US infrastructure: Plans, progress and the path to growth

The global pandemic has not dampened enthusiasm for infrastructure investment in the US. Investors and developers are looking to increase their stakes in multiple sectors and states

The US infrastructure market is at a critical juncture. President Biden's approximately US$1 trillion plan for investment in key infrastructure asset classes has attracted bipartisan support. That paves the way for large-scale spending across the country, with investment in transport, energy and power, water and digital connectivity at the center of proposals that offer the prospect of fundamental transformation.

President Biden's plans reflect a twin imperative: to renew and modernize US infrastructure, but also to provide further stimulus to the US economy as the recovery from the COVID-19 pandemic continues. The combined effect could be an unprecedented boost for the US infrastructure market.

Against this backdrop, White & Case, in association with Acuris Studios, surveyed key US infrastructure market participants—the public authorities commissioning new projects and the investors, financiers and developers who will fund, deliver and manage them. Our survey results reflect on current market sentiment, identify the opportunities that participants are prioritizing and pinpoint the challenges.

Boosted by substantial support from the Biden administration and rising demand for infrastructure investment both in the US and internationally, our research reveals that the mood is upbeat with four main findings:

1. Growth industry

Respondents see the US as a land of opportunity. Their intentions are to grow not only their investments in US infrastructure, but also the size of their teams.

2. The COVID-19 effect

While the majority state that the pandemic had a negative effect on levels of investment in US infrastructure, it also prompted respondents to consider new practices including investing in a more diverse set of assets and improving digital technology.

3. Sector watch

While transportation (in particular, roads, tunnels and bridges) is seen as the key investment sector in 2022, social infrastructure has rocketed up the agenda due to the pandemic and the growing influence of environmental, social and governance (ESG) issues.

4. A connected future

Sustainability and technology are the watchwords for respondents when it comes to futureproofing their infrastructure investments.

In the third quarter of 2021, White & Case, in partnership with Acuris Studios, surveyed 85 senior-level investors that have, or plan to, develop/fund/invest in US infrastructure, and 15 public authorities that have awarded or plan to award a PDA, DBOM, DBFOM or lease for the development or replacement of US infrastructure.

Investors surveyed included infrastructure funds, pension funds, sovereign wealth funds, sponsors, developers, institutional investors and commercial banks.

The global pandemic has not dampened enthusiasm for infrastructure investment in the US. Investors and developers are looking to increase their stakes in multiple sectors and states

While the effects of COVID-19 were unsurprisingly largely negative, the pandemic did prompt most respondents to weigh new opportunities and ways of working

The pandemic has irreversibly hastened existing trends in the world of infrastructure. Digitalization, ESG considerations and climate change are no longer side issues, they are fundamentals

Respondents are broadly optimistic about the outlook for the US infrastructure sector, but there is no room for complacency. In this final chapter, we explore funding and future plans and reveal seven key factors for infrastructure success

The global pandemic has not dampened enthusiasm for infrastructure investment in the US. Investors and developers are looking to increase their stakes in multiple sectors and states

Stay current on your favorite topics

Despite the volatility of the past 18 months, global infrastructure has continued to attract significant investment. US infrastructure in particular has been under the spotlight. President Biden's approximately US$1 trillion plan could be the stimulus for both the US economy and for private investment into the asset class. Research group S&P Global estimated that the bill could add US$1.4 trillion to the US economy over the next eight years.

US $1.4 trillion

Estimated sum the infrastructure bill could add to US economy in next 8 years

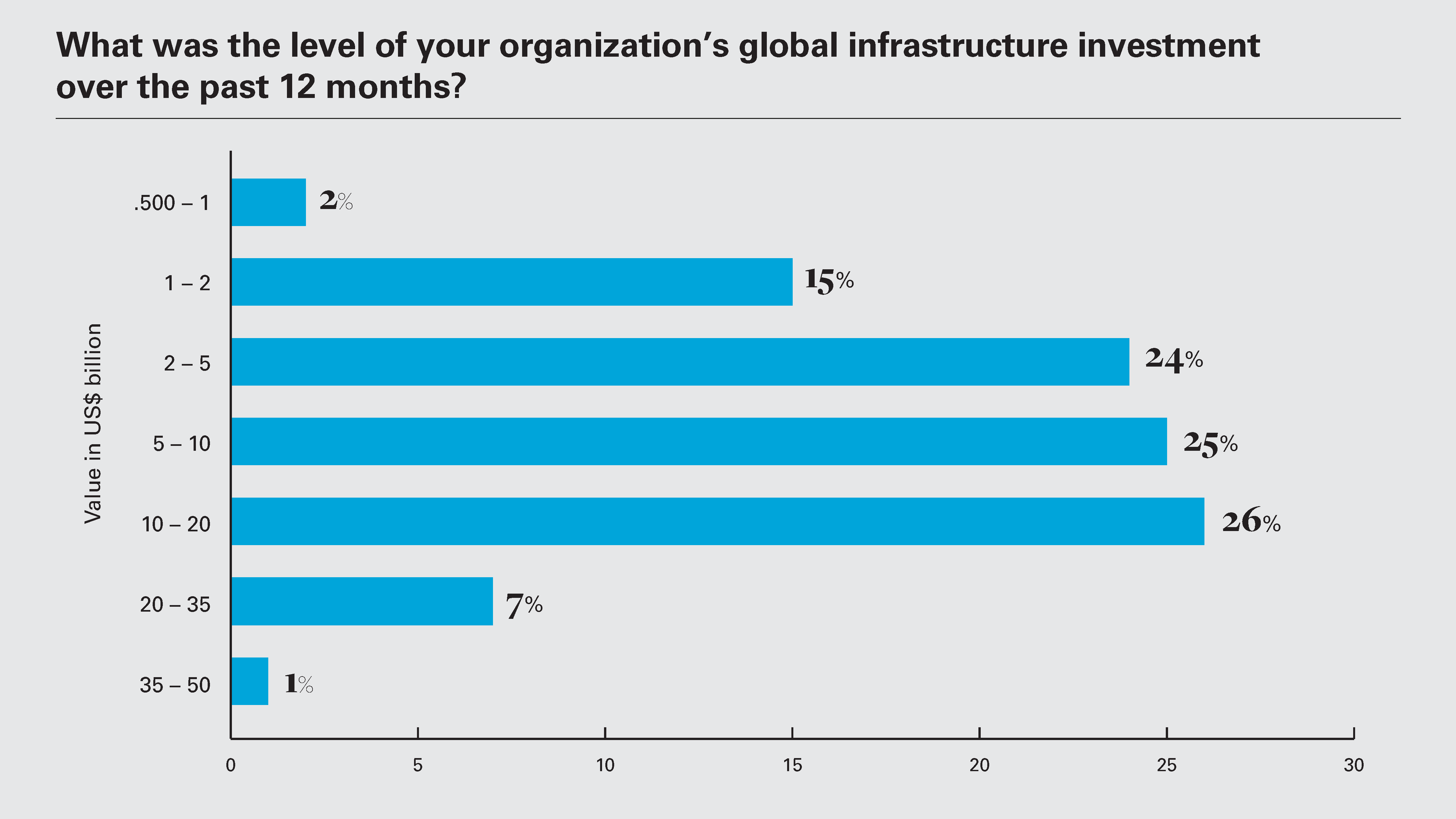

While the pandemic undermined confidence in certain asset classes, the long-term profile of infrastructure—and its more reliable income streams—has offered a safe haven. More than a third (34 percent) of investors, financiers and developers in our survey have invested US$10 billion or more in global infrastructure assets over the 12 months ending Q3 2021.

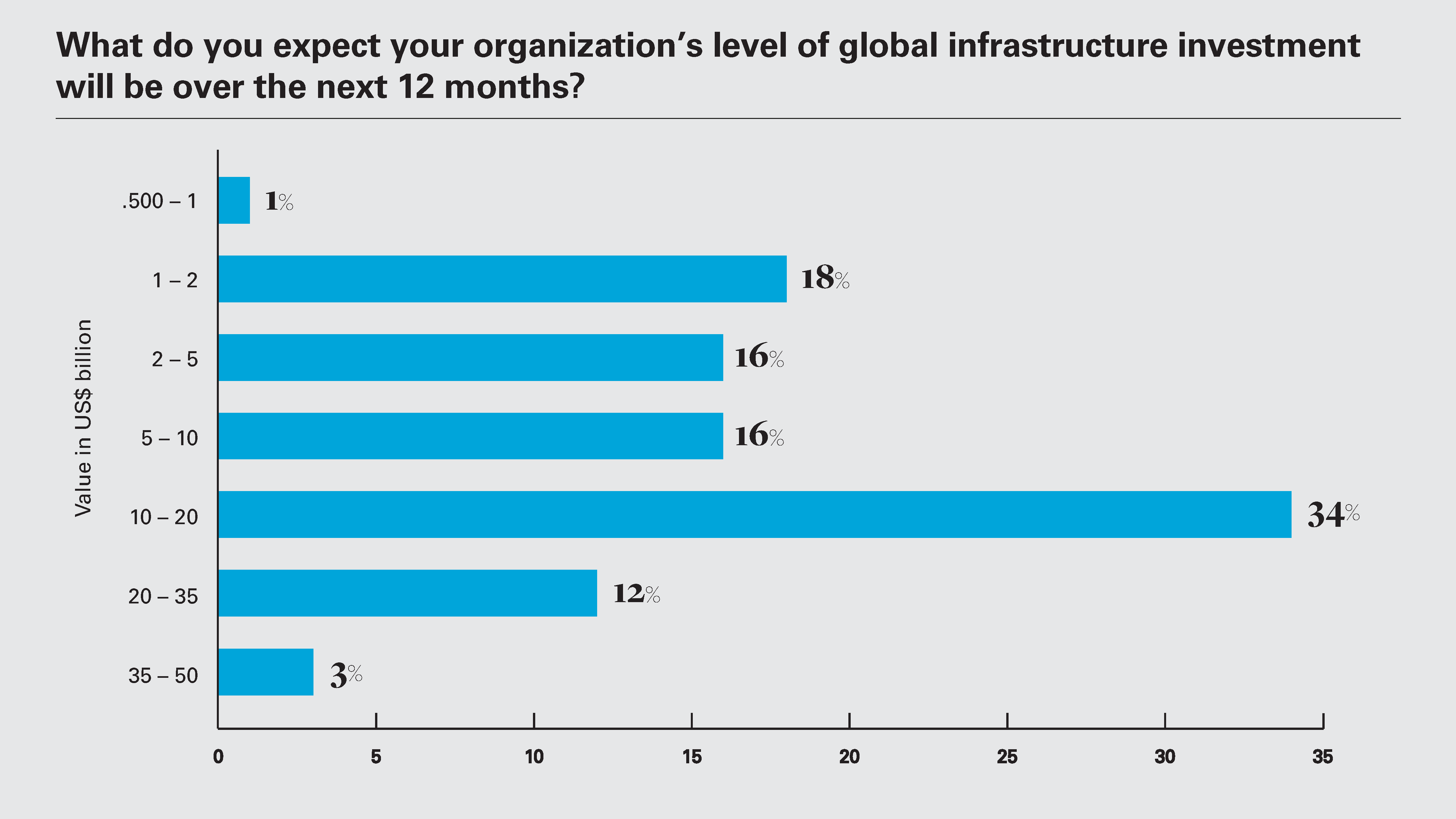

Moreover, investment now looks set to accelerate. Almost half of respondents (49 percent) expect to invest more than US$10 billion in global infrastructure over the 12 months to Q3 2022. That figure includes 15 percent who expect to make investments of more than US$20 billion in the asset class.

This acceleration may reflect both demand- and supply-side drivers. Certainly, as confidence returns in the wake of the pandemic, many investors, financiers and developers are likely to find it easier to make significant new commitments. But on the supply side, many of the public authorities surveyed are now considering whether to put delayed projects back on the agenda. Almost three-quarters (73 percent) of these respondents found it necessary to cancel the procurement of a project over the past year. As these projects are resurrected, the opportunities available to infrastructure investors will multiply.

There is also a drastic need for investment in the asset class. A 2021 report from the American Society of Civil Engineers (ASCE) stated that there is an "investment gap of US$2.6 trillion this decade, which could cost the country US$10 trillion in lost GDP by 2039." This necessity breeds opportunity—there is an array of sectors where good returns are available because the need for optimization is so great in the US. For investors willing to turn the dial on asset performance, the prospects are lucrative.

45%

of respondents are planning investments in New York state

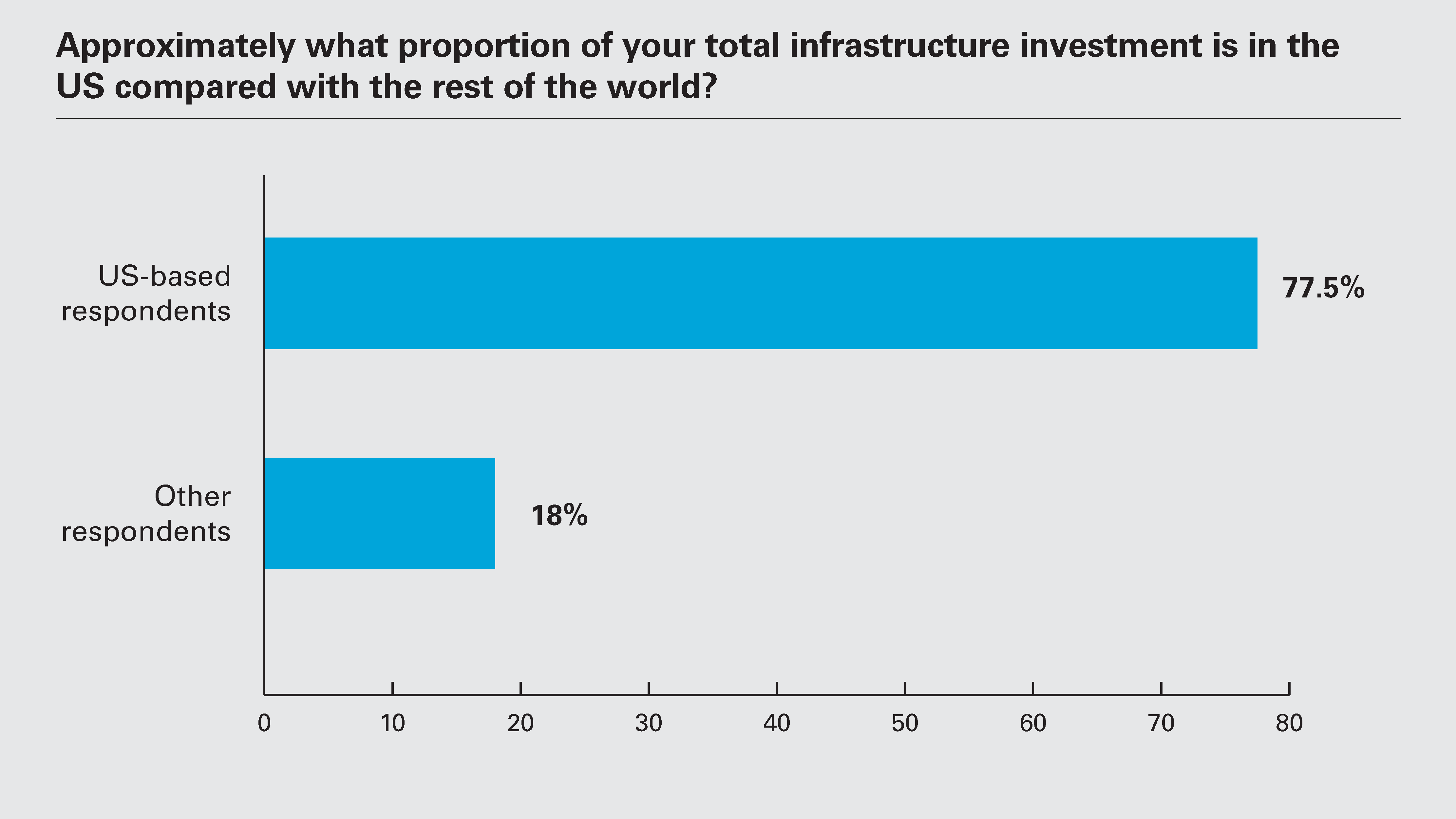

Respondents—both domestic and international—view the US as a key market for infrastructure investment. For US-based respondents, the home market is clearly the first port of call as they search for opportunities. On average, these firms hold more than three-quarters (77.5 percent) of their total infrastructure assets in the US.

However, while non-US firms understandably have higher allocations to global assets, their exposure to the US is significant, accounting, on average, for 18 percent of their infrastructure assets.

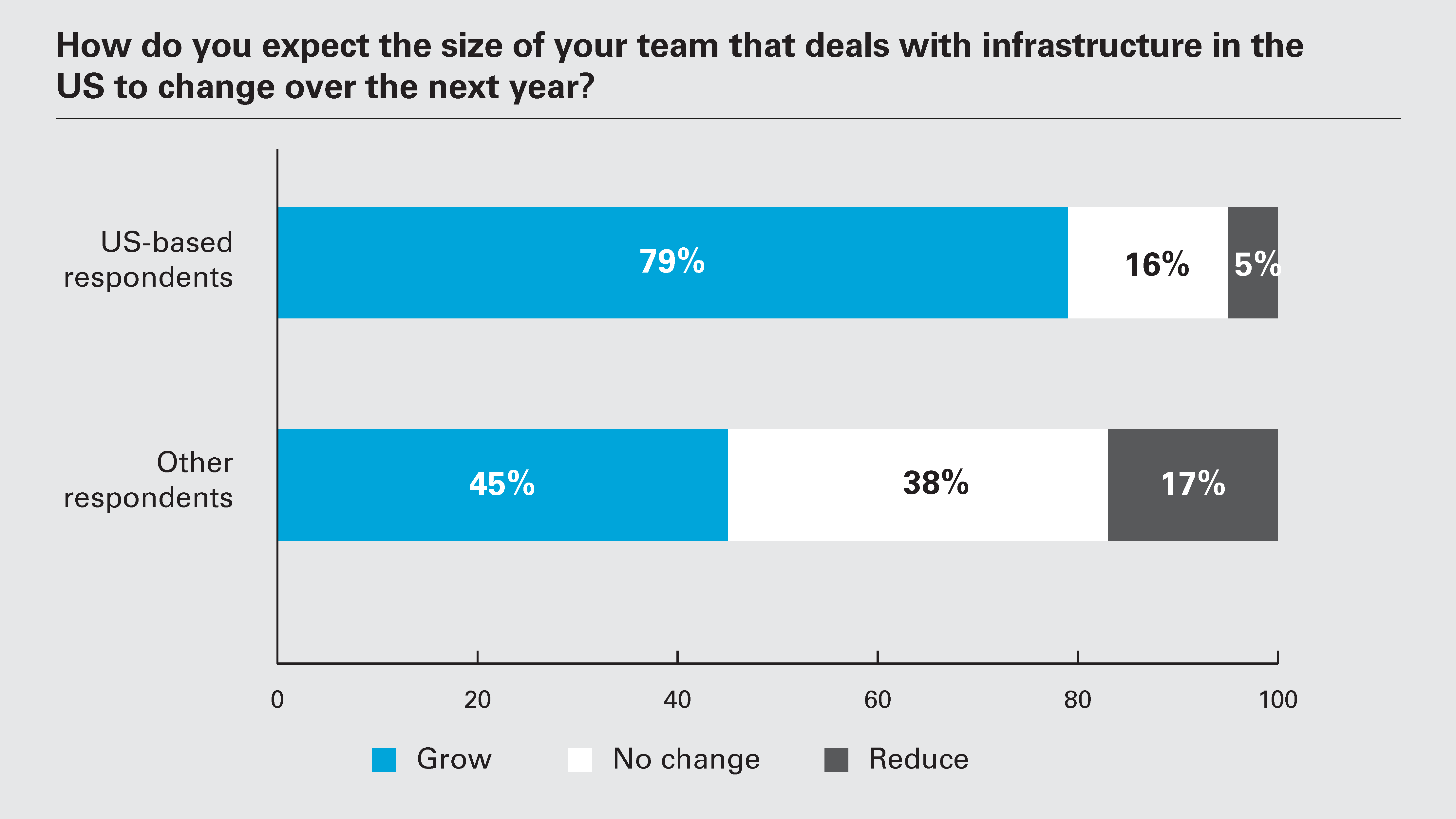

Moreover, many respondents, both US- and non-US-based, appear to be gearing up to expand their infrastructure investment resources in the country. Among the former, 79 percent expect their US infrastructure deal-focused teams to increase in size over the next 12 months; 45 percent of non-US respondents say the same (only 17 percent see teams reducing in size).

Clearly, many investors expect to sate their overall appetite for increased infrastructure exposure with a particular focus on US assets. Investors, financiers and developers can see the need for modernization given the legacy issues faced by the US infrastructure sector. A huge leveling up exercise is required to raise standards across a swath of subsectors, from airports and bridges to water and waste water, and these respondents are preparing to put more boots on the ground to deliver on that objective.

Spending on highways alone is not going to mitigate the underlying issues in the US. Healthcare and childcare support need to be increased

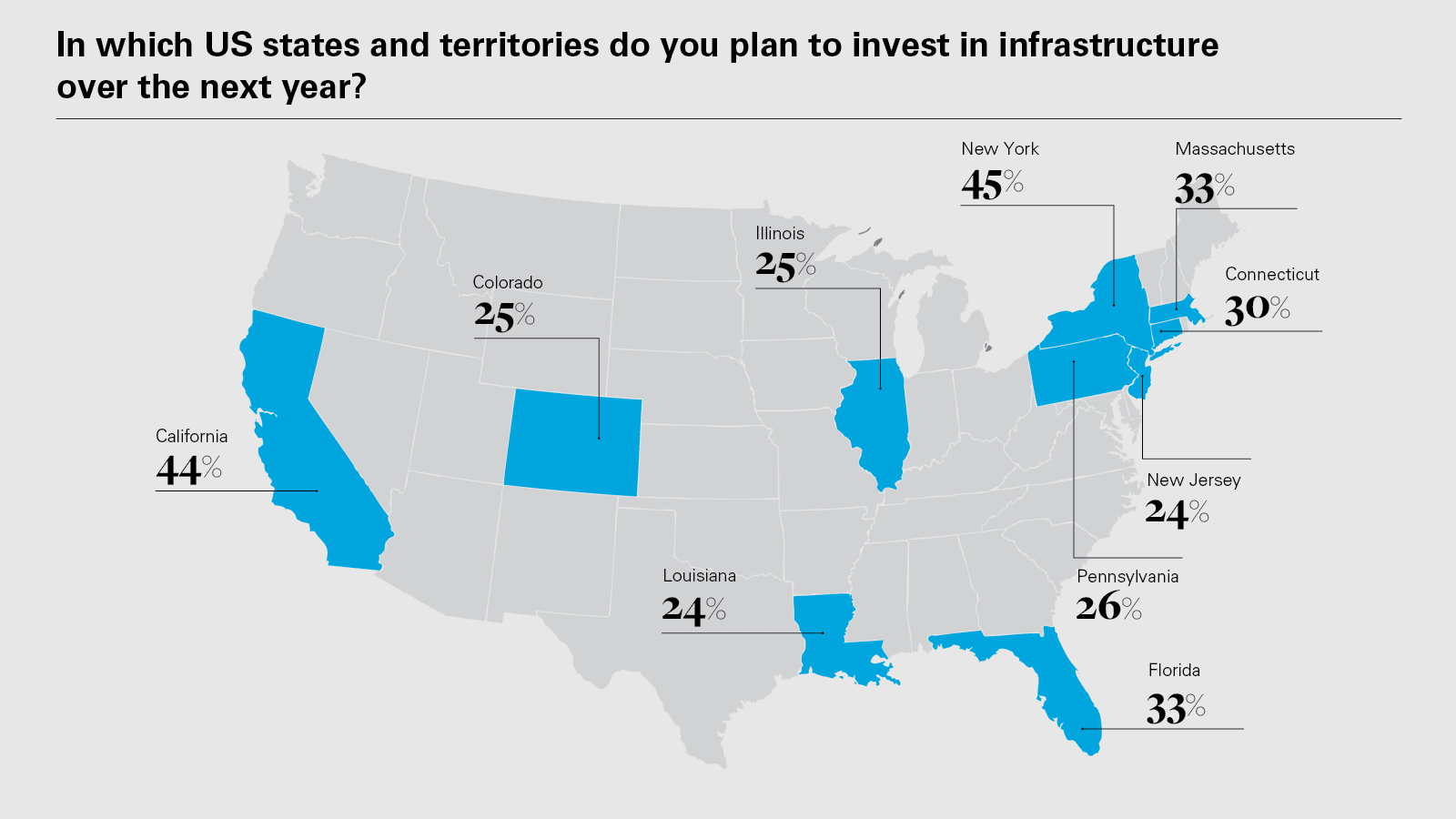

In terms of regional distribution, much of the infrastructure investment to come is expected by respondents to be focused on a handful of key states. New York (cited by 45 percent of respondents) and California (44 percent) rank one and two respectively as the states where respondents are planning investments over the coming year.

Given the high profile of these states, it is hardly surprising that they feature in the top two, but a look at this year's Infrastructure Report Card, compiled by the American Society of Civil Engineers (ASCE), demonstrates that both are in dire need. The report estimates that 9.9 percent of bridges in New York are structurally deficient, while the condition of California's roads is "among the worst in the nation, ranking 49th according to the latest US News and World Report Ranking." Florida—where 13 percent of roads are in sub-standard condition, according to the ASCE—is also attracting significant interest, with a third (33 percent) of respondents planning investments there over the next 12 months.

These investment intentions largely mirror respondents' views of which states offer the most attractive opportunities, with New York and California topping the survey here. Notably, Connecticut is seen as the third most attractive state for infrastructure investment over the next 12 months, climbing above Massachusetts and Florida.

"Infrastructure in New York is quite old and with so much emphasis on infrastructure development, things will now change for the better," says the head of infrastructure at one Asia-Pacific–based pension fund. Meanwhile, at a US commercial bank, the head of infrastructure argues: "California is going to see robust investment levels, with smart city and smart building development projects now under consideration, alongside plans for integrated renewable energy facilities."

The US is the largest and most influential economy in the world. You do get those competitive advantages when investing there

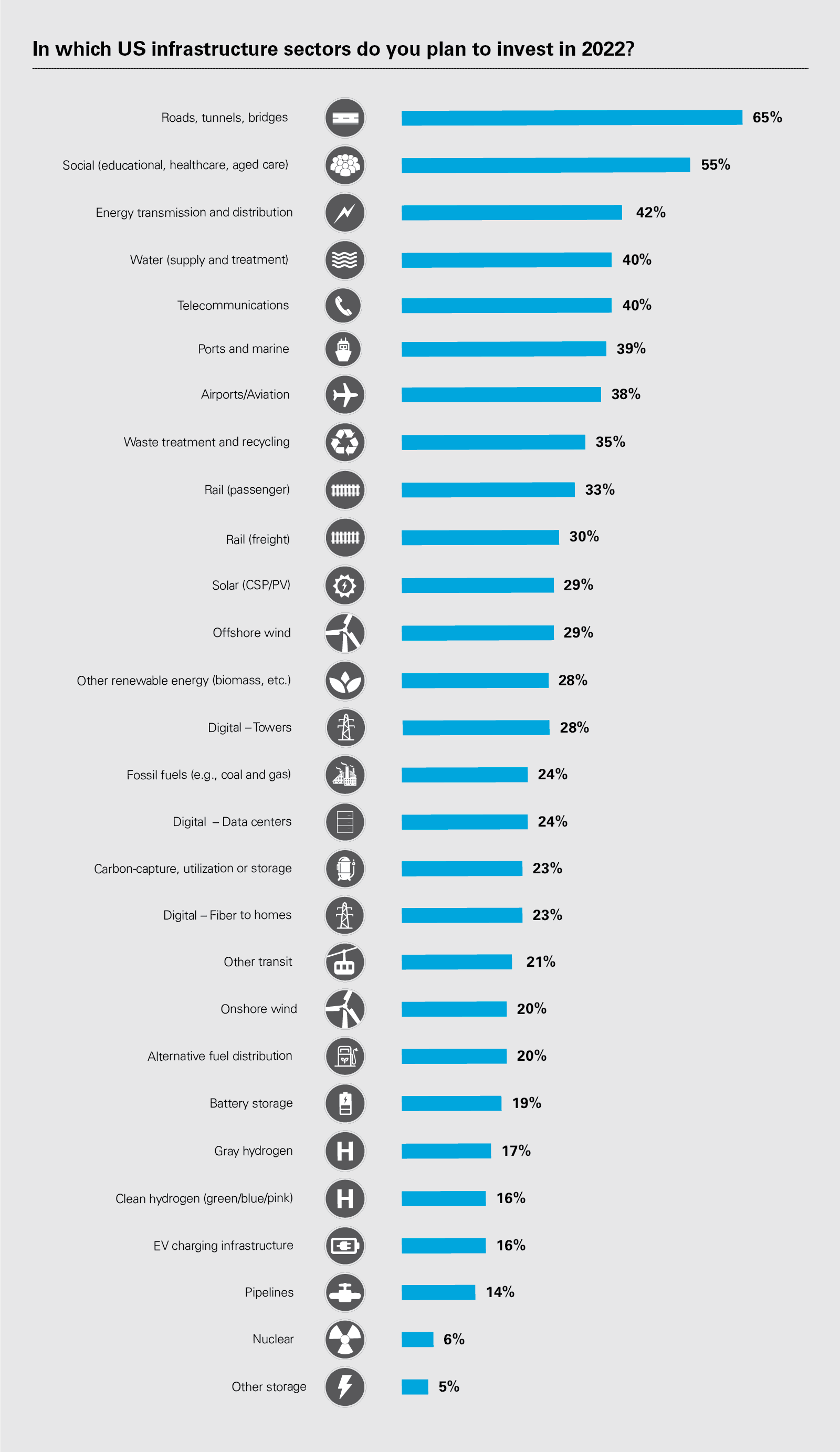

From a sectoral viewpoint, infrastructure investors are interested in a broad range of assets. Roads (and adjacent projects such as bridges and tunnels) are regarded as a standout area of opportunity, cited as a likely area of investment by almost two-thirds of investors (65 percent). Given that surface transportation has the biggest projected funding gap in the country, US$1.2 trillion according to ASCE, if public authorities focus on optimizing these assets with private sector expertise, there should be no lack of investment opportunities.

"The key theme [for the future of US infrastructure] will be the rebuilding of roads," says the head of energy and investment at a pension fund based in the Asia-Pacific region. "Compared to other countries, the US already has good connectivity. But it is important that the government continues to invest."

Many investors are also homing in on less "traditional" areas of the infrastructure market. Social assets such as healthcare facilities and elder-care facilities feature in the investment plans of 55 percent of respondents, for example.

Indeed, when asked which sectors should receive more funding, social needs featured heavily. The director of investment at a pension fund in the US says: "Spending on highways alone is not going to mitigate the underlying issues in the US. Healthcare and childcare support need to be increased."

The climate change agenda is also influencing many respondents' investment intentions, particularly in the context of green energy. Solar and offshore wind, for example, are both regarded as a priority by 29 percent of investors. And 23 percent intend to invest in carbon-capture assets that enable the energy industry to reduce the impact of its activities. For more on ESG and climate change, see A changing world.

One area in which respondents may lack a certain level of foresight is digital transformation. While a certain percentage of respondents do intend to invest in these assets—28 percent have plans for towers, for example, while 24 percent cite data centers and fiber to homes—traditional sectors are still gaining the lion's share of investment.

However, the pandemic provided definitive proof that the future is digital. If the US is to be at the forefront of digital transformation, then investment must keep pace with China, which is committing between US$1.5 and US$2.5 trillion over the next five years to "innovative infrastructure," according to an announcement by the Communist Party of China at the 2020 National People's Congress.

This is not to underestimate the desire for exposure to the digital economy. Many respondents point to the need for greater support for digital infrastructure.

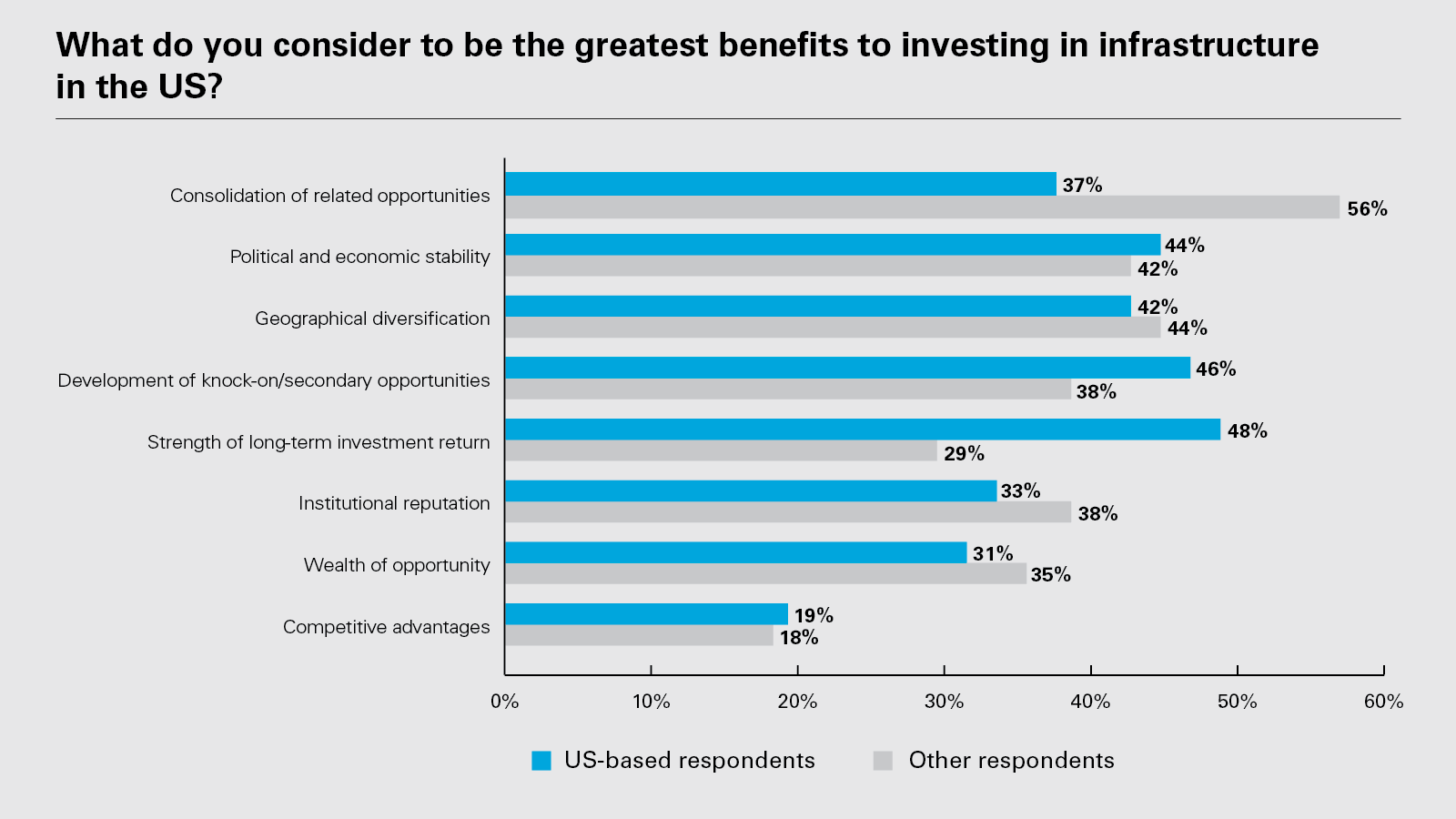

Meanwhile, respondents continue to identify key benefits of investing in US infrastructure. For those in the US, it is the strength of long-term returns (cited by 48 percent) that stands out, followed by the possibility of developing knock-on or secondary opportunities (46 percent). Indeed, investors are flooding infrastructure funds—according to research group Preqin, US$54.8 billion was raised globally for deals in H1 2021, with US$31.8 billion of that coming in the second quarter (an 88 percent increase on the same period a year earlier).

The political and economic stability that the US offers is also a key benefit. "US projects provide the long-term growth opportunities that other regions might be lacking," says the head of infrastructure at a US infrastructure fund. "The projects are managed well, are cost-effective and procurement is efficient."

Non-US-based respondents see the market slightly differently. More than half (56 percent) single out the possibility of consolidating related opportunities as they pursue infrastructure strategies in the US. With so much fragmentation in individual industries and across different sectors, there is a wealth of opportunities in the US market for those with the expertise.

Geographical diversification (44 percent) is the next key benefit for international investors, with US assets representing a foundation stone of their global portfolios. "The US is the largest and most influential economy in the world," says the director of infrastructure at a European investment fund. "You do get those competitive advantages when investing in the US."

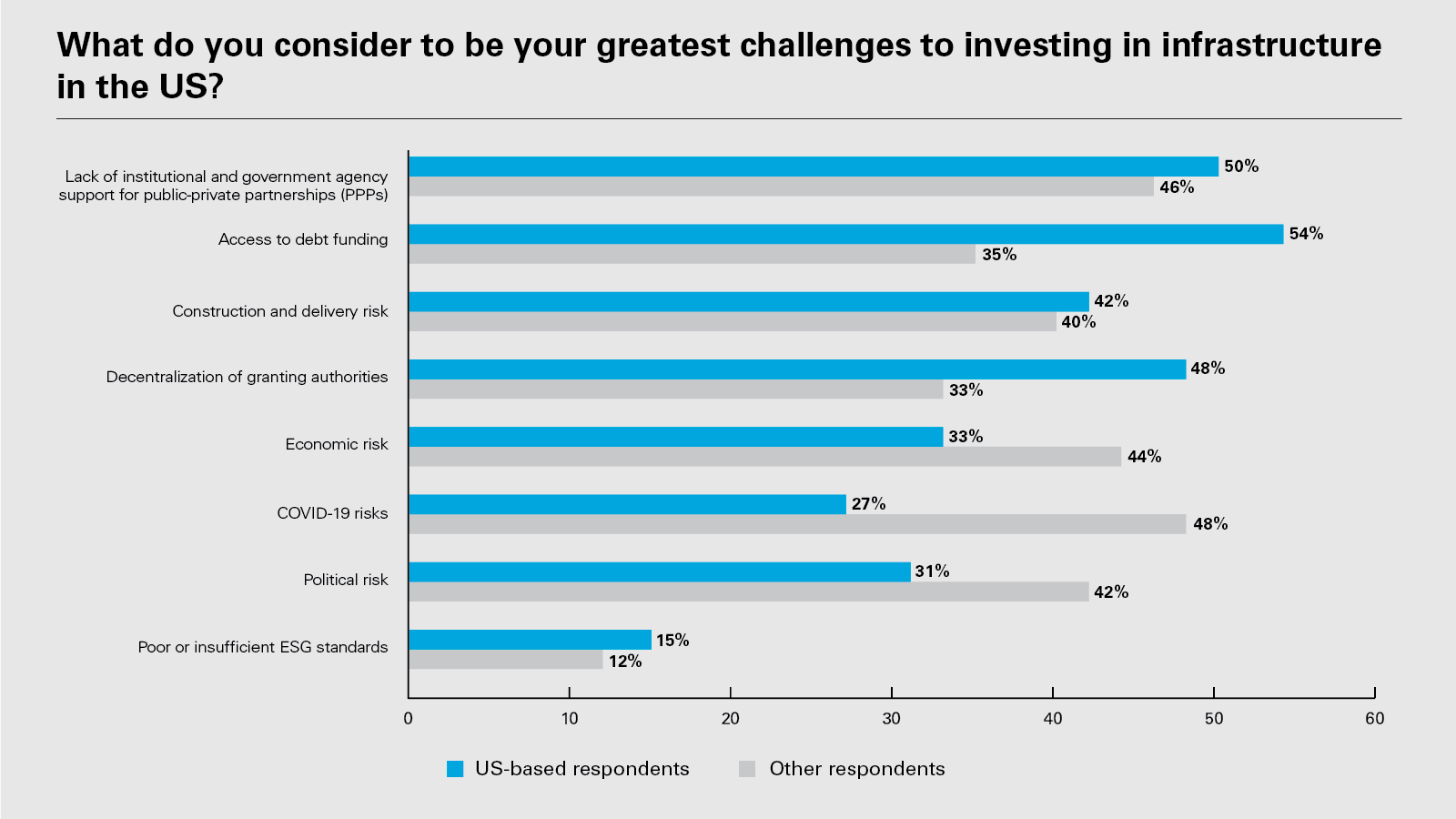

As for challenges, there are both similarities and differences between US-based respondents and their international counterparts. For example, both groups point to a perceived lack of institutional and governmental support for public-private partnerships (P3) as a key worry. Although, in many cases, this may be more a matter of perception than reality. While there have been some unsuccessful deals, many public authorities support the public-private model and expect to use it for future deals. For more on P3s, see Delivering the goods.

When it comes to differences, respondents from outside the US tend to be more worried about big-picture issues. For example, 48 percent of these respondents cite COVID-19 risks as a challenge as they consider US infrastructure investment; 44 percent cite economic risk.

This makes sense. For investors, financiers and developers on the ground in the US, it is the granular challenges of infrastructure investment that are now front of mind. Non-US-based respondents face these obstacles too, of course, but are also contemplating macro themes as they make decisions about international asset allocation.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image: What was the level of your organization’s global infrastructure investment over the past 12 months? (PDF)

View full image: What was the level of your organization’s global infrastructure investment over the past 12 months? (PDF)

View full image: What do you expect your organization’s level of global infrastructure investment will be over the next 12 months? (PDF)

View full image: What do you expect your organization’s level of global infrastructure investment will be over the next 12 months? (PDF)

View full image: Approximately what proportion of your total infrastructure investment is in the US compared with the rest of the world (PDF)

View full image: Approximately what proportion of your total infrastructure investment is in the US compared with the rest of the world (PDF)

View full image: How do you expect the size of your team that deals with infrastructure in the US to change over the next year? (PDF)

View full image: How do you expect the size of your team that deals with infrastructure in the US to change over the next year? (PDF)

View full image: In which US states and territories do you plan to invest in infrastructure over the next year? (PDF)

View full image: In which US states and territories do you plan to invest in infrastructure over the next year? (PDF)

View full image: In which US infrastructure sectors do you plan to invest in 2022? (PDF)

View full image: In which US infrastructure sectors do you plan to invest in 2022? (PDF)

View full image: What do you consider to be the greatest benefits to investing in infrastructure in the US? (PDF)

View full image: What do you consider to be the greatest benefits to investing in infrastructure in the US? (PDF)

View full image: What do you consider to be your greatest challenges to investing in infrastructure in the US? (PDF)

View full image: What do you consider to be your greatest challenges to investing in infrastructure in the US? (PDF)