1. Why Repos are important for the Islamic finance industry

Islamic finance is a full-fledged financial system, including well-established banking, capital markets, money markets and insurance products and practices. Islamic finance is governed by principles of Shari'ah, which in practice provides an alternative or complementary ethical investment approach promoting risk and reward sharing, social justice and the benefit to wider society, profit generation from legitimate assets and investments, and seeks to avoid uncertainty and speculation.

The Islamic finance industry, much like the broader finance market, has spent much of the past three years weathering the global economic turmoil and market volatility, which has affected Islamic finance institutions' liquidity and has proven the importance of the ability to access short-term funding on a secure, low-cost and low-risk basis. A Shari'ah-compliant repurchase transaction, a Repo, provides efficient access to short-term funding, as well as giving Islamic financial institutions and corporates the ability to utilize their sukuk portfolios and other Shari'ah-compliant instruments in their liquidity management operations.

2. What is a Repo?

A conventional Repo is a type of short-term secured borrowing in which one party (the Seller) sells securities (usually highly liquid bonds) to another party (the Buyer) at an agreed price (the Purchase Price). This transfer is often on a full title basis, with the Buyer becoming the owner of the securities. The Seller commits on the purchase date to repurchase equivalent securities from the Buyer at a different price (the Repurchase Price) at a future date (subject to the potential for substitution of securities and early termination in certain circumstances). The term “Repo" is a generic name for both repurchase transactions and buy/sell-back transactions.1

In a Repo, the Repurchase Price will typically be higher than the sale price. The difference or "price differential" will likely be the equivalent of interest on the cash received by the Seller from the purchase date to the repurchase date, although this amount may be paid periodically during the trade term as well. The Seller of the securities therefore obtains funding, usually at a lower cost than a bank loan, as they have provided security in exchange for the funding. The Buyer makes a commercial return on any surplus cash it is holding, being protected against default by the purchased securities, which function as a form of collateral, and may make a commercial return on usage of the purchased securities themselves.

Repos make up an important part of conventional financial markets, and they are a mechanism that not only allows holders of securities a cheaper form of funding but Repos have the wider economic benefit of increasing liquidity of the securities in a market and their use allows market makers to make two-way prices in respect of the securities. The existence of a liquid Repo market may also reduce securities issuers' borrowing costs under the securities themselves. In June 2022, according to a survey by the International Capital Market Association, the size of the European Repo market was estimated to be approximately of €9,680.3 billion2, and the size of US Repo market for the same period was estimated to be approximately US$2,480 billion.3 As of September 2021, the total notional value of derivatives contracts held by US commercial banks was estimated to be approximately US$230 trillion according to the Bank for International Settlements.4 Thus, while the Repo market is much smaller, its vital role as a source of short-term funding and liquidity for the financial system should not be underestimated.

3. How are conventional Repos documented?

There is not any documentary requirement for a conventional Repo, and parties may enter into such a Repo verbally should they wish. To the extent that a conventional Repo is to be documented, this will usually be under a repurchase agreement in the form of an umbrella master agreement. Repurchase agreements in the conventional Repo market are often in the form of the Global Master Repurchase Agreement published by the Securities Industry and Financial Markets Association and the International Capital Market Association, with the most recent version from 2011 (the GMRA).

The GMRA consists of a pre-printed master agreement that contains standard provisions, which are generic to the market in respect of conventional Repos, and Annex I, which lists specific elections that need to be made by the parties to operationalize the agreement (e.g., fixing minimum delivery periods) while also providing a means to record supplemental terms and conditions. The specific commercial terms of each transaction are documented in a confirmation, a model template for which is provided in Annex II of the GMRA.5 The GMRA can be further supplemented with transaction-specific provisions. Annexes are published for particular types of transactions (e.g., agency transactions, bill transactions and jurisdiction-specific transactions).

4. Can a conventional Repo be entered into as an Islamic finance transaction?

While in the conventional financial market Repos are commonly used as a means of borrowing and lending money, in Islamic finance, conventional Repos are generally considered to be haram (forbidden). There are a number of reasons for this, for example6:

- A conventional Repo involves the sale and purchase of a security for a pre-determined amount of money at a pre-determined future date, which is considered to be a form of riba (interest or usury). Riba is prohibited in Islamic finance, as it is considered to be exploitative and unfair. The prohibition of riba is based on the belief that money should not be used as a commodity to generate profit without any real underlying economic activity. In the case of a conventional Repo, the profit generated by the transaction is solely based on the difference in the price at which the securities are purchased and repurchased, and there is no underlying economic activity taking place

- Furthermore, a conventional Repo could be considered to be a form of gharar. Gharar is the concept of excessive uncertainty or risk in a financial transaction. Gharar can take many forms, such as a lack of information about the underlying securities in a financial contract, or a lack of clarity about the terms of the contract. In a conventional Repo transaction, the short-term speculation on the value of the security that is being bought and sold could be considered as gharar. Additionally, the use of leverage and margin in conventional Repos also creates a higher degree of risk and uncertainty, which could also be considered gharar in the eyes of Islamic scholars.

5. How may Repos be structured in the Islamic market?

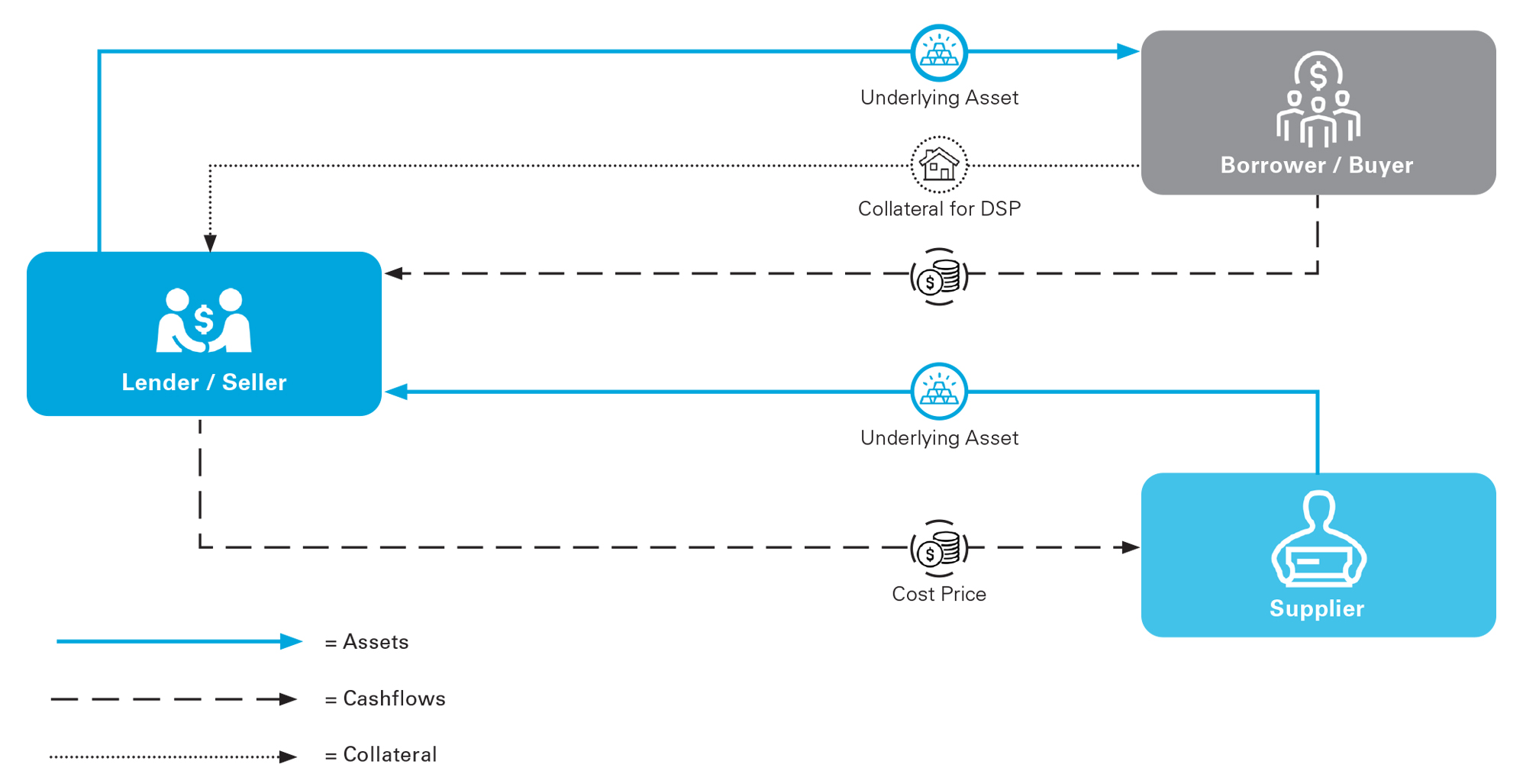

A Repo in Islamic finance is typically structured using a contract called a murabaha—a Shari'ah-compliant alternative of loans—that has been used for both secured and unsecured lending in the Islamic finance industry for many years. Murabaha is a cost-plus financing structure where the financier (the Seller) agrees to purchase Shari'ah-compliant assets (typically metals traded on a metal exchange, other than gold and silver) from a third-party supplier (typically a commodity broker) paid at cost price on a spot delivery and spot payment basis, and immediately sells such assets to the financed party (the Buyer) on immediate delivery and deferred payment terms, at a marked-up price (at cost plus profit). In a Shari'ah-compliant financing transaction, the financed party then immediately on-sells such assets at cost price to a pre-determined third-party purchaser (typically another commodity broker). As illustrated in the diagram below, under an Islamic Repo structured as a murabaha contract, the Seller purchases the security from a third party for a spot delivery and spot payment immediately, and then sells it to the Buyer at a marked-up price, with the profit margin disclosed to the Buyer.

View the full image: Repos in Islamic Finance (PDF)

View the full image: Repos in Islamic Finance (PDF)

The wide-spread use of a murabaha contract for an Islamic Repo, and the perceived need for a unified and standardized Repo market within the Islamic financial system, prompted the International Islamic Financial Market (IIFM) to publish the form of Master Collateralized Murabaha Agreement (MCMA) for an Islamic Repo7 in 2014.

The advantage of the MCMA includes that, like the GMRA, it is a master agreement that contains standard provisions that are generic to the Islamic Repo market, and each murabaha contract entered into pursuant to the MCMA and in the form set out in the MCMA will constitute a collateralized murabaha transaction. The MCMA thus provides a mechanism for access to liquidity on a collateralized basis (based on the Shari'ah principle of Ar'Rahn8) utilized for this purpose as collateral sukuk and other Islamic securities, including shares of Islamic financial institutions and the shares of companies whose original activities are Shari'ah-compliant. Accordingly, Islamic Repo transactions based on conventional (non-Shari'ah-compliant) securities as collateral will not be permissible. Note that under the MCMA, there is a distinction between the commodities or goods that are sold by the Seller to the Buyer and the commodities or goods that are used as collateral. In respect of the former, the commodities or goods are sold to the Buyer on a deferred payment basis9, whereas a security interest is created over collateral that is posted. In respect of this collateral, it is permissible for the Buyer (charger) to use the collateral with the consent of the Seller (secured party), although this is not the case for the Seller (secured party) even if the Buyer (charger) consents.10

While the terms of the MCMA are approved by the IIFM Shari'ah Board, such approval does not extend to underlying murabaha transactions nor any amendments to the MCMA. Therefore, parties intending to use the MCMA may also need to receive independent approvals from their respective Shari'ah supervisory boards. To aid market participants in their Shari'ah review, the IIFM Shari'ah Board published the Key Features and Scope of the IIFM Shari'ah Board Review and Guidelines of the IIFM Collateralized Murabahah Agreement which, among other requirements (such as the prohibition on speculation and interest and the requirement to use Shari'ah-compliant collateral), requires the collateralized murabaha transaction to be entered into only for liquidity management purposes.

Although the MCMA has been approved by the central banks of Malaysia, Bahrain and the United Arab Emirates, the usage of the MCMA has mostly been limited to the United Arab Emirates11.

6. Any drafting considerations?

When drafting a Repo as a murabaha contract, the following key considerations should be kept in mind:

- The underlying securities must be selected among Shari'ah-compliant instruments (sukuk, trust certificates and other Islamic securities, including Shari'ah-compliant equities (e.g., shares of Islamic financial institutions and companies whose original activities are Shari'ah-compliant))

- The terms of the Repo should be clearly stated, including the Repurchase Price, the date of repurchase, and any penalties for late or non-repurchase

- The contract should clearly state the rights and obligations of both parties, including the rights and obligations of the Seller with respect to the securities being sold and the rights and obligations of the Buyer with respect to the repurchase of the securities

- The contract should include a description of the securities being sold, including any warranties or guarantees, and should specify the condition of the securities at the time of sale and at the time of repurchase

- The contract should comply with the local laws and regulations of the country where the contract is being executed, as there may be some additional local law nuances. Some examples of local laws and regulations that need to be kept in mind are:

- The local securities laws, tax laws, and laws related to the ownership and transfer of assets which may have an impact on the Repo

- The applicable central bank regulations, as these may vary across different jurisdictions with respect to rules and regulations related to Islamic finance and Repos as a murabaha contracts specifically and

- The requirement to comply with any applicable accounting standards, for example, the accounting standards set by the Accounting and Auditing Organization for Islamic Financial Institutions

- If the parties to the contract elect to appoint an agent to perform the murabaha trades on their behalves, this must be clearly stated in the contract and, if an MCMA is used, the parties may elect to enter into a separate IIFM Master Agency Agreement to complement the MCMA with respect to such agency services

- The contract should be written in clear, easily understandable language, and should be reviewed and approved by legal counsel before being executed

- The contract should clearly state who is responsible for any risk or loss associated with the securities being sold, particularly in case of default. For example, in the MCMA, on the occurrence of an event of default with respect to the Buyer, the Seller may deliver an acceleration notice (Acceleration Notice) to the Buyer declaring all or any part of the deferred Purchase Price and any other outstanding amounts to be immediately payable to it or payable on demand. The Seller following the delivery of the Acceleration Notice may then exercise its rights of enforcement in respect of the collateral without notice to the Buyer, including selling all or any of the collateral with any excess proceeds to be payable to the Buyer

- The contract should clearly state who will be responsible for collateral management (i.e., one of the parties to the contract or an independent third-party may act as the custodian)

- The contract should include a provision for dispute resolution in case of any disagreement. In this regard, it should be noted that arbitration is a preferred form of dispute resolution, particularly in international Shari'ah-compliant transactions, as it is relatively easier to enforce an arbitral award in reliance on the Convention on the Recognition and Enforcement of Foreign Arbitral Awards (New York Convention)

- Following the finding of the court in the case of The Investment Dar Company v Blom Developments Bank12 certain key representations should be included in the contract such as representation on:

- The underlying assets: The parties should clearly state the type and value of the underlying assets being used as collateral

- The ownership of the assets: The parties should provide a representation on the ownership of the assets and the absence of any prior liens or encumbrances on the assets

- The legal and Shari'ah compliance of the contract: The parties should represent that the transaction is legally valid and in compliance with Shari'ah principles

- The use of proceeds: The parties should represent that the proceeds of the transaction will be used only for permissible purposes under Shari'ah law and

- The absence of speculative intent: The parties should represent that the transaction is not entered into with speculative intent, but rather with the intention of generating a profit based on the underlying assets

1 The main distinction between a repurchase transaction and a buy/sell back transaction relates to the payment of income in respect of the underlying security. In the case of a repurchase transaction there is immediate payment of any income whereas in a buy/sell back transaction the repurchase price to be paid on the repurchase date is reduced by the amount of the income payment plus interest

2 European Repo Market Survey (Number 43 – Conducted June 2022) – International Capital Market Association (October 2022)

3 US Repo Statistics - SIFMA - US Repo Statistics - SIFMA

4 https://www.bis.org/statistics/otcder/dt1920a.htm

5 What is the GMRA? » ICMA (icmagroup.org)

6 Dar, H. A. (2008). Islamic Financial Services: An Overview of the Global Market. John Wiley & Sons

7 Master Collateralized Murabaha Agreement (MCMA) – International Islamic Financial Market

8 This is a sales contract where the seller declares the cost of the item and the profit margin added to it. The buyer agrees to purchase the item at the marked up price. The buyer and the seller agree on the cost of the item and the profit margin, and the buyer then pays the marked-up price in instalments

9 Master Collateralized Murabahah Agreement Operational Guidance Memorandum

10 Master Collateralized Murabahah Agreement

11 Liquidity Stress Highlights Importance of Effective Sharia-Compliant Repo Market

12 S.A.L [2009] All ER (D) 145

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP