France

The most notable development for the French Competition Authority over the past 18 months has been its growing attention to the digitalization of merger control.

20 min read

Subscribe

Stay current on your favorite topics

The merger control procedure before the FCA has been increasingly characterized by a search for greater precision in its analyses, with tailor-made solutions, including use of behavioral commitments

Key developments

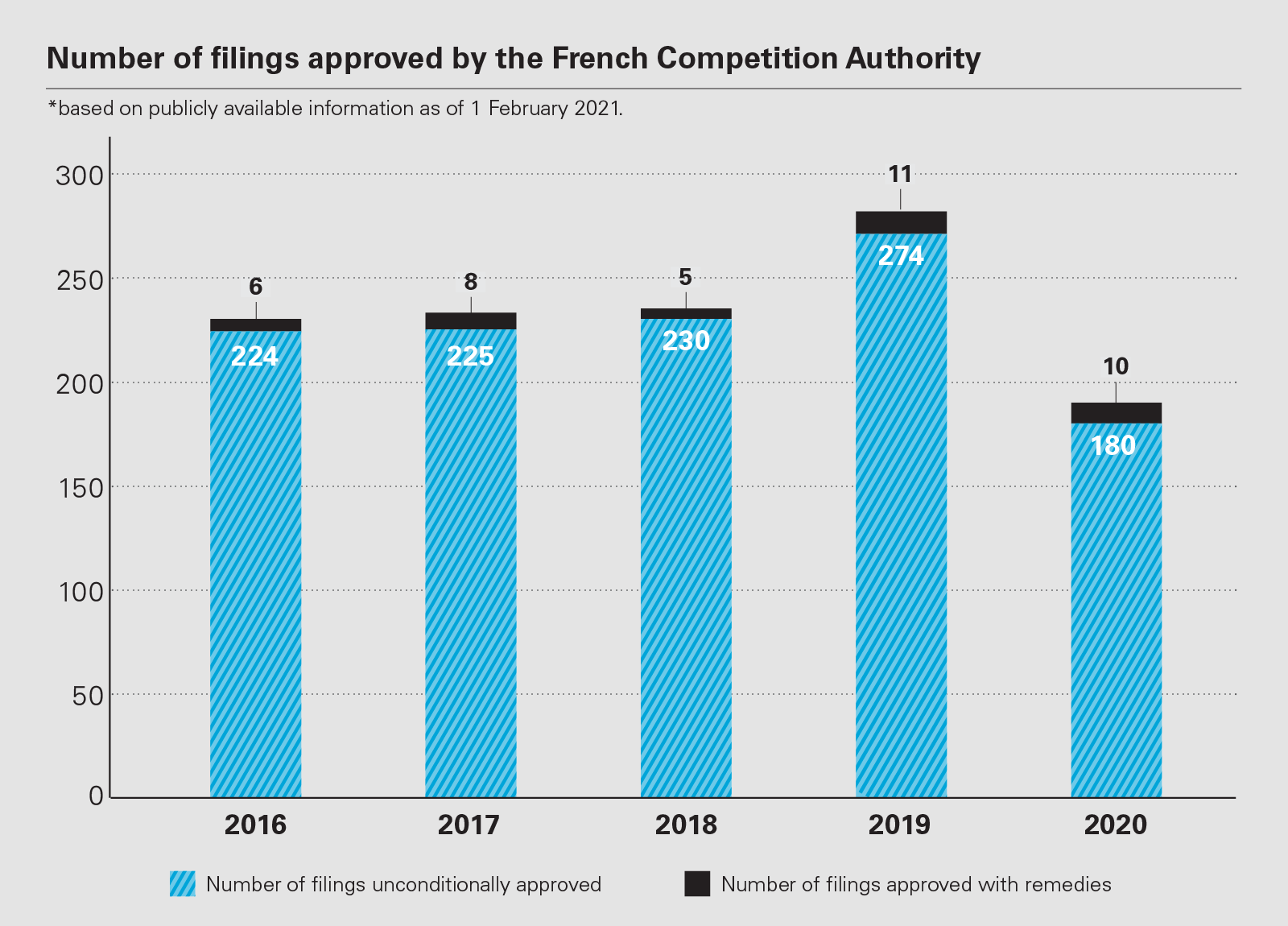

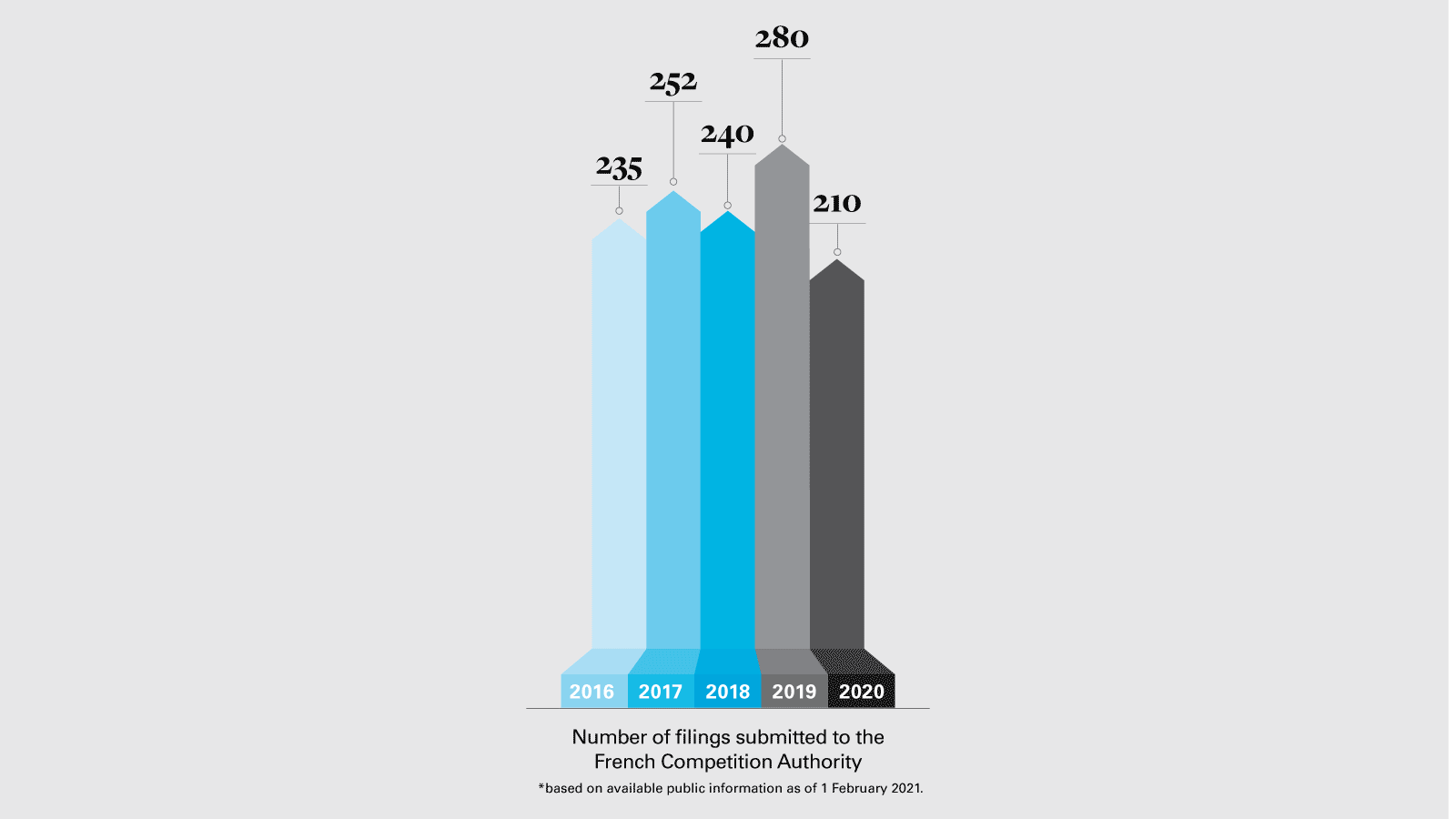

A quick look at the year 2019 shows that the French Competition Authority (FCA) was very active, with 285 authorization decisions, of which eleven were cleared with conditions. However, these activity levels reduced in 2020, probably due to the COVID-19 pandemic: the FCA only rendered 210 merger decisions based on publicly available information as of 1st February 2021.

The main developments in the past year include a focus on digital issues, particularly large digital platforms; an emphasis on behavioral commitments and their monitoring; and the modernization of the notification procedure.

From a substantive perspective, the most notable development has been the growing attention given by the FCA to digital issues relating to merger control.

First, the FCA updated its market definitions to take into account the growth of online sales in the retail sector. For instance, in its 2019 decision on Luderix's acquisition of Jellej Jouets, the FCA considered that the retail toy market included both in-store and online sales.

In a study on competition and e-commerce released in June 2020, the FCA said the rapid growth of e-commerce—accentuated by the COVID-19 pandemic—had led it to adapt its analytical framework by more frequently identifying relevant markets that cover both online and offline sales.

This trend follows the landmark 2016 Fnac/Darty decision, in which the FCA updated its product market definition on the retail market for electronic products by considering that in-store sales and online sales were part of the same market, and that online sales exerted significant competitive pressure at the retail level.

The merger guidelines introduced in July 2020 now contain a section dedicated to online sales, in which the FCA specified the elements that should be taken into consideration when assessing the substitutability of in-store and online sales.

The FCA made digital issues in competition law one of its main priorities in 2020, as illustrated by the creation of a specific service for the digital economy within the FCA organization. It has also voiced the need to adapt the legal framework in order to deal with competitive issues relating to large digital platforms. At the end of 2020, the FCA announced that digital issues would remain a top priority in 2021 and that its specific service for the digital economy would strengthen its expertise on platforms, algorithms and data sciences.

The FCA has been making consistent use of behavioral commitments and, in line with its practice in past years, has been closely monitoring compliance with the remedies made binding by its merger control decisions. Among the nine FCA-conditional clearances in 2019, three included behavioral commitments while in 2020, four out of ten conditional decisions contained behavioral remedies.

For instance, in August 2019, the FCA approved, subject to behavioral remedies only, the creation of TV platform Salto by TF1, France Televisions and Metropole Television. Salto offers television services, including free-to-air television channels and related services, directly over the internet.

The FCA identified several competition concerns. The FCA considered that the parent companies were likely to use their strong market position for the acquisition of linear broadcasting rights in order to favor Salto's access to non-linear broadcasting content.

The authority also found that the parties would have the ability and incentive to eliminate competitors' access to their channels and related services. Finally, the FCA was concerned that the common platform would increase market transparency and facilitate coordination between the parent companies.

Despite these strong competition concerns, the FCA cleared the transaction subject to several behavioral commitments, including: limiting the amount of video-on- demand content that Salto can purchase from the parties, excluding any exclusive distribution agreements by Salto; offering on objective and non- discriminatory terms the distribution of the parties' free-to-air channels along with their associated services to any interested third-party distributor; and, lastly, establishing a set of guarantees to limit the exchange of information.

Similarly, in its RATP Développement/Keolis/CDG Express decision of April 2019, the FCA conditionally authorized the creation of a joint venture for the operation of the CDG Express transport between the center of Paris and Paris-Charles de Gaulle airport.

The FCA had identified the risk that the new entity could rely on its market position for the provision of public transport between Paris and Paris- Charles de Gaulle to sell, together with a ticket for CDG Express and on preferential terms, a check-in and baggage transport service. In order to maintain effective competition, the companies committed to entrusting the baggage service to an independent partner with autonomy in determining its commercial policy.

In September 2020, the FCA conditionally cleared the acquisition of the local finance company (SFIL) by the French deposit and consignment office, la Caisse des Dépôts et Consignations (CDC).

The FCA identified risks of harm to competition in the export credit sector concerning refinancing offers and confidentiality. The CDC committed not to favor its subsidiary, La Banque Postale, in the refinancing process and to maintain confidentiality provisions in the agreements entered into with commercial banks. For the application of the first commitment, ex-ante control by a representative is provided in situations of risk of foreclosure of LBP's competitors.

In December 2020, the FCA also authorized the BouyguesTelecom group to take exclusive control of Euro Information Telecom (EIT), subject to conditions. To address the risk of foreclosure on the wholesale supply market for virtual operators marketing their offers to businesses, Bouygues Telecom committed to maintain a wholesale offer equivalent to EIT's current offer at the end of the transaction.

Despite not imposing any sanctions for failure to comply with commitments in 2019, the FCA has continued to closely monitor compliance with remedies as well as their continued adequacy in light of changes in market conditions.

For example, in September 2019 or 2020, the FCA closed its ex officio proceedings reviewing Altice's compliance with its commitment to sell Completel's DSL network, obtained in 2014 when the authority cleared Altice's acquisition of SFR.

The FCA concluded that the delay in the delivery of the components of Completel's DSL network was due to the diligence of third-party operators and the performance of services over which Altice France had no control, and therefore did not constitute a breach of its commitments.

In October 2019, the FCA also decided not to renew the behavioral commitments made by Altice upon acquiring SFR in 2014—notably giving all telecom operators access to its cable network—in light of changes to market conditions.

As the five-year behavioral commitments were about to expire, the FCA considered that it was not necessary to extend the cable access commitment because other telecom operators, especially Orange, had significantly deployed their own fiber-optic networks since the merger. This non-renewal of Altice's commitments illustrates the careful monitoring by the FCA of the adequacy of behavioral commitments considering changes in market conditions.

Since 2017, the FCA has also committed to modernizing and simplifying its merger control procedures.

In line with this approach, a decree issued in April 2019 introduced several practical measures to reduce burdens on notifying parties. The decree removed the obligation to submit four hard copies of the notification files; one copy is now sufficient. The decree also reduced the amount of financial data required for the companies concerned from 93 statistical items previously down to just 12.

In addition, in October 2019, the FCA launched an online electronic notification system for certain mergers that fall under the simplified procedure. These include transactions in which the acquirer is not present in the same markets as those in which the target operates or in upstream, downstream or related markets; transactions relating to food distribution that do not lead to a change in the name of the retail stores concerned; and transactions relating to motor vehicle distribution. The FCA anticipates that approximately half of the notifications filed will be eligible for this online notification procedure.

New merger control guidelines, published by the FCA on 23 July 2020, constitute an additional step in the modernisation of merger control procedures. In the guidelines the FCA provided several indicative time frames to give greater visibility to notifying parties. It will now indicate within 10 working days of the notification whether or not the file is complete, and will also confirm within 10 working days if a transaction is eligible for the simplified procedure.

The FCA has clearly expressed its wish to adapt merger control rules to the challenges of the digital economy and has been pushing for new tools in order to tackle more effectively the transactions entered into by digital platforms and tech giants

Impact on merging parties

The merger control procedure before the FCA has been increasingly characterized by a search for greater precision in its analyses, with tailor- made solutions. The greater use of behavioral commitments and the close monitoring of their adequacy in changing market conditions are clear examples of this.

Another illustration of this quest for tailor-made solutions is the extension of the pre-notification period in recent years, with numerous exchanges with the rapporteur, substantial requests for information and the increasing use of market tests. In fact, to keep to the notification period timeline, most of the investigation is now carried out during the pre-notification phase. In this regard, the FCA has aligned to a greater extent with the practice of the European Commission.

More generally, the FCA has no hesitation in launching particularly extensive consultations with important market participants during pre-notification and investigation procedures.

For instance, in the 2018 Concept Multimedia/Axel Springer deal, which consisted of the merger of the two main online property advertising platforms (Logic-lmmo.com and SeLoger.com), the FCA conducted a broad consultation with all real estate professionals as well as an online questionnaire sent to more than 30,000 estate agencies to assess the capacity of current or potential competitors to stimulate competition.

Similarly, in the February 2020 clearance of Elsan's acquisition of Hexagone Sante Mediterranee, which concerned the acquisition of healthcare facilities, the FCA conducted a large consultation with market players and local private doctors through market tests, polls and interviews before conditionally clearing the transaction. It appears that the FCA is aiming for a higher level of granularity and depth in its data collection on relevant markets.

In 2019, the FCA also granted several derogations from the classical standstill obligation in light of exceptional circumstances, illustrating again its flexible approach. The FCA granted four derogations in mergers involving distressed targets: one in British Steel's acquisition of Ascoval in May 2019 where Ascoval was facing severe financial difficulties, and three derogations for the acquisition of AlteAd in December 2019 as part of an insolvency procedure.

More uniquely, the FCA also granted a derogation from the standstill obligation in the Ineos takeover of football club OGC Nice's decision in August 2019, its first sports-related merger control case. It was the first time the FCA has granted such a derogation on grounds not relating to the financial hardship of the target. Instead, the FCA considered that the derogation was necessary so as not to unduly limit the club's ability to recruit players and allow it to sufficiently prepare for the upcoming season.

This trend continued in 2020 where the FCA granted two derogations from standstill obligations for operations involving distressed targets, namely Buffalo Grill's acquisition of Courtepaille and in Financiere Immobilière Bordelaise's acquisition of Camaïeu.

Also, in the past year, the FCA has been increasingly using upfront buyer and fix-it-first purchaser clauses when structural remedies are entered into.

In September 2019, the authority agreed on its first-ever upfront buyer when it approved the sale of French Guianese supermarket company NDIS to SAFO, which was already operating a Carrefour supermarket in the country.

SAFO committed not to run the hypermarket acquired in the deal under a Carrefour brand and not to implement the transaction until prior approval by the FCA of the purchaser of its subsidiary, NG Kon Tia. While the European Commission routinely imposes upfront buyer clauses, it was the first time the FCA had accepted such a commitment.

In the sale of baking brand Alsa France to Dr. Oetker, the FCA cleared the acquisition subject to a fix-it commitment. Dr. Oetker committed to entering into a trademark licensing agreement for five years for the Ancel brand with the company Sainte Lucie, which the FCA approved before clearing the deal.

This trend is set to continue in 2020. The FCA has already made use of a fix-it-first commitment in the Vindemia/GBH decision of May 2020, where GBH committed to divesting seven stores to two purchasers, Make Distribution and the Tak group, which received prior approval from the FCA.

These specific types of commitments limit the risk that the parties will encounter particular difficulties—unknown to the FCA—in finding a suitable purchaser, which would make it difficult to execute the divestiture.

While this gives more certainty in the execution of the remedies, there are still potential drawbacks for parties, especially as an upfront buyer process inevitably delays the closing of the transaction. This also means that in complex transactions, parties need to carefully consider at an earlier stage the assets to be divested, and potential buyers.

During the COVID-19 pandemic, the FCA adapted its merger control procedures by inviting companies to postpone their planned mergers as well as suspending the applicable time limits in which the FCA has to render its decisions. However, this exceptional framework ended on June 24, 2020 and, since then, the FCA has returned to business as usual.

In the context of the economic crisis, the FCA also announced that it would carefully assess the transactions in 2021 to ensure that those transactions do not artificially escape control because of a low turnover achieved in 2020. In this regard, Isabelle de Silva, the head of the FCA, declared at a conference held in December 2020 that the FCA will consider whether revenues recorded by coronavirus-struck businesses in 2020 can be used for merger control thresholds or whether they do not reflect the target's true value.

In our view, this statement will need to be clarified in the light of the FCAs newly published merger guidelines. Indeed, the guidelines (§128) provide that the turnover figures must be valued at the date of the last closed financial year on the basis of the audited accounts and can only be corrected, if necessary, to take into account permanent changes in the economic reality of the company.

