In nine months, the Trump administration's policy of energy dominance has reshaped the competitive landscape for the mining & metals sector in the US and beyond. American policy has pivoted from a focus on tax credits for critical minerals projects and preferences built around free trade agreements to a focus on expanding domestic mined and refined supply. Among other things, US government-backed financing aligned to geopolitical priorities is to be used to secure supply in the US and abroad.

While projects can take years, even decades, to move from exploration to production, the administration's supportive approach to the industry shows promise in moving capital toward miners and processors. But partial shutdowns during the US government budget impasse are pushing out the window in which projects can secure permissions and financing. Even if the shutdown is short-lived, mining projects need to plan for a window that may shut within 12 to 24 months, after which renewed political uncertainty could stymie further progress. If a project isn't shovel-ready, miners and processors must get it ready as fast as possible, before this window closes.

The administration's approach can be divided into three buckets. First, the use of administrative interventions such as deregulation, accelerated permitting processes and the executive authority invested in the National Energy Dominance Council to direct all-of-government efforts to accelerate project development; second, the use of existing funding authorities and offtake powers delegated to the Department of Defense and other federal bodies to finance and support projects deemed critical to national security; and third, the application of tariffs and negotiation of investment agreements linked to geopolitical and diplomatic initiatives, namely the critical minerals investment agreement with the Ukrainian government, a peace deal between the governments of the Democratic Republic of the Congo (DRC) and Rwanda, a memorandum of cooperation regarding critical minerals with Saudi Arabia, and an agreement to co-invest into critical minerals value chains with the UAE.

Taken together, the current policy mix is a more supportive environment for investment into the mining & metals value chain in the US or in partnership with US allies elsewhere. The One Big Beautiful Bill Act (OBBBA) is supportive in the near-term, allowing companies building manufacturing projects before 2029 to deduct 100 percent of the eligible property's cost in its first year of operations as long as it's in service before January 1, 2031. On paper, this should support greenfield processing, refining and smelting projects in the US. However, potential constraints on labor, a more inflationary economic environment, and uncertainty over investment, the cost of capital and economic growth may challenge projects, especially those dependent on private sector demand instead of publicly backed offtake support.

Racing for critical mineral dominance

Seeking to onshore the extraction and/or processing of those critical minerals vital to national security, manufacturing and tech giants undertaking huge AI-driven investment into datacenters and associated utilities, the administration has launched a dramatic reform effort to accelerate permitting. Begun with the Unleashing American Energy executive order (EO) on January 20, 2025 and continued with additional EOs since, the administration's highest priority has been reducing the immensely long, arduous lead times to receive permission to build mines. Additionally, the administration has also designated copper a critical mineral, extending access to policy support.

The National Energy Dominance Council formed in February 2025, a cabinet-level coordinating body chaired by the Secretary of the Interior, is explicitly tasked with improving permitting and accelerating projects deemed vital for national security. Acting on its mandate, the Council's deliberations and parallel action from the White House rescinded existing regulatory burdens imposed by the National Environmental Protection Act (NEPA) on June 30, 2025. The EO delegates more authority to each department to narrowly apply the law for NEPA reviews, impose review page limits, and eases the process of establishing exclusions from the review process. These regulatory rollbacks potentially come at the expense of environmental outcomes, a legitimate cause for concern that poses legal risks after the Supreme Court's overturning of the Chevron Deference doctrine.

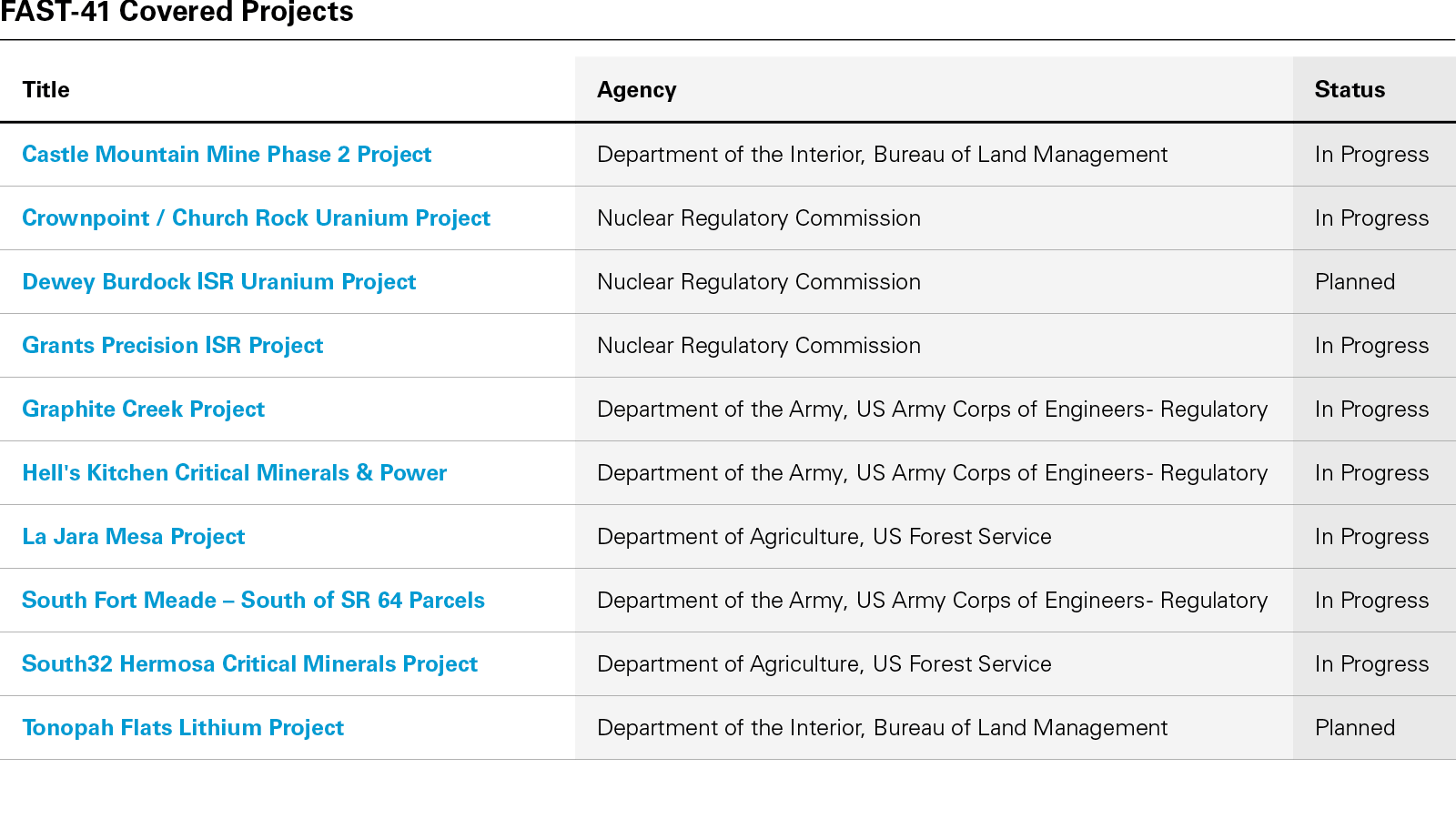

Existing projects stuck in limbo have benefited from designation under FAST-41, a federal designation for projects to accelerate decisions on outstanding permit applications. The largest project among them—the Rio Tinto–led Resolution Copper in Arizona—received an expedited environmental impact statement and decision from the US Forest Service in June. Resolution Copper could provide up to 400,000 tons of copper production, equivalent to approximately 25 percent of US demand and enough to significantly reduce dependence on refined copper imports as smelting and refining capacity comes online. Resolution Copper still faces a legal injunction on a necessary land swap to build the mine, but the federal government continues to support a faster development timeline.

View full image: FAST-41 Covered Projects (PDF)

View full image: FAST-41 Covered Projects (PDF)

Please see the list of the FAST-41 Transparency Projects here.

With or without FAST-41 status, copper, rare earths, uranium and gold projects are the likeliest to benefit most in the near term. Persistent fears of large copper concentrates deficits after 2030 dovetail with greater demand growth linked to electrification. China's export controls on light and heavy rare earths have left defense and automotive manufacturers exposed to supply chain concentration. A significant expansion of domestic uranium mining and processing similarly would support the administration's efforts to kickstart a nuclear power renaissance.

