The 5 March 2021 announcement by the Financial Conduct Authority (the "FCA") signalled the definitive end of LIBOR.1 With attention turning to the post-LIBOR landscape, we examine the key features of forward-looking rates derived from RFRs ("RFR Term Rates") as an alternative to other rates derived from RFRs and the circumstances and considerations for their use.

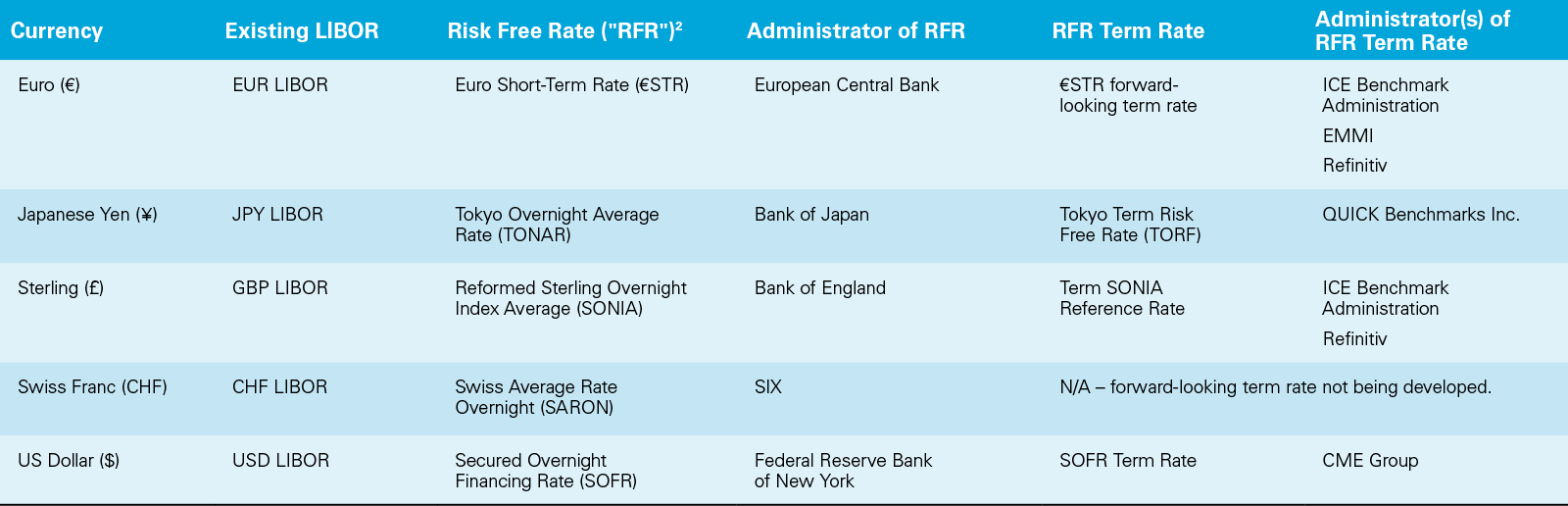

RFR Term Rates by currency

View full image: RFR Term Rates by currency (PDF)

View full image: RFR Term Rates by currency (PDF)

Status of RFR Term Rates

Euro – as yet, the EUR derivative markets are not sufficiently liquid to publish a €STR forward-looking term rate. No indication on timing has been provided, though administrators such as Refinitiv have indicated an intention to publish a forward-looking term €STR rate at the earliest opportunity.

Japanese Yen – TORF has been published and available for use since 26 April 2021.

Sterling – The Term SONIA Reference Rate has been published and available for use since 11 January 2021.

US Dollar – The New York Federal Reserve's Alternate Reference Rates Committee (the "ARRC") had set out in its Paced Transition Plan a target to recommend a SOFR Term Rate by 30 June 2021. The ARRC had consistently stated that any such recommendation was dependent on: (i) the development of sufficiently liquid SOFR derivatives markets underlying the rate; and (ii) the identification of appropriate use cases. The ARRC stated on 23 March 2021 that it would not be in a position to recommend a forward-looking Secured Overnight Financing Rate (SOFR) term rate ("SOFR Term Rate") by that date, nor could it guarantee that it would be in a position to recommend an administrator that can produce a robust forward-looking term rate by the end of 2021. The ARRC's subsequent statements on key principles, market indicators and its announcement of the selection of CME Group as the administrator of any SOFR Term Rate once recommended offer a roadmap for the remaining steps and reference market progress. However, the ARRC has yet to consult on use cases and while there is hope that the use of a "SOFR first" initiative could mirror the success of the UK's "SONIA first" drive in shifting liquidity in (especially shorter tenor) derivatives markets from USD LIBOR to SOFR, the timing for satisfaction of the market indicators is uncertain. The combination of the ARRC's 23 March 2021 statement and its encouragement (and UK and US regulatory pressure) on market participants to transition from LIBOR now, and using other SOFR rates, brings into play "in advance" rates, among others.

Products for whom "in arrears" RFR reference rates present adoption challenges

Regulators are encouraging the widespread adoption of RFR reference rates. Nonetheless, for certain loan markets and products most acutely concerned with advance calculation of interest, "in arrears" reference rates derived from RFRs ("in arrears" RFR reference rates") present complications, whether by reason of the product or country/borrower specifics. These include:

- Receivables discounting products, in which the purchase price is calculated by reference to the forward interest rate curve (often after tenor interpolation) in a discount formula to give a purchase price net of discounted interest to maturity;

- Islamic / Sharia-compliant products, which require that variable rates of return are pre-determined (i.e., the variable profit rate is set in advance of the commencement of the relevant period);

- FX cash loans to emerging market borrowers and export credit financings of large capital projects, in which advance notice of interest payable is required by certain categories of borrower (especially sovereigns or other debtors with fx conversion procedures to adhere to) in order to forecast cash flows or arrange outgoing fx payments;

- Commodity prepayments, in which scheduled amortisation and accrued interest on funds advanced against the future supply of commodities is set-off against the purchase price and needs to be calculated before the commercial invoice due date;

- Project finance or other structures with debt service account or debt service reserve account structures, requiring interest to be calculated in advance in order to enable compliance testing;

- End-user-facing derivatives, which are used to hedge (i) cash products that reference RFR Term Rates, or (ii) tough legacy products that reference synthetic LIBOR based on RFR Term Rates, and end-user derivatives used to manage such hedges.

Scope of use

Despite demand, regulators are deliberately limiting the scope of use of RFR Term Rates. The FCA and ARRC have respectively confirmed that 'the use of these forward-looking term rates is meant to be limited' and there will be a 'limited set of cases in which [the ARRC] believes a term rate could be used'. In its March 2021 draft Standard on use of Term SONIA Reference Rates (the "FMSB Standard") the FICC Markets Standard Board (the "FMSB") quoted the FCA's statement that "overnight RFRs provide the most robust benchmark interest rate available' and the regulatory expectation of widespread adoption in the UK £ market of overnight SONIA compounded in arrears. These statements reflect the concerns of regulators to 'ensure that a recommended term rate does not reintroduce the vulnerabilities that first prompted the transition away from LIBOR.'

The Working Group on Sterling Risk-Free Reference Rates (the "£ RFR WG") effectively recognised all of (1), (2) and (3) above in its January 2020 paper as permitted use cases for term / alternative rates to SONIA compounded in arrears. The £ RFR WG also identified less sophisticated clients for whom "in arrears" RFR reference rates present adoption challenges and who might benefit from alternative rates such as fixed rates or Bank of England Bank Rate (aka "Base Rate").

The Working Group on Euro Risk-Free Rates (the "€ RFR WG") published in May 2021 its recommendations on EURIBOR fallback triggers and €STR-based EURIBOR fallback rates. These contemplate a forward-looking methodology as the first step in a two-step waterfall as an alternative for: "trade finance", "export and emerging market finance products for which counterparties prefer to know the interest rates and amounts in advance"; and (surprisingly, but presumably aimed at SMEs) corporate lending products to corporates who "require the rate at the start of the interest period".

The ARRC is yet to consult on, let alone publish, SOFR Term Rate use cases. However, market participants expect substantial alignment with the approach in £ and €, with the exception of the use of SOFR Term Rate as a transition tool for legacy contracts: Term SOFR (i.e., a SOFR Term Rate selected or recommended by the US official sector) is the first step of the ARRC's recommended hardwired fallback waterfall.

Participants in the £ fixed income and wholesale lending markets should be aware of the FMSB Standard. In its current draft, this guidance essentially requires governance processes to underpin the assessment and record keeping of a 'robust rationale' for the application of Term SONIA within permitted use cases.

Considerations for use

Nature of the rates

Reference rates derived from RFRs are constructed in different ways. Regulators emphasise the importance of understanding the construction of these different rates. Key differences include:

- "in arrears" RFR reference rates vs LIBOR: RFRs (from which "in arrears" RFR reference rates are derived) are 'risk free' overnight rates and are determined, for any day, when "historic" (since they are published on the day when the overnight (in the case of SOFR, for example, repo) transaction is due to be repaid). "In arrears" RFR reference rates for a period are determined by aggregating the value of the daily RFRs over that period (hence, the use of compounding and other conventions like "lookback" to enable a rate to be determined prior to the due date for payment). Unlike LIBOR, "in arrears" RFR reference rates exclude any credit sensitivity component or term liquidity premium (hence, the need for a credit adjustment spread to avoid value transfer on transition).

- RFR Term Rates vs "in arrears" RFR reference rates: RFR Term Rates reflect market expectations on the future movement in the rate over an interest period (although they do not contain any credit sensitivity component or term liquidity premium), whereas "in arrears" RFR reference rates are historic and reflect actual rates. RFR Term Rates can therefore be used for rate fixing on or before the first day of an interest period, as per LIBOR rate determination mechanics. However, both "in advance" and "in arrears" RFR reference rates exist. Whereas "in arrears" RFR reference rates can only be determined towards the end of a period (using lookback, or other less common conventions such as lockout or payment delay), "in advance" RFR reference rates would, like an RFR Term Rate or LIBOR, be set on or before the first day of an interest period.

- RFR Term Rates v "in advance" RFR reference rates: two of the most common "in advance" RFR reference rate methodologies are where the rate is determined by reference to:

- ("last reset") the corresponding rate for the immediately preceding interest period; or

- ("last recent") a recent observation period shorter than the interest period.

Both the RFR Term Rate and any "in advance" RFR reference rate could be rate set on or before the first day of the period. The RFR Term Rate is a predictive rate for the relevant interest period; the "in advance" RFR reference rate is a historic rate for a prior observation period. A concern with "in advance" RFR reference rates is over "congruency" (the lack of alignment between the interest period to which the rate applies and the observation period from which it is taken). While application of the "lookback" convention creates the same issue to a degree, the € RFR WG, among others, has raised concerns over the use of "in advance" rates for interest periods in excess of three months.

-

RFR Term Rates v credit sensitive rates: especially in the US market, certain creditors have taken an interest in so-called credit sensitive rates, which, like LIBOR, embed both credit sensitivity and term liquidity premium. These rates (whether published or in progress) include Bloomberg's BSBY; ICE Benchmark Administration's Bank Yield Index; AFX's AMERIBOR and IHS Markit's USD Credit Spread Adjustment & Rate. Well-advised borrowers will be reluctant to give up the anticipated lower volatility of an RFR reference rate in favour of rates that re-introduce credit sensitivity. Moreover, credit sensitive rates are not endorsed by the official sector: in his speech at the ARRC's 11 May 2021 SOFR Symposium, Andrew Bailey (Governor of the Bank of England) addressed this directly:

"Transition from Libor was always going to be challenging given its widespread use, but to those looking for an easy descent by substituting Libor for credit sensitive rates that do not address all of its fundamental weaknesses, they risk much of the good progress that has been made. While these rates may offer convenience as a short-term substitution, they present a range of complex longer term risks. And while they may remove the reliance on expert judgement, they veneer over the fundamental challenges of thin and incomplete markets through the extrapolation of data. The ability of such rates to maintain representativeness through periods of stress remains a challenge to which we have not seen adequate answers."

Pros and Cons

Whether driven by product need (e.g., receivables discounting), borrower identity or (generally, emerging market) fx procedures or currency control regimes, for certain products and markets, there is a strong rationale for the use of a rate (whether RFR Term Rate or "in advance" RFR reference rate) that can be determined in advance. Advantages include:

- easier short-term operational adoption across loan IT / software / treasury management systems; the ARRC describes Compounded SOFR in Advance as 'the most like how LIBOR functions today and […] easiest to operationalize';

- "payment certainty", i.e., the ability to forecast and manage cashflow and liquidity; however, payment certainty can also be achieved for "in arrears" RFR reference rates via a longer lookback (although loans with linked hedging would require bespoke interest rate hedges with an equivalent adjustment); and

- (RFR Term Rates only) incorporation of market expectations on anticipated interest rate movement in the relevant interest period.

Potential drawbacks include:

- Inconsistency across currencies – An "in arrears" RFR reference rate is available in all currencies for which an RFR is available. Not all currencies are developing an RFR Term Rate; the National Working Group on Swiss Franc Reference Rates does not intend to develop a term rate for SARON.

- Lower liquidity in RFR Term Rate derivatives markets – Lower liquidity in RFR Term Rate derivatives markets is likely to make RFR Term Rate derivative pricing more expensive than equivalent risk management in deeper "in arrears" RFR reference rate derivatives markets.

- Greater expense and availability of RFR Term Rate exposure hedging – Risk management trades for RFR Term Rate exposures will require a dynamic hedging operation. This in itself further increases transaction costs. Not all banks are yet able to offer hedging products for RFR Term Rate hedging.

- Operational burden – The multiplicity of approaches and methodologies (within or across currencies) further increases operational burdens for market participants beyond complexities in the IBOR transition already resulting from: differences in timelines and progress across currencies or in counterparty readiness; access or licensing issues for relevant data; information service providers not displaying relevant rates or conventions.

Conclusions

Regulators are concerned to ensure that LIBOR transition does not perpetuate the systemic risks resulting from the imbalance between the volume of transactions referencing the LIBOR benchmark and the volume of transactions underlying its calculation.

At a time when regulatory pressure to transition is increasing and the "end game" and the "final countdown" are already behind us, market participants should focus on transition using already available RFR reference rates. Borrowers should approach their bank counterparties to establish what products those lenders are able to offer them in both cash markets and hedging products.

The complications relating to Term SOFR in the USD transition have de facto delayed transition more widely, given the role of USD in multicurrency financing in other markets and its prevalence in international cross-border trade and in many emerging markets.

"In arrears" RFR reference rates are the primary solution for mainstream loan markets and mainstream adoption of these rates in derivatives markets is necessary to provide a sufficiently deep underlying market to support the development of robust RFR Term Rates. Absent such increase in underlying liquidity, RFR Term Rates in key currencies will remain unavailable even to those within approved use cases.

The IBOR transition is ushering in a multi-rate environment, especially, but not only, in the US. Currency working groups have recognised certain more specialist markets and products where the use of RFR Term Rates can be justified on a permanent basis (beyond the use of Term SOFR as a transition tool for legacy USD exposures). For USD exposures, market participants outside the US may adopt an approach equivalent to the New York market "flip forward" to Term SOFR, using an alternative to Term SOFR until the latter has been recommended by the ARRC and operationalised in the market. However, "in advance" RFR reference rates or other alternatives (for some products and borrowers, perhaps central bank base rates) also provide "payment certainty" and may represent more than just a temporary solution.

Market participants considering the application of RFR Term Rates should take care to do so within use case parameters and should implement appropriate governance procedures.

1 Please see our separate alerts for, respectively, English and New York law documents.

2 Reference rates derived from RFRs can take different forms (see "Considerations for use"; "Nature of the rates"). We use "RFR" to refer to the daily overnight rate from which reference rates can be derived.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP