US infrastructure: Plans, progress and the path to growth

The global pandemic has not dampened enthusiasm for infrastructure investment in the US. Investors and developers are looking to increase their stakes in multiple sectors and states

The US infrastructure market is at a critical juncture. President Biden's approximately US$1 trillion plan for investment in key infrastructure asset classes has attracted bipartisan support. That paves the way for large-scale spending across the country, with investment in transport, energy and power, water and digital connectivity at the center of proposals that offer the prospect of fundamental transformation.

President Biden's plans reflect a twin imperative: to renew and modernize US infrastructure, but also to provide further stimulus to the US economy as the recovery from the COVID-19 pandemic continues. The combined effect could be an unprecedented boost for the US infrastructure market.

Against this backdrop, White & Case, in association with Acuris Studios, surveyed key US infrastructure market participants—the public authorities commissioning new projects and the investors, financiers and developers who will fund, deliver and manage them. Our survey results reflect on current market sentiment, identify the opportunities that participants are prioritizing and pinpoint the challenges.

Boosted by substantial support from the Biden administration and rising demand for infrastructure investment both in the US and internationally, our research reveals that the mood is upbeat with four main findings:

1. Growth industry

Respondents see the US as a land of opportunity. Their intentions are to grow not only their investments in US infrastructure, but also the size of their teams.

2. The COVID-19 effect

While the majority state that the pandemic had a negative effect on levels of investment in US infrastructure, it also prompted respondents to consider new practices including investing in a more diverse set of assets and improving digital technology.

3. Sector watch

While transportation (in particular, roads, tunnels and bridges) is seen as the key investment sector in 2022, social infrastructure has rocketed up the agenda due to the pandemic and the growing influence of environmental, social and governance (ESG) issues.

4. A connected future

Sustainability and technology are the watchwords for respondents when it comes to futureproofing their infrastructure investments.

In the third quarter of 2021, White & Case, in partnership with Acuris Studios, surveyed 85 senior-level investors that have, or plan to, develop/fund/invest in US infrastructure, and 15 public authorities that have awarded or plan to award a PDA, DBOM, DBFOM or lease for the development or replacement of US infrastructure.

Investors surveyed included infrastructure funds, pension funds, sovereign wealth funds, sponsors, developers, institutional investors and commercial banks.

The global pandemic has not dampened enthusiasm for infrastructure investment in the US. Investors and developers are looking to increase their stakes in multiple sectors and states

While the effects of COVID-19 were unsurprisingly largely negative, the pandemic did prompt most respondents to weigh new opportunities and ways of working

The pandemic has irreversibly hastened existing trends in the world of infrastructure. Digitalization, ESG considerations and climate change are no longer side issues, they are fundamentals

Respondents are broadly optimistic about the outlook for the US infrastructure sector, but there is no room for complacency. In this final chapter, we explore funding and future plans and reveal seven key factors for infrastructure success

Respondents are broadly optimistic about the outlook for the US infrastructure sector, but there is no room for complacency. In this final chapter, we explore funding and future plans and reveal seven key factors for infrastructure success

Stay current on your favorite topics

It is an exciting time for US infrastructure. Alongside the potential passage of President Biden's historic bill, our research indicates that investors, financiers and developers expect to step up their activity over the year to come—and public authorities are ready to return to projects that were delayed during the pandemic.

However, on a range of key issues, this optimism is more nuanced. The US infrastructure sector continues to grapple with a number of challenges as it plots its path toward recovery and renewal.

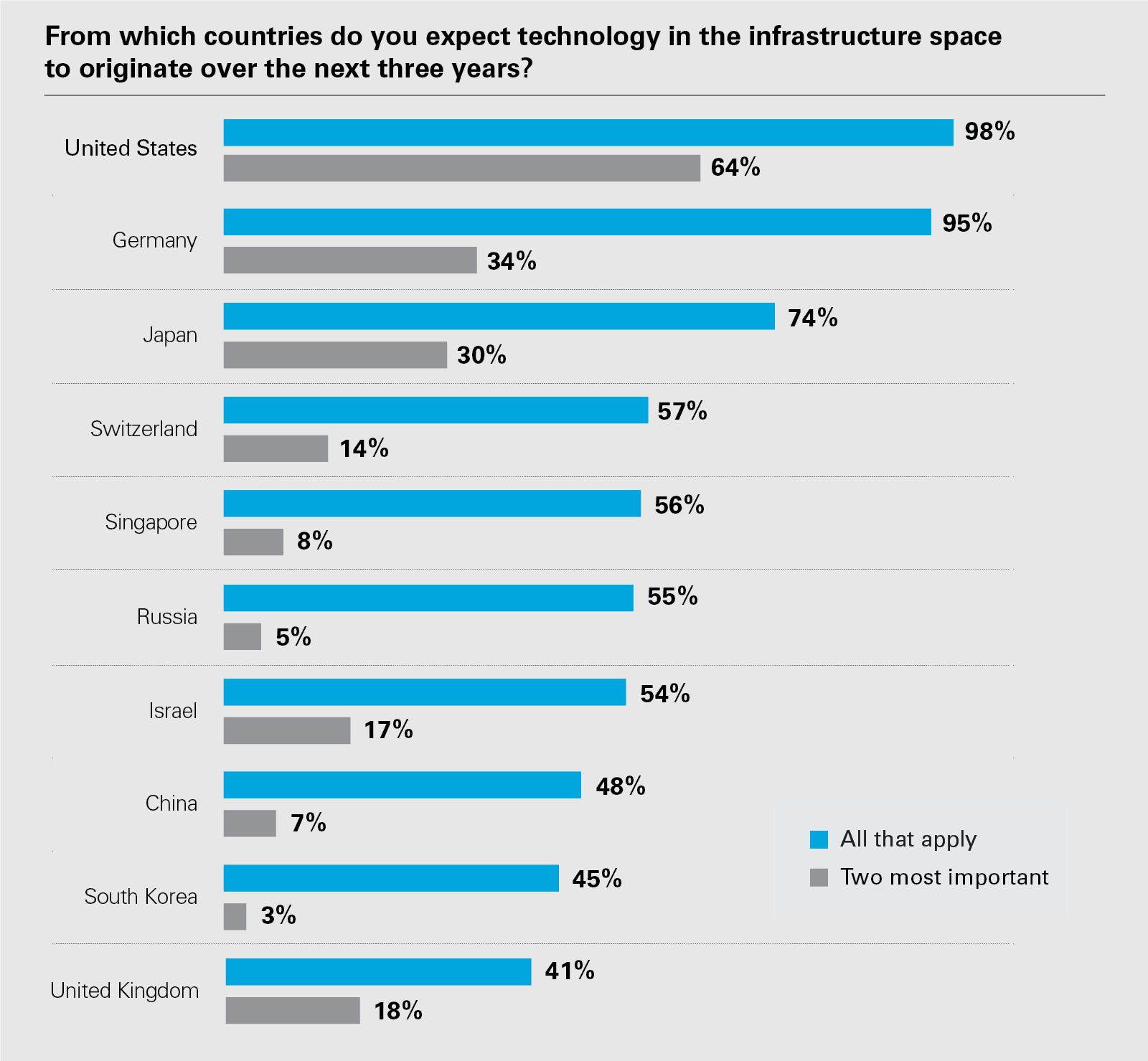

98%

of respondents believe US suppliers will be key providers of innovation and technology

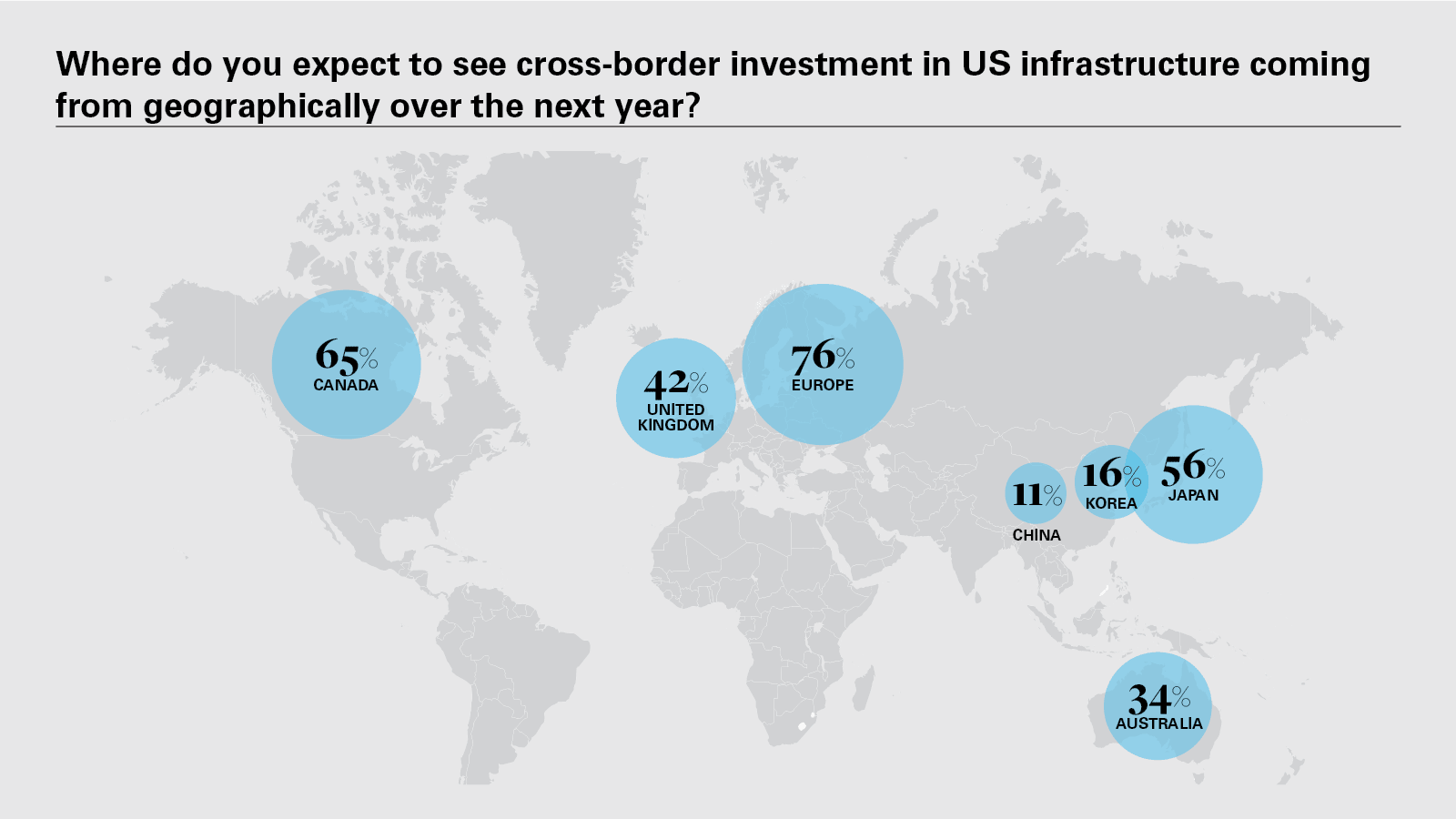

As chapter 1 revealed, while US-based respondents are largely prioritizing US infrastructure over the next 12 months, their non-US-based counterparts intend to allocate a more limited proportion of their portfolio to the US marketplace. Public authorities will hope to attract as broad a range of competitors for new projects as possible.

Europe (excluding the UK) is one likely source of that competition, our research shows. Three-quarters of respondents (76 percent) expect market participants from the region to be among the three most significant funders of US infrastructure projects over the next 12 months. Canada (65 percent) and Japan (56 percent) are also seen as important sources of funding for the US infrastructure market.

International partners can also be vital allies, as the imperative to integrate new technologies into infrastructure projects continues to increase. Almost all respondents (98 percent) believe US suppliers will be key providers of innovation and technology, but they also see partners in Germany (85 percent) and Japan (74 percent) as likely sources of the disruptive tools now required. Switzerland, Singapore, Russia and Israel are also regarded highly for their technological prowess.

86%

of public authorities surveyed agreed that P3s were the preferred way to deliver infrastructure projects

One aspect that may be hindering more foreign investors is the steep learning curve and the plurality of legal and operational obstacles that they need to overcome to access the US market. One key to overcoming these obstacles is to either partner with a US firm or work closely with local experts and to convince public authorities of their ability to get the job done, regardless of their country of origin.

Public authorities are keen on P3s, sending a clear message to investors that these types of partnerships are a solution to the infrastructure gap

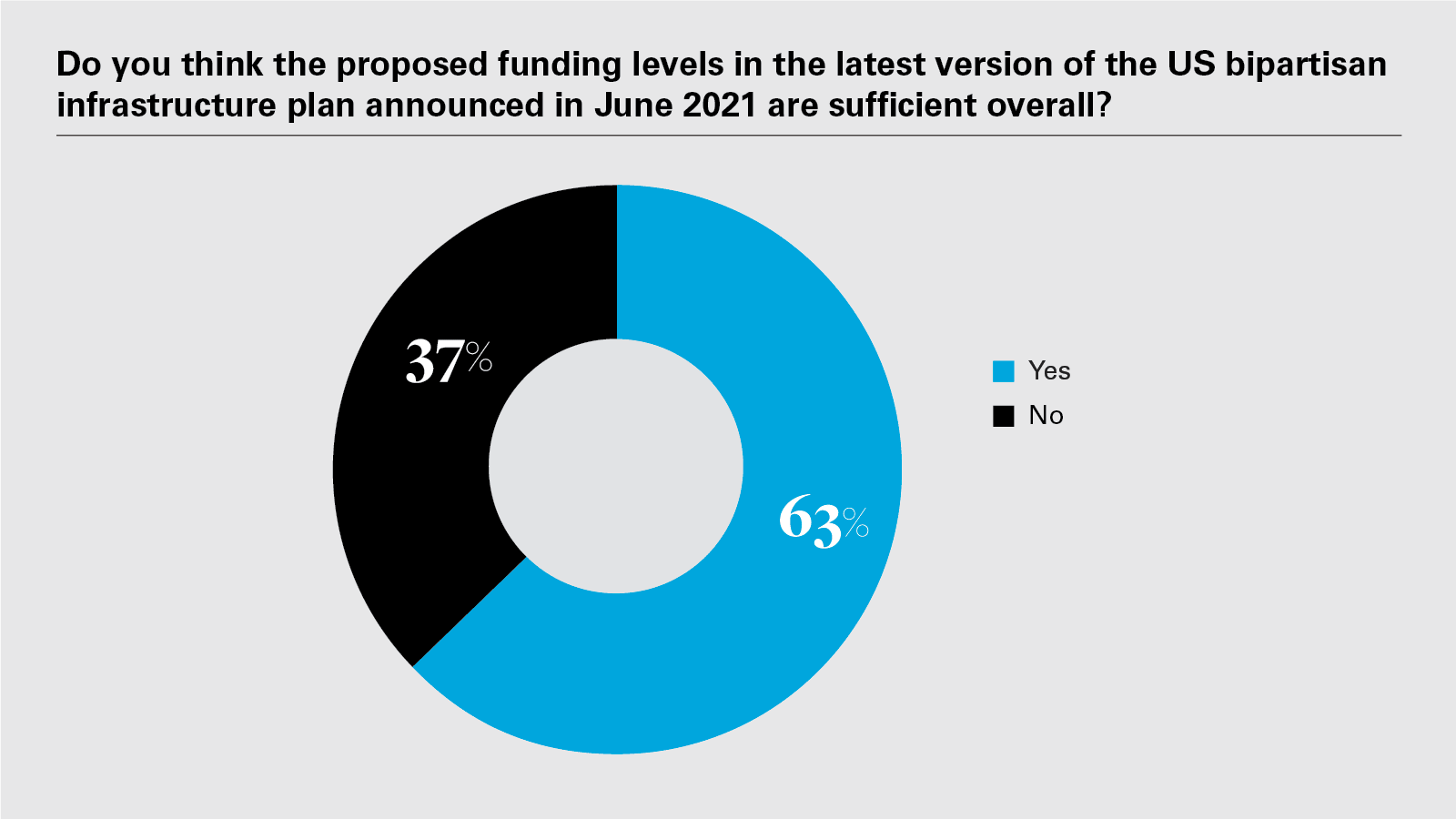

While two-thirds of respondents (63 percent) believe funding levels in the infrastructure bill are currently sufficient for the infrastructure sector's needs, that still leaves a great deal of room for partnerships and private financial investment.

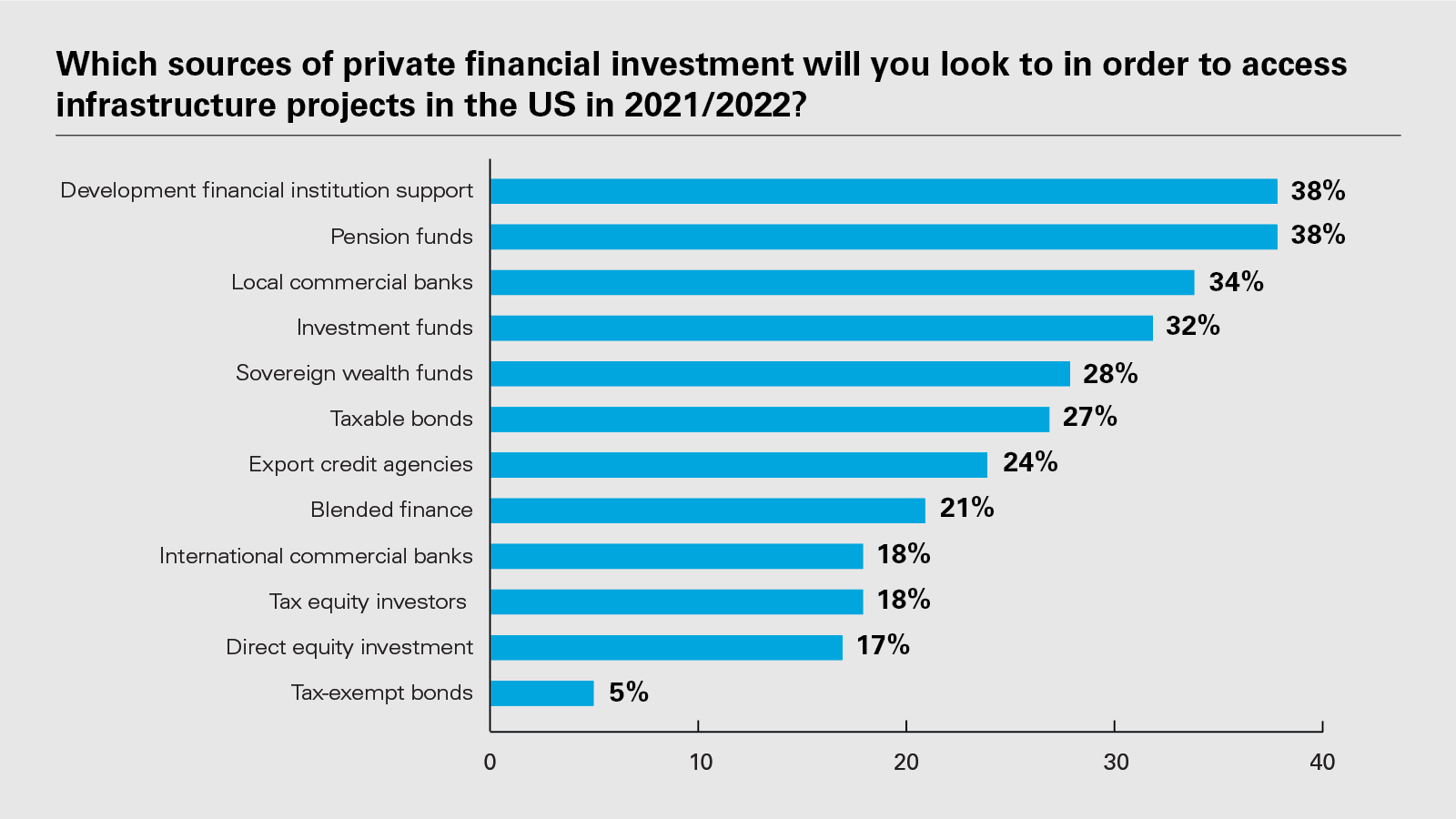

Among private finance sources, a broad range of support is available. However, pension funds and development-focused financial institutions are seen as the most likely targets for those seeking capital, with 38 percent of respondents citing each of these.

However, the key for private investment is to play a defining role in the deployment of capital. If capital from public sources is distributed around the country through traditional procurement, it will likely be seen as a wasted opportunity from a private capital perspective. Traditional procurement is usually focused on the design and construction rather than the long term maintenance profile, cost and optimization. If the focus fails to shift to include asset performance, customer service and quality standards, the country will likely find itself generating the same legacy problems of deferred maintenance that it is facing today.

Public authorities continue to focus on a variety of different delivery mechanisms for infrastructure projects. Encouragingly, more than three-quarters (77 percent) say public-private partnerships (P3) will be among their preferred options for infrastructure projects outside of the energy sector; 68 percent say the same of pre-development agreements (PDAs). Indeed, 71 percent believe that PDAs can increase the likelihood of a successful outcome for a project.

Our survey results show that the public authorities themselves are keen on P3s—of the public authorities we interviewed, 86 percent agreed that P3s were the preferred way to deliver infrastructure projects (no public authorities disagreed), sending a clear message to investors that these types of partnerships are a solution to the infrastructure gap.

And, while the infrastructure bill does not actively promote P3s, there are several sections that could prove beneficial. These include Section 70701, which would require a value for money analysis, which in turn would require public agencies to weigh the cost but also benefits of public versus private finance for projects. Meanwhile, Section 80403 would raise the cap on private activity bonds (PABs) for qualified highway and surface freight transfer facilities from US$15 billion to US$30 billion. PABs are tax-exempt bonds that enable lower interest rates for assets that have been developed and operated by the private sector.

Investors need to approach the different states and municipalities and work closely with them to ensure their goals are aligned.

The prospects for US infrastructure investment look bright. There is no doubt that COVID-19 has had a significant impact on the development and financing of infrastructure over the past 18 months, but the negative effects of the pandemic are now beginning to ease—and the sector is harnessing some elements of the disruption for positive benefit. Low-carbon projects, digital infrastructure and public health are good examples.

Many of the key themes that respondents highlighted as emerging over the next 12 months will come to reflect this new reality. Respondents point to the continuing rise of smart and digital infrastructure; further prioritization of renewable energy; environmental projects and broader ESG issues, and the importance of social infrastructure. They expect to see upgrades to road, rail and other transport networks, with an emphasis on technology and sustainability here too. And they see scope for increased investment and fundraising, including from the private equity sector.

US federal funding, proposed in the Biden administration's infrastructure plans, would result in an additional boost for the US infrastructure sector. Survey respondents point to seven factors that could make the infrastructure plan successful in delivering the necessary new upgrades and infrastructure to meet the future needs of the US population:

US infrastructure market participants are looking at a golden opportunity. Huge federal government spending should unlock the ability to do deals at the state and local level. The key is for both the public and private sectors not to waste that opportunity.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: Where do you expect to see cross-border investment in US infrastructure coming from geographically over the next year? (PDF)

View full image: Where do you expect to see cross-border investment in US infrastructure coming from geographically over the next year? (PDF)

View full image: From which countries do you expect technology in the infrastructure space to originate over the next three years? (PDF)

View full image: From which countries do you expect technology in the infrastructure space to originate over the next three years? (PDF)

View full image: Do you think the proposed funding levels in the latest version of the US bipartisan infrastructure plan announced in June 2021 are sufficient overall? (PDF)

View full image: Do you think the proposed funding levels in the latest version of the US bipartisan infrastructure plan announced in June 2021 are sufficient overall? (PDF)

View full image: Which sources of private financial investment will you look to in order to access infrastructure projects in the US in 2021/2022? (PDF)

View full image: Which sources of private financial investment will you look to in order to access infrastructure projects in the US in 2021/2022? (PDF)