Partner, Latin America Group Leader and Editor of Latin America Focus

What a difference a year makes.

In our inaugural edition of Latin America Focus, produced by the Latin America Group at White & Case in the autumn of 2021, we offered scant good news. COVID-19 had thumped Latin American business harder than it had companies anywhere else, contracting Latin America's 2020 economies by nearly 7 percent, compared to a global average contraction of 3 percent. Latin America also was riding a rollercoaster of mounting populism and resource nationalism in 2021, and feeling the uncertainty that accompanies such trends.

Despite the then-present challenges, in that edition we highlighted a number of reasons to anticipate a LatAm resurgence in 2022, including an expected investment push into the region in certain sectors; the search for yields in emerging markets, commitments to mitigate climate change by global natural resources and energy companies; and the technology-driven push to digitize an increasingly global world economy.

How inspiring it has been to see most of this resurgence flower throughout the year since.

In this Fall 2022 edition of Latin America Focus, partners in our Latin America Group have written articles based on their personal experiences in the trenches and on market research that look forward to 2023 and together reveal the continuation—and perhaps acceleration—of many of the same global megatrends that propelled selective investment growth in the region in 2022.

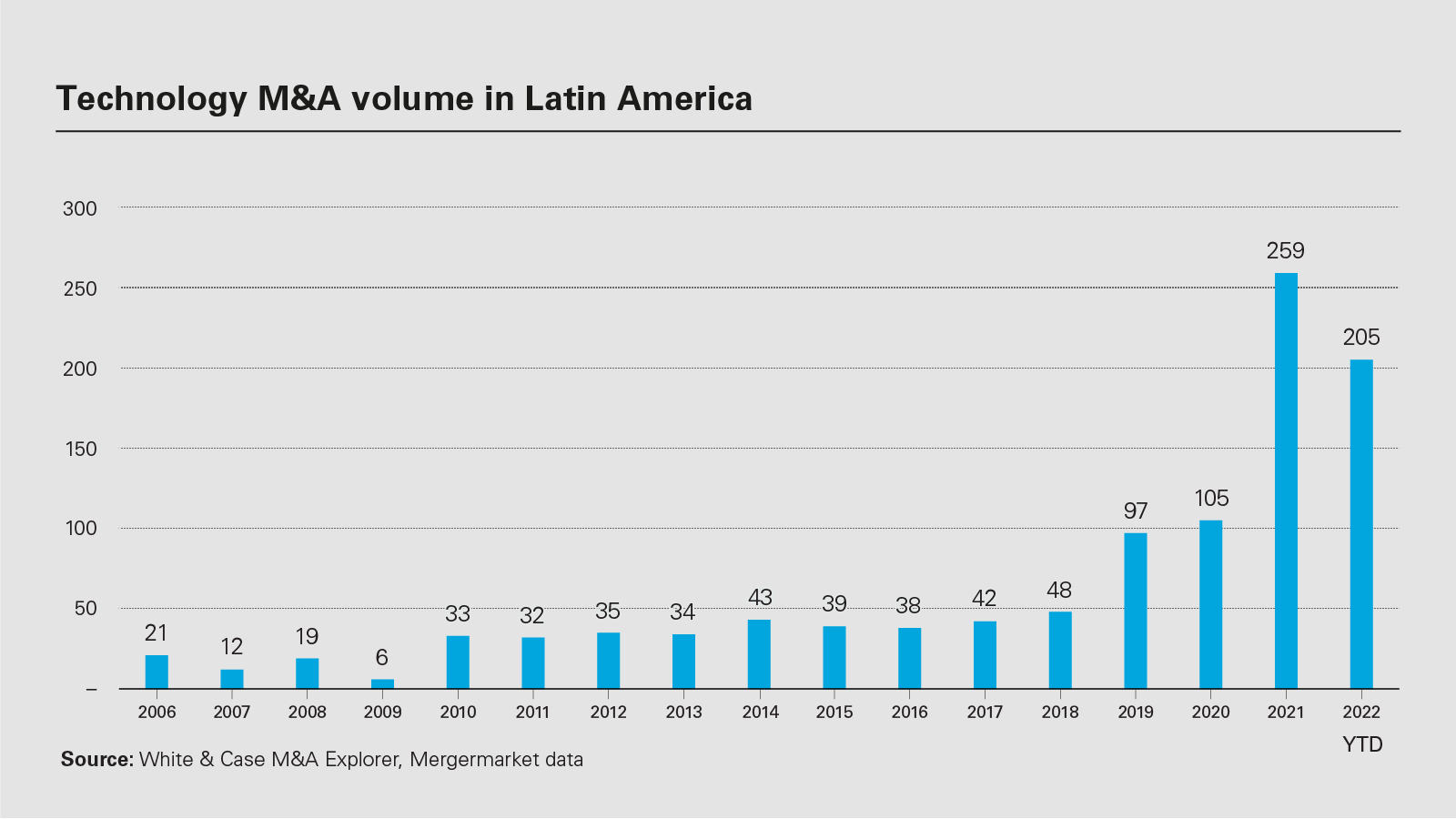

Chief among these megatrends is Latin America's forceful digitalization efforts. The region's large, young and habitually connected population, the current global financial equity investor liquidity and related resilient M&A activity and its booming fintech industry are effectively working together to position Latin America as a gigantic growth market for the tech sector over the next five years. In the tech hotbeds of Brazil, Chile, Colombia and Mexico, the number of tech startups has nearly tripled in the past five years, and across Latin America, technology transactions accounted for more than 40 percent of M&A deal value through the first half of 2022.

Not far behind the technology deal growth is the global energy transition; already Latin America's abundant wind and solar energy sources bolster its economy, attracting investment and creating new job opportunities. Still a major global player in oil & gas, the region looks well placed to emerge as a key global producer of green hydrogen. And as the energy transition picks up pace, carbon markets are starting to emerge across the region, teasing a future wherein Latin America stands as an innovative hub of carbon market activity and low-carbon development for the benefit of the entire world.

To be sure, challenges remain in both energy and tech: National hydrocarbons companies in the region, which account for a massive slice of hydrocarbon production there, continue to prioritize energy security over energy transition. Latin American countries (Brazil perhaps excepted) lag behind their North American and European counterparts on investment in digital infrastructure and addressing the digital divide between rich and poor. Despite the fintech boom, Latin Americans still have relatively little access to banking services and secure online payment gateways. Latin American countries also lag on developing intermediary liability frameworks and related consumer protections that offer security and certainty to digital platforms and their users.

The White & Case Latin America Group has produced this publication to provide market insights from our practical experiences and proprietary research that could be valuable to senior decision-makers eyeing the region for opportunities. I hope that you enjoy reading these insights and will contact us if there are any topics that you would like us to cover in future editions of Latin America Focus.

Latin America is closely aligned with global megatrends and 2023 will likely see the continuation—and perhaps even acceleration—of these trends in the region

Is Latin America the next frontier for technology M&A?

In a region suffering from global trade dislocations, inflation, higher interest rates and complex political cycles, dealmakers remain cautiously optimistic that the transition to digital services across the region will create significant M&A opportunities in the technology sector.

The future of US-Latin America trade relations: What can we achieve in the next few years?

From the Washington Consensus of the 1990s to the Biden administration's recently proposed Americas Partnership for Economic Prosperity, policymakers seem to have lost some of their ambition.

Is Latin America the next frontier for technology M&A?

In a region suffering from global trade dislocations, inflation, higher interest rates and complex political cycles, dealmakers remain cautiously optimistic that the transition to digital services across the region will create significant M&A opportunities in the technology sector.

Historically, transactional activity in Latin America has been driven by energy and infrastructure transactions. In the past two decades, the region experienced significant growth as most of its largest economies enjoyed political stability and adopted market-friendly policies that attracted significant foreign direct investment. Commodities played an important role in this growth. Latin America is home to some of the world's most abundant reserves of metals and minerals. The region also has vast reserves of oil & gas, which fueled major infrastructure investments throughout the region.

As a result, Latin America is more connected and prosperous than ever before.

Dealmakers watching the region will certainly remember the commodities boom in Brazil, the infrastructure and real estate frenzy in Mexico and Colombia, and the inflow of foreign direct investment that positioned Peru and Chile as dominant regional players.

In the past 20 years, these countries developed robust industries and attracted trillions of dollars in foreign investment while making strides to reduce poverty and expand access to infrastructure.

Broadening the scope of opportunities

Fast-forward to the 2020s, opportunities appear to be broader than energy and infrastructure, with technology becoming a critical part of economic growth in the region. Before the pandemic, Latin America was already on its way to becoming a hotbed for technology startups. Fueled by a rapidly expanding middle class and an influx of foreign investment, the region saw a boom in new businesses specializing in everything from e-commerce to digital media. The pandemic exacerbated this growth as consumers moved dramatically toward online and digital services. This surge of entrepreneurial activity was particularly evident in countries like Brazil, Chile, Colombia, and Mexico, where the number of tech startups has nearly tripled in the last five years.

In the first half of 2022, technology transactions in Latin America accounted for approximately 42 percent of regional deal value. As we continue to emerge from the COVID-19 pandemic, the technology sector is likely to experience high deal volume as new technologies and digital services continue to evolve into the region.

Why is Latin America an attractive region for technology investors?

US$5 billion

By 2021, fintech investments in the region totaled US$5 billion, up from US$2 billion in 2020

US$6.57 billion

In H1 2022, transactions in the telecommunications and media sectors amounted to an aggregate amount of US$ 6.57 billion

Source: Market data

What makes Latin America an attractive destination for technology investors? First and foremost, the region boasts a large and young population that is increasingly connected to the global economy. Secondly, many Latin American countries such as Mexico, Chile, Colombia and Brazil, have enacted favorable policies toward entrepreneurs, making it easier for new business to get off the ground. A loose economic policy around the world and access to cheap capital during 2020 and 2021 provided a significant boost to valuations, prompting an unprecedented uptick of M&A activity in this sector. The combination of low interest rates and a surging U.S. Dollar made it easier for U.S. investors to acquire or invest into Latin America targets at a faster pace.

With its vast potential for growth and innovation, Latin America is poised to become a major player on the technology landscape. For one, the region is home to a number of fast-growing tech companies that continue to be attractive acquisition targets for larger multinationals. Moreover, Latin America is an increasingly important market for many global tech companies, and acquiring local firms is a good way to gain a foothold in the region. Finally, many Latin American countries have been implementing legal reforms that make it easier for foreign companies to do business in this segment, which has also boosted M&A activity. As a result, it is no surprise that Latin America has emerged as a leading destination for tech startups and technology M&A activity, and is now one of the most active regions for tech M&A. This trend shows no signs of slowing down.

The fintech sector provides an excellent example. Banking services in the region have traditionally focused on conventional brick-and-mortar banking, which generally excludes a large portion of the population. Regional startups seized the opportunity to service this sector with impressive results by providing clever and disruptive solutions such as mobile payments, access to electronic payment platforms and micro-financing to the broader population. In 2018, fintech investments in the region hit a record high of US$2.5 billion, nearly double the 2017 figure. By 2021, fintech investments in the region totaled US$5 billion across 120 deals, up from US$2 billion and 82 deals in 2020. This growth was driven by a number of factors, including, at the macro level, low rates and a strong dollar, and at the country level the increasing availability of online banking and mobile payment services, the expanding middle class, and the region's young population. Fintech companies are also benefiting from supportive government policies in many countries.

With economies that are still largely cash-based, M&A activity in the fintech sector will remain strong in the years to come as investors seize opportunities to build up equity positions in great companies with an

enormous growth potential

As fintechs continue to proliferate in Latin America, they are significantly changing the way people manage their finances. From digital banks to peer-to-peer lending platforms, they are providing new and innovative solutions to meet the needs of Latin America's growing population. With economies that are still largely cash-based, we anticipate M&A activity in this sector to remain strong in the years to come. Financial and institutional investors will seize the opportunities to build up equity positions in great companies with an enormous growth potential, presumably at much lower valuations than just a few months ago, as a result of tightening of monetary policy. We also expect banks to engage in defensive M&A across the region to improve their technology platforms and serve a much younger demographic that is hungry for faster, better and cheaper banking services. At the very least, banks will seek to retain their market share and client base.

There is similarly growing demand for telecommunications and media sector services. Many companies in this sector have been looking to M&A opportunities to consolidate and expand their reach. The digital infrastructure and internet service provider segments are experiencing a high volume of M&A transactions by strategic and financial investors alike. The 2021 transactions involving AT&T, Telefonica and DirectTV are the clearest examples of dealmaking activity in this segment. According to public sources, there were 148 announced deals in the media sector in the first half 2022, for an aggregate amount of US$6.57 billion.

Consumer demand is driving strong M&A opportunities throughout the technology sector in Latin America. The shift to digitally enabled experiences and services is also stimulating investment across the different segments of the sector. The first half of 2022 saw a strong volume of growth capital, financing and M&A transactions, which provided significant amounts of fresh capital to some of the most successful technology companies in the region. This new trend has placed well-capitalized companies at the forefront of the M&A regional market, as they can now seek to deploy some of that capital through strategic M&A transactions at much more competitive valuations. High-quality startups are now better positioned for inorganic growth via M&A.

On the other hand, smaller or less-capitalized startups are having a harder time accessing fresh capital due to higher interest rates and stricter and more disciplined investment guidelines for private equity and venture capital funds. These less fortunate companies will likely become acquisition targets or seek for financing sources with tighter terms at much lower valuations, and in some cases, open the door for opportunistic and distressed M&A transactions.

In a regional market adapting to its new post-COVID-19 reality, which is shaped by global supply chain disruptions, inflation, higher interest rates, and new political cycles rethinking economic policies, dealmakers remain cautiously optimistic that the regional transition to digital services will create significant M&A opportunities, particularly in the technology sector. The current economic environment will create attractive opportunities for venture and private equity funds to pursue M&A through the remainder of 2022. Other well-funded startups that seek to remain competitive and keep up the growth rates demanded by their investors are also perceiving the opportunity and engaging in significant strategic M&A activity under less pressure and at more realistic and sustainable valuations. Stronger market participants certainly have the means to navigate current uncertainties, including the risk of an economic slowdown. M&A professionals remain vigilant for those opportunities as they explore this vibrant and exciting segment of the Latin America economy.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

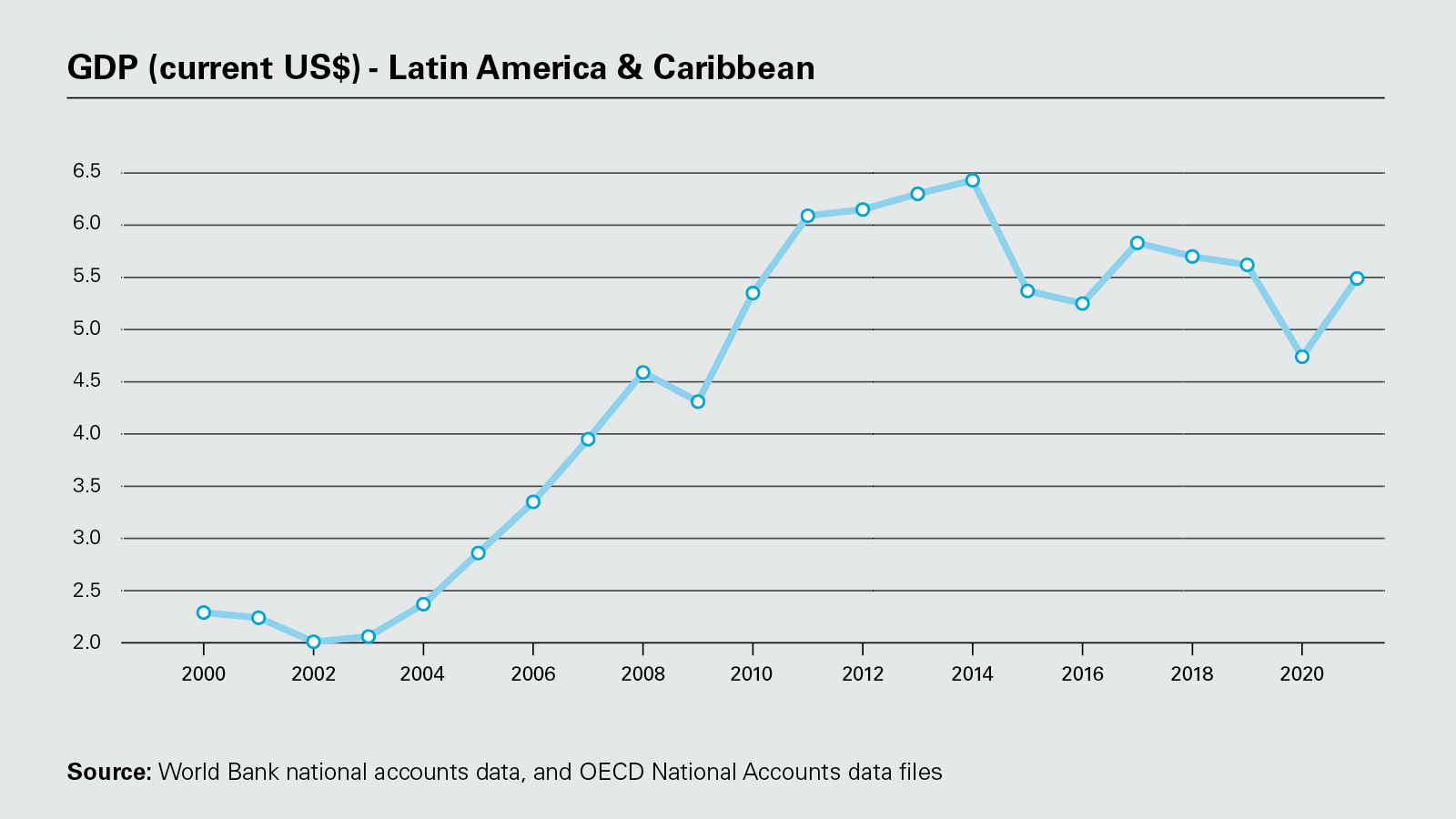

View full image: GDP (current US$) - Latin America & Caribbean (PDF)

View full image: GDP (current US$) - Latin America & Caribbean (PDF)

Technology M&A volume in Latin America

Technology M&A volume in Latin America

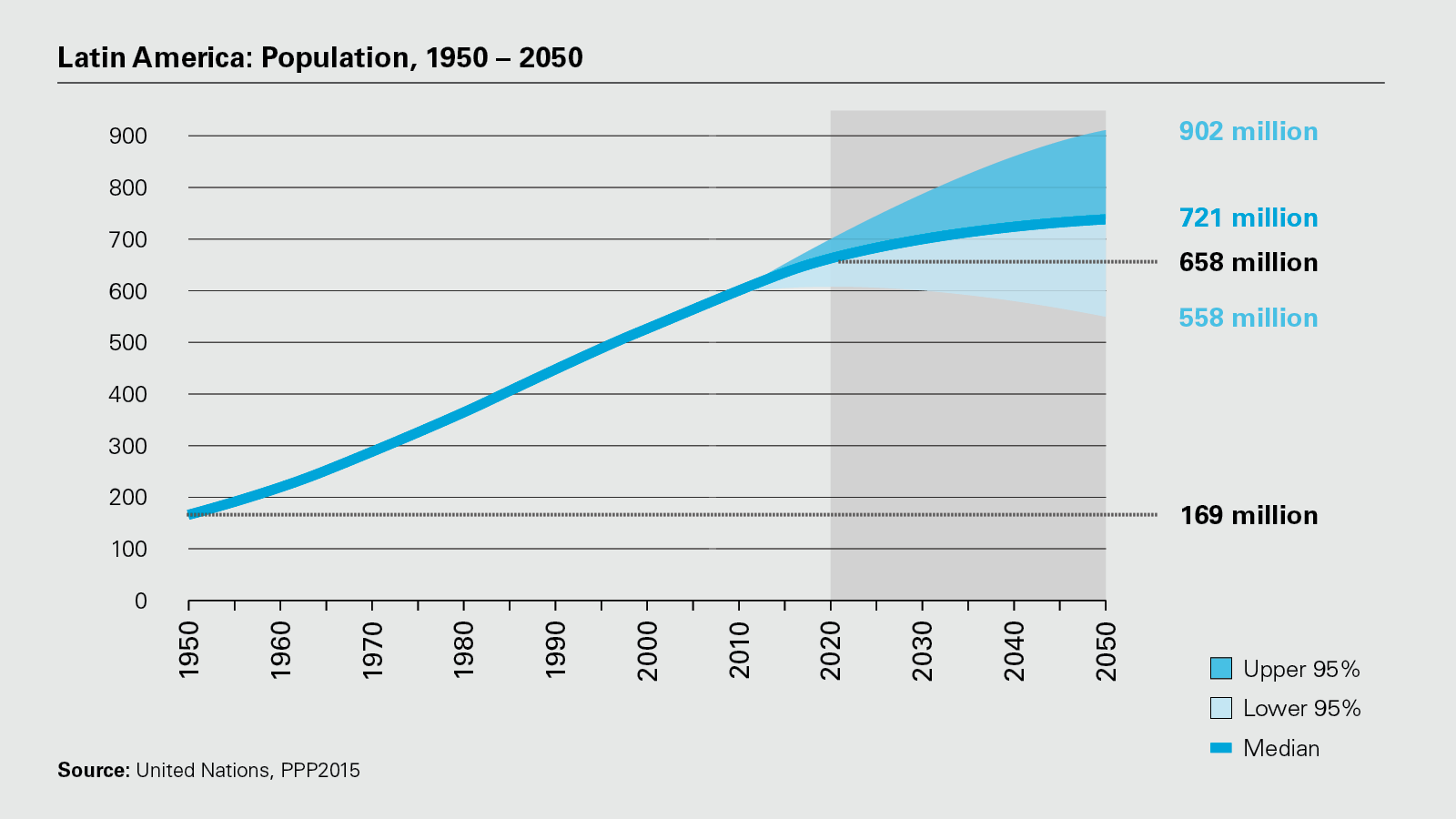

View full image: Latin America: Population, 1950 – 2050 (PDF)

View full image: Latin America: Population, 1950 – 2050 (PDF)