European leveraged finance: From survive to thrive

What's inside

European leveraged finance markets rebounded in the past 12 months, driven by enthusiastic refinancing activity and a resurgent M&A marketplace, setting the stage for a healthy year ahead

Foreword

European leveraged finance markets look remarkably healthy as we enter 2022. This may come as a surprise, after 12 months of economic volatility underpinned by everything from a new COVID-19 variant to growing inflationary pressures. What does this mean for the months ahead?

The start of the new year is full of positives in the European leveraged finance market. There has been a clear shift from survival to growth strategies among lenders and borrowers, setting the stage for significant activity in almost all sectors.

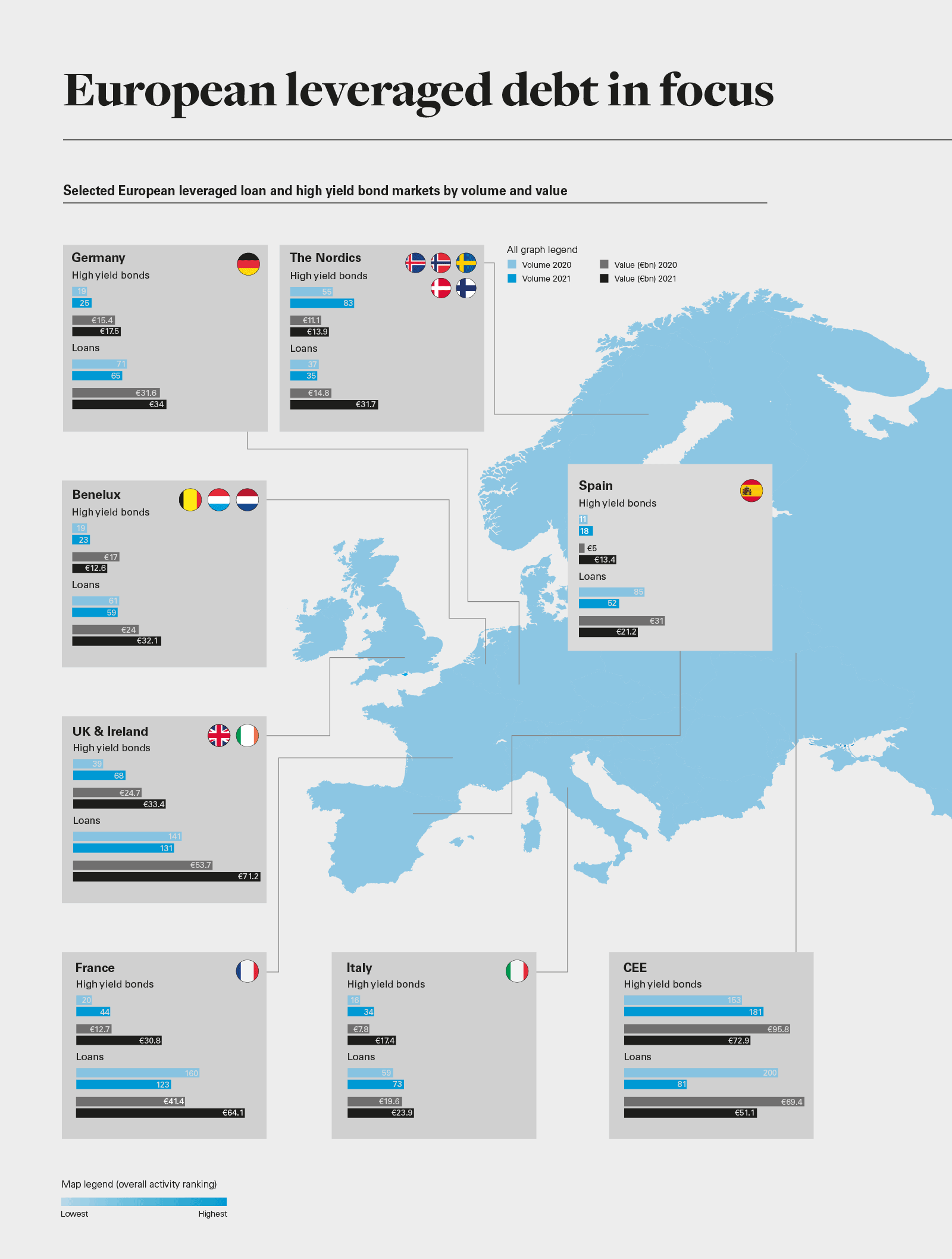

The numbers paint a clear picture. European leveraged loan issuance climbed more than 25% in 2021, year-on-year. High yield bond markets in the region were even more enthusiastic, with issuance for the year up 47% on 2020's total.

Ongoing government support in the EU and the UK helped companies that might otherwise have fallen victim to the pandemic stay afloat. Low interest rates and pricing sparked a wave of refinancing. CLO activity—most of which was intended for refinancing and resets—pushed new CLO issuance up by 75% year-on-year.

A bottleneck of demand as well as significant private equity dry powder also brought a flood of new deal money into the market. Companies that were once hesitant to sell encountered enthusiastic buyers aggressively looking for targets. Buyers, meanwhile, found themselves in a better position to judge whether a potential target was likely to struggle or grow in 2022 and beyond. Lenders reaped the benefits, with high deal volume in which to participate. At the same time, unlike many other industries, European direct lending funds avoided any significant downturn in deployment and deal activity due to COVID-19. According to data from Debtwire Par, direct lending issuance in the region reached €36.2 billion in 2021, surpassing 2020's full-year total of €21.4 billion. This provided a liquid and competitive market for finance products.

Possibilities and pitfalls

Set against this positive backdrop, does the future look entirely bright for leveraged finance? Not necessarily—some challenges remain, and each may have an impact on European issuance.

For example, climbing COVID-19 case numbers driven by the Omicron variant may convince some corporates to hold on to their reserves. Any resulting new lockdowns or restrictions could also be the final straw for businesses that have already struggled during the pandemic.

Inflation and attendant interest rate rises are also likely to influence potential borrowing decisions in the coming months. The UK got the ball rolling with its first interest rate rise in three years in December 2021, and the EU may follow suit in 2022—despite claims to the contrary by the European Central Bank.

Any rise in the cost of debt will affect M&A and buyout activity, as well as financing. Some may pause while others—from corporates in good financial shape to PE firms with money to spend—may decide to invest in a post-COVID-19 future. Either way, M&A and buyout deals in the pipeline already suggest that issuance will remain healthy in the first half of the year at least.

And, finally, environmental, social and corporate governance criteria will be on the menu for every European business. New benchmarks due in 2022—from the EU's Sustainable Finance Disclosure Regulation to the European Leveraged Finance Association's updated Sustainability Linked Loan Principles—are already making lenders and borrowers sit up and take notice.

All this activity means the stage is set for companies hoping to thrive rather than simply survive. Lenders chasing higher-yield opportunities will be on the hunt for new investments, and borrowers can be expected to provide lenders with a healthy volume of demand for debt financing in 2022.

From survive to thrive: European leveraged finance looks to the future

European leveraged loan issuance was up by more than a quarter, year-on-year, to €289.7 billion in 2021

High yield issuance reached €148 billion in 2021, up 47% on 2020 (year-on-year)

Refinancing accounted for approximately half of overall leveraged loan and high yield bond issuance for the year

Both M&A and buyout activity saw double-digit year-on-year rises in deal-related issuance

New European collateralised loan obligation (CLO) issuance in Europe is up 75% year-on-year, reaching €38.5 billion in 2021

CLO issuance intended for refinancing and resets came in at a record €57.5 billion for the year

By July 2021, 34% of the EU's total assets under management was compliant with the region's new Sustainable Finance Disclosure Regulation (SFDR), and this is expected to climb to more than 50% in 2022

From recurring revenue to sticky customers: The trends driving tech sector issuance

Leverage loan technology and computer-related issuance in Western and Southern Europe almost doubled from annual pre-pandemic levels to €19.9 billion by the end of 2021

Technology and computer-related high yield bond issuance in the region hit an all-time high of €7.3 billion by the end of 2021

Start-up debt issuance in Europe had already reached a record annual total before the end of Q3 2021

A flurry of activity saw year-on-year leveraged finance issuance in Europe hit new heights in 2021. Can this pace be maintained in the months ahead? Based on pipeline activity and investor appetite for growth, the answer seems to be: Yes.

Supply chain risks are going to be of increasing concern for lenders

Inflation and interest rate rises may influence deals, even if they do not shift the market

Private equity (PE) is still on a spending spree that will influence debt market decisions

Lenders searching for yield will finance riskier credits on the right terms

Terms and documentation will continue to be influenced by credit quality, sector and rating

It was a year of rebounds in 2021, from the early hike in refinancing activity to the subsequent surge in M&A and buyout deals, as well as frenetic activity in the PE space, all of which contributed to a noteworthy uptick in leveraged loan, high yield bond and direct lending issuance.

The drivers underpinning this activity—from the deep pool of credit in the market to investors chasing higher-yield deals—continue to influence borrowing and lending decisions, including the changing levels of acceptable credit risk to the terms and documentation being put on the table.

What does this mean for borrowers and lenders for the next 12 months? Here are five key trends that will drive activity in the market in 2022.

A key component of 2022 lender due diligence will be assessing supply chain risk and its potential impact on credit quality, in the same way that lenders scrutinised borrower exposure in the first months of the pandemic

1. Supply chain risk will be a significant blip on the lender radar

A key component of 2022 lender due diligence will be assessing supply chain risk and its potential impact on credit quality, in the same way that lenders scrutinised borrower exposure in the first months of the pandemic. At the time, lenders did not restrict their diligence to sales and EBITDA, doing far more work on understanding borrower markets, business models and downside risks.

Similar frameworks are now being applied to supply chain risk, as global shortages of key commodities (e.g., CO2 and oil) and components (e.g., semiconductor chips), as well as tight labour markets in areas such as logistics and shipping, increase the chances of business disruption and lost sales across European businesses.

Some argue that this disruption is the short-term result of economies opening up post-COVID-19, generating a sudden rise in demand and creating a temporary bottleneck. For example, in the US, analysis from Debtwire Par, published in November 2021, shows imports increasing 20% year-on-year and 0.6% month-on-month, to an all-time high of US$289 billion by September (compared to US$260 billion in January 2021).

At the same time, according to data from the Marine Exchange, there were 81 container ships in the waters surrounding the ports of Long Beach and Los Angeles—which, combined, handle 40% of the cargo containers entering the US. Pre-pandemic, it was rare for a single ship to have to wait for a berth.

Any supply chain disruptions such as these in the months before a transaction may well form a red flag for some lenders, as it is not optimal to be forced to address supply chain issues and amend models in the period immediately following the funding of a deal. Such risks may increase business costs and delay tight delivery schedules, to say nothing of the potential loss in customers.

Borrowers will need a plan to address any supply chain concerns investors may have, whether shifting to local supply chains or ensuring enough of a stockpile to lock in prices until such shortages are worked out.

2. Inflation and interest rate rises will need to be watched carefully

Low interest rates supported the growth of leveraged finance markets in the past decade and helped lenders and borrowers navigate any disruption caused by the pandemic. The market, however, is becoming choppier, with inflation risks coming to the forefront and some effects being seen in the US and Europe. It is still unclear whether rising inflation is a short-term phenomenon, but interest rate rises are clearly on the cards.

In a scenario where rates start to tick upwards, the question is whether a higher cost of capital will reduce borrower appetite and make leveraged finance credits less attractive for lenders.

The answer depends on the speed and degree with which rates rise. Most investors will still have cash to deploy and will still be looking for attractive returns on risk. Inflation and interest rates may be back in the frame, but the risk/return picture will not necessarily change if rates rise, especially with enough warning.

In November 2021, for example, European Central Bank President Christine Lagarde stated that 'conditions to raise rates are very unlikely to be satisfied' in 2022.

In the UK, it's been a slightly different picture. The Monetary Policy Committee (MPC) held off raising rates for most of 2021 but, in November, when asked when it could happen, the governor of the Bank of England and chair of the MPC, Andrew Bailey, said, 'from now onwards'. Then, just one month later, that prediction came true, with the MPC voting to raise interest rates from 0.1% to 0.25%.

The US Federal Reserve has also made it clear that they are likely to follow suit as soon as March 2022, which could have knock-on effects for borrowers and lenders in Europe as well.

If and when interest rates start to rise in the EU, volumes may drop off slightly as opportunistic borrowers fall away, but the fundamentals underlying the leveraged finance proposition will remain very much the same.

3. The PE spending spree has a way to go yet

Buyout-backed deal flow will remain a driving force in leveraged finance markets in 2022, as financial sponsors continue to raise, deploy and distribute capital at unprecedented levels. European buyout loan issuance soared 81% year-on-year to €66.7 billion in 2021, with high yield buyout provision ratcheting up 120% to €15.1 billion.

European exit and buyout value reached US$613.2 billion in 2021—the highest annual total on Mergermarket record, up 47% on its previous record year back in 2007 and more than triple in size from levels a decade ago. With global dry powder reserves topping US$3 trillion, there is little sign of PE's growth trajectory slowing down.

A bursting pipeline of buyout-backed financing deals coming to market—including the large debt packages that will be required to fund Clayton, Dubilier & Rice's £10 billion buyout of supermarket chain Morrisons and KKR's €33 billion bid for Telecom Italia (should the deal go ahead)—will provide lenders with a steady flow of work well into 2022.

4. Lenders searching for yield will broaden net and finance riskier credits

Although COVID-19 variants, as well as the prospect of rising interest rates and inflation, all pose significant challenges for debt markets in the coming year, investors will remain open to backing the right lower-rated credits to lock in yields.

Lenders still have large pools of capital to deploy and are actively seeking opportunities to invest. For example, new CLO issuance in Europe climbed 75% to €38.5 billion in 2021, reaching a record monthly high of €6.3 billion in November.

Lenders are still leaning towards high-quality issuers but have broadened their net in the past 12 months to include a higher proportion of credits with lower ratings.

In the absence of higher-rated credits issuing debt at increased interest rates—which was a feature of the market's initial reaction to COVID-19 as borrowers topped up liquidity lines—B-rated credits accounted for a larger share of overall issuance in 2021 than in 2020.

In 2022, investors will remain open to taking on more perceived risk in return for the higher pricing these issuers are offering. A wildcard will be whether the major ratings agencies see fit to downgrade a material number of credits as events unfold in 2022 and beyond.

5. Perspectives on credit quality will continue to affect terms and documentation

Even in a red-hot market, borrowers are not having it all their own way. Leveraged loan and high yield bond pricing moved higher in 2021, as did the number of margin flexes in syndication processes.

In 2022, if a higher volume of lower-rated credits come to market, lender and sponsor views on credit quality will determine what terms and pricing are made available.

Top-tier sponsors will continue to push hard for documentation flexibility on popular credits, and lenders will be willing to give more ground in these situations. Convergence with the looser US term loan B structures will continue apace on sought-after deals. For example, in limited cases, sponsors may be able to exclude revolving credit facilities from leverage limit calculations.

For deals that do not fly off the shelves, however, lenders and borrowers will be more prudent. Mid-tier sponsors will likely be more flexible and accept tighter documents and higher prices to close their deals, as a pragmatic tone will run through the market to continue to get deals done.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: European leveraged debt in focus (PDF)

View full image: European leveraged debt in focus (PDF)