Nevertheless, there will remain the possibility for those transactions to be assessed under Article 22 of the EU merger regulation which—since the European Commission's recent change of approach—will allow national competition authorities to request that the European Commission examine merger transactions that do not have an EU dimension even when these mergers do not exceed the national notification thresholds.

Recent changes in priorities

Consistent with its practice in 2018, the FCA has been focusing heavily on online platforms, both in terms of anti-competitive practices and merger control. The assessment of digital tools and platforms in competition policy is one of the FCA's top priorities in 2020.

In the past year, the FCA has set out several proposals to adapt merger control to the new challenges posed by digital platforms. In particular, in its February 2020 contribution to the debate on competition policy and the challenges posed by the digital economy, the FCA observed that a number of transactions carried out by digital giants were not monitored by competition authorities because they concerned a developing innovative player, and notification thresholds were not crossed.

To address these challenges, the FCA has been advocating for a new tool that would enable the FCA to instruct companies to notify a transaction in cases where all the undertakings have a combined aggregate worldwide turnover above €150 million and the operation raises "substantial competition concerns" in the territory concerned. The FCA suggested that this intervention should only be open for a period of 12 months after the deal completes.

In addition, there is an ongoing debate before the French parliament on the creation of a list of systemic companies that would be obliged to inform the FCA of any planned mergers that are likely to affect the French market one month before these are carried out, even if the notification thresholds are not reached However, Cedric O, the French minister for the digital transition, declared that this new mechanism will not be introduced at the French level, but at the European Union level with the adoption of the Digital Market Act, which provides for such list of systemic companies.

Key enforcement trends

On August 28, 2020, the FCA blocked a transaction for the first time.The FCA vetoed Leclerc's bid to buy a hypermarket operated by Géant Casino outside the French town of Troyes after the parties failed to submit sufficient remedies to counter the creation of a duopoly in the area with Carrefour.

Until this decision, there had been no prohibition by the FCA, although there had been several cases where parties withdrew their notification during a Phase II in-depth examination. An example would be the withdrawal of the acquisition of Trapil by Pisto in July 2020, where the FCA had identified a serious risk to competition in the refined product pipeline transport and storage markets, and opened a Phase II procedure.

More generally, in 2019, a high number of transactions were abandoned by the parties before the FCAs final decision. Indeed, 31 planned transactions were withdrawn in 2019, whereas in 2018 only 13 transactions were withdrawn after their notification to the FCA. Based on the available information for 2020 on the FCAs website, four notifications were withdrawn in 2020.

In June 2020, the FCA conditionally cleared the Coopérative Dauphinoise/Terre d’Alliances deal with an unprecedented behavioral commitment. In this deal, the two agricultural cooperatives notified the FCA of their planned merger, but the FCA was concerned that the tie-up would harm competition in the market for the sale of gardening products in the local areas where the companies' activities overlapped.

As a result, the companies committed to submit for the FCAs prior approval any strategic decision, such as a change of brand name for a store located in the catchment areas where their businesses overlap, since such a decision could influence the local competitive structure.

Such a commitment—which is unheard of in the FCAs decision-making—enables the authority to monitor any future strategic decisions that might affect the competitive structure in the catchment area of the store concerned.

Recent studies and guidelines

The FCA has made several key advances in merger control in the past year. It revamped its merger control guidelines in July 2020, completely reshaping the previous version issued in 2013 in order to incorporate recent FCA decision-making, simplify merger control procedures and make the guidelines more practical.

Among the significant changes, the guidelines added a new, optional stage prior to the pre-notification phase. In this stage, companies can request the appointment of a "rapporteur" in order to anticipate and speed up the information flow and notification process—similar to case allocation requests to the European Commission.

The FCA also said it would provide a response within ten working days on the completeness of the notification file and on whether the transaction is eligible for the simplified procedure. It seems that these indicative time frames depend on a very complete and detailed pre-notification phase during which the FCA obtains all the information requested.

The new guidelines include several appendices comprising templates regarding online notification, requests for information and structural commitments.

Meanwhile, eligibility criteria for the simplified procedure have been revised, increasing the number of transactions that may fall within its scope. For instance, all operations where the combined market share of the companies involved is under 25 percent in markets consistently defined by decision-making practice are now eligible for the simplified procedure.

In May 2020, the FCA published a study on competition and e-commerce that highlighted the impact of e-commerce on distribution models with the emergence of new types of players and new consumer behaviors toward digital tools for purchases, as well as the FCA's decision-making practice in the field of e-commerce.

The study said the growth of e-commerce had led the FCA to adapt its analytical framework to assess the various competitive constraints, in particular by identifying more and more frequently relevant markets that cover both online and offline sales.

Lastly, to promote the use of behavioral remedies in practice, the FCA released a lengthy study on behavioural commitments in January 2020. The study provides an analysis of its decision-making practice in regard to behavioral commitments, some discussion on its significant use of this tool compared to other competition authorities, and a comparison with structural remedies in terms of implementation and monitoring.

Looking ahead

The FCA has clearly expressed its wish to adapt merger control rules to the challenges of the digital economy and has been pushing for new tools in order to tackle more effectively the transactions entered into by digital platforms and tech giants. It will be interesting to see if any changes to the merger control framework will be adopted in the next few years.

The importance of the pre-notification phase will continue to increase in the future, bringing French processes closer to the typical procedure before the European Commission. Indeed, the importance of the formal phase from notification to the FCA decision is diminishing in comparison to the pre-notification phase, and the FCA seems inclined to conduct an in-depth analysis from the start of the whole process.

Companies and advisers should therefore approach the informal phase more strategically by being more meticulous and transparent in their analysis of the proposed transaction.

Another current trend is the increased judicial review of merger control decisions, measured by the increasing number of challenges against FCA decisions before the French Supreme Court, the Conseil d'Etat.

Indeed, three FCA authorization decisions rendered in 2019 were subject to a challenge. Since the beginning of 2020, three additional FCA authorization decisions have already been challenged before the Conseil d'Etat, including one emergency procedure aimed at suspending the completion of a merger after FCA approval, which was rejected.

While it is not impossible to call into question the FCAs approval of the merger before the Conseil d'Etat, a third party should first attempt to influence the review process by proactively intervening during the FCA's examination of the potential deal.

Number of filings approved by the French Competition Authority (PDF)

Number of filings approved by the French Competition Authority (PDF)

Number of filings submitted to the French Competition Authority (PDF)

Number of filings submitted to the French Competition Authority (PDF)

THE INSIDE TRACK

What should a prospective client consider when contemplating a complex, multi-jurisdictional transaction?

Any client confronted with a complex multijurisdictional transaction should, firstly, not underestimate how strenuous the process will be for its organisation. The process is long, often frustrating and unpredictable, and always intense, especially in the phase where multiple authorities send rapid-fire requests for information with tied deadlines.

Merger control aspects, including potential remedies, must be prepared well in advance to be able to change course quickly if need be. A legal partner with a global reach, able to deal with the trans-national aspects of the transaction efficiently, is a must.

In your experience, what makes a difference in obtaining clearance quickly?

Obtaining clearance quickly requires anticipation. This means gathering relevant information such as economic data well ahead of signing if possible.

Data gathering and shaping often consumes a lot of time and has to be started as early as possible, otherwise it risks delaying pre-notification discussions. Remedies anticipation is also key: if the deal is likely to require remedies, they should be framed very early on, well ahead of the first contact with the authorities.

Finally, in a complex deal requiring many filings, the sequencing of such filings is key and should be planned early on.

What merger control issues did you observe in the past year that surprised you?

The most surprising trend is the high number of transactions that have been abandoned. This is mainly due to the fact that parties now notify the planned deal earlier than in the past, before having carefully analysed all the competition issues, and that the pre-notification stage enables the parties to identify insurmountable competitive concerns before any formal decision is reached.

The past year was also marked by the increasing number of challenges against FCA decisions by interested parties, including through emergency suspensive procedures. Clients and their advisors thus need to prepare for another obstacle to the closing of the transaction, even after the FCA has given clearance.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP