US public M&A in the first half of 2026 has been defined by transactions of exceptional scale. Deal volume softened, but boards pursued transformational scale across media, energy, real estate, banking and the AI stack, and competing proposals, unsolicited approaches and shareholder votes shaped outcomes on several of the half's largest transactions.

- Megadeals carry the market

- The H1 megadeal board

- Six sectors, six megadeals

- Contested and competing situations

- Predictions for the rest of 2026

- White & Case in the market

- Selected representations

Megadeals carry the market

+44%

Growth in value of US $100m+ deals year over year

Volume up just 16%

+149%

Surge in $5bn+ megadeal value

Megadeal volume +94%

12

$10bn+ deals announced globally in Q1

Most in any first quarter since 2008

$110bn

Paramount–Warner Bros. Discovery enterprise value

A topping-bid win

62

Global activist campaigns

Roughly two-thirds in the US

Reflects the latest published market data as of June 2026; half-year figures will be updated following quarter-end.

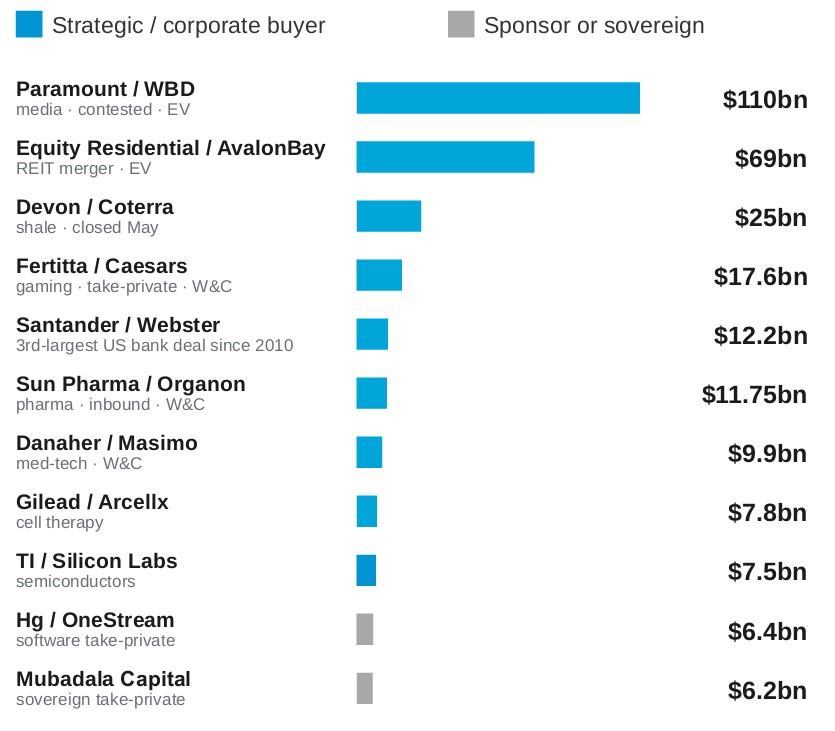

The H1 megadeal board

Selected US public deals announced Jan-Jun 2026, $ billion*

View the full image: The H1 megadeal board (PDF)

*Values as publicly reported per deal; a mix of enterprise and announced transaction values. Strategic buyers dominate the top of the board, with sponsor and sovereign capital (Hg, Mubadala) active in take-privates further down.

Six sectors, six megadeals

One headline transaction per sector, all converging on scale

Media & Entertainment

$110bn

Paramount / WBD

Paramount's $31.00/share cash offer determined superior to a signed Netflix all-stock merger after a tender offer and solicitation. Approved April 2026.

Energy

$25bn

Devon / Coterra

Closed May, creating a multi-basin shale major. AI-driven power demand keeps energy assets strategic.

Real estate

$69bn

Equity Residential / AvalonBay

Largest merger of the modern REIT era: all-stock merger of equals, ~180,000 units, ~$52bn equity cap.

Financial institutions

$12.2bn

Santander / Webster

Santander's first US retail bank acquisition in ~17 years; third-largest US bank deal since 2010. Received OCC approval June 2026.

Life sciences

$7.8bn

Gilead / Arcellx

On track for a banner year: Sun Pharma's $11.75bn move on Organon, Gilead / Arcellx in cell therapy, and a string of Eli Lilly pipeline acquisitions.

Technology & AI stack

$7.5bn

TI / Silicon Labs

AI infrastructure is the gravitational center: semis consolidation, a wave of cybersecurity deals, hyperscaler capex above $350bn/yr.

Contested and competing situations

Competing proposals, unsolicited approaches and contested shareholder votes shaped several of the largest situations in the half and its immediate run-up

Topping bid prevailed

$31.00 / share

Warner Bros. Discovery

Paramount's all-cash offer determined superior to the signed Netflix deal (Feb 26-27, 2026); shareholders approved Apr 27. Close targeted Q3.

Shareholder vote failed

Sale voted down

Core Scientific

Shareholders, led by Two Seas Capital, voted against CoreWeave's ~$9bn all-stock acquisition on Oct 30, 2025; agreement terminated same day.

Signed · FTC 2nd request

~$5.5bn cash & stock

UniFirst

Cintas's third approach culminated in a merger agreement (Mar 10, 2026); the Croatti family signed a support agreement and shareholders approved Jun 12. FTC Second Request issued; close expected H2.

Rebuffed · pursuit ended

United approach declined

American Airlines

United's CEO confirmed in April 2026 that he had approached American about combining two of the four largest US carriers. American declined to engage, calling such a combination anticompetitive. United subsequently ended its pursuit.

Our perspective

A signed merger agreement secures a transaction; it does not assure its completion. Through the first half of 2026, executed deals encountered competing bids, shareholder opposition and price pressure prior to closing, placing a premium on deal certainty; boards that had planned for each from the outset preserved the most optionality.

Predictions for the rest of 2026

The White & Case US Public M&A team's outlook for the remainder of the year

Deal values & volume

↑ Elevated

Deal values to remain elevated, with megadeals accounting for an outsized share of activity even as announcement counts stay selective. Boards to concentrate capital on fewer, larger strategic moves.

Bidders

→ Steady

Strategics to remain dominant at the top of the market. Private equity, infrastructure and sovereign capital to stay active in take-privates and consortium structures on the largest transactions.

Sectors

↑ Rising

Technology and AI infrastructure to lead: compute, power, data and connectivity assets command strategic premia. Continued strength in life sciences, financial institutions and energy.

Deal features

↑ Rising

More unsolicited approaches and competing offers testing signed transactions. Greater shareholder scrutiny of announced deals, including price-based dissent, and more activist campaigns built on M&A theses.

Regulatory

↑ Rising

Merger notification volumes rising as boards pursue larger-scale consolidation. Review timelines, CFIUS and non-US regimes remain the key gating items on complex and cross-border deals.

Risks & preparedness

→ Watch

Geopolitical volatility (energy prices, trade friction, sharp market moves) can narrow financing windows quickly. Volatility rewards prepared bidders, and prepared targets.

White & Case in the market

Recognized across the leading M&A league tables and award programs

Top 10

Global M&A adviser by deal value & volume

Mergermarket

Elite

Ranked in Corporate/M&A: The Elite, USA, Nationwide

Chambers USA

#1

M&A legal adviser for power-sector deals by value

GlobalData

#1

Global law firm for shareholder activism

Bloomberg League Tables

2026

Dealmaker of the Year, Michael Deyong

The American Lawyer

Selected representations

Publicly announced US public company and related strategic transactions, 2025-2026

$17.6bn

Fertitta Entertainment

Advising on the all-cash acquisition of Caesars Entertainment (NASDAQ: CZR): $31.00/share, announced May 2026.

$9.9bn

Masimo Corporation

Advised Masimo (NASDAQ: MASI) on its acquisition by Danaher, completed June 2026.

-$4bn

DigitalBridge Group

Advising the transaction committee of the DigitalBridge (NYSE: DBRG) board on the company's sale to SoftBank, squarely on the half's AI-infrastructure theme.

$12bn

NRG Energy

Advised NRG (NYSE: NRG) on its acquisition of a power portfolio from LS Power, closed January 2026.

~$40bn

EchoStar Corporation

Advising EchoStar (NASDAQ: SATS) on spectrum transactions: the ~$23bn AT&T and ~$17bn SpaceX sales.

Proxy contest

Sturm, Ruger & Co.

Advised Sturm Ruger (NYSE: RGR) and its board on the successful resolution of a proxy contest by Beretta Holding, announced May 2026.

$11.75bn

Sun Pharma

Advising on its acquisition of Organon (NYSE: OGN), the largest pharma deal of the half.

$16.4bn

Calpine Corporation

Advised on the acquisition by Constellation Energy, plus assumption of ~$12.7bn net debt.

£9.9bn

Wells Fargo Securities

Advised Wells Fargo Securities, as lead financial adviser to Schroders plc, on the £9.9bn takeover by Nuveen, announced February 2026.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2026 White & Case LLP