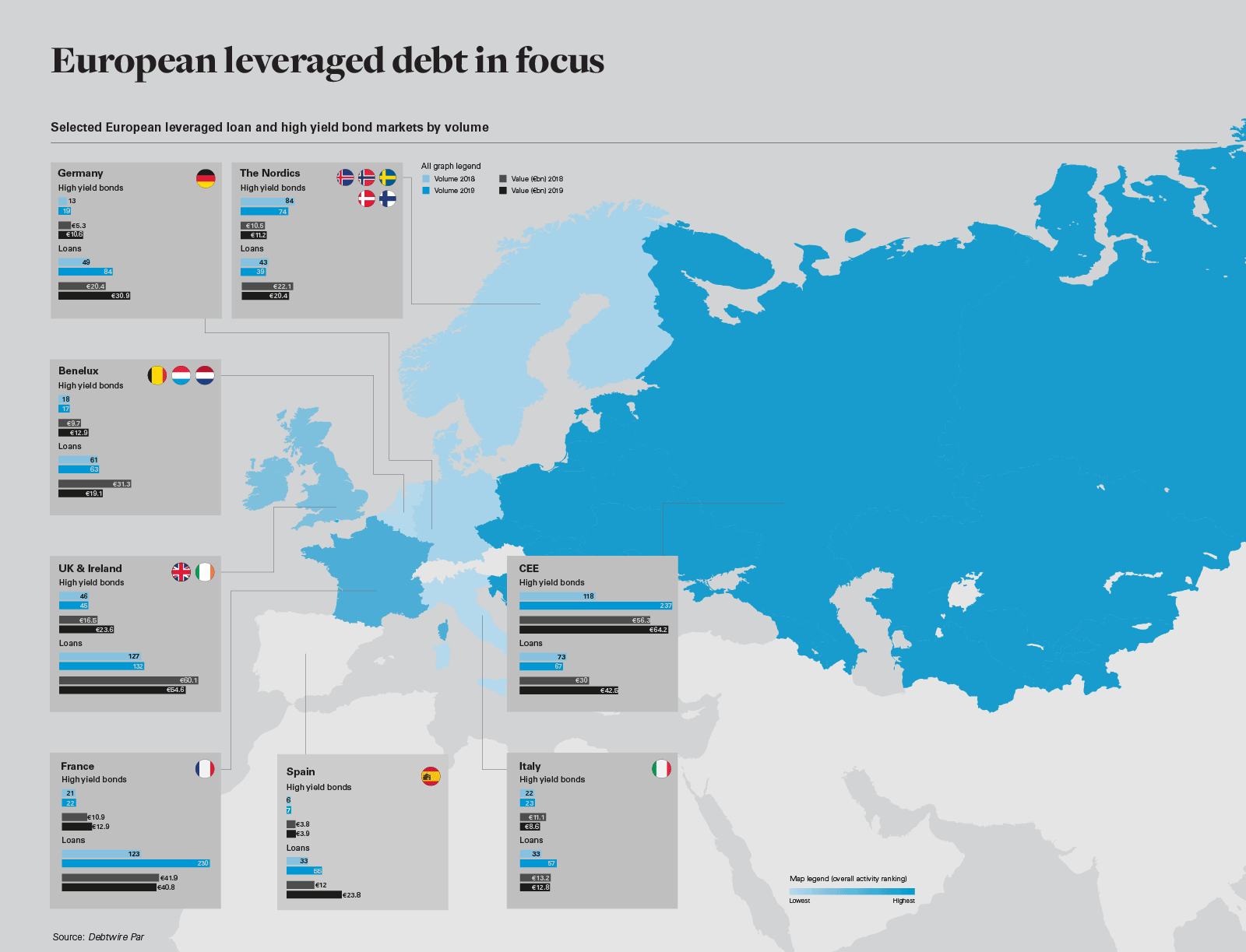

The Spanish leveraged finance market went from strength-to strength in 2019, with a selection of large deals and the market’s capacity to execute complex deal structures pushing issuance to four-year highs.

High yield offered few surprises in 2019, but the leveraged finance market in Spain has enjoyed a particularly good year, boosted by several larger deals and significant activity in the mid-market, which is the biggest market in the country. The market has matured, grown

more sophisticated and, as far as investors are concerned, is more closely aligned with Western European trends than ever before.

By the end of 2019, Spanish leveraged finance issuance (loans and high yield) totalled €27.7 billion across 64 deals. This was well ahead of the €15.7 billion issued during all of 2018 and the €20.7 billion of issuance in 2017.

Maturity matters

The market’s maturity is evidenced by pricing in Spain, where spreads have narrowed. In 2014, institutional Spanish loans were priced at 389 basis points (bps) versus 424 bps in the UK, 410 bps in France and 416 bps in Germany, according to Debtwire Par data. In 2019, Spanish loans were pricing at 342 bps on average, versus 381 bps in the UK, 407 bps in France and 396 bps in Germany.

The growth of Spain’s market is further reflected in the big-ticket deals the market has been able to digest and deliver.

KKR’s €602.23 million (US$667.5 million) take-private of pizza group Telepizza, for example, saw the investment firm start out with a standard bridge loan and revolving credit facility, with a view to refinance the whole facility through a €333.8 million (US$370 million) high yield bond priced at 6.25 per cent, according to Debtwire Par.

This deal was particularly notable in that the bridge loan was subject to English law, while the covenant package was subject to New York law. A few years ago, the Spanish market would have found it difficult to understand a complex structure like this. In today’s more sophisticated market, deals like these are no longer unusual.

Grifols is another prime example: The pharmaceuticals group secured a refinancing involving a term loan B (TLB) that sat alongside a high yield bond and a super-senior revolving credit facility. Spanish telecoms group MásMóvil, meanwhile, sought to refinance a convertible bond and simultaneously increase its debt in 2019 by combining a covenantlite loan with the issue of preferred equity.

While TLB structures were considered better suited to London and New York a few years ago, they are now viewed as another viable source of financing by banks and borrowers in Spain.

Spain enters new territory

Deal momentum is expected to carry the market in 2020, with airline operator IAG’s €1 billion (US$1.11 billion) acquisition of Air Europa and a bidding war for Spanish Stock Exchange group BME both expected to tap into leveraged markets.

Despite the positive outlook and cov-lite characteristics of loan issuance, however, an uptick in restructuring activity is anticipated. Deals like the €1.8 billion (US$2 billion) issue for supermarket cooperative Eroski have already made a telling contribution to restructuring values. With the Spanish Socialist Workers’ Party winning the most seats in the November 2019 general election, rising taxes are also a distinct possibility and could weigh on both consumer spending and corporate cash flows

While acquisitions are in the pipeline, the market may see more restructurings by Q3 and Q4 2020, running in parallel with acquisitions. This is new territory for Spain, and should make for an interesting year ahead.

"The leveraged finance market in Spain has enjoyed a particularly good year, boosted by several larger deals and significant activity in the mid-market, which is the biggest market in the country."

European leveraged debt in focus (PDF)

European leveraged debt in focus (PDF)