Designation for faster review doesn't guarantee success. The administration is blocking the development of Northern Dynasty's Pebble Mine project in Bristol Bay, Alaska, one of the world's largest undeveloped gold and copper prospects, fearing environmental impacts on the Bay's salmon fisheries. As officials begin reviewing projects with significant environmental impacts—Orla Mining's Dark Star Mine near Elko, Nevada is the first open-pit mine receiving an accelerated review—market participants will learn more about the relative importance assigned to local concerns.

Despite some uncertainty about degree, there is a definitive change and expansion of what's considered a permissible tradeoff between development, environmental concerns and national needs. Newfound support for research, exploration and international leadership for offshore deep sea mining projects highlights this shift, though the lack of an established regulatory framework remains troublesome.

Show me the money

Alongside aggressive coordination efforts fast-tracking permissions, policymakers are expanding support for strategically important projects. The Department of Energy's loan program office is having its remit expanded to include traditional fossil fuel infrastructure, while backing away from its past mandate to lend to projects aiding emissions reduction like battery gigafactories requiring lithium and other metals offtakes. Make More in America (MMIA) supports a broad range of U.S. manufacturing and production projects that strengthen American competitiveness. While EXIM financing has included projects in the critical minerals sector, with environmental statements posted for mining projects, MMIA is not limited to mining. It is important to note that MMIA applies only to domestic U.S. projects. Separately, EXIM provides international export financing through its traditional programs under a distinct statutory framework. Additional lending authorities through the Office of Strategic Capital at the Department of War have become a vehicle to secure critical minerals value chains.

China accounts for 70% of global rare earth ore extraction and 90% of rare earth ore processing.

Source: The Oxford Institute for Energy Studies

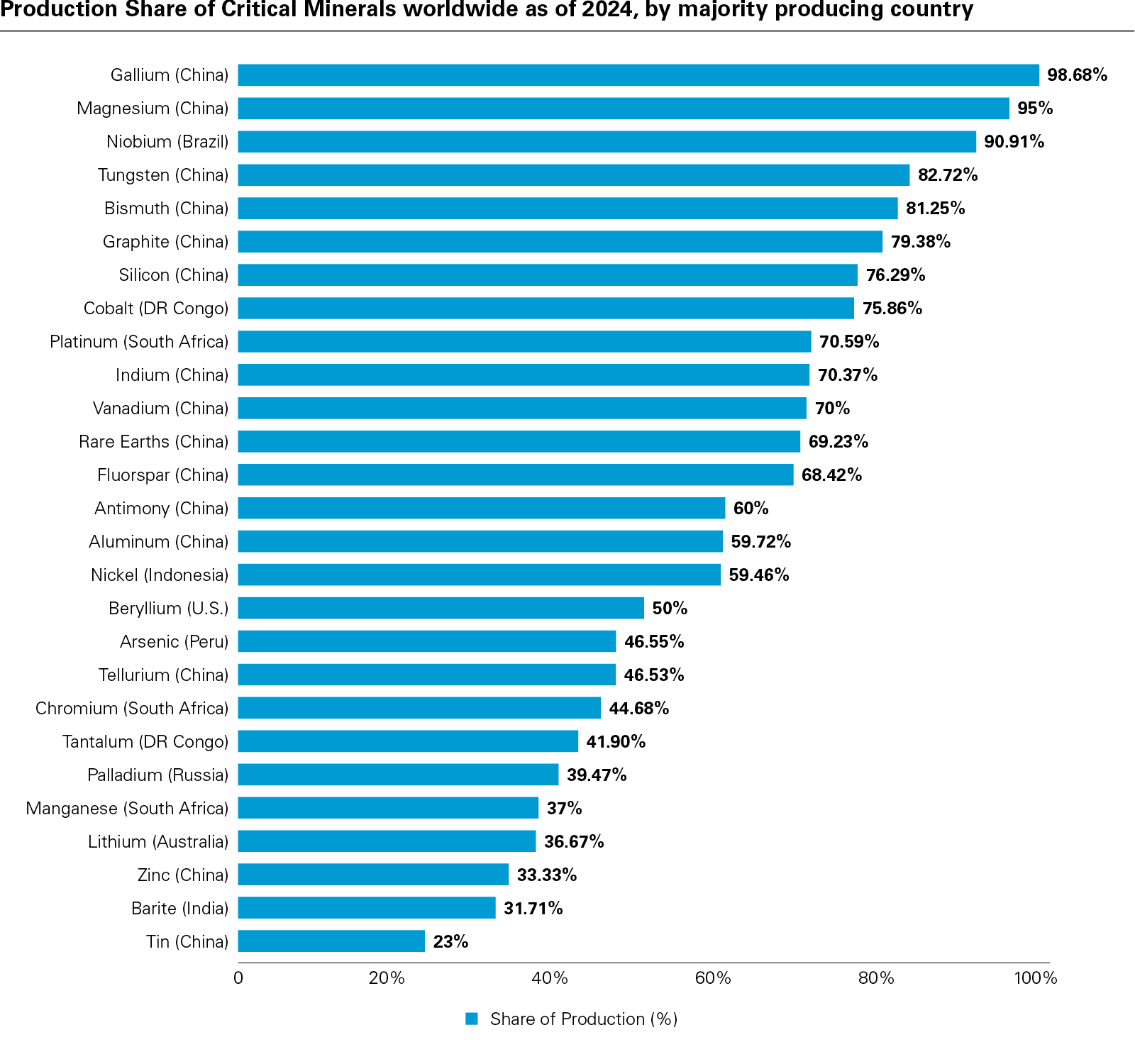

The concentration of rare earths mining and refining in China poses significant national security risks exposed by China's implementation of export license controls on a widening array of rare earths and battery metals since 2023. In the spring, western OEMs and defense manufacturers panicked over any sudden halt to trade flows from a lack of large inventories. But breaking into the mining and processing of rare earths has been notoriously difficult because of the low price points at which Chinese producers can operate and their advantages from existing economies of scale.

By considering equity stakes and supporting profitability through price interventions, the administration is prioritizing onshoring production of key inputs, particularly for existing brownfield assets. Current policy also aims to leverage the International Development Finance Corporation (DFC).

View full image: Production Share of Critical Minerals worldwide as of 2024, by majority producing country (PDF)

View full image: Production Share of Critical Minerals worldwide as of 2024, by majority producing country (PDF)

By taking on equity and guaranteeing profitability through price interventions, the administration is prioritizing onshoring production of key inputs where possible with greater influence over investment decisions. Taking equity positions in exchange for financial support has become a vote of confidence for investors and an implicit promise of support when market conditions deteriorate. DFC has in place commitments to support the Lobito Corridor, a rail route linking the Angolan port to the Copperbelt in the DRC and Zambia. In September, the agency announced a US$75 million equity commitment to seed the US-Ukraine Reconstruction Investment Fund that will provide seed capital to jumpstart the fund's investment in critical minerals, hydrocarbons and related infrastructure in Ukraine. Other initiatives to combine the DFC's efforts with private funding, in some cases, and sovereign wealth, in others, may be explored with a particular focus on investments in critical minerals. A significant increase in the DFC's investment capacity is also under consideration in a congressional reauthorization hoping to take place in November 2025. But with many staff of both DFC and EXIM currently furloughed and both looking for congressional reauthorization in the coming months, a speedy resolution to the budget impasse may be critical for them to maintain momentum to finance mining projects during the window described above.

Carrots and sticks

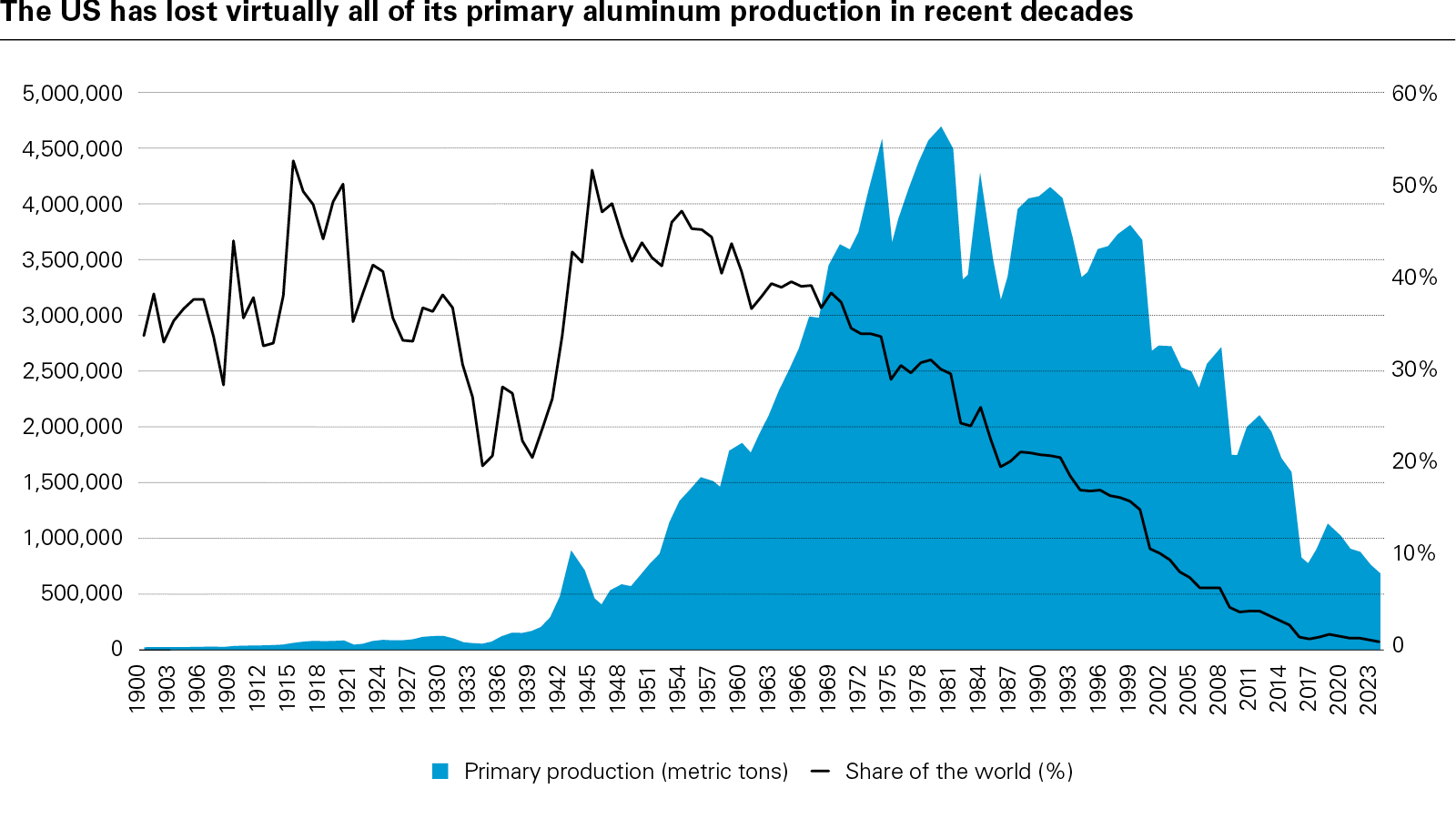

Trade policy has expanded into an instrument organizing industrial policy through a broad array of carrots and sticks. Since 2018, tariffs have been featured as a tool to protect domestic steel and aluminum production under Section 232 of the Trade Expansion Act. The Trump administration expanded the use of Section 232 in 2025, increasing the steel tariffs from 25 percent to 50 percent, and the aluminum tariffs from 10 percent to 50 percent. On August 1, 2025, 50 percent of Section 232 tariffs were also levied on imports of semi-refined copper products, a move meant to foster more investment into domestic smelting and refining. Officials are still considering a 15 to 30 percent general copper import tariff for 2027 that will be reviewed next year. A similar investigation is ongoing for a broad range of processed critical minerals and derivative products, including rare earths and uranium, with a report and policy recommendations scheduled for delivery to the President in October.

View full image: The US has lost virtually all of its primary aluminum production in recent decades (PDF)

View full image: The US has lost virtually all of its primary aluminum production in recent decades (PDF)

Each shift in the tariff regime alters domestic project economics—higher import costs can offset higher construction, labor and operational costs for US projects. But their application by executive order also creates the potential for negotiated exemptions with foreign partners in line with diplomatic and geopolitical initiatives. Conversely, the Republican majorities in Congress's unwillingness so far to challenge the Trump administration's tariffs in regulating trade or establishing these priorities beyond budget allocations can create longer-term risks from shifts in policy. However, policies supporting critical minerals value chains are largely bipartisan, evidenced by the administration's expansion of financings begun during the Biden administration.

Two major diplomatic initiatives have produced intergovernmental framework agreements for mining and metals projects—attempts to broker peace and post-war stability in Ukraine and the DRC. Responding to Ukrainian concerns that the US might disengage from military and security support, the US government negotiated the creation of a joint fund for exploration and early-stage development. All projects' equity will be split between the two governments. Since much of Ukraine's critical mineral wealth currently sits in occupied territory, the agreement provides a longer-term basis for US involvement.

More pressing for metals markets, the Trump administration brokered the Washington Accord between the governments of the DRC and Rwanda, which risked threatening mining operations. While the agreement only begins implementation in October, and did not include M23, which continues to fight against the Congolese government in Kinshasa, the DFC has begun underwriting exploration agreements in the region. To date, there is no systematic process for US firms to invest, and a durable peace deal has yet to be reached.

Finally, the administration has brokered a memorandum of cooperation with the Saudi government to collaborate securing critical minerals and an agreement with the UAE to co-invest into relevant projects. These agreements build on both countries' existing critical minerals strategies acquiring strategic stakes in mining businesses and projects internationally. The administration's approach has therefore fused security and geopolitical interests with critical minerals policy domestically, and abroad to secure investment and supply. These efforts can also create headwinds for US firms and opportunities for miners based in Europe. Tensions between the governments of Greenland and Denmark with Washington over talk of incorporating Greenland into the United States opened the door to more agreements with European companies. The unintended consequences of transactional minerals diplomacy can create opportunities in Europe and elsewhere too.

Macro-economic road bumps

Miners and investors attempting to capitalize on these shifts in policy face demand uncertainty and structural constraints that will likely elevate project costs. The repeal of most tax credit provisions from the Inflation Reduction Act in the OBBB creates a headwind for the uptake of electric vehicles on the US market. Coupled with the slowdown in federal permissions for clean energy and battery storage, the demand outlook for domestic lithium projects faces uncertainty. Among the major US automakers, Ford is the only company committing to aggressive EV production targets and investment timelines.

More broadly, current policies create risks of significant increases in the cost base for projects. A more restrictive immigration policy has begun to pose a challenge for the construction sector. Projects requiring significant infrastructure investment and development will likely cost more as a result. But labor shortages are most pronounced for more senior expertise because new mines haven't been developed at scale in the US for a generation. Tariffs and the lack of a large domestic industrial base for mining & metals kits pose additional cost pressures. In the years ahead, electricity will also become a cost pressure point driven by rapidly growing demands on power grids, for AI data centers, and balancing supply between baseload, renewables and batteries.

Gold’s performance is strongest during periods of high inflation or U.S. dollar weakness — rising an average of 15% in years when inflation exceeds 3%.

Source: CFA Institute, 2024

Finally, greater uncertainty about future economic growth may challenge the economics of some proposed mines. For instance, copper prices and demand correlate strongly to GDP growth, a relationship strengthening from electrification. But the present policy mix creates headwinds for growth, even as it encourages domestic investment into mining & metals. By contrast, the demand for gold often correlates to uncertainty, inflation and the value of the US dollar, which has depreciated against other major currencies at near historic levels for the past 50 years.

These challenges will not stop investment into the sector, nor will they necessarily last. Miners like Ivanhoe Electric, which concluded its preliminary feasibility study for the Santa Cruz copper project in Arizona in June, can lock in the benefit of more accommodative policy. But the current policy environment creates a market landscape with two tiers. Miners chiefly serving private sector demand and making use of expedited permitting alone face greater risks than miners receiving financial support from the US government. Both groups enjoy an accommodative policy environment, but the latter also enjoys financial support that may be unavailable in commercial markets.

This article is written and provided on behalf of White & Case LLP and not on behalf of any agency or other person or entity.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP