Partner, Latin America Group Leader and Editor of Latin America Focus

What a difference a year makes.

In our inaugural edition of Latin America Focus, produced by the Latin America Group at White & Case in the autumn of 2021, we offered scant good news. COVID-19 had thumped Latin American business harder than it had companies anywhere else, contracting Latin America's 2020 economies by nearly 7 percent, compared to a global average contraction of 3 percent. Latin America also was riding a rollercoaster of mounting populism and resource nationalism in 2021, and feeling the uncertainty that accompanies such trends.

Despite the then-present challenges, in that edition we highlighted a number of reasons to anticipate a LatAm resurgence in 2022, including an expected investment push into the region in certain sectors; the search for yields in emerging markets, commitments to mitigate climate change by global natural resources and energy companies; and the technology-driven push to digitize an increasingly global world economy.

How inspiring it has been to see most of this resurgence flower throughout the year since.

In this Fall 2022 edition of Latin America Focus, partners in our Latin America Group have written articles based on their personal experiences in the trenches and on market research that look forward to 2023 and together reveal the continuation—and perhaps acceleration—of many of the same global megatrends that propelled selective investment growth in the region in 2022.

Chief among these megatrends is Latin America's forceful digitalization efforts. The region's large, young and habitually connected population, the current global financial equity investor liquidity and related resilient M&A activity and its booming fintech industry are effectively working together to position Latin America as a gigantic growth market for the tech sector over the next five years. In the tech hotbeds of Brazil, Chile, Colombia and Mexico, the number of tech startups has nearly tripled in the past five years, and across Latin America, technology transactions accounted for more than 40 percent of M&A deal value through the first half of 2022.

Not far behind the technology deal growth is the global energy transition; already Latin America's abundant wind and solar energy sources bolster its economy, attracting investment and creating new job opportunities. Still a major global player in oil & gas, the region looks well placed to emerge as a key global producer of green hydrogen. And as the energy transition picks up pace, carbon markets are starting to emerge across the region, teasing a future wherein Latin America stands as an innovative hub of carbon market activity and low-carbon development for the benefit of the entire world.

To be sure, challenges remain in both energy and tech: National hydrocarbons companies in the region, which account for a massive slice of hydrocarbon production there, continue to prioritize energy security over energy transition. Latin American countries (Brazil perhaps excepted) lag behind their North American and European counterparts on investment in digital infrastructure and addressing the digital divide between rich and poor. Despite the fintech boom, Latin Americans still have relatively little access to banking services and secure online payment gateways. Latin American countries also lag on developing intermediary liability frameworks and related consumer protections that offer security and certainty to digital platforms and their users.

The White & Case Latin America Group has produced this publication to provide market insights from our practical experiences and proprietary research that could be valuable to senior decision-makers eyeing the region for opportunities. I hope that you enjoy reading these insights and will contact us if there are any topics that you would like us to cover in future editions of Latin America Focus.

Latin America is closely aligned with global megatrends and 2023 will likely see the continuation—and perhaps even acceleration—of these trends in the region

Is Latin America the next frontier for technology M&A?

In a region suffering from global trade dislocations, inflation, higher interest rates and complex political cycles, dealmakers remain cautiously optimistic that the transition to digital services across the region will create significant M&A opportunities in the technology sector.

The future of US-Latin America trade relations: What can we achieve in the next few years?

From the Washington Consensus of the 1990s to the Biden administration's recently proposed Americas Partnership for Economic Prosperity, policymakers seem to have lost some of their ambition.

The future of US-Latin America trade relations: What can we achieve in the next few years?

From the Washington Consensus of the 1990s to the Biden administration’s recently proposed Americas Partnership for Economic Prosperity, policymakers seem to have lost some of their ambition.

While the Washington Consensus policies resulted in seven years of economic growth in the 1990s, the years that followed brought about a period of recession and stagnation

71%

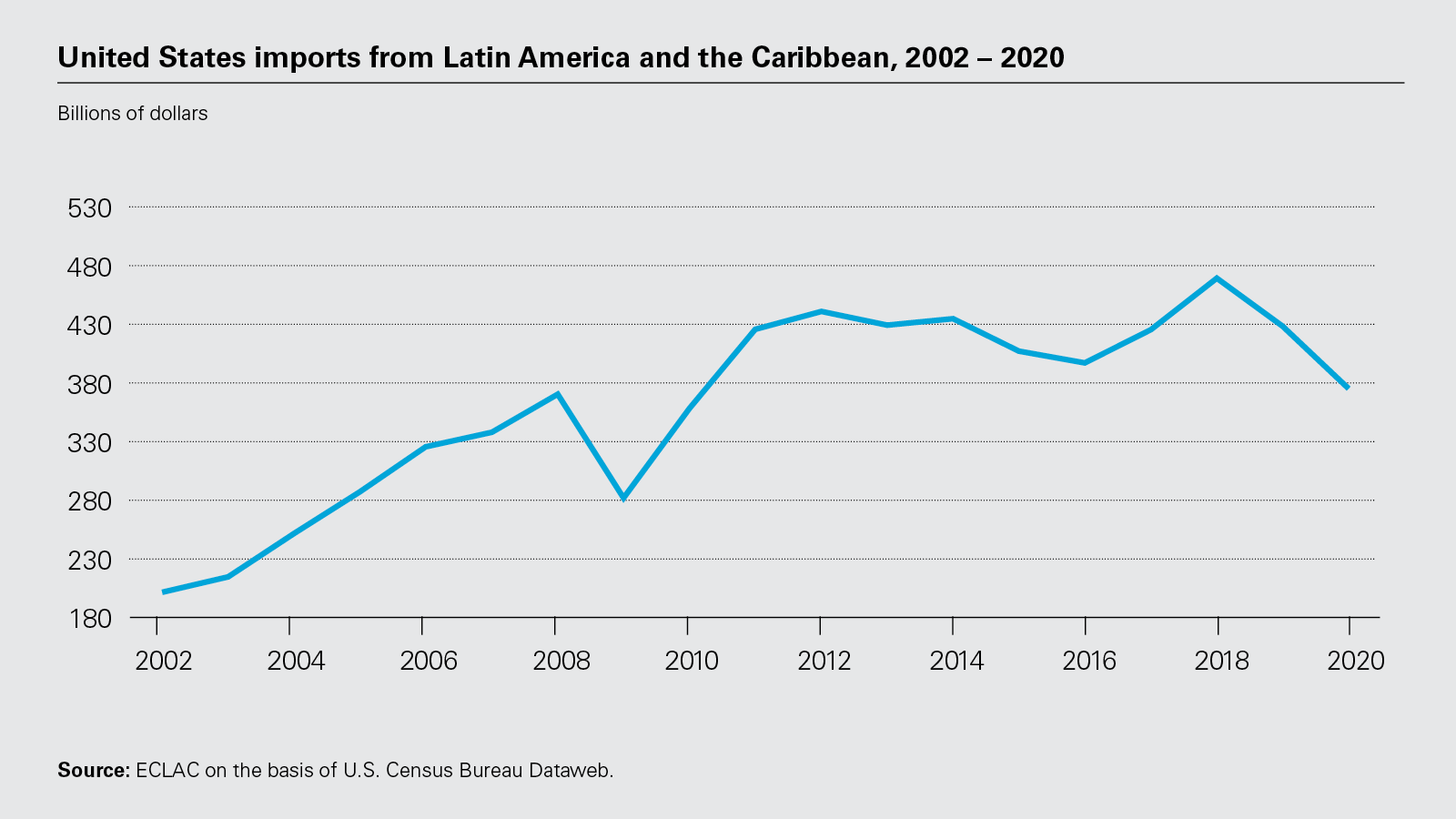

US trade with Latin America is dominated by trade with Mexico, approximately 71% of US trade with the region

The Washington Consensus

The late 1980s and early 1990s were a time of change and hope for many Latin American countries. The region moved toward openness in their societies and economic policies, some of which became enshrined in new laws and constitutional reform. But expectations outpaced performance, and what followed was economic instability, short-term cycles of hyperinflation, recession and increases in public debt. Policymakers—and the International Monetary Fund (IMF)—searched for ways to stabilize the region and continue the trajectory toward open economies and societies.

The Washington Consensus was an economic, social and political approach to the problem, and it gained support among governments, development agencies, and institutions such as the IMF and World Bank. Economist John Williamson is credited with coining the term in 1989 when he described a list of ten policy reforms that he argued were universally agreed upon by US and regional policymakers as the most preferable to be implemented in Latin America.

Williamson's list of reforms distanced itself from the long-accepted policies of inflation tolerance and import substituting industrialization, and instead focused on "macroeconomic discipline, outward orientation and the market economy," with a particular emphasis on economic liberalization. The ten reforms included: fiscal discipline; reordering of public expenditure priorities; tax reform; liberalizing interest rates; creating competitive exchange rates; liberalizing trade; liberalizing inward foreign direct investment; privatization; deregulation; and legal security for property rights. While there has been much criticism and interpretation of this approach over the years, many describe the Washington Consensus as paradigm-shifting.

Since then, the term "Washington Consensus" has come to refer more generally to the international development strategies focusing on the goals of privatization, macro-stability and liberalization. It has also grown to develop an association with market fundamentalism, a concept that markets solve most economic problems on their own if left alone.

In the 1990s, almost all of the Central and South American countries adopted nearly all ten of the original reforms of the Washington Consensus. Some proponents of the approach have cited inflation control, increases in foreign investment, and increased fiscal stability as positive results of the implemented reforms.

Today, the Washington Consensus is generally regarded as having failed. Its policies did not improve poverty or employment rates in the region. Countries that followed the policies saw limited growth: From 1990 to 2002, Latin America had only a 2.4 percent average annual growth rate, with many countries experiencing a net decline in income per capita.

While the Washington Consensus policies had resulted in seven years of economic growth in the 1990s, the years that followed brought about a period of recession and stagnation. Countries in the region developed some of the worst wealth and income distribution disparities in the world, with the broad perception that any advancements were benefiting the elite few rather than society at large. As a result, disillusionment with the Washington Consensus spread, with some critics attributing the failure to US policymakers' lack of understanding of international development and developing countries, as well as the narrow development objectives that focused on increasing GDP.

Trade played an important role in the notion of a more open Latin America on the principles of the Washington Consensus: It was no coincidence that support for a Free Trade Area of the Americas (FTAA) developed in the early 1990s. The first Summit of the Americas in Miami in 1994— the first post-Cold War meeting of American heads of state—signaled a joint effort to connect the economies of all the countries in the Americas into one free trade zone. As part of the FTAA agreement, barriers to trade and investment between the 34 countries in the region (excluding Cuba) were to be eliminated progressively, with a plan of making significant progress in the FTAA by 2000 and completing negotiations by 2005.

Despite an initial draft agreement in 2001, the project ultimately failed in 2005 at the Fourth Summit in Mar del Plata. As with any complex negotiating process, it would be difficult to pinpoint the reasons for failure, but there were certainly a number of difficult issues. Disagreements over controversial issues such as subsidies for agriculture and protections for intellectual property stalled the talks initially. Also, in the aftermath of the September 11, 2001 terrorist attacks on the United States, the US agenda was less focused on negotiations with Latin America. Some Latin American leaders expressed skepticism over the Bush administration's War on Terror and the invasion of Iraq. New leaders such as Hugo Chavez of Venezuela rose to power in the late 1990s and early 2000s, pursuing a more nationalist approach focused on greater autonomy in policy formulation. These and other forces led to a disappointing result: After years of negotiations, technical training, and general optimism in creating a hemispheric free trade zone, the process came to an abrupt end.

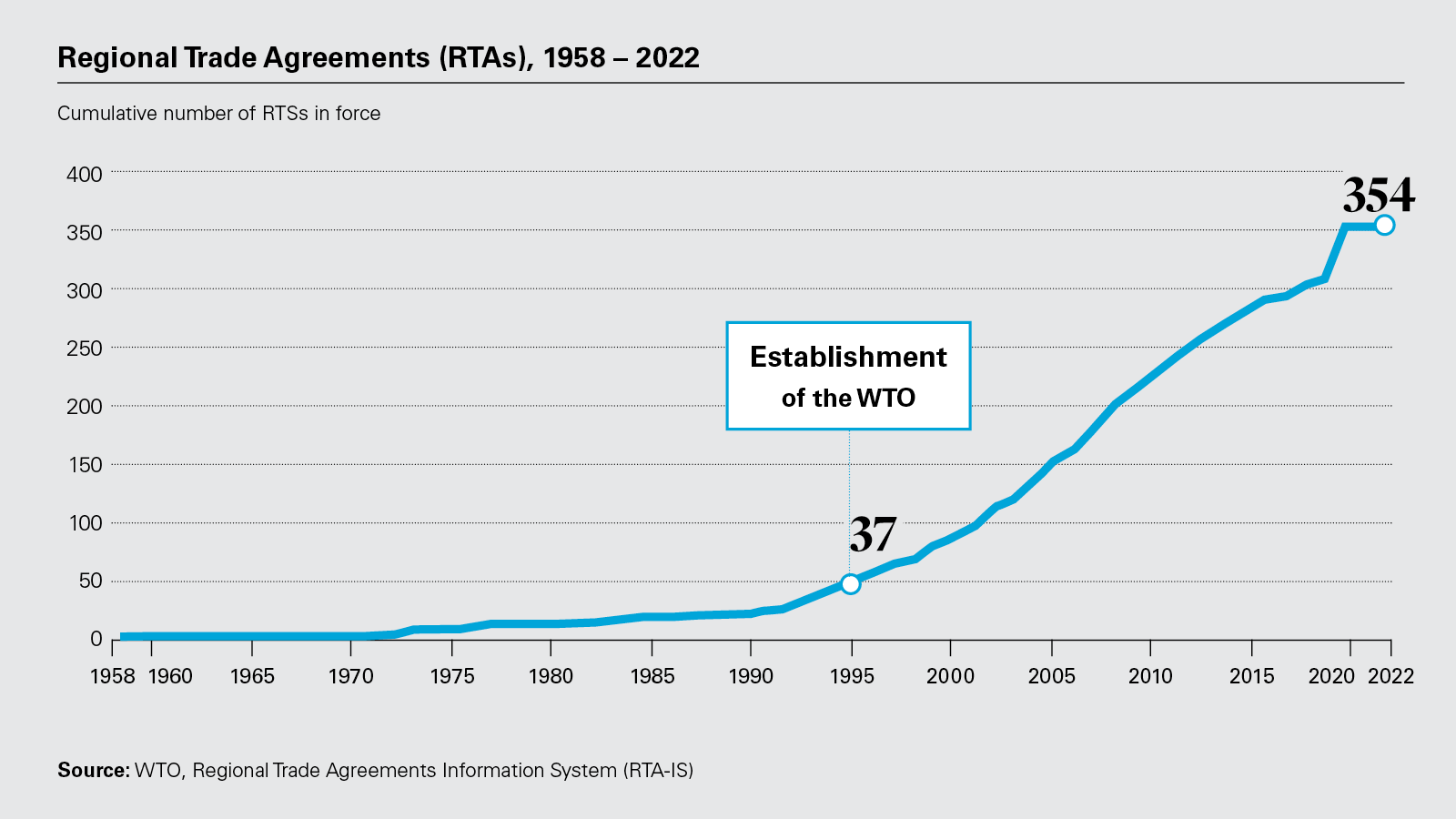

If support for a comprehensive, hemispheric FTAA waned, enthusiasm for trade liberalizing agreements among smaller groups of countries within the hemisphere seemed to grow. The North American Free Trade Agreement (NAFTA) of 1994 committed the US, Canada and Mexico to a process of integration that was broad in scope. Through the MERCOSUR, the countries of the Southern Cone of South America (except Chile) formed their own FTAA that promised to go further toward a customs union. In the meantime, individual countries, such as Mexico, seemed to have embraced a policy of signing FTAs with individual countries or groups of countries, many of which saw an agreement with Mexico to be a prelude to increasing relations with the NAFTA countries. In this sense, the countries of the Western Hemisphere contributed to the explosion of regional and other preferential trading agreements developing—somewhat paradoxically—after the creation of the World Trade Organization and the commitment to multilateralism. (See graph below.)

Has the Biden administration made an impact so far?

The Biden administration has expressed interest in deepening economic cooperation among countries in the Americas, but this has yet to translate into meaningful trade outcomes. So far, the administration has prioritized resolving disputes with the European Union, reasserting US trade leadership in Asia-Pacific following the US withdrawal from the Trans-Pacific Partnership, and managing US trade and competition with China. The administration has not approached trade relations in the Americas with the same urgency, focusing on other regional challenges such as migration and immigration policy.

Moreover, and consistent with its predecessor, the administration has expressed skepticism about the benefits of free trade agreements (FTAs), particularly for US workers and the manufacturing sector. There is, therefore, little optimism that the US will pursue new bilateral or regional FTAs with Latin American partners—much less reinvigorate the hemispheric FTAA—in the near future. Instead, the administration has shown a preference for narrower, less binding arrangements and bilateral dialogs, even with close allies and trading partners such as the EU, the UK and Japan.

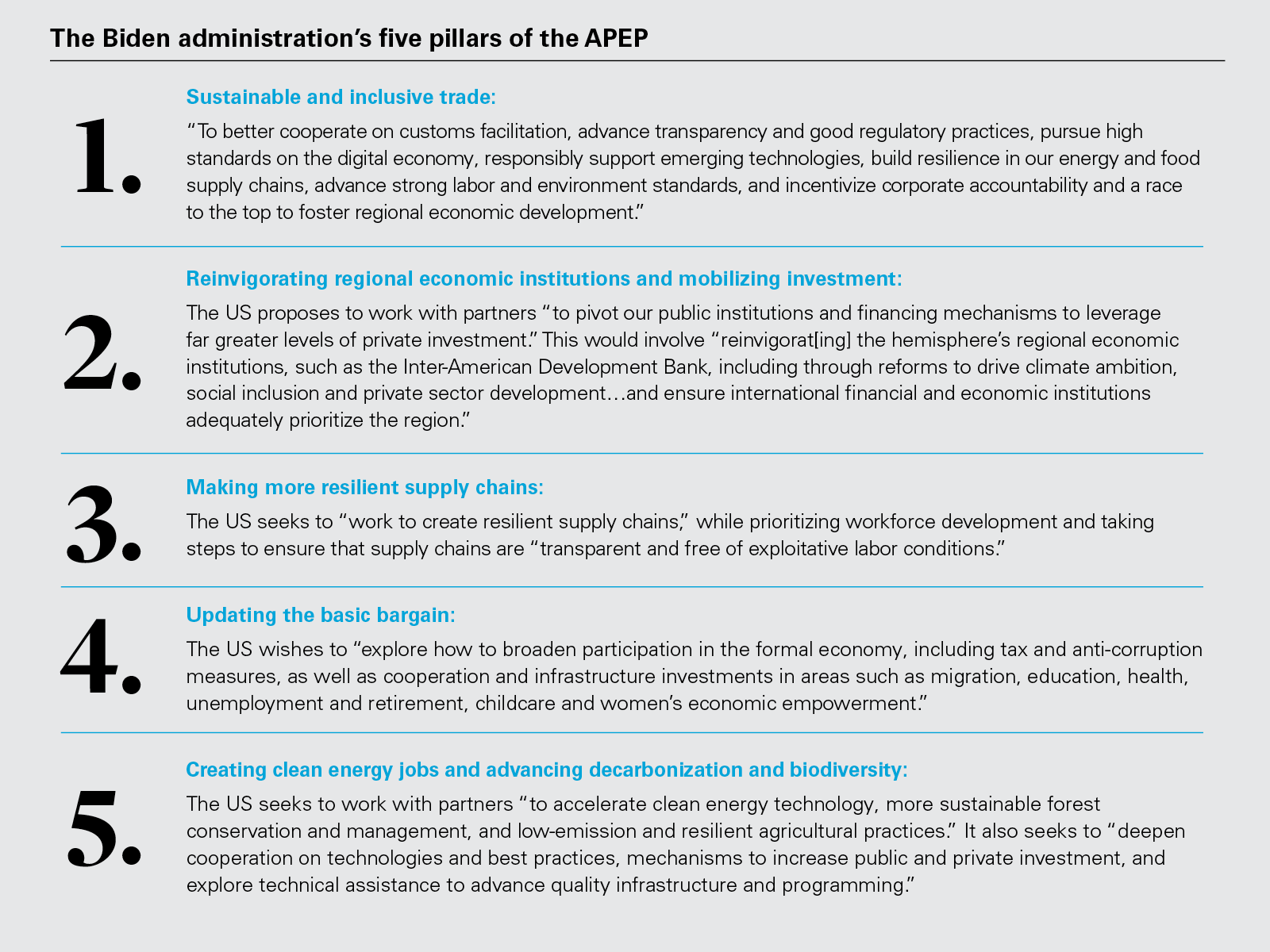

The new Americas Partnership for Economic Prosperity (APEP) was announced on June 8, 2022 at the Ninth Summit of the Americas

Enter the Americas Partnership for Economic Prosperity (APEP)

On June 8, 2022, at the Ninth Summit of the Americas, the Biden administration announced that it would seek to negotiate the APEP with countries in the Western Hemisphere. Representatives of 15 countries in the region, including Argentina, Brazil, Colombia, Mexico and Peru, attended the summit. The proposed scope and structure of the APEP would resemble that of the Indo-Pacific Economic Framework (IPEF) that the Biden administration is pursuing with Indo-Pacific countries, covering supply chains, clean energy, infrastructure and a small subset of trade issues, among other topics. The Biden administration intends to hold initial consultations with like-minded partners in the region over the coming months, with the goal of reaching agreement on the scope of the APEP and launching formal negotiations this autumn, and later opening the process up to other countries in hopes of garnering widespread support.

The APEP is not expected to involve tariff liberalization or other market access commitments, and the administration has indicated that it does not intend to submit it to Congress for approval. Administration officials have also proposed that the APEP use a flexible structure, allowing countries to choose the pillars they want to join, as opposed to requiring them to assume obligations under all five.

However, the administration has not yet announced whether any countries have agreed to participate in the initial consultations, and Latin American countries do not appear to be receiving the proposal with enthusiasm.

Regional Trade Agreements were in force as of March 2022

14.7%

Mexico is one of US top three trade partners, accounting for 14.7% of US total trade in 2021

Source: ECLAC

Rationale and prospects for the APEP

China has rapidly expanded economic ties with Latin America over the past two decades, becoming South America's largest trading partner, and has become a major source of foreign direct investment and lending in the region. These trends have increased the pressure on the administration to develop an economic and trade agenda that solidifies the US role as central in the region.

The APEP was modeled on the IPEF, with similar economic and geopolitical considerations. Among its objectives is the desire to counter China's growing influence in a region of critical importance to the US—the adoption of trade rules that reflect current US priorities— without committing the US to a comprehensive FTA.

The Biden administration also views the APEP as an opportunity to promote higher labor and environmental standards in the region, in line with recent trade agreements such as the US-Mexico-Canada Agreement (USMCA). But given the domestic political constraints placed on its scope, it will be challenging to ensure that the APEP appeals to a wide range of Latin American countries and has meaningful commercial benefits. The US has provided few details regarding the APEP's specific objectives, making it difficult to gauge the progress.

Key challenges and considerations for the negotiation of the APEP include:

Balancing inclusivity with high ambition. The Biden administration wants to secure widespread participation in the APEP, while also ensuring that it includes high-standard commitments in politically sensitive areas such as digital trade, labor and the environment. Given the differing levels of development and divergent policy approaches in the region, this will be difficult to achieve. The administration has proposed to allow APEP participants to self-select the pillars they will join, which could broaden membership in the overall framework while allowing like-minded countries to pursue high-standard outcomes. However, the limited participation approach could greatly reduce the commercial significance of the APEP to a small group of like-minded countries that have already undertaken similar commitments to existing FTAs.

Exclusion of market access. The decision of the US to exclude market access from the APEP will make it harder to achieve broad participation and high-standard commitments. In past trade agreements, the promise of duty-free access to the US market has been critical for securing commitments on labor, the environment, digital trade and other sensitive issues. Developing countries in Asia-Pacific are questioning the benefits of participation in the IPEF based on the same exclusion, and Latin American leaders are certain to follow suit. Though several countries in the region already enjoy preferential access to the US market through existing FTAs, these partners are unlikely to accept new trade obligations in the APEP absent clear and commensurate new benefits. The Biden administration has indicated that it intends to make development financing available to participating countries as an incentive for participation in the APEP. However, few details are currently available on how these financing commitments would operate, the types of entities and projects that would be eligible, the amount of funding the US would make available, and conditions that may be attached. It is unclear whether the promise of new development financing would provide a sufficient incentive for countries to undertake new trade commitments. It is not clear how development financing would encourage countries to participate in the APEP's trade pillar, since countries themselves choose the pillars in which they participate.

Enforceability and effectiveness. Market access commitments, which are excluded from the APEP, play an essential role in the enforcement of trade agreements: WTO and FTA dispute settlement mechanisms allow a complaining party to suspend market access concessions (typically by raising tariffs) where a dispute settlement panel finds that the respondent party has violated its obligations. Though the US intends for benefits other than market access, such as development financing, to attract participants to the APEP, such benefits are untested as a means of enforcing or encouraging compliance with trade commitments.

Durability of the APEP. The Biden administration does not intend to seek congressional approval of the APEP, instead treating it as an executive agreement. While this approach avoids the delays and challenges associated with securing congressional approval, it raises questions as to the durability of US support for the APEP. Congress and future administrations may feel less committed to an executive agreement than one that is approved through the legislative process that requires bipartisan support and codifies certain trade commitments into law. Some negotiating partners may therefore question whether the US will remain committed to the APEP in the long term.

Geopolitics. Given China's role as a major trading partner and source of investment in the region, many Latin American countries may wish to avoid the perception that the APEP is designed to counter or contain China, the region's major trading partner and investor. This may influence participation and the types of obligations that can be incorporated into the APEP, and may require flexibility on the part of the US.

The US business community, including the National Foreign Trade Council, has expressed hope that the APEP will include binding and commercially meaningful commitments in areas such as customs and trade facilitation and digital trade, promoting deeper economic integration in the region. Such commitments could provide important commercial benefits by allowing more efficient movement of goods across borders, facilitating the continued growth of electronic commerce, and enabling international data transfers that are critical for many services industries and, increasingly, for the manufacturing sector. For these outcomes to be possible, the US will need to make a compelling case that the arrangement offers tangible benefits to regional partners with varying levels of economic development, beginning with a clarification of the APEP’s objectives and concessions.

The administration may need to recalibrate certain expectations, including whether standards and enforcement mechanisms derived from the USMCA are achievable in the context of an agreement that lacks market access commitments. It will also need to work with partners to find creative solutions for dispute settlement and the legal architecture of the APEP. Until the obligations and benefits are clarified, many partners in the region are likely to view the APEP as a modest first step toward more formal and comprehensive trade arrangements, rather than a final destination.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: United States imports from Latin America and the Caribbean, 2002 – 2020 (PDF)

View full image: United States imports from Latin America and the Caribbean, 2002 – 2020 (PDF)

View full image: The Biden administration’s five pillars of the APEP (PDF)

View full image: The Biden administration’s five pillars of the APEP (PDF)

View full image: Regional Trade Agreements (RTAs), 1958 – 2022 (PDF)

View full image: Regional Trade Agreements (RTAs), 1958 – 2022 (PDF)

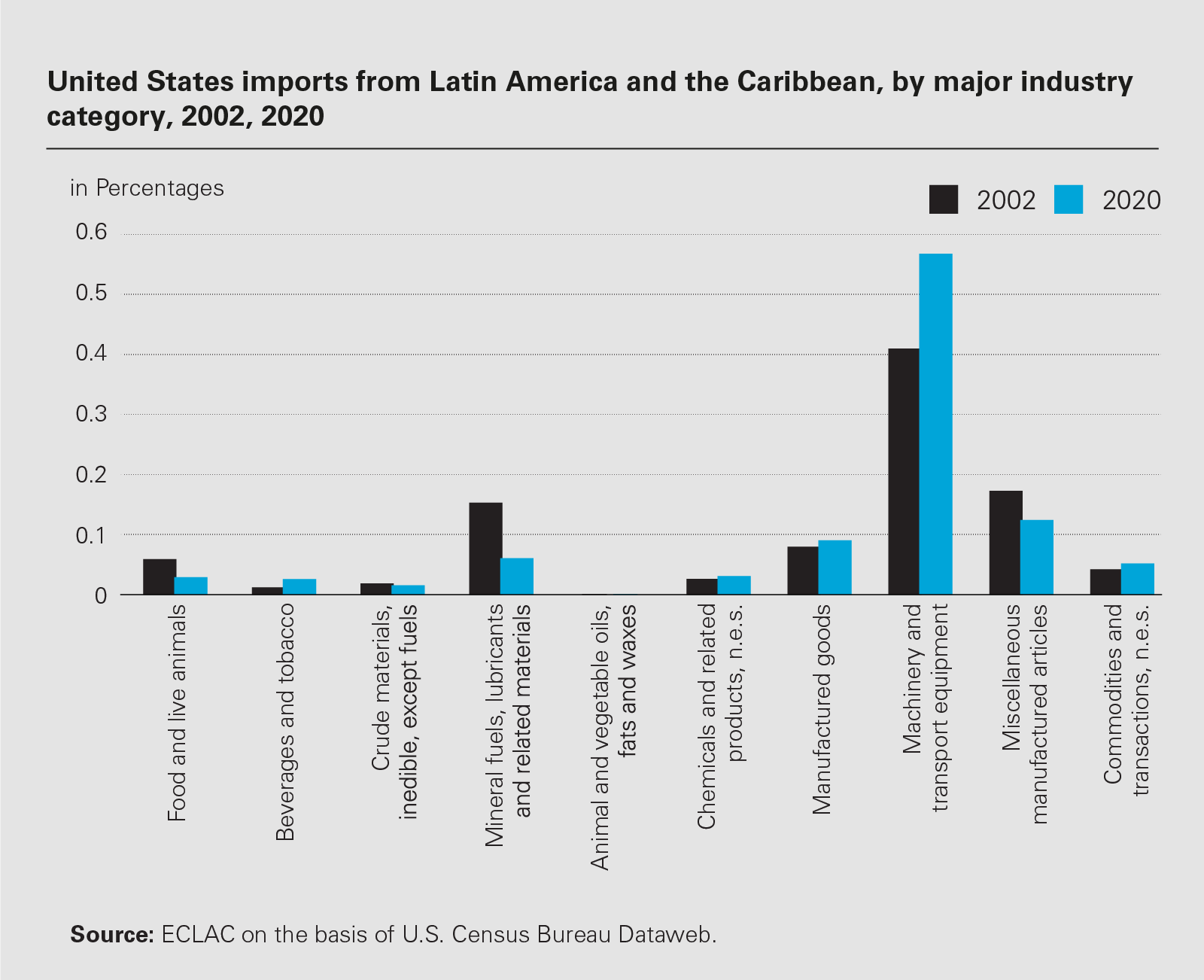

United States imports from Latin America and the Caribbean, by major industry category, 2002, 2020

United States imports from Latin America and the Caribbean, by major industry category, 2002, 2020