Partner, Latin America Group Leader and Editor of Latin America Focus

What a difference a year makes.

In our inaugural edition of Latin America Focus, produced by the Latin America Group at White & Case in the autumn of 2021, we offered scant good news. COVID-19 had thumped Latin American business harder than it had companies anywhere else, contracting Latin America's 2020 economies by nearly 7 percent, compared to a global average contraction of 3 percent. Latin America also was riding a rollercoaster of mounting populism and resource nationalism in 2021, and feeling the uncertainty that accompanies such trends.

Despite the then-present challenges, in that edition we highlighted a number of reasons to anticipate a LatAm resurgence in 2022, including an expected investment push into the region in certain sectors; the search for yields in emerging markets, commitments to mitigate climate change by global natural resources and energy companies; and the technology-driven push to digitize an increasingly global world economy.

How inspiring it has been to see most of this resurgence flower throughout the year since.

In this Fall 2022 edition of Latin America Focus, partners in our Latin America Group have written articles based on their personal experiences in the trenches and on market research that look forward to 2023 and together reveal the continuation—and perhaps acceleration—of many of the same global megatrends that propelled selective investment growth in the region in 2022.

Chief among these megatrends is Latin America's forceful digitalization efforts. The region's large, young and habitually connected population, the current global financial equity investor liquidity and related resilient M&A activity and its booming fintech industry are effectively working together to position Latin America as a gigantic growth market for the tech sector over the next five years. In the tech hotbeds of Brazil, Chile, Colombia and Mexico, the number of tech startups has nearly tripled in the past five years, and across Latin America, technology transactions accounted for more than 40 percent of M&A deal value through the first half of 2022.

Not far behind the technology deal growth is the global energy transition; already Latin America's abundant wind and solar energy sources bolster its economy, attracting investment and creating new job opportunities. Still a major global player in oil & gas, the region looks well placed to emerge as a key global producer of green hydrogen. And as the energy transition picks up pace, carbon markets are starting to emerge across the region, teasing a future wherein Latin America stands as an innovative hub of carbon market activity and low-carbon development for the benefit of the entire world.

To be sure, challenges remain in both energy and tech: National hydrocarbons companies in the region, which account for a massive slice of hydrocarbon production there, continue to prioritize energy security over energy transition. Latin American countries (Brazil perhaps excepted) lag behind their North American and European counterparts on investment in digital infrastructure and addressing the digital divide between rich and poor. Despite the fintech boom, Latin Americans still have relatively little access to banking services and secure online payment gateways. Latin American countries also lag on developing intermediary liability frameworks and related consumer protections that offer security and certainty to digital platforms and their users.

The White & Case Latin America Group has produced this publication to provide market insights from our practical experiences and proprietary research that could be valuable to senior decision-makers eyeing the region for opportunities. I hope that you enjoy reading these insights and will contact us if there are any topics that you would like us to cover in future editions of Latin America Focus.

Latin America is closely aligned with global megatrends and 2023 will likely see the continuation—and perhaps even acceleration—of these trends in the region

Is Latin America the next frontier for technology M&A?

In a region suffering from global trade dislocations, inflation, higher interest rates and complex political cycles, dealmakers remain cautiously optimistic that the transition to digital services across the region will create significant M&A opportunities in the technology sector.

The future of US-Latin America trade relations: What can we achieve in the next few years?

From the Washington Consensus of the 1990s to the Biden administration's recently proposed Americas Partnership for Economic Prosperity, policymakers seem to have lost some of their ambition.

Three factors distinguish Latin America as a potential leader in carbon markets: its adoption of carbon markets at the national and subnational level; government incentives promoting low-carbon technologies; and existing energy infrastructure

The accelerating climate change crisis has shifted the investor focus onto how companies incorporate ESG factors—environmental, social and governance—into their business strategy. Investors are putting companies under increased scrutiny for their environmental impact and especially greenhouse gas (GHG) emissions. That interest, along with commitments by countries to international pledges such as the Paris Agreement to reduce GHG emissions, has led to growing participation in carbon markets from businesses seeking to meet climate-related targets or offset certain climate-related impacts. Although it's not without challenges, this is a time of tremendous opportunity for companies and countries alike. Carbon markets represent an increasingly useful solution for reducing GHG emissions and driving investment in energy transition and low-carbon technologies.

Three factors distinguish Latin America as a potential leader in the field: its adoption of carbon markets at the national and subnational level; government incentives promoting low-carbon technologies; and existing energy infrastructure. The region is also abundant in natural resources. Experts predict that the development of advanced carbon marketplaces in Latin America could lead to significant revenue generation as global revenues from carbon pricing continue to soar. Moreover, expansion of carbon markets in the region would increase the global competitiveness of the supply of credits, further encouraging the development of carbon markets globally.

The international climate regime has shifted in recent years from a top-down approach (based on mandatory emissions commitments) to a system driven largely by voluntary pledges from both governments and private actors. Latin America's existing carbon landscape includes both voluntary carbon markets and markets for purchasing credits for regulatory compliance purposes. According to a 2021 McKinsey report, based on the existing market infrastructure in Latin America, both forces are expected to drive continued growth of carbon markets in the region.

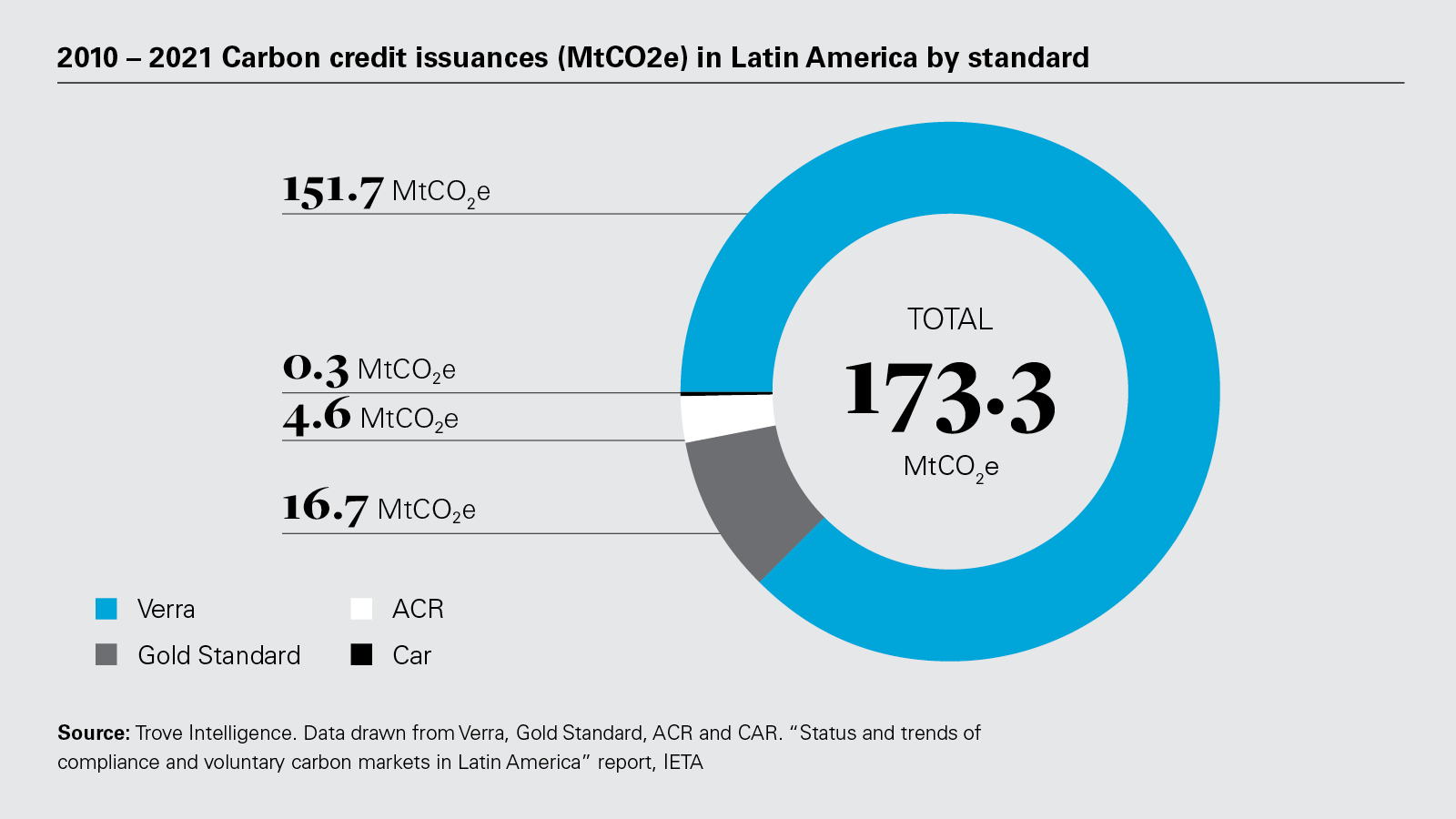

Latin America is the world’s second largest provider of voluntary credits, with slightly less than 20% of the total global credit supply coming from the region in 2020 and 2021

Source: "Status and trends of compliance and voluntary carbon markets in Latin America" report, IETA

64

Carbon pricing instruments (CPIs) in force worldwide in 2021

Source: "Status and trends of compliance and voluntary carbon markets in Latin America" report, IETA

Strong momentum in Latin American carbon markets

Regulatory frameworks within Latin America vary by country. The region has the second-highest number of subnational jurisdictions with a pledge to achieve net-zero emissions, with 209 cities and five regions making such a pledge. As of 2021, the region also has four federal carbon taxes, three subnational carbon taxes and one national emissions trading system (ETS). Colombia, Chile and Mexico lead through their comprehensive and tailored carbon marketplaces, while Brazil and Argentina are gathering data to implement effective strategies. These frameworks have strong support from key international organizations.

Colombia, Chile and Mexico are at the forefront of the development and advancement of carbon markets. These countries have established both carbon taxes at national and state government levels, and voluntary carbon marketplaces at the national level. In addition, Colombia is in the process of developing an ETS. Carbon taxes remain a popular instrument for emissions reductions in Latin America, in part because the revenues raised by carbon taxes can achieve a variety of national environmental, social and economic goals. For example, in Colombia, the revenue from the country's carbon tax flows to the Sustainable Colombia Fund, an initiative to support sustainable projects in areas affected by violent conflict. Similarly, Argentina and Brazil are capitalizing on the momentum and have begun implementing carbon-pricing instruments (CPIs).

Certain international bodies are demonstrating a commitment to expanding carbon markets in Latin America. A notable example is the World Bank's Partnership for Market Readiness (PMR), with its commitment to provide technical assistance to 23 countries to design and deploy CPIs, including direct assistance to Argentina, Brazil, Chile, Colombia, Costa Rica, Peru and Mexico. This global platform has provided information obtained through country-specific studies to instruct governments on successful tactics for carbon market implementation. For Colombia, for example, PMR has conducted an evaluation of ETS system design, an impact assessment of an ETS on sectoral competitiveness, and a study on design options for a mandatory GHG reporting program. An increasing number of international organizations are taking notice of the abundant opportunities in Latin America and have pledged to work alongside lawmakers to expedite the process.

Regulatory and implementation efforts in carbon markets by country

While carbon markets are expanding throughout Latin America, there are variations across countries in the region in terms of market design and project development.

Mexico

Following the introduction of the 2012 General Climate Change Law (GCCL), Mexico established a carbon tax in 2013 for sources with emissions exceeding a standard set for natural gas, with the value of the tax capped at 3 percent of the value of the resource. Mexico also established MexiCO2, a voluntary exchange that provides carbon credits to companies that develop environmentally friendly projects, which can be used to offset costs from the carbon tax. In 2019, amendments to the GCCL gave Mexico's environmental authority, the Secretariat of Environment and Natural Resources (SEMARNAT), the mandate to establish an ETS program. It would operate for three years, two years in the pilot phase and one to transition into the fully operational ETS, scheduled to begin in 2023. Industrial and energy plants that declared emissions of more than 100,000 metric tons of CO2-equivalent between 2016 and 2019 are taking part in the pilot phase, totaling approximately 300 facilities and representing approximately 45 percent of national emissions. The pilot program has no economic impact on regulated entities and looks to test system design and build capacity in emissions trading, as well as to generate a reference value for emission allowances and offsets in the operational phase.

Brazil

Brazil's National Climate Change Policy law was established in 2009 and introduced the concept of a Brazilian Market for Emission Reduction. Recently, the country's Ministry of the Environment made notable advances in developing a voluntary carbon market by establishing the Forest+ Carbon Program in 2020 and the National Payment Policy for Environmental Services in 2021. In May 2022, Brazil's president signed Federal Decree No. 11.075/2022, announcing a plan to create a national carbon market. The plan assigns Brazil's Ministries of the Environment and Economy the responsibility for proposing "Sectoral Plans for the Mitigation of Climate Change," to effectively set sector-specific goals for emissions reduction. Sectors that include electric energy, urban public and cargo transport, manufacturing and durable consumer goods, chemicals, paper and cellulose, mining, civil construction, and health services and agriculture can register their carbon footprints in the new registry. Sectors can present proposals for establishing the emission reduction curve within 180 days (i.e., by November 2022, but with the deadline extendable for another 180 days), considering the long-term climate neutrality objective informed by Brazil's Nationally Determined Contribution under the Paris Agreement. In addition to the regulatory path, Bill 528/21, which is being debated in Brazil's Congress, is intended to establish the legal framework for the Brazilian Market for Emission Reduction.

Colombia

Colombia has several carbon pricing mechanisms. In 2016, it adopted a carbon tax of approximately US$5 per metric ton of CO2 that covers fossil fuel emissions. The system allows companies to avoid paying the tax by purchasing carbon offsets from projects within Colombia. The government also launched the Colombian Voluntary Carbon Market Platform the same year with the aim of attracting investors. Notably, the marketplace has been subject to concerns regarding the integrity of some carbon credits.

In 2018, Colombia adopted its climate change policy, the National Climate Change System (SISCLIMA), by decree, mandating the adoption of an ETS, the National Program of Greenhouse Gas Tradable Emission Quotas. This program, currently in the developmental stage, will create a system of carbon allowances and allocations, and contains crediting provisions granting allowances for voluntary GHG reductions that are verified and certified through the proper channels.

Chile

Chile has adopted several policies relating to the pricing of carbon. In 2017, it introduced a tax on carbon emissions, which has been levied at a rate of US$5 per metric ton of CO2. Chile's carbon tax is widely considered too low, and the government has announced plans to set a higher tax or explore other options. Chile released a long-term national energy strategy released in 2021, setting the objective of a tax of US$5 per metric ton of CO2 starting in 2030, and other proposals have suggested a carbon tax of US$40 per metric ton of CO2.

Chile's new legal framework on climate change came into force in June 2022 and includes measures to achieve net carbon neutrality by 2030. The law requires Chile's Ministry of the Environment to create an emissions mitigation plan with limits for each economic sector, and to specify GHG emission limits for a range of sources, based on a system of emission standards set by technology, sector or activity. Regulated entities that perform better than the standard for their sector will be required to have their surplus emission reductions certified, which may then be sold to and used by other regulated entities for compliance with their respective emissions standards.

Latin America has the potential to emerge as a leading hub of compliance and voluntary carbon market activity and low-carbon innovation in the region

Recent trends driving carbon markets in Latin America

Among the many factors driving the expansion of carbon markets, perhaps one of the most critical is the growth of low-carbon technologies financed and developed throughout Latin America. While governments across the region have offered incentives for production of renewable energy, not all carbon markets include renewable energy projects. As a result, while renewable energy projects remain a leading source of carbon credits, especially in voluntary markets, governments will need to incentivize other low-carbon technologies, such as carbon capture, utilization and storage (CCUS), to increase the supply of high-quality credits in the region.

There is substantial CCUS potential in Latin America due to existing oil & gas development and additional production sources because oil & gas reservoirs offer geologic carbon storage potential. Due to high implementation costs and a scarcity of incentives, CCUS has yet to achieve commercial-scale success in the region. There is, however, optimism around coupling a carbon tax or offset credits with regulatory support to aid in promoting adoption of CCUS. Further, the oil & gas industry's prolonged presence in Latin America gives the region another critical advantage: a long record of reservoir characterization providing data for assessing suitable hydrocarbon reservoirs for geological CO2 storage.

Several companies are already pursuing Latin America's CCUS potential by piloting CCUS projects. Petrobras announced it is developing a new carbon sequestration project that will re-inject carbon dioxide into the subsea reservoir in Brazil's Libra oil field, to be implemented in 2024; and Ecopetrol will pilot a CCUS project in 2023 with the goal of capturing 1 million metric tons of CO2 from its refineries and storing the emissions at a gas-depleted reservoir.

Additionally, there is significant opportunity for the supply of carbon credits in connection with reforestation projects or avoided deforestation (REDD+) due to significant forest resources in the region. Carbon credits associated with REDD+ projects have a strong presence in Latin America. REDD+ projects providing carbon credits have been highlighted for the potential economic benefit they can provide to the often-marginalized communities that steward these forests.

There are challenges to be noted with respect to the monitoring and verification of carbon credits associated with such projects in Latin America. Credits generated from reforestation or avoided deforestation projects are subject to criticism for lack of regulatory oversight and relying on imprecise calculations with the potential to result in inaccurate accounting of these carbon credits. This uncertainty can jeopardize regional climate goals and the reliability of carbon markets generally. Market participants looking to rely upon carbon credits associated with REDD+ projects should conduct independent diligence and exercise caution in relying upon the verification of these credits.

Overall, there has been an increase in participation in Latin American carbon markets due to both the expansion of compliance and voluntary carbon markets, and ambitious climate goals established globally by governments and private actors, with the hydrocarbon industry leading the energy transition efforts in the region. Similarly, participation by oil & gas companies in emissions reduction will likely influence the advancement of future carbon markets in the region. Recent announcements by Latin American oil & gas companies suggest that demand will continue to surge for carbon credits. For example, Ecopetrol recently announced it is aiming for net-zero carbon emissions by 2050, targeting a 50 percent reduction in scope 1, 2 and 3 emissions from a 2019 baseline. Additionally, Ecopetrol sold its first million barrels of "carbon-neutral" oil (i.e., oil from which the emissions from the production, extraction and transportation are offset by carbon credits generated from renewable energy projects). As Latin American companies continue to advance their emissions reduction efforts, the growth of carbon markets in the region is likely to accelerate.

Tremendous potential for voluntary carbon market activity and innovation

Latin America has the potential to emerge as a leading hub of compliance and voluntary carbon market activity and low-carbon innovation, including expansion of REDD+ projects and accelerated CCUS investment in the region. The region's efforts to regulate GHG emissions demonstrate that carbon pricing has an important role to play in driving decarbonization in the region. As additional jurisdictions in Latin America move toward the implementation of carbon markets, market participants must educate themselves on the operation of carbon market mechanisms. Partnerships with and investment in private companies leading in the low-carbon technology space are likely to spur further development of carbon markets.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: 2010 – 2021 Carbon credit issuances (MtCO2e) in Latin America by standard (PDF)

View full image: 2010 – 2021 Carbon credit issuances (MtCO2e) in Latin America by standard (PDF)

View full image: Carbon market and pricing initiatives in Latin America implemented or under consideration/development (PDF)

View full image: Carbon market and pricing initiatives in Latin America implemented or under consideration/development (PDF)