA has become in a very short period of time, as well as the breadth of the powers that are vested in the SoS as the ultimate decision-marker.

"Today I've issued a Final Order under the NSI Act requiring Nexperia to sell at least 86% of Newport Wafer Fab. We welcome foreign trade & investment that supports growth and jobs. But where we identify a risk to national security we will act decisively." Rt Hon Grant Shapps MP

There have been three SoS in the year since the NSIA regime became effective. The difference in approach by the various office-holders is particularly apparent Nexperia given Kwasi Kwarteng, the first NSIA Secretary of State, was originally minded not to call-in the transaction at all, according to a letter written by Tom Tugendhat MP to then Prime Minister Boris Johnson in July 2021 urging intervention. This position was reversed, however, with the deal being exposed to further scrutiny under the NSIA call-in process before eventually being prohibited, mandating an unwinding of the completed transaction, per a final order published by Mr Shapps on 16 November 2022.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP