The second Annual Report on the UK's National Security and Investment Act is the first to cover a full 12 months' operation and provides some valuable insights into the review process. We explore some of the key metrics and trends and what they mean for investors navigating the regime.

The second National Security and Investment Act 2021 ("NSIA") Annual Report was published on 11 July 2023, providing an overview of the regime's operations from April 2022 to March 2023 ("NSIA Report"). It is the second NSIA Report, but the first to cover a full year of the NSIA's operations and yields some valuable insights into a regime that has often been characterised as a black box for investors.

Overview: the NSIA in brief

The NSIA has been operational since January 2022 and has quickly cemented itself as a standard consideration in M&A deals. Transactions in the UK may require mandatory notification under the NSIA if the target engages in specified activities in one or more of 17 sensitive sectors – covering areas including defence, military & dual use, energy and communications. These are set out in detail in the National Security and Investment Act 2021 (Notifiable Acquisition) (Specification of Qualifying Entities) Regulations 2021 ("NSIA Regulations"). Even if a mandatory notification is not required, transactions may still be reviewed so investors are also able to submit voluntary notifications.

Once a filing is submitted, and accepted as complete, transactions will either be cleared within a 30-working day review period or subject to a call-in notice. A call-in notice signifies that the transaction will be subject to more detailed review. This triggers a 30-working day "assessment period", which may be followed by another 45-working day "additional period" (that can be further extended with the notifying party's consent).

Once the review is complete, transactions will either be cleared (via a "final notification") or subject to NSIA powers in the form of conditions or a potential prohibition (via a "final order"). Our more detailed overview of the NSIA, including notification triggers and timelines, is accessible here.

The NSIA Report

Notifications

During the first full year of the NSIA's operations, the Investment Security Unit received 866 notifications, with around one in five submitted on a voluntary basis. This is still somewhat below the 1,000 - 1,830 notifications that the government originally anticipated. In terms of review, clearance very much remains the norm, with over 90% of transactions cleared without call-in.

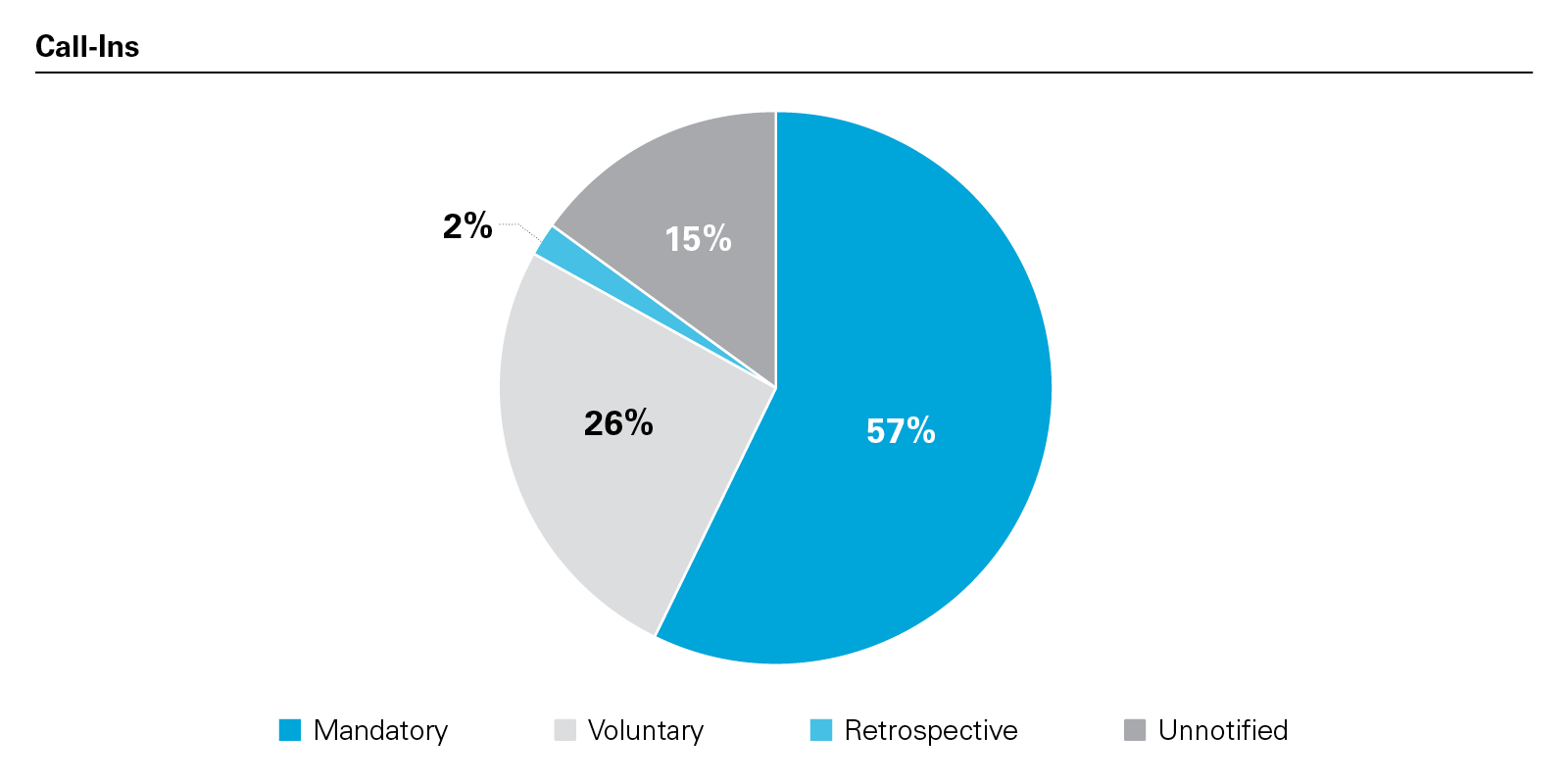

Call-In Review

Nearly 80% of the transactions subject to call-in review during the reporting period were cleared via a final notification (without conditions). Of the 65 call-in notices issued during the reporting period, 17 emanated from voluntary notifications and 10 were issued in respect of unnotified transactions.

View full image: Call-Ins (PDF)

View full image: Call-Ins (PDF)

Final Orders: Conditional and Prohibition Decisions

If the Secretary of State determines, following a call-in review, that a transaction poses a risk to national security, then a final order will be issued either imposing conditions on the deal, or prohibiting it entirely (which, in the case of unnotified deals that have completed, means unwinding of the transaction). There were 15 final orders imposed overall, representing about 20% of all transactions where a call-in decision was taken during the reporting period. Of these 15 final orders, five either prohibited or unwound the transactions under scrutiny. Final orders look set to stay the exception rather than the norm looking at the second quarter of 2023, with only one final order issued since 31 March 2023 (i.e., since the period covered in the NSIA Report).

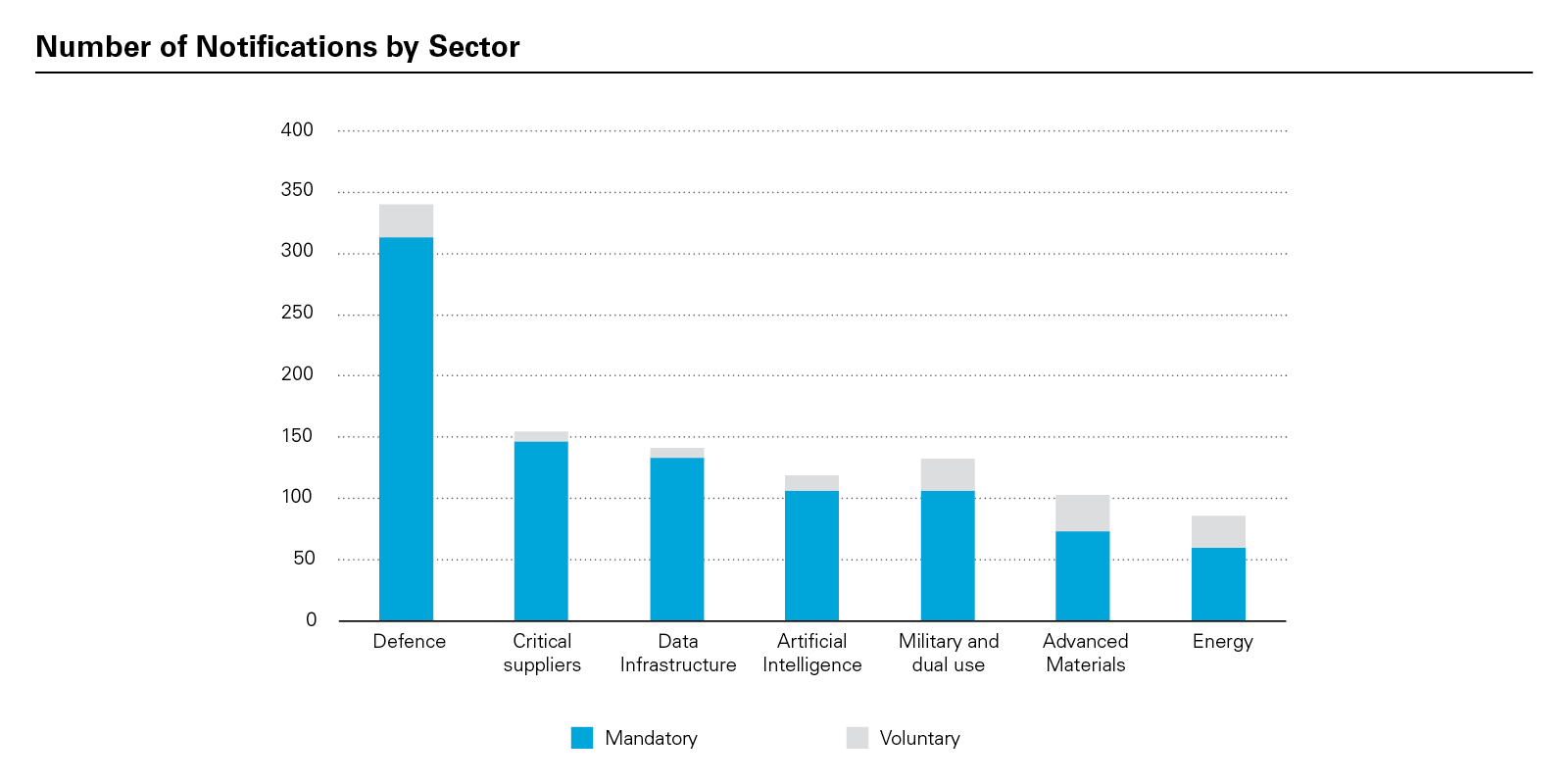

Sectoral Focus

The NSIA Report provides a breakdown of the sectors triggering the most mandatory notifications, voluntary notifications, call-ins, final notifications (i.e., clearance after call-in), and final orders (i.e., the imposition of conditions or prohibition). Mandatory notifications were most common in relation to defence (47%), critical suppliers to government (22%) and data infrastructure (20%). Voluntary notifications focused on advanced materials (18%), defence (17%), military & dual use (16%) and energy (16%). Transactions will often be notified based on multiple sectors, with, for example, defence and military & dual use often triggering simultaneously.

The prevalence of defence across all metrics is, according to the NSIA Report, "as one might expect" but will no doubt also reflect the breadth of the "Defence" heading under the NSIA Regulations. The Defence heading will capture companies at all tiers of any supply chain that ends in the provision of goods and services for defence or national security purposes in the UK. As NSIA guidance makes clear, this includes contractors and subcontractors who provide goods or services "with no clear military application".

View full image: Number of Notifications by Sector (PDF)

View full image: Number of Notifications by Sector (PDF)

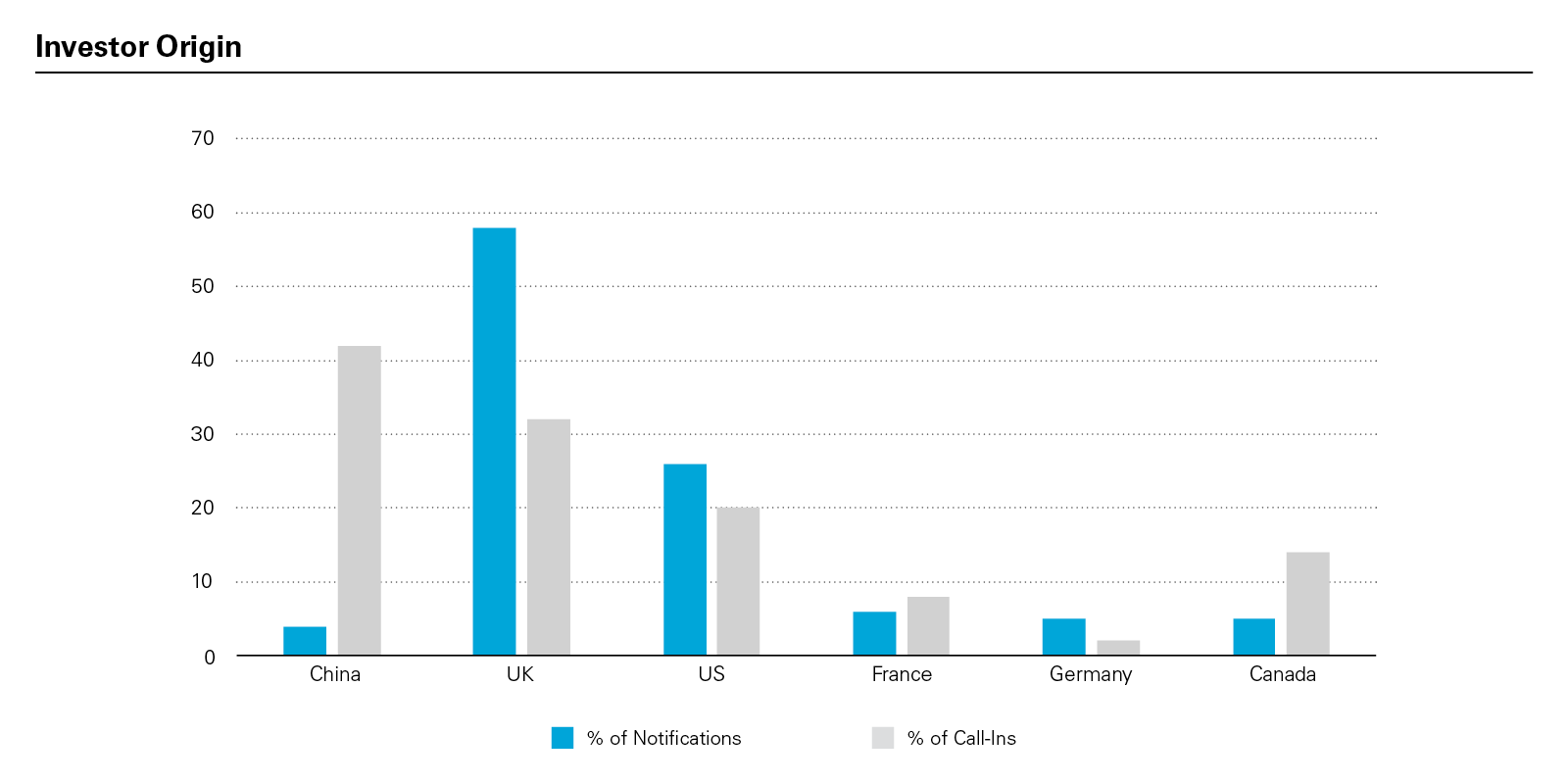

Investor Origin

The NSIA, somewhat unusually, does not take an investor's origin into account when determining whether a transaction will require notification or not. As such UK investors are subject to exactly the same notification requirements as overseas investors. Indeed, 58% of the accepted notifications listed the origin of investment as the UK.

Two key trends emerge from the NSIA Report in terms of investor origin. First, despite the Secretary of State's statements on agnosticism, there is a discernible China-focus, with Chinese investors responsible for just 4% of accepted notifications but 42% of call-ins. It is particularly striking, for example, that of the 15 final orders, 8 were issued to Chinese investors, including four of the five prohibition/unwinding decisions.

Second, UK investors cannot assume preferential treatment, with UK investors being the subject of 32% of all call-ins. This is consistent with the overall notification figures, where the UK accounts for 58% of all notifications accepted. However, co-investments by, for example, UK and Chinese investors will have the call-in attributed to both jurisdictions. This will at least in part account for the prevalence of the UK and the US in the call-in statistics.

"The NSI Act applies equally to all acquirers and does not target any particular origin of investment."

View full image: Investor Origin (PDF)

View full image: Investor Origin (PDF)

Penalties

The NSIA sets out various offences, including the completion of a notifiable transaction without approval. Such offences can attract penalties of up to £10 million or 5% of turnover (whichever is the higher). The NSIA Report states that the Secretary of State did not issue any penalties during the reporting period either for failure to notify or procedural breaches, suggesting a high degree of compliance.

Efficiency

The NSIA Report states that "[a]ll cases were decided within statutory timelines, providing welcome certainty for businesses". This is not as comforting as it may seem when estimating maximum timescales, however. The Investment Security Unit has been making increasing use of requests for information, which will stop-the-clock on those statutory time periods, and parties engaged in discussions around remedies will invariably agree to an extension of the additional review period rather than insist on the statutory deadline and risk prohibition. The acquisition of Newport Wafer Fab by Nexperia BV, for example, was called-in on 25 May 2022. Yet a final order was not published until 16 November 2022. That is over 120 working days between call-in and final decision, as compared to the statutory deadline of 75 working days.

Transparency

The NSIA Report helpfully includes some new categories of information that are not required by statute and were not included in the first NSIA Report. This includes a monthly breakdown of notifications, the breakdown between mandatory and voluntary notification numbers, and the number of call-in notices by investor origin. Even so, there is still a long way to go in terms of maximising certainty for investors in terms of ensuring transparency and predictability on the substance of NSIA review, something responsible Secretary of State Oliver Dowden MP has pledged to address.

Ruth Benbow (White & Case, Knowledge Manager, London) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2023 White & Case LLP