Asia-Pacific oil & gas infrastructure: New opportunities for the nontraditional investor

Without being part of the full hydrocarbon value chain, pension and super funds are now claiming stakes in the Asia-Pacific oil & gas market, bringing into play nontraditional sources of funding for processing infrastructure assets in the region. But can these new entrants navigate the underlying risks and complex legal and regulatory challenges surrounding this asset class?

15 min read

Subscribe

Stay current on your favorite topics

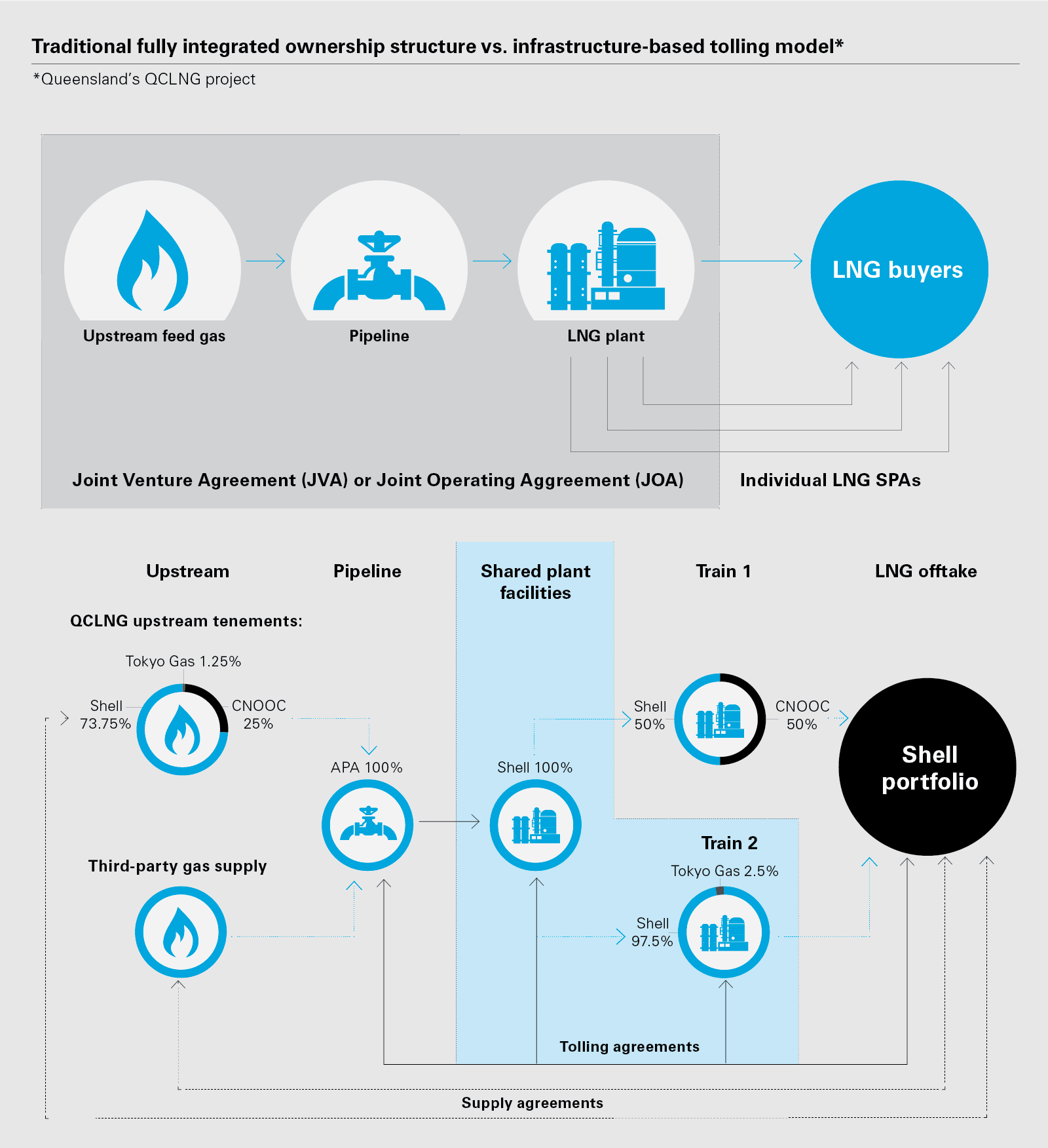

Big changes are afoot in the Asia-Pacific oil & gas sector. The region is witnessing a shift away from the traditional resource-based fully integrated ownership and governance model, which allows resource owners to use their own infrastructure to bring products to market, toward an infrastructure-based model. Under this model, revenues are sourced from a range of resource owners using a tolling— or "user pays"—system.

The nontraditional investors now have a “once in a generation” opportunity to enter the hydrocarbon market and take advantage of the assets being sold at discounted rates

Key drivers

Historically, complex hydrocarbon projects operated as integrated entities, but now the efficacy of this single structure is being called into question. One of the key factors underpinning this profound shift away from the fully integrated model is the desire of oil & gas incumbents to free up capital across the hydrocarbon value chain and efficiently deploy it on other ventures, particularly those enabling them to lower their carbon footprint.

It also comes down to simple economics and business sense. Upstream field owners cannot justify the capex on offshore infrastructure on a stand-alone basis, so the tolling model allows them to avoid that capital outlay by using infrastructure owned by third parties and where the payment to those third parties is spread out over a number of years.

In addition, third-party ownership and tolling arrangements allow joint venture (JV) partners to exit when the interests between the owners of the processing infrastructure and upstream fields are no longer fully aligned, or one or more JV participants is looking to exit, particularly when the remaining JV partner is not providing access rights to processing infrastructure on an "all users equal" basis.

As integrated upstream projects disaggregate, processing infrastructure owners find themselves in a difficult position—sitting on what have effectively become stranded assets—compelled to seek innovative operating structures to maximize returns. As a result, common facilities are now emerging that are able to serve multiple upstream fields.

The adverse oil price environment has also given an additional impetus to the disaggregation of the fully integrated ownership, as oil majors seek to dispose of noncore assets. All these factors have led to the "once in a generation" opportunity for the nontraditional investors to enter the hydrocarbon market and take advantage of the assets being sold at discounted rates. Gaining access to such assets will allow investors to capture value from the disaggregation of ownership structures and develop particular expertise in the niche areas of the oil & gas market and in many circumstances without the market risk, given that the upstream participants are willing to enter into long-term contracts for use of the assets.

According to Kyle Mangini, Global Head of Infrastructure at Melbourne-based IFM Investors, who is responsible for implementing the fund manager's infrastructure investment strategy, bringing financial investors into the space makes a lot of sense. "Infrastructure investors tend to be very long term, and very patient. And that's a pretty attractive set of characteristics."

US$12 billion

An estimated US$12 billion worth of new upstream assets could come up for sale across Asia-Pacific in the near future

Source: Wood Mackenzie

View full image: Traditional fully integrated ownership structure vs. infrastructure-based tolling model (PDF)

View full image: Traditional fully integrated ownership structure vs. infrastructure-based tolling model (PDF)

The pension and super funds are ready to plow vast amounts of capital into oil & gas infrastructure, compelled by the prospect of stable infrastructure-style revenue streams that have the added benefit of diversifying their portfolios

The rise of nontraditional investors

The infrastructure-based tolling model is, of course, not new. It is well established in the US and the UK North Sea but is relatively new to Asia-Pacific, and it is now paving the way for a new class of investors in the region.

There is an economic logic driving these investors toward oil & gas, as Tim Baldwin, CEO of GB Energy, the developer of Australia's Golden Beach Gas project, explains. "The explorers, developers and the infrastructure players have seen costs increase markedly over the past ten years. They are now looking to be much more capital-efficient, whether that's reducing capital, or whether it's reducing the cost of capital."

Observationally, deal flow in this space is a function of the price of oil. "At US$100 a barrel, there's not a lot of interest in divesting assets. But when prices are at the lower end of the cycle, there tends to be more internal competition for capital within the organization, and a greater willingness to think about bringing in outside investors. When the prices are high and cash flow is strong, there tends to be much less of an interest," says Mangini.

A spate of recent asset disposals underpins the burgeoning interest. Energy majors are seeking ways to monetize their infrastructure assets and deploy the capital elsewhere in the value chain, including in ventures that will facilitate a less greenhouse-intensive energy mix. Australia's LNG projects are a case in point: In June 2020, Royal Dutch Shell announced it was considering raising more than US$2 billion from the sale of a stake in the common facilities at its Queensland Curtis LNG plant. US major Chevron—a founding member of Australia's North West Shelf (NWS) project for 30 years—also in June 2020 announced it would sell its 16.6 percent interest in the gas project after receiving interest from credible buyers. It has been reported that Woodside is also considering acquiring Chevron's stake in NWS. Reports suggested Woodside would bid in conjunction with an infrastructure fund as the LNG train facilities shift to a third-party tolling agreement. This involves processing gas from producers outside the six NWS shareholders, providing a chance for new long-term contracts and bringing in an owner with a lower cost of capital.

US$71.38

Brent crude oil price per barrel as of March 8, 2021

Source: FT

In November 2020, Woodside Energy said it was on course to sell approximately 50 percent of its proposed US$6 billion Pluto Train 2 LNG liquefaction facility to infrastructure investors, and that it is considering offloading parts of other assets.

Woodside CFO, Sherry Duhe, said interest from infrastructure investors had grown stronger. The company is reported to be wanting to sell some of its infrastructure assets to investors to fund new projects. Woodside will target equity holdings of approximately 50 percent, with the sales raising money to fund project developments.

Earlier, US oil major ExxonMobil had indicated an intention to sell its Gippsland Basin assets in Australia, though it has been reported that those plans have been withdrawn.

This marks a shift in attitude. Historically, oil & gas asset holders were resistant to outside participation. "Producers with large positions in a basin seemed to try to protect their turf, which is quite different in the US where there's been more activity, and which has made it a much more efficient market," says Baldwin.

Recent moves have whetted international infrastructure investors' appetite for the Asia-Pacific asset market. As a result, a well-heeled group of financial investors has emerged onto the scene. Pension and super funds have started entering the LNG infrastructure space and are now moving onto upstream oil & gas assets that were once part of fully integrated resource-based structures.

These investors are ready to plow vast amounts of capital into oil & gas infrastructure, compelled by the prospect of stable infrastructure-style revenue streams that have the added benefit of diversifying their portfolios. Large pension funds and sovereign wealth funds have boosted direct allocations to oil & gas pipeline infrastructure in recent years.

US$426 million

Deal activity in Asia-Pacific as of mid-November 2020, down from US$5.1 billion in 2019

Source: Wood Mackenzie

Experienced investors attest to their robust appetite for such assets. "There are investors like us, which are fund-based and then there are other large institutional investors like the Canadian pension funds, all of whom are active in this market and are familiar with the asset class," says Mangini. "The appetite has been there for a long time, and yet the demand has been unfulfilled."

One attraction for incumbent asset holders considering sales is that institutional money is not competitive to them—in the sense that the oil companies are not selling assets to their competitors—they're selling assets to financial investors. That provides relatively more comfort.

And as more transactions are done, those comfort levels will only increase, says Mangini. "There's a recognition that this is capital that does not otherwise compete with the majors so it's very different from entering into a divestiture where you're selling it to another oil company. This is a fundamentally different and very deep pool of capital."

Having a long-term lens is key. Infrastructure investors view these as essentially long-life assets. However, the preference is for these assets to be already in operation, essentially brownfield assets. "The key issue is that they don't want to be exposed to geological or subsurface risk," says Baldwin. "And they're generally reluctant to provide development capital. They would much rather pay a huge premium for something that's actually in operation. So there is a little bit of a disconnect that the market is trying to work through."

However, there are ways of mitigating the greenfield risk. "You're just pricing a different risk profile. So as you go through the process of building an asset and commissioning it, and demonstrating that it works effectively, you're de-risking the asset."

As ownership models start to evolve, investors' interests are shifting too. Pension and super funds are now taking stakes in oil & gas assets directly without being part of the full hydrocarbon value chain. Such investors are generally not looking for quick exits or booking quick gains, so long-term infrastructure-style returns are attractive.

Investment in this sector requires a comprehensive understanding of the upstream production regime and operational risks inherent in complex hydrocarbon projects, from governance and competition issues to reputational risk and potential exposure to environmental and safety liabilities

Overcoming challenges

But, investment in this sector is not without its challenges and risks. It requires a comprehensive understanding of the upstream production regime and operational risks inherent in complex hydrocarbon projects, from governance and competition issues to reputational risk and potential exposure to environmental and safety liabilities. From an operational standpoint, these new entrants will need to be able to renegotiate commercial arrangements to align with their desired risk profile, and restructure the governance arrangements under the joint operating agreement (JoA) in order to carve out the relevant assets.

This is particularly evident in Australia, where LNG projects have predominantly adopted fully integrated structures in which project participants hold ownership interests across the entire hydrocarbon value chain through highly complex corporate JV arrangements. These arrangements involve either a single JV—whether incorporated or unincorporated—or a combination of an unincorporated JV with an incorporated OpCo, typically used, with one participant or the jointly owned OpCo designated as the operator of all, or a significant portion, of the integrated project.

Despite the sizable offering, ensuring deal success is not easy. Understanding the project finance risk profile is also key. Traditionally, investment in Australian oil & gas assets has been led by balance-sheet financing supported by direct supply purchase agreements (SPAs). In contrast, North American assets have more frequently seen nonrecourse project financing supported by lifting and tolling agreements (LTAs) on a take-or-pay basis. This means that the risk profiles and the nature of the agreements themselves in Australia are likely to be different from those of nonrecourse project finance agreements used in the US.

The potential for disputes between owners within the overall project is another obstacle. There remains a region-wide legacy of integrated unincorporated JVs in which each JV partner owns a portion of the equity with alignment of interests across the value chain. If equity in some assets is held instead by a separate special purpose vehicle (SPV) with different owners, alignment could break down and disputes between different interest holders across the project value chain could increase. For this reason, many projects have a "stapled interest" mechanism and departing from this to bring in a new owner for only some portion of project assets could be challenging. Exit strategies for fund investors may also be more limited if the investments are not placed into SPVs established for the sole purpose of operating the relevant assets.

60%

LNG opportunities account for almost 60% of the new upstream opportunities in Asia-Pacific

Source: Wood Mackenzie

There is also exposure to tax and stamp duty obligations, with some taxes owed immediately if no capital costs are outlaid.

The issues associated with decommissioning will also need to be carefully considered, and the issues and risks associated with decommissioning will vary from jurisdiction to jurisdiction. In many countries in Asia-Pacific, legislative frameworks are in early stages of development, and the provisions in older contracts, which were signed when decommissioning was a distant concern, often fail to cover in full or in any detail decommissioning responsibilities.

Intellectual property rights (IPR) issues figure prominently. Oil & gas assets generally involve complex operating equipment that requires significant in-house knowledge and know-how and/or licenses and IPR arrangements with specialist technical providers. Parties are generally reluctant to invite suitors into their day-to-day operations and risk losing know-how that has been developed over an extended period. That can lead to difficulties in conducting the necessary diligence activities required when purchasing operational assets.

The underlying nature of oil & gas assets is inherently more risky than traditional asset classes. In Australia, these are often isolated "field specific" investments (unlike in North America, where assets are able to service multiple fields within the same vicinity), so diligence on the underlying tenements—and the particular equipment—becomes even more critical.

Investment in this asset class requires investors to take a view of the future of oil & gas and the global push to reduce emissions. Oil & gas investments could become stranded assets should emission targets be intensified, and renewables favored in the short to medium term. Environmental, social and corporate governance (ESG) issues are a key consideration, particularly in light of growing shareholder activism. Coal has long felt the impact of activist groups, and now natural gas is attracting more of their attention.

The process will force both buyer and vendor to assess and allocate risk in a thoroughly detailed and considered manner. "The process is hugely complicated from a legal perspective. Every contract that you do in this space is going to be bespoke, because every situation is different. That means your legal team needs to really have a deep understanding of the risks, the counterparties, the different structures and how to fit them together. That's a fairly unique skillset," says Baldwin.

Regulatory certainty is also important. In parts of Asia-Pacific, where state-owned national oil companies are mandated to operate oil & gas infrastructure on behalf of the government, the investment landscape can be extremely challenging to navigate for outside entrants.

As investment activity shifts from midstream to upstream infrastructure, complexity levels increase; it is a big step investing in an offshore platform providing services to third-party market participants, compared to buying into an onshore pipeline system.

Investors have a variety of means to deal with such challenges. In the US, one method in use is to dedicate reserves to the pipeline. This in turn requires a deeper understanding of what the upstream arrangements are, because without it, the risk of holding a stranded asset amplifies.

The confluence of interests between investors looking for stable assets to place capital into and resource holders looking to scale down their interests in parts of the extended value chain has created an exciting and vibrant market

Optimism for the future

Growth in urbanization and electrification of energy consumption in Asia-Pacific, driven by the expanding middle class, will continue to underpin the demand for LNG in the future. Governments across the region are looking to an infrastructure-led recovery in overcoming the devastating economic impacts of COVID-19. But how will Asia-Pacific oil & gas infrastructure assets fare against the backdrop of the global oversupply of oil?

This raises important questions for nontraditional investors as they enter the market. They will have to take a firm view as to whether this is the right place for them to be in the long term. They may have support from their investor base at the time of investment, while there are still good returns to be made, but will they find themselves under increased scrutiny from ESG-conscious shareholder activists in the future?

"Where there's probably going to be an increased focus is the risk of carbon," says Mangini. "Whereas these assets were previously viewed [as] a perpetuity that would go on forever, now they are much more thought of as an annuity in the sense that it's going to have a finite life. One can debate how long that life is. But given the focus on carbon, that's going to continue to be a risk."

The confluence of interests between investors looking for stable assets to place capital into and resource holders looking to scale down their interests in parts of the extended value chain has created an exciting and vibrant market, with a "once in a generation" opportunity for the nontraditional investors in this sector. But, will they take advantage of this opportunity and use it wisely? Only time will tell.

This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.

© 2021 White & Case LLP