The EU Commission’s fifth annual FDI report: Significant scrutiny in ever more member states

7 min read

On 14 October, the European Commission (EC) issued its Fifth Annual Report on FDI screening in the Union providing an overview of FDI trends in the 27 EU Member States in 2024. The findings are much in line with the previous Annual Report showing a march towards wider and more frequent scrutiny, the introduction of more screening regimes, the expansion of existing schemes, and a significant number of transactions subject to screening by Member States.

FDI in the EU: the Investment Environment

Statistics first: Total FDI transactions, including both greenfield and M&A investments, are down by 8.4% compared to 2023, which was itself a 23% decrease from 2022. However, this is largely driven by a decrease in greenfield projects. While the number of M&A FDI deals increased slightly (by around 2.7% in 2024), greenfield FDI investments were down 19%. In terms of investor origin, the US retains its status as the top foreign investor in the EU, accounting for around 30% of acquisitions, followed by the UK. Investments from China and Hong Kong saw a notable recovery in 2024, with M&A transactions up 23% from 2023 (which had seen a decline of nearly 20% from 2022).

FDI Screening by the Member States

The EC's Annual Report, now in its fifth year, amalgamates data reported by all 27 Member States on the operations of their national FDI regimes over the previous 12 months. It reports that, across the Union, 3,136 transactions were reviewed by Member States' national FDI authorities, either via notification or because of a call-in review by a national authority.

41% of these transactions were subject to 'formal screening', with around 59% not requiring formal screening or otherwise being deemed ineligible. These 2024 figures, however, are "strongly influenced" by Sweden, which implemented the (very broad) Swedish FDI Act in 2024. This apparently resulted in a very significant number of "irrelevant" transactions being reported in Sweden due to the lack of formal guidance. Excluding the Swedish statistics would change the percentages to 67% of cases requiring formal screening, and 33% being excluded. For more information on the operation of the Swedish FDI Act please see our dedicated overview here.

Screening Outcomes

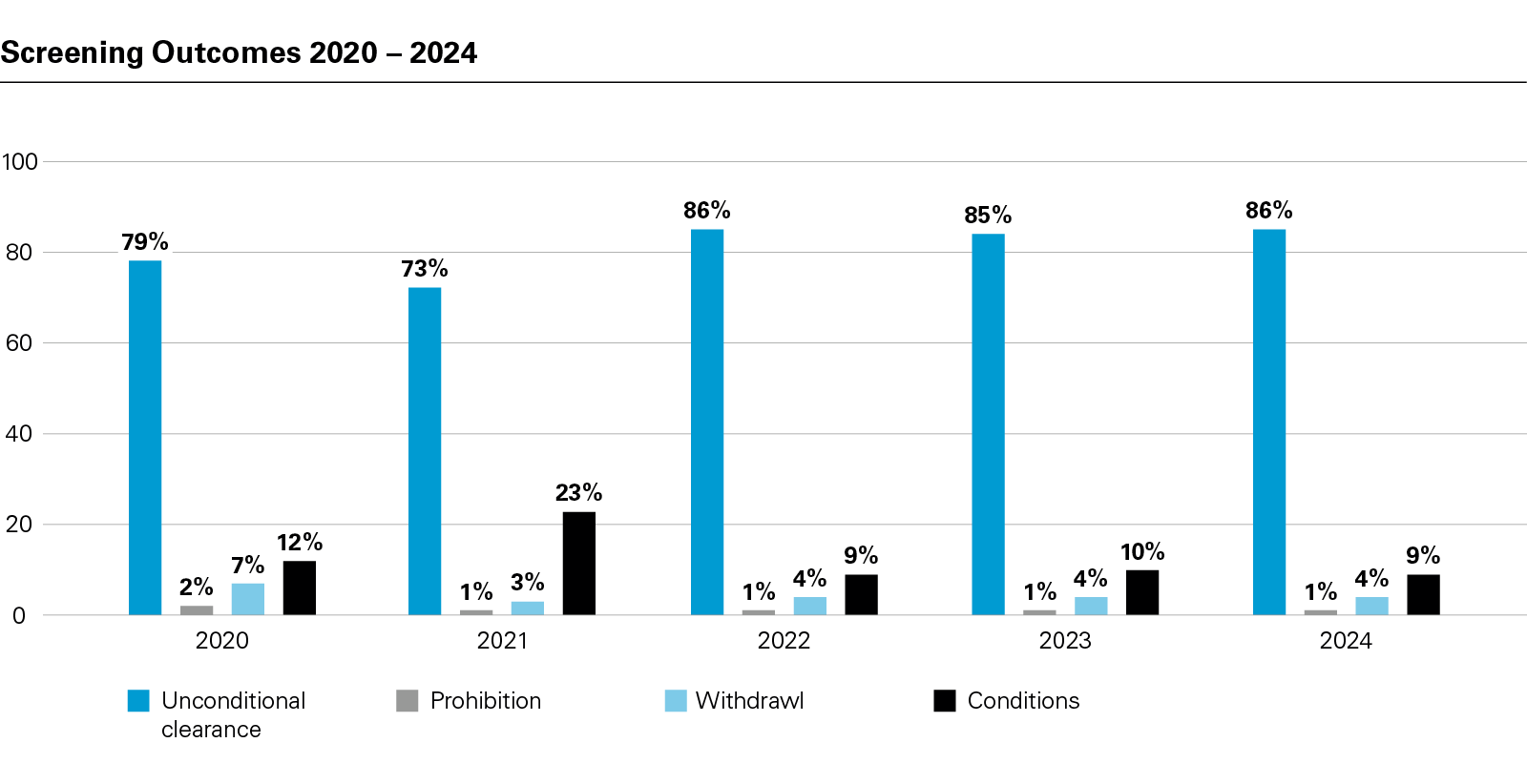

Overall, the statistics show that the EU remains open to foreign investment, with interventions remaining an exception. Of all the transactions that were formally screened:

- 86% were cleared unconditionally;

- 9% were subject to conditions;

- 4% were withdrawn; and

- 1% were subject to prohibition.

Measured against the respective number of cases reviewed, screening outcomes have remained fairly consistent over the last three years, as set out below.

View full image: Screening Outcomes 2020 - 2024 (PDF)

View full image: Screening Outcomes 2020 - 2024 (PDF)

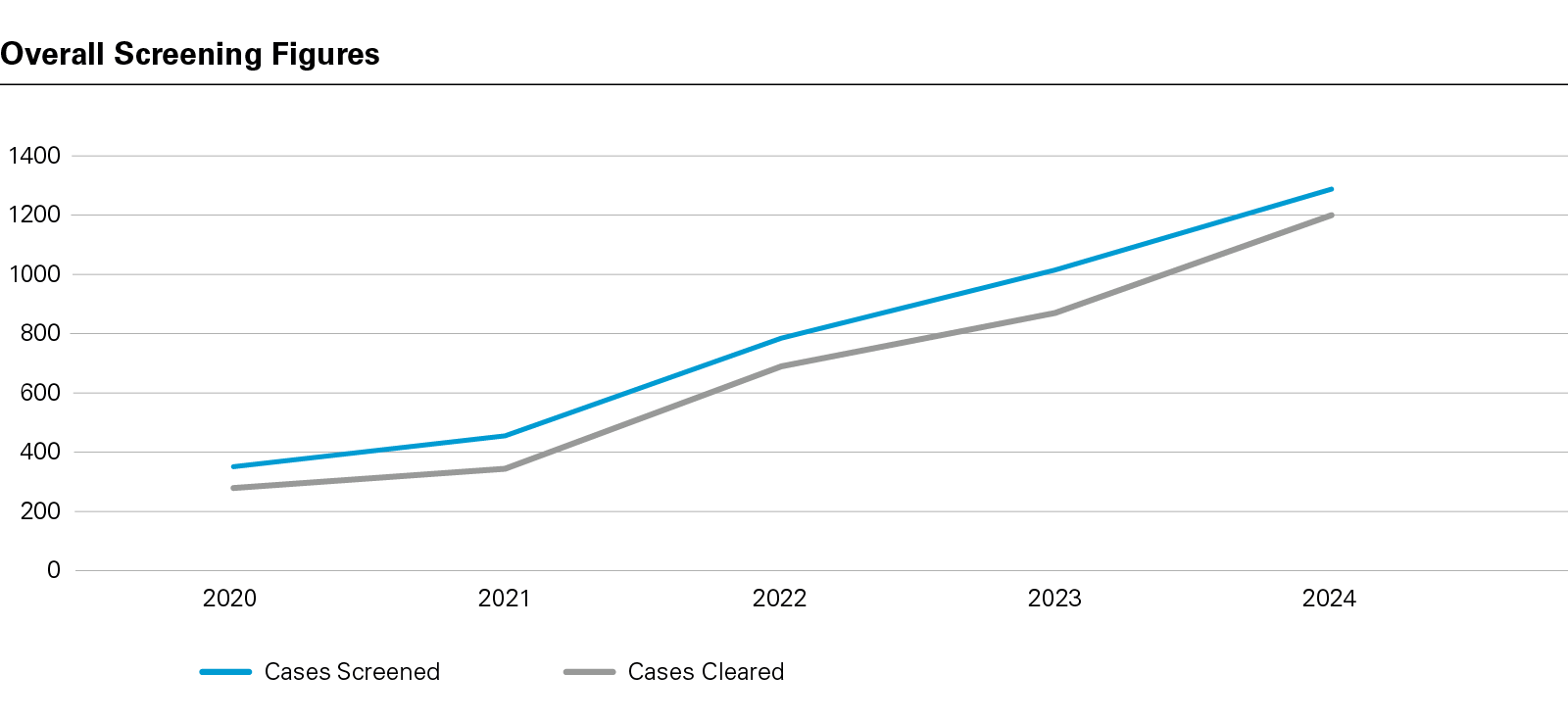

However, as more regimes proliferate and the scope of existing regimes expands, the numbers of deals falling into each category have increased significantly. Since 2020, the number of cases being formally screened by Member States annually has nearly quadrupled from 362 in 2020 to 1,286 (i.e., the 41% of all cases mentioned above) in 2024. Annual figures are illustrated below on this basis.

View full image: Overall Screening Figures (PDF)

View full image: Overall Screening Figures (PDF)

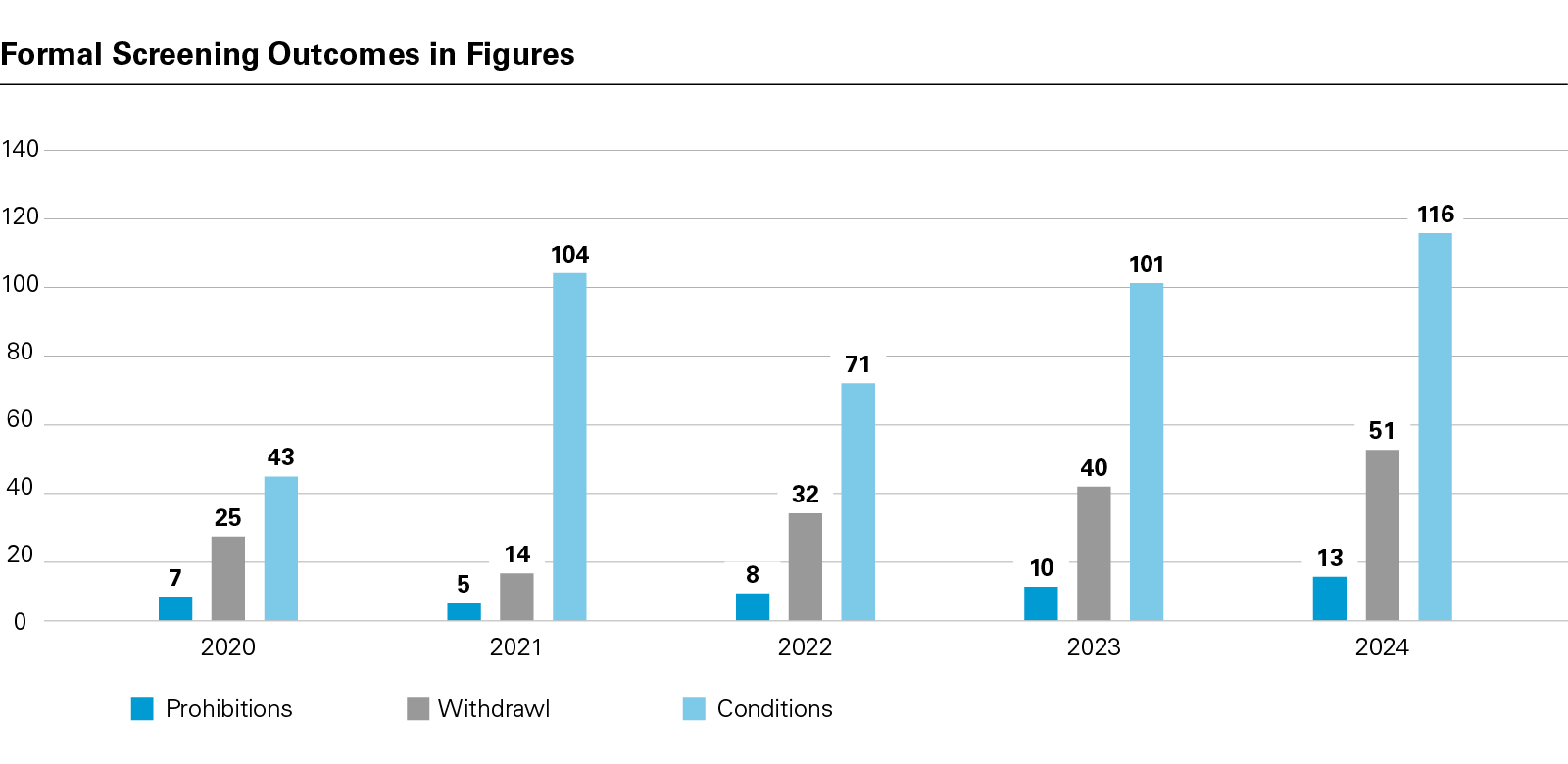

View full image: Formal Screening Outcomes in Figures (PDF)

View full image: Formal Screening Outcomes in Figures (PDF)

In absolute terms, therefore, over 100 cases were subject to conditions in 2024, over 50 were withdrawn during screening, and more than ten were prohibited.

The EU Cooperation Mechanism

Although the EC does not operate its own screening mechanism, the EU Cooperation Mechanism created by Article 7 of the EU FDI Regulation is a forum via which Member States can comment on notified deals, and the EC can ask questions and issue opinions. Reviews by the EC are divided into Phase 1, which is a 15-calendar day review, and Phase 2, which is more in-depth. In 2024, 92% of cases screened by the EC via the Cooperation Mechanism fell into the Phase 1 category.

A Phase 2 review involves a more detailed review of those transactions that "could affect security or public order in more than one Member State or create risks to projects or programmes of EU interest". In these cases, the EC will typically pose questions and can issue an opinion including its assessment, its recommendations on conditions, and/or any other information it deems relevant. That opinion is not made known to the notifying parties. Indeed, it may not be apparent at all to the notifying parties that the EC has become involved in their assessment as questions from the EC are posed via the national FDI authorities. In 2024, around 38 cases were subjected to Phase 2 scrutiny by the EC. In around ten of these, the EC elected to issue an opinion.

Sectoral Focus

In terms of the sectoral focus of the EU Cooperation Mechanism, the EC Annual Report is based on NACE codes, rather than by reference to the sectors in the EU FDI Regulation. 'Manufacturing', therefore, remains the most prevalent sector in terms of the number of transactions screened and the sector most frequently subjected to Phase 2 review (accounting for 50% in 2024). However, this broad sector encompasses a range of activities, including manufacturing electrical equipment and motors, industrial machinery and equipment, weapons and ammunitions, and pharmaceuticals.

Helpfully, however, the Report also provides an overview of the factors that were used to assess the criticality of the manufacturing sector during Phase 2 reviews. In order, these factors were:

- Critical technologies (49%);

- Critical infrastructure (26%);

- Supply of critical inputs (20%); and

- Access to sensitive information (5%), including personal information.

Legislative Developments and Outlook

Updates during 2024

Although Member States are not (yet) obliged to operate a national screening mechanism, almost all have heeded the EC's call and, as of the date of the Annual Report, 24 EU Member States had national legislation in place, with the remaining three, Croatia, Cyprus, and Greece, all on their way towards adoption. Indeed, the Greek regime has since been adopted – for more information on the details of how it will operate, please see our previous alert here.

Adoption of screening regimes is not the only trend, however. As well as the adoption of new regimes in Ireland and Bulgaria, 2024 saw ten Member States update their existing mechanisms. These updates vary in scope and direction, but, for example, those in Lithuania, Sweden and Slovakia, have expanded the scope of transactions subject to mandatory notification.

Outlook

EU FDI Regulation

In January 2024, the European Commission presented its proposal for a revision of the EU FDI Regulation (the Proposal). As drafted, the Proposal would require all Member States to implement a national screening mechanism, although this should be a fait accompli by the time of its adoption. More significantly, the Proposal will also set a "common minimum scope" for assessment in terms of the factors that Member States will be required to take into account. This includes, for example, the "availability of critical technologies", "the continuity of supply of critical inputs" and "freedom and pluralism of the media, including online platforms that can be used for large scale disinformation of critical activities". The proposed sectoral scope is also significant, with an obligation for all Member States to screen qualifying investments across a range of sectors deemed relevant to security and public order, ranging from entities active in critical medicines to financial systems.

Therefore, although all Member States are expected to have a national screening regime in place by the time that any version of the Proposal is adopted, there is a very real prospect that Member States will need to adjust their existing mechanisms in line with the changes likely to be introduced by the Proposal. In terms of next steps, the Proposal remains subject to finalisation by the EU institutions. The next trilogue meeting between the EC, the Parliament and the Council is scheduled for November 2025. Regardless, once an agreement is reached and voted upon by the Parliament and the Council, an implementation period (of 15 months in the current draft of the Proposal) will precede the coming into force of any changes.

Outbound investment screening

In January 2025, the EC adopted a recommendation on reviewing EU outbound investments (the Recommendation). The Recommendation applies to three technology areas of strategic importance which are considered to present a high level of potential risk (semiconductors, artificial intelligence and quantum technologies) and called on Member States to assess risks to economic security potentially arising from EU outbound investment transactions. Member States are due to report on the implementation of its Recommendation by June 2026.

Sally Staunton (Trainee Solicitor, London) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP