The 'Taskforce on Scaling Voluntary Carbon Markets' (the "Taskforce") is a private sector initiative working to scale an effective and efficient voluntary carbon credit market to help meet the goals of the Paris Agreement.

The Taskforce is spearheaded by Mark Carney, UN Special Envoy for Climate Action and Finance Advisor to UK Prime Minister Boris Johnson for the 26th meeting of the Conference of the Parties to the United Nations Framework Convention on Climate Change (UNFCCC) ("COP26"). The Taskforce is chaired by Bill Winters, Group Chief Executive, Standard Chartered, and sponsored by the Institute of International Finance ("IIF") under the leadership of IIF President and CEO Tim Adams. It is made up of more than 250 member and consultation group institutions, representing buyers and sellers of carbon credits, standard setters, the financial sector, market infrastructure providers including Ingrid York of White & Case, and relevant sector trade associations. The Phase I final report of the Taskforce (the "Phase I Final Report") was introduced by Bill Gates, Mark Carney, Bill Winters and Annette Nazareth at the Davos Agenda 2021.

On 21 May 2021, the Taskforce launched a new consultation process (the "Phase II Consultation") on three core topics:

- the establishment of a new umbrella governance body to oversee the growth of voluntary carbon markets;

- the development of legal principles and contracts; and

- recommendations relating to the definitions of Core Carbon Principles ("CCPs") for credit level integrity.

The Taskforce has published three documents as part of the Phase II Consultation (the "Phase II Consultation Documents") including:

- a 'Public Consultation Report' (the "Report");

- governance 'Terms of Reference' and a call for initial engagement from interested parties; and

- a 'Technical Appendix' for public consultation containing analysis of the material in the previous two documents.

The Phase II Consultation Documents were developed with the extensive engagement of Taskforce members and working groups.

The Phase II Consultation represents the first output of Phase II of the Taskforce's project to scale-up voluntary carbon markets, being the 'Development and Implementation' phase. The Phase II Consultation follows on from the Phase I consultation on an initial blueprint for a voluntary greenhouse gas or carbon market, published on 10 November 2020, which was summarised in our 13 November 2020 client alert here (Voluntary Carbon Markets: A Blueprint). The Phase II Consultation also follows the publication of the Phase I Final Report after such initial consultation in November and December 2020, which was summarised in our February 2021 client alert here (Scaling Voluntary Carbon Markets: The Final Report).

Timeline

|

10 November 2020 |

Taskforce publishes Phase I Consultation Document |

| 13 November 2020 |

White & Case publishes client alert on Phase I Consultation Document. |

|

28 January 2021 |

Taskforce publishes Phase I Final Report and Summary on Taskforce |

|

18 February 2021 |

White & Case publishes client alert on Phase I Final Report. |

|

21 May 2021 |

Taskforce publishes the Phase II Consultation Documents including: |

|

21 June 2021 |

Deadline for market participants to provide feedback on Phase II Consultation Documents. |

|

Mid-July 2021 |

Publication of report on outcome of Phase II Consultation. |

|

9 August 2021 |

Interested parties to submit final expressions of interest for participation in the new umbrella governance body. |

|

September 2021 |

Taskforce's advisory board to recommend participants to assume roles on the new governance body. |

Phase II Consultation Overview

The Report is structured across four chapters providing specific details on how the Taskforce is seeking to further the development and growth of the voluntary carbon markets. The chapters are supplemented by public consultation survey questions. The four chapters include:

- Objectives and Focus of the Taskforce. The Taskforce has set a dual ambition of ensuring high-integrity carbon credits and robust, transparent and liquid markets. The remaining chapters of the Report set out in greater detail the methods to be adopted in achieving this ambition.

- Governance. Having identified the need for a more robust governance regime in the Phase I Final Report, this chapter presents the work of the newly formed Taskforce Governance Working Group which has developed a blueprint and set of concrete recommendations for the mandate, organisational design and implementation path for a new umbrella governance body overseeing the scaled-up voluntary carbon market.

- Legal Principles & Contracts. This chapter focuses on the work of the newly formed Taskforce Working Group on Legal Principles and Contracts of which Ingrid York was a workstream lead, which aims to standardise the legal framework underpinning the issuance of carbon credits and thereby promote liquidity.The new working group has addressed this aim by defining use cases to drive awareness of the methods by which participants can utilise the market and by clarifying operational requirements for standard setters terms of use and also developing general trading term.

- Credit Level Integrity. The new umbrella governance body will draw on the expertise of the newly formed Taskforce Credit-level Integrity Working Group, which was established to support the governance body on the development and curation of CCPs in particular. This process will be operationalised through an assessment framework for standards as well as a set of credit eligibility guidelines. The new working group has also set out a proposal for the taxonomy of additional attributes for each CCP credit.

Topic One: Governance

As part of the Phase II Consultation, the Taskforce's newly formed Governance Working Group has produced governance 'Terms of Reference' for the new umbrella body setting out a blueprint for the operation of such new body, as well as calling for initial engagement from (potentially) interested parties to assume roles within such new body. The Terms of Reference and call for initial engagement aspects are set out in a separate deep-dive document published alongside the Report.

The development of the terms of reference are supplemented by the Taskforce's technical appendix which provides in-depth analysis on how the new body can draw on some of the key features of other governance bodies operating in the carbon markets or financial markets. This analysis has informed the blueprint for the new governance body's design and framework as set out in the terms of reference.

Mission and Mandate

The new umbrella governance body has a mandate that covers three main areas:

- Core Carbon Principles. The new body will be responsible for the establishment, hosting and curating of:

- credit eligibility guidelines for different project and methodology types and additional attributes;

- CCP assessment framework for new and existing standard setters; and

- eligibility principles for existing market bodies including suppliers and Validation and Verification Bodies ("VVBs").

- Oversight. The new body will provide oversight over standard setters on adherence to the CCPs. The body will be responsible for approving standard setters that apply for eligibility and conducting regular spot checks to ensure adherence.

- Coordination. The aim of the new body is not to undermine the current market structure, but rather to strengthen and expand the role of existing bodies and frameworks, as well as plug the critical gaps in the current landscape.

- The new body will coordinate the work of, and manage the interlinkages between individual bodies and serve as a steward for, and endeavour to foster the responsible growth of, the voluntary carbon market by defining a roadmap for success.

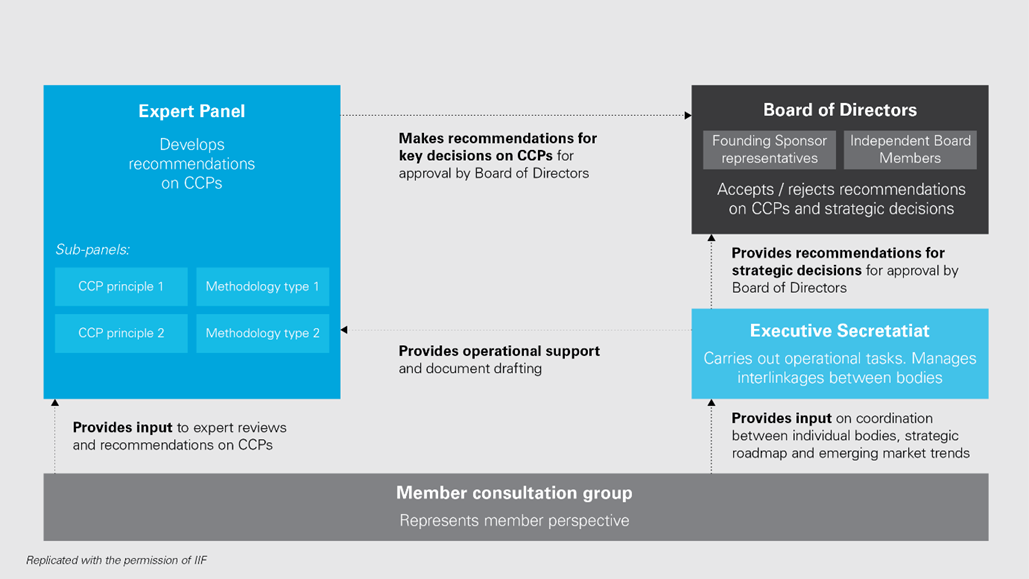

Organisational Design

As well as setting out the mission and mandate of the new umbrella governance body, the Governance Working Group has also detailed a proposed structure and composition of such new body. The new body will be independent, voluntary, stakeholder-led and self-regulating.

The new umbrella governance body will comprise of four parts, each with their own tasks, composition and nomination process.

Design of the New Umbrella Governance Body

It remains to be seen how credits developed in accordance with CCPs recommended under the new governance structure will interface with existing regulations in the financial services sphere - and, in particular, different jurisdictions' approaches to regulating specific types of financial instruments and the activities and services relating to these.

Call for Initial Engagement from (Potentially) Interested Parties

During the publication consultation running from 21 May to 21 June 2021, the Taskforce is calling for initial engagement from parties that are (potentially) interested to assume the various roles on the new body. Interested parties should consider the questions set out in the Report as well as the Taskforce's preliminary guidelines on which type of entities could assume the various roles within the new body, being a Founding Sponsor, Independent Board Member, Expert Panel Member and Executive Secretarial Host. The Taskforce is willing to engage with interested parties and explain the recommendation process on who could assume the various roles in further detail.

Following the Phase II Consultation, the Taskforce will refine the governance guidelines and publish them in its final report in mid-July 2021. Following this, parties can submit to the Taskforce their final expression of interest until 9 August 2021 (this includes parties who did not initially engage in the Phase II Consultation in May/June 2021).

Funding

The new body will operate on a not-for-profit basis, with a phased-approach to its funding requirements as follows:

- Setup Phase (first three years). The initial setup phases will require seed funding of approximately USD 23 to 33 million, with responsibility for securing this fund falling on the Founding Sponsors of the new body and the Taskforce. Key sources of funding will include governments, contributions from corporates and philanthropic donations.

- Steady State Phase. The steady state phase will require approximately USD 7 to 10 million per year to cover the new body's expenses. Funding schemes may include membership fees and/or a service-based user fee e.g. based on CCP credit issuance or retirement which could potentially be levied on CCP credit purchasers. If expectations of the predicted voluntary carbon market growth come to fruition, the steady state funding requirements will amount to less than 0.4 per cent. of the predicted voluntary carbon market size in 2024.

Transition

The focus and specific objectives of the new body will shift once the foundations for the body and its role within the global voluntary carbon market have been laid. It is anticipated that the new body will transition from the setup phase to the steady state phase after three years with the transition applying across all aspects of the body including the mission and mandate, organisational design and funding needs.

Operating Principles, Transparency and Grievance Mechanism

- Operating Principles. The new body will adopt key operating principles including the adoption of a highly collaborative approach, capitalising on the current momentum of voluntary carbon markets, obtaining buy-in from the private sector, ensuring transparency in decision-making and high integrity in decision making.

- Participant Rights. The new body will endeavour to ensure due process and procedural fairness by demonstrating e.g. independence, freedom from bias and conflict of interest, ensuring market participants have a right to be heard, ensuring decisions taking by the body are properly explained and providing a right to challenge the most serious decisions.

- Transparency Mechanism. Measures will be put in place to ensure the new body's procedures are disclosed transparently to the public. The body will also disclose its financial position, update the market on its activities and hold annual general meetings with all members. The body's approach to transparency will also be translated into the trading of voluntary carbon credits via public disclosure of certain trading information.

- Grievance Mechanism. The governance body will define a grievance mechanism to ensure that complaints against the procedures and decisions of the body are made publicly available. The body will also establish mechanism to provide privileges and immunities for individuals serving in a role in the governance body.

- The standard assessment framework will require standard setters to establish a grievance mechanism to apply for eligibility under the CCPs. The governance body will also assume a mediation role for disputes that cannot be resolved between market participants.

Topic Two: Legal Principles and Contracts

Current Legal Landscape

- The Taskforce asserts that the current legal landscape in carbon markets is characterised by fragmentation and a lack of standardisation between the various market participants. The ambiguous legal landscape creates a significant burden on market participants who must navigate the following issues across their portfolio of credits:

- Methodology types: different project types make it more or less challenging to ascribe rights over carbon credits issued to the parties involved.

- Standards: different standard setters apply varying definitions of a carbon unit and the associated rights attached to it.

- Fragmentation: the heterogeneous supply chain consists of small players, multiple trading venues and different contracts. The high volume of small suppliers can also make it costly and complex to interface with exchanges.

- Unclear liabilities: in most contracts, the current position is that legal liability rests with the verifier, which can prove to be an unattractive business model.

- Complexity from emerging services: new services such as distributed ledger technology (DLT) applied through a meta-registry or trading network add further complexity to the legal underpinnings.

- Lack of access to financing: access to financing and the often significant lag between a project receiving financing and credit being produced provides serious challenges to market growth.

- Different jurisdictions and financial regulatory frameworks: different legal frameworks across jurisdictions have given rise to different legal rights associated with carbon credits and the rights of governments and private stakeholders to them. In relation to Article 6 of the Paris Agreement specifically, the Taskforce has made it clear that more work will need to be done to ensure voluntary carbon markets comply with the rules of the Paris Agreement once the outcome of the hotly debated Article 6 negotiations becomes clearer.

- Fraud risks: the presence of bad actors in the market can pose risks of money-laundering, tax fraud (e.g. EU ETS related incidents), consumer fraud and double counting.

Current Legal Nature of Carbon Credits

- Market scaling: market scaling is hindered by the hesitancy of market participants to commit to transactions, where the legal implications of doing so are unclear.

- Fungibility: the divergence of treatments of carbon credits across regimes hinders liquidity and trading.

- Existing documentation: providing the necessary legal underpinning to general trading terms by way of sound legal opinions presents a challenge given the uncertain and fragmented legal treatment.

- The newly formed Working Group on Legal Principles has sought to address these legal issues by:

- providing clarity over use cases which demonstrate how harmonised contracts and standard clauses and procedures can help scale the market. These use cases are discussed further in the accompanying technical appendix;

- providing operational requirements for standard setters' terms of use; and

- providing key general trading terms.

- The Taskforce sets out an implementation phase from July to October/November 2021 during which:

- the newly formed governance body will host and update operational requirements for standard setters' terms of use recommended by the Taskforce; and

- external industry bodies (e.g. IETA, ISDA and EFET) will be able to integrate key general trading terms recommended by the Taskforce into the contract templates.

Standard Setters' Terms of Use

As part of the Phase II Consultation, the Working Group on Legal Principles has set out proposals which could be introduced across all standard setters' terms of use. Some of the key areas of focus are highlighted in the graphic below and discussed in further detail within the technical appendix.

Although current practice shows it is possible to trade multiple standard setters' credits under one reference contract, the Taskforce asserts that a more legally uniform product, backed by harmonised terms of use across standard setters, will provide clarity to buyers on the legal structure underpinning their investment in carbon credits.

Operational Requirements for Standards' Terms

|

Topic |

Proposal |

Rationale |

|

Uniform onboarding procedures |

Users must undergo rigorous onboarding procedures upon registration with periodic checks performed on a regular basis thereafter. The new governance body will have the mandate to define minimum documentation required by the standard setters. |

Ensure standards provide for uniform protection against risks from fraudulent actors |

|

Force Majeure |

Standard setters will not be held liable for losses incurred under Force Majeure. |

Protect standard setters from liability before credits have been issued |

|

Limitation of Liability |

Registry users will assume full responsibility and risk of loss resulting from their use of the registry and will have no claim against the standard setters' or any of its contractors. |

Avoid litigation due to losses indirectly related to the use of the standards setters |

|

Prohibited practices and suspension of service |

Standard setters may suspend services and/or close the User's account if they reasonably suspect that the User has engaged in fraudulent, unethical or illegal activity; standard setters make all reasonable efforts to ensure that neither developers nor their subcontractors engage in such practices. |

Ensure an equal degree of protection against bad actors across standard setters |

|

Dispute Resolution |

The TSVCM recommends standard setters require arbitration. |

Ensure the maximum possible degree of harmonization among standard setters |

|

Auditable logs |

Standard setters commit to keeping auditable transaction logs and secure transfer procedures. |

Ensure transparency |

|

Tax compliance |

Standard setters ensure to the maximum degree possible that developers pay all taxes and charges imposed by governmental authorities related to the use of the standard setters. |

Ensure maximum degree of harmonization across standard setters; enforce legal quality |

|

Cybersecurity |

Standard setters should have in place cybersecurity systems adequate to minimize risks related to hacking and fraud. |

Ensure standard setters provide for uniform protection against cyber risks |

|

Termination |

Both Parties may terminate the Terms of Use by giving 30 days' notice to the respective other. |

Ensure maximum degree of harmonization across standard setters; enforce legal quality |

Replicated with the permission of IIF

General Trading Terms

The Taskforce asserts that currently the general trading terms of carbon credit contracts lack uniformity thereby adding to fragmentation and illiquidity in the voluntary carbon credit market.

The Working Group on Legal Principles and Contracts has set out proposals for a harmonised contractual foundation for key trading terms. Enhanced clarity over trading documentation will widen access to smaller market players in particular, allowing them to circumvent complex and redundant drafting procedures and associated legal expenses.

These general trading terms will be of more particular relevance to OTC contracts. In relation to exchange-traded contracts, the Taskforce's expectation is that exchanges may follow the recommendations in building on their existing trading rules.

The full language and analysis of the key general trading terms set out below can be found in the technical appendix. These terms can be adapted to parties' requirements and readily integrated into OTC and exchange trading contracts.

Key General Trading Terms

|

Topic |

Proposal |

Rationale |

|

Definition of Products |

The product is defined as either a removal or an avoidance/reduction CCP credit that has been issued by one of the standard setters approved under the Governance Body and that meets all of the requirements of the CCPs as well as some of the additional attributes specified. See credit-level integrity below. |

Establish the CCPs as the unit on which reference trading contracts are based. |

|

Avoidance of double counting |

The Seller warrants to the Buyer that they have not and will not use or make any claims with respect to the CCPs being traded, and that they have not sold, transferred, retired, or otherwise created any interest in the CCPs other than as contemplated by the Agreement. In a primary sale, the Seller commits not to double count, i.e. not to have registered CCP credits in more than one standard setter. Upon transfer of the CCP credit, the Buyer commits to use, make claims with respect to, or further sell the credit exclusively one time on behalf of either themselves or one subsequent Buyer. |

Ensure CCPs are uniquely retired on behalf of one entity. Double counting refers to the practice of two or more participants claiming the same carbon credit towards their sustainability goals thereby providing a misleading impact of the credit. |

|

Settlement and Delivery |

For OTC: Parties hold accounts in one specific standard setter, agreed upon upfront. For Exchange-traded contracts: Parties hold accounts in all standard setters that the Exchange shall transfer the credits from. Parties are expressly encouraged to consider the legal implications which different delivery mechanisms have in different jurisdictions (resulting in CCPs being considered commodities, securities, or other types of assets). |

Enable different types of delivery to accommodate different needs, while raising attention to complex legal implications. |

|

Failure to Deliver |

Credits already exist: the Party breaching the Agreement will reimburse the other. Credits are in development: the Parties either apply the same provisions, or negotiate appropriate remedies for non-delivery. |

Protect both Parties; account for unit contingent contracts (payment is settled upon delivery) |

|

Force Majeure |

The Parties choose one among three modalities of termination payment: (i) No termination payment (ii) Partial termination payment (iii) Full termination payment |

Protect Parties from liability for damage caused out of their control |

|

Limitation on Liability |

Neither Party is liable for any loss of income, loss of profits or loss of contracts, or for any indirect or consequential loss or damage. |

Avoid litigation due to losses indirectly related to trading of CCPs (e.g. reputational damage in case of other Parties' wrongdoing). |

|

Compensation |

Each party compensates the other for claims directly incurred in connection with: (i) any violation of applicable law, regulation or order by such party; and/or (ii). any breach of a representation or warranty by such party. |

Avoid litigation due to losses indirectly related to trading of CCPs (e.g. reputational damage in case of other Parties' wrongdoing) |

|

Change in Law |

Parties are given two options: (i) if changes in law do not materially impact on the quantity of credits to be delivered, it is the Seller's responsibility to comply with those changes; if they do, the Buyer may terminate the Agreement. (ii) if any Party is prevented by the change of law from complying with its obligations under the Agreement, the Parties seek to agree on amendments in good faith; if such agreement cannot be found, either Party may terminate the Agreement. |

Provide a choice to Parties and allow for minimisation of legal expenses |

|

Dispute Resolution |

Parties are given two options based on standard ISDA language, which they can adjust to their needs (choice of court, choice of jurisdiction, Arbitration Body): (i) Jurisdictional clause (exclusive / non-exclusive) (ii) Arbitration clause. |

Give Parties the choice to select the mechanism they find most suitable, while providing standard language for each; minimize legal expenses |

|

Benchmark price/source |

In the long term, if a benchmark price is used for CCP credits, it should comply with IOSCO principles. |

Ensure a high quality standard for benchmark prices used |

|

Tax Compliance |

The Seller will pay all taxes arising prior to delivery; the Buyer will pay all taxes after delivery. Where the Seller is required by law to pay taxes that are the Buyer's responsibility, the Buyer will reimburse the Seller. |

Avoid uncertainty emerging from different jurisdictions involved |

Replicated with the permission of IIF

Commentary

Role of Market Participants

The process of harmonising standard setters' terms of use and general trading terms will require the assistance and expertise of a wide-range of market participants, including in respect of trading terms for example the input of international industry bodies such as the International Swaps and Derivatives Association, Inc. (ISDA), the International Emissions Trading Association (IETA), the European Federation of Energy Traders (EFET) and the Futures Industry Association (FIA) and intergovernmental bodies such as UNFCCC, UNCITRAL and UNIDROIT who have significant expertise in the development of nascent markets and model laws.

The expertise of these entities will need to be complemented by the experience of various other existing and new market participants within the voluntary carbon markets in order to ensure wide acceptance and usage of the respective terms.

We note that the Taskforce has specifically called upon external industry bodies (e.g. IETA, ISDA and EFET) to integrate key general trading terms recommended by the Taskforce into their contract templates, as well as such entities to commission legal opinions on the legal nature of carbon credits, and on international governmental bodies (e.g. UNFCCC, UNCITRAL and UNIDRIOT) to provide respective recommendations.

The results and feedback from the Phase II Consultation will provide useful insight into the appetite for standard setters and also industry bodies to embrace the recommendations of the Working Group on Legal Principles and Contracts.

Legal Framework

As noted above, it remains to be seen how credits developed in accordance with CCPs recommended under the new governance structure will interface with existing regulations in the financial services sphere - and, in particular, different jurisdictions' approaches to regulating specific types of financial instruments and the activities and services relating to these.

In addition, current financial market infrastructure global principles and post-crisis regulation applicable to trading platforms and financial market utilities will similarly need review and potential revision in order to clarify their application to and interface with rapidly scaling voluntary carbon markets and to ensure that they do not stifle these innovative markets as they grow and develop.

Such reviews will also inevitably consider these markets' interoperability with wider trading and post-trade ecosystems across areas such as clearing, settlement, reporting and market surveillance. They will also likely draw regulators' post-pandemic focus on these markets' operational resilience, third party risk management, cybersecurity and use of risk-concentrated cloud services.

A major challenge in these reviews will be determining how aligned current and any amended regulatory frameworks are and can be, taking into account the global and cross-border nature of climate change risks, together with many governments' policy drivers to encourage all industry sectors to focus on mitigating them, both directly and indirectly.

Governments may take the view that the financing of reduction and removal projects overseas is just as impactful as domestic investment, and direct their regulators in legislation, via mandated regulatory objectives or otherwise, to seek global regulatory alignment.

In this regard, we note that the Taskforce has invited jurisdictional regulators to review their treatment of voluntary carbon credits with the aim of providing further guidance on their legal nature, aligned across jurisdictions

Topic 3: Credit-level Integrity

The newly formed Credit-level Integrity Working Group was established to support the new umbrella governance body by providing input on the key documentation it would need, including in both developing and operationalising the CCPs. The main purpose of the CCPs is to provide for a threshold standard for high quality credits at the credit level and to ensure integrity of the bodies assessing these thresholds at the participant level. The Taskforce asserts that tackling these issues around credit quality and credit assessment will foster confidence in the market and drive buyer demand.

In this Phase II, the Credit-level Integrity Working Group has produced a draft assessment framework for standard setters, an analysis of a set of credit eligibility guidelines and an initial set of additional attributes that will act as an identifier of each CCP credit based on its specific characteristics. The intention is that the development of these initiatives will enable the CCPs to have a tangible impact on the integrity of credits and the voluntary carbon credit market.

Assessment Framework for Standards

The assessment framework for standards will be used by the new governance body to evaluate which standard setters may issue CCP credits. The aim of further developing CCPs has been both to harmonise and also exceed quality standards currently in the market. The below proposal is a first draft that the governance body will refine and develop.

Assessment Framework for Standard Setters:

- Additionality: projects or activities yielding CCP credits must demonstrate additionality before credits are issued to them, including:

- Financial additionality test: ensures the environmental gain would not have occurred without the revenue from carbon credits.

- Penetration level test: the penetration level of project activity must be below an appropriate threshold to demonstrate low availability. This only applies to avoidance/reduction type carbon credits. It is stated in the Report that Taskforce members have provided strong arguments for and against the proposal, which requires both the financial additionality test and also the penetration level test.

- Regulatory additionality test: in order to demonstrate regulatory additionality, the project must not be in response to legal or regulatory obligations under laws or regulations in a jurisdiction.

- Permanence: standard setters should ensure credits are issued only for projects and activities in which green house gas reductions or removals are permanent or, for those activities which carry a 'reversal risk', adhere to a minimum permanence timeframe and a comprehensive risk mitigation and compensation mechanism.

- Standard setters must ensure the risk of reversals are monitored throughout the minimum permanence timeframe.

- Standard setters will be expected to maintain a reversal compensation procedure, for example through insurance or a buffer pool in order to compensate for any reversal events for methodology types that include storage. Buffer volumes will need to be maintained in line with the specific portfolio risk. This compensation procedure will apply to both intentional and unintentional reversals.

- Minimum buffer requirements will be defined by the new governance body and will vary depending on the level of the reversal risk associated with the different methodology types.

- In case of a reversal event, the relevant standard setters will retire the same number of credits as are affected by the reversal event from the buffer pool to which the invalidated credits belong.

- Standard setters must include the requirement to project or activity owners to notify likely reversals within 30 days of their discovery, indicating whether the reversal as avoidable or unavoidable.

- Leakage Minimisation: standard setters must require leakage assessments for those projects or activities where leakage is identified as a risk. Credit issuance volumes should be adjusted to mitigate for any increase in emissions outside the boundary of the project or activity. Leakage must be monitored on a continual and systematic basis during the credit period where standard setters are using the confirmed leakage approach for deductions and standard setters must require the publication of leakage estimates and monitoring results in the interest of transparency.

- Baseline Setting Approach: standard setters must require the estimation and use of conservative and independently audited baselines for any activity or project aiming to receive CCP credits.

- At the start of each new crediting period, standard setters must ensure developers revise baselines where necessary and indicate triggers for revisions of baselines.

- Baselines must be independently audited and endorsed by third party experts and be open to public scrutiny.

- It is stated in the Report that Taskforce members have provided strong arguments for and against the proposal on baselines for forestry projects.

- Verification: Assessments of projects and activities must be calculated in a conservative and transparent manner, based on accurate measurements and quantification methods. The monitoring of emissions reductions and removals must be validated and verified by accredited validation/verification bodies.

- Real: No CCP carbon credits can be issued on an ex-ante basis on the basis of potential emissions reductions or removals.

- Do No Net Harm: Any emission reductions or removals against which CCP credits are issued must be the result of activities that at a minimum do no net environmental or social harm.

- Standard setters can ensure the projects' overall impact prevents any net social or environmental by conducting impact assessments and regular community or stakeholder consultations.

- Standard setters must indicate the safeguards in place to prevent social and environmental risks and define dispute resolution mechanisms to address issues relating to the net impact of projects.

Operational Considerations for Standard Setters:

- Programme Governance: standard setters must be managed by government or non-profit organisations which set out in a transparent manner their governance structure.

- Programme Transparency: regulatory documents (e.g. standards), core normative references (e.g. statutes, bylaws and principles) and the different quantification methodologies must be made publicly available. Standard setters are also obliged to put in place provisions for public stakeholder consultation on the development of programme rules and procedures, accounting methodologies and project and governmental programmes.

- Independent Third-party Verification: the standard setter must publish requirements for independent third-party verification, including for accreditation and oversight of validation and verification bodies through spot checks on the work of these bodies.

- Legal Underpinning: standard setters must ensure a robust legal framework to underpin the creation and ownership of credits.

- Publicly Accessible Registry: standards setters must establish a publicly available registry that tracks the credits issued and provides the basic functionality to:

- provide access to all underlying project information;

- transparently issue, retire and cancel credits;

- individually identify the credits through unique serial numbers to avoid practices such as double counting;

- identify unit status;

- track the chain of custody, from creation to retirement and keep auditable transaction logs and secure transfer procedures.

- Registry Operation: standard setters must establish procedures to ensure all account holders meet rigorous onboarding procedures and agree to legal requirements regarding the use of the registry. The registry must guard against service provider conflicts of interest and also have robust security and provisions for matters such as redundant data storage, regular security audits and systems backups.

- Liability for Credit Permanence: as mentioned above, standard setters will be liable to retire credits from the corresponding buffer pool where voluntary or involuntary reversal events occur. In the event that reversals are greater than the buffer, the standard setter commits to cover any shortfall by replacing lost credits with equivalent replacement credits.

- Registry Terms & Conditions: some of the key provisions for standard setters to consider include dispute resolution procedures, tax compliance and termination provisions. The terms and conditions should also set out the circumstances where a user's account may be suspended or closed, for example following engagement in fraudulent or illegal activity.

Credit Eligibility Criteria

- The Credit-level Integrity Working Group has carried out an analysis of the current credit eligibility guidelines used by standard setters in the market today.

- The analysis highlights issues around which methodology types require greater degrees of assessment in order to give effect to the CCPs. For example, the Credit-level Integrity Working Group identified that the CCP relating to the permanence of reductions or removals from a project would require a greater degree of assessment for afforestation projects than it would for renewable energy generation activities.

- By taking a tailored approach to designing individual methodology protocols, standard setters will be able to evaluate and identify which specific methodologies comply with the relevant credit eligibility guidelines and CCPs. Market participants can therefore be confident that CCP credits achieve their intended purpose.

- The Credit-level Integrity Working Group has set out within the technical appendix detailed analysis in relation to each of the CCPs mentioned above explaining the current market practices across standard setters. In conjunction with this analysis, the working group has provided some key questions for the future governance body to take into account in seeking to define credit eligibility guidelines.

Taxonomy of Additional Attributes

- The Credit-level Integrity Working Group has identified proposed additional attributes which will serve as mandatory tags thereby codifying attributes that all standard setters must specify in issuing CCP Credits. Additional attributes allow for CCP credits to be easily differentiated by buyers and sellers in the market and provide clear price signals and price differentiation for CCP credits.

- Additional attributes will not substitute any information attached to a carbon credit, rather they will act as mandatory additional labels to enhance the categorisation of CCP credits.

- The additional attributes put forward by the Credit-level Integrity Working Group in this Phase II include:

- Type of credit: specifies whether a CCP represents a ton of CO2 which has been avoided/reduced or removed.

- Removal/reduction method: identifies the methodology used in removing or reducing CO2 – for example, nature-based or tech-based methodology types.

- Storage method: allows buyers to select credits with storage methods that may carry a lower reversal risk.

- Co-benefits: buyers may want credits that deliver wider benefits beyond the specific removal or reduction project, such as achieving Sustainable Development Goals or achieving broader ESG targets.

- Corresponding adjustments: buyers may require CCP credit with letters of authorisation from host countries specifying that steps have been taken to avoid issues such as the double counting of credits.

- Exchanges will be capable of creating contracts for CCP credits from different standard setters that share common underlying additional attributes. In the OTC market, additional attributes will credits to have standard supplements with price signals from the exchange market.

- Specifically labelled CCP credits will permit corporate participants to take a more targeted approach to achieving their corporate claims, whether that be achieving net zero, carbon neutral status or individual corporate claims. This will have a corresponding effect on suppliers, who will be incentivised to develop projects in line with the demand profile in the market.

- The new governance body will ultimately be responsible for finalising the recommendations of the Credit-level Integrity Working Group and will provide oversight over standard setters to ensure credits are labelled appropriately.

- As the carbon markets grow, the governance body may need to consider how it strikes a balance between retaining the flexibility to adjust and update CCP credit labels as technologies and climate objectives shift, whilst also providing a consistent and reliable identification system for buyers and sellers.

Public Consultation Survey Questions

The Phase II Consultation will be open between 21 May and 21 June 2021, with the Taskforce strongly encouraging market participants to express their views on the Phase II Consultation Documents and proposals by completing the structured public consultation survey at the back of the Report and/or submitting an open letter with feedback published on the Taskforce's website.

The Survey can be accessed at https://www.iif.com/tsvcm, with all survey responses (including which party provided the input) made public.

As mentioned above in relation to the new umbrella governance body, the Taskforce's advisory board also invites participants to express their interest in assuming roles on the new umbrella governance body, with the governance 'Terms of Reference' setting preliminary guidelines to inform recommendations on who could fulfil the relevant body roles.

Interested parties should consider the range of survey questions contained in the Phase II Consultation Documents in order to prepare for a potential submission of interest in July or August 2021. The Taskforce's advisory board will then recommend participants to act in the roles they have put themselves forward for in September 2021.

Concluding Remarks

Commentary

The feedback received from the market in response to the Phase II Consultation will be crucial in shaping the future direction of global voluntary carbon markets, especially in assessing the market's perspective on the role and importance of the proposed new umbrella governance body and its structural framework.

The position taken by standard setters on the proposed terms of use and CCPs will also be of particular interest. Likewise, the views of industry groups on the general trading terms and their adoption will be critical. Wide-ranging approval and adoption by industry players of the Taskforce recommendations will be necessary to help drive forward the legitimacy and speed up the growth of the voluntary carbon markets.

Further details regarding the Taskforce can be located here.

The Report can be located here.

Vic Sohal (Trainee Solicitor, White & Case, London) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP