Recent disruptions in the global food supply chains have highlighted Africa's urgent need to become self-sufficient in food production. Traditionally, the continent has turned to small-scale community-based agricultural projects as a means to meet its food needs. But feeding a population of more than 1.2 billion people requires more than communal farming; it calls for a paradigm shift toward agriculture on an industrial scale. Our milestone tenth edition of Africa Focus opens with an article exploring obstacles to large-scale farming in Africa and how they may be overcome to secure funding required for such agricultural megaprojects.

While Angola has entered an ambitious plan to diversify its economy, it remains heavily dependent on its oil & gas industry. Hydrocarbon revenues are crucial for funding Angola's commitments under the Paris Agreement, but also for diversifying the country's economy and improving the livelihoods of its citizens. Our second article looks at the latest developments in Angola's oil & gas sector, including increased M&A activity and a three-well offshore exploration project at a depth of 3,628 meters (11,903 feet) below mean sea level—a new world record water depth set in 2021.

Africa is home to many of the world's most biodiverse regions, including eight of the 36 recognized global biodiversity hotspots. The Congo rainforests have also overtaken the Amazon as the most significant carbon sink on Earth. Our third article highlights the scale of the challenge of biodiversity protection in Africa and options to fund it.

Trade ties between Africa and the United States are seeing something of a revival as the US seeks to revitalize its economic engagement on the continent. The US African Growth and Opportunity Act (AGOA) is one such pivotal agreement that is due to go before the US Congress in 2025.

Africa holds a remarkable 30 percent of the world's mineral reserves, yet it only accounted for less than 10 percent of global mining exploration spending and less than 5 percent of the sector's global revenue in 2022. Many of Africa's minerals are vital for reducing carbon emissions and transitioning to renewable energy. Developing these reserves sustainably is crucial for Africa's economies. Our final article examines how mining companies across Africa continue to find financing for the development of their projects.

Africa's agricultural revolution: From self-sufficiency to global food powerhouse

Africa's agricultural revolution: From self-sufficiency to global food powerhouse

Among its many intricately interlinked challenges, Africa faces burgeoning cities and increasing numbers of rural mouths to feed. But these challenges are not insurmountable: With agriculture at the core of the continent’s economic transformation, Africa has the potential to become a global agricultural powerhouse and a net exporter of food.

*Stephen Pickup, Head of Agriculture at Traditum Private Equity, co-authored this publication.

US$1 trillion

Africa’s food and agriculture market could increase from US$280 billion a year in 2023 to US$1 trillion by 2030

Africa has 60 percent of the world's uncultivated arable land. The agriculture sector accounts for 35 percent of Africa's GDP and employs more Africans than any other sector. So why does Africa spend a staggering US$78 billion of scarce foreign currency on food imports each year, with some countries such as Zimbabwe, Guinea and Sudan exceeding 100 percent of their annual foreign currency receipts? Why in 2020 did more than 20 percent of Africans face hunger—a figure twice as high as any other region in the world? Why is it that approximately 80 percent of the continent's food supply still comes from small-scale farmers, many still practicing subsistence agriculture?

The 2030 Agenda adopted by the United Nations General Assembly on September 25, 2015, notes the need to "devote resources to developing rural areas and sustainable agriculture and fisheries…"; to "account for population trends in national, rural and urban development strategies and policies"; to "increase investment in rural infrastructure, agricultural research"; and to "support positive economic, social and environmental link between urban, peri-urban and rural areas". Agricultural aspirations for Africa are set out further by the African Union (AU) "Agenda 2063: The Africa We Want," which calls for accelerated agricultural growth and transformation, leading to shared prosperity and improved livelihoods. Although such global and pan-African statements of intent are crucial, they must be followed by concrete national regulations and policies if African agriculture is to attract the scale of investment required to become a net exporter of food.

With agriculture at the core of Africa’s economic transformation, the continent has the potential to become a global agricultural powerhouse and a net exporter of food

Among many other intricately interlinked challenges, Africa faces burgeoning cities and increasing numbers of rural mouths to feed. Between 1990 and 2021, the rural population of sub-Saharan Africa experienced a shift in both proportion and magnitude. While the percentage of the rural population decreased from 72 percent to 58 percent over the period, the actual number of rural residents increased significantly, surging from 374.5 million to 687 million.

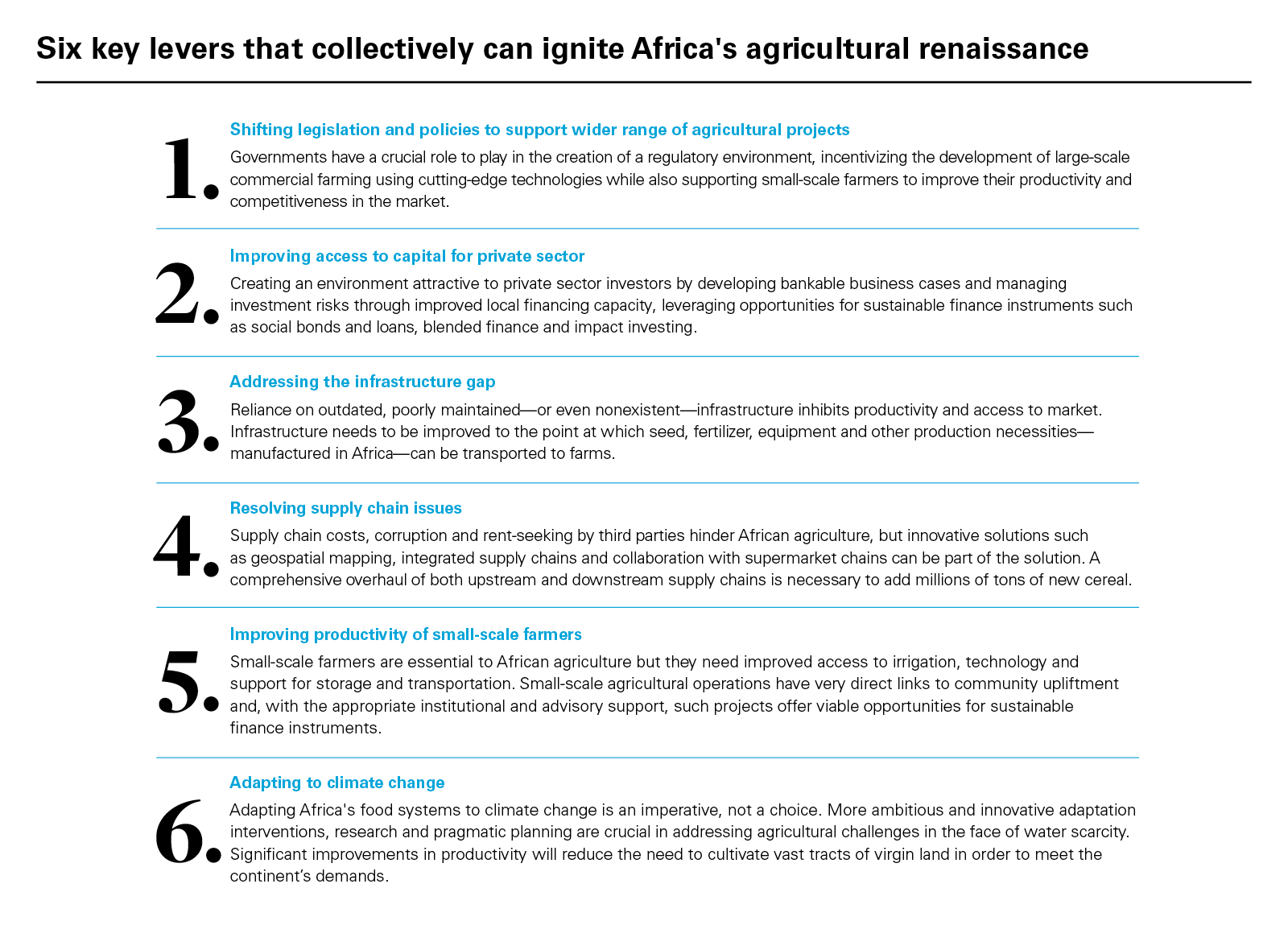

These challenges are not insurmountable, though. Africa has the potential to be a global agricultural powerhouse and a net exporter of food, with agriculture being a core driver of the continent's economic transformation. According to the African Development Bank, Africa's food and agriculture market could increase from US$280 billion a year in 2023 to US$1 trillion by 2030. But what would it take for Africa to emerge as a prominent global agricultural force? There are six levers that, when applied collectively, can trigger the agricultural renaissance in Africa that is necessary to achieve this vision.

Shifting legislation and policies to support wider range of agricultural projects

Impact investors being involved not only encourages new investors to come in, but they have capacity to support developers to bring about design improvements that commercial financial institutions cannot

An African agricultural renaissance will require a shift in national development policies from supporting a small number of mostly export-focused crops—cotton, cocoa beans and coffee—to prioritizing a wider range of agricultural products for consumption on the continent. Agricultural exports are crucial, as they generate valuable foreign currency. A significant portion of Africa's cross-border trade is between African countries, which is also vital in fostering pan-African food security. In 2018, intra-African trade accounted for 15 percent of exports and, in turn, 15 percent of that was in agricultural products. The African Continental Free Trade Area (AfCFTA), established in that same year, will—in time—no doubt significantly enhance this flow of agricultural products across African borders. Improved customs processes at border crossings will help minimize the volume of produce spoiling in transit. Moreover, processing such exported goods locally rather than exporting raw products would increase revenues and create new job opportunities.

Improving access to capital for private sector

The COVID-19 pandemic wreaked havoc upon Africa's fiscal health, but it has not diminished the needs of the continent's agricultural sector or the urgency for them to be effectively met. Through the Comprehensive African Agricultural Development Programme (CAADP), African Union member states committed to a minimum of 10 percent of their government expenditure toward agriculture. In 2021, however, the average government expenditure on agriculture in Africa stood at a mere 4.1 percent.

Access to credit is a major impediment to private sector investment in African agriculture. According to the African Development Bank, the estimated current financing shortfall ranges between US$27 billion and US$65 billion annually. Even more direly, the Commercial Agriculture for Smallholders and Agribusiness (CASA) program—a flagship initiative of the UK Foreign, Commonwealth & Development Office—estimates the financing gap to be in excess of US$1 billion, based on the demand of US$160 billion, minus the current provision of US$54 billion by banks, impact investors and other financial intermediaries.

US$78 billion

Africa spends a staggering US$78 billion of scarce foreign currency on food imports each year

Impact investors also play important roles. According to Philippa Viljoen of the impact investment firm InfraCo Africa, "Impact investors being involved not only encourages new investors to come in, but they have capacity to support developers to bring about design improvements that commercial financial institutions cannot. This can make the difference between a project being bankable, or not."

The CASA report proposes four long-term strategies to bridge the funding gap: (i) grow more small agribusinesses into commercially viable projects to anchor local bank financing; (ii) develop capacity, incentives and infrastructure for local banks and funds to profitably support smaller, less commercial agribusinesses; (iii) enhance the effectiveness of blended finance instruments; and (iv) build infrastructure around climate finance. These strategies are enormous both in scope and in scale. Transforming them into tangible reality will depend heavily on coordinated action from stakeholders within the agricultural finance ecosystem.

Small-scale agricultural operations have very direct links to community upliftment. With the appropriate institutional and advisory support and compelling business cases, such projects offer viable opportunities for sustainable finance instruments such as social bonds and loans, blended finance and impact investing, and can become attractive investment options for institutional investors.

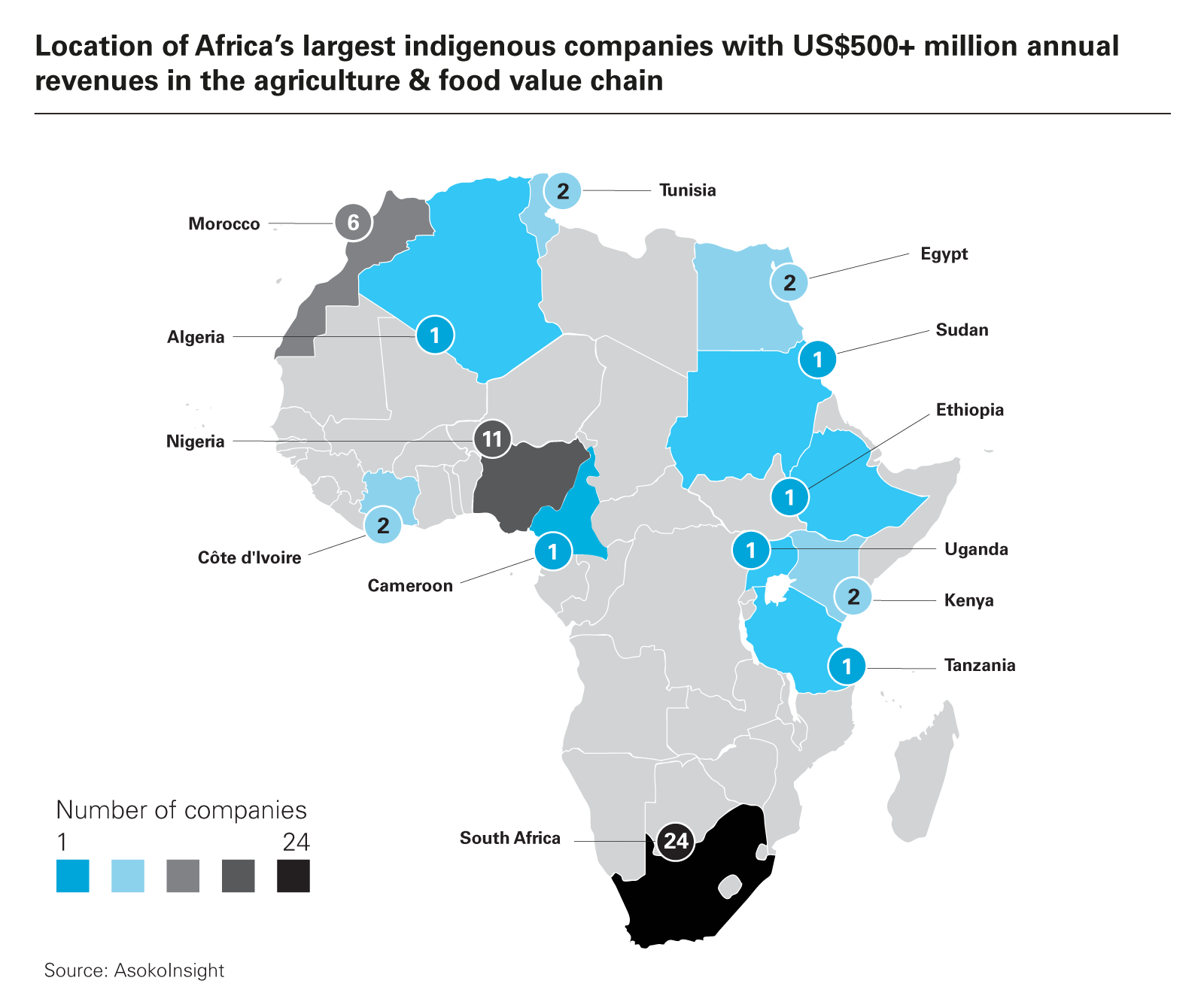

Within Africa's agriculture and food & beverage sectors, there are currently 56 companies with annual revenues above US$500 million, of which 14 companies have turnovers in excess of US$1 billion. Such larger-scale agro-industrial enterprises are better placed to attract their own capital, and their future seems bright. Some of the world's largest agriculture companies—including the three biggest players, Cargill, ADM and Bayer—also have significant operations in Africa.

In 2021, the average government expenditure on agriculture in Africa stood at a mere 4.1 percent

The infrastructure gap in Africa is well documented, and it impacts agriculture as significantly as it does other sectors. The reliance on outdated, poorly maintained—or even nonexistent—infrastructure inhibits productivity at least as much as other institutional challenges, such as weak governance, onerous regulation and lack of access to finance.

Poor road, rail and harbor infrastructure hinders farmers from being able to get their goods to market, and add as much as 30 to 40 percent to the costs of goods traded among African countries. While investment in African infrastructure projects has seen a general increase in recent decades, the reality remains that fewer than 10 percent of infrastructure projects in Africa reach financial close, with 80 percent failing at the feasibility and business plan stage. Lack of clarity about the commercial viability, political and currency risk, counterparty and regulatory risk, and lack of exit opportunities are all factors in such a high rate of failure.

Involvement of credible development finance institutions provides assurance that due diligence has been rigorous and the overall approach prudent, which enhances the probability of closure, and proper risk mitigation instruments help improve the credit rating of the borrower, hence the cost of finance.

Additional cost to goods traded between African countries because of poor road, rail and harbor infrastructure

Supply chain costs and related issues are a major obstacle to the renaissance of African agriculture. Making food supply chains more efficient and profitable requires reliable and efficient delivery of upstream goods and services, as well as downstream delivery of the goods to market. One notable example is Releaf, a Lagos-based company that uses cutting-edge technologies, including geospatial mapping, to identify optimal locations for supply chain infrastructure and to bring processing capacity directly to palm nut farmers in Nigeria, eliminating the need for these farmers to rely on large factories, located too far away to be affordably reached.

Rent-seeking by third parties—which can sometimes extend to corruption—can increase the costs of doing business, both upstream and downstream, and discourage investment into African agriculture projects.

While regulatory reform and institutional enhancement will help reduce such practices, some large-scale farming enterprises have resorted to resolving this challenge through vertical integration of upstream and downstream supply chain components into their own businesses, rather than relying on external parties. The emergence of large-scale supermarket chains working directly with their suppliers to improve supply chain efficiencies is also helping to alleviate some of the downstream challenges.

Improving productivity of small-scale farmers

US$ 1,526

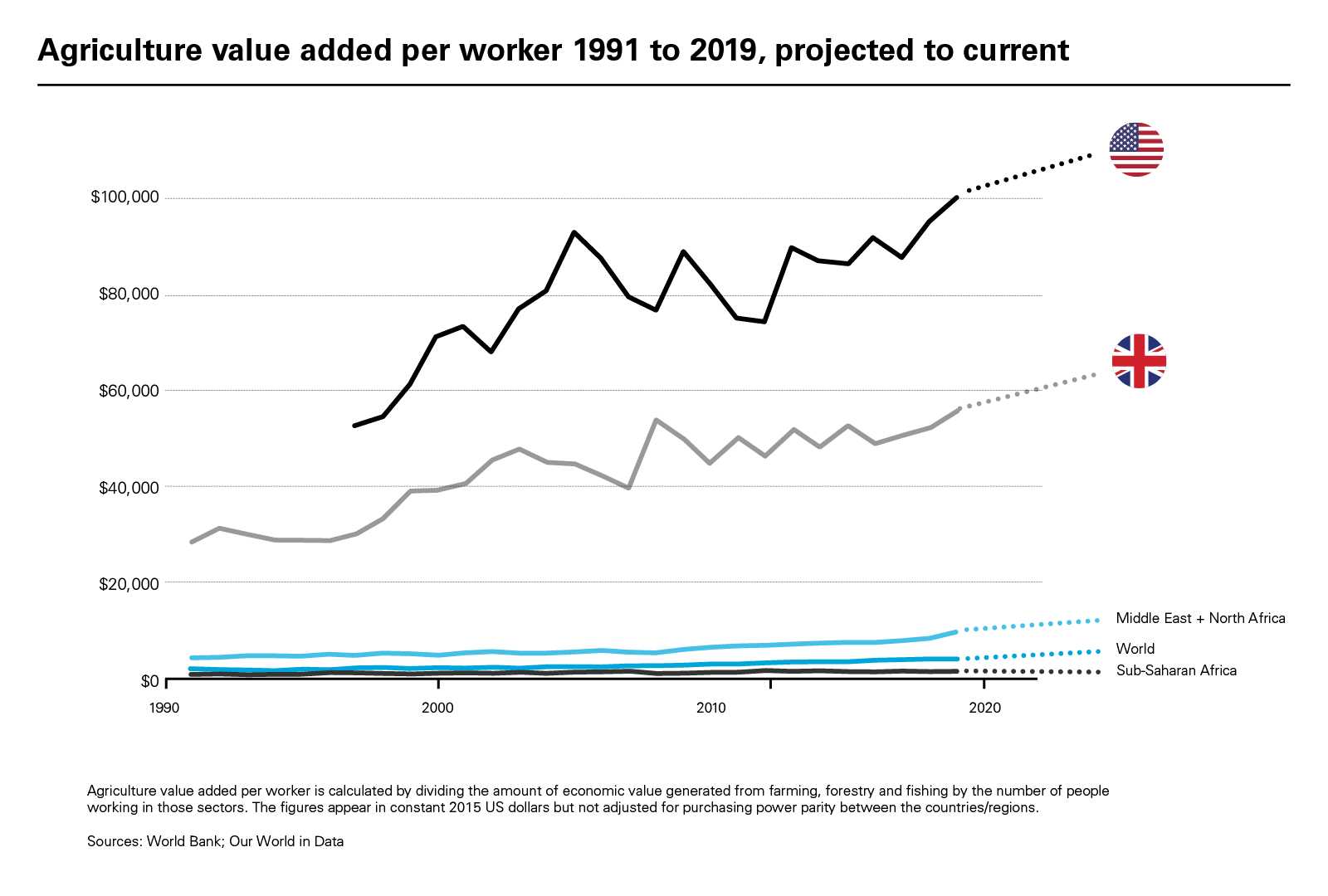

The agricultural value added per farmworker in sub-Saharan Africa was a mere US$1,526 in 2019, in stark contrast with that of a US farmworker, which exceeded US$100,000

Small-scale farmers will remain crucial to African agriculture for years to come, but they are facing significant pressures. Both small- and medium-scale farming enterprises are focusing almost exclusively on markets immediately local to them. These farmers need better access to irrigation and technology to improve their productivity and farming practices. Small-scale farmers also need support in storing and transporting their produce to market. Centralized entities that are properly managed—rather than individual farmers themselves—would be far better positioned to attract funding and deliver results.

of cereals have been displaced in Africa due to the situation in Ukraine

Adapting Africa's food systems to climate change is an imperative, not a choice. If global temperatures rise by 2° to 3° Celsius above pre-industrial levels, as current trends suggest, disruption to African food security will be profound—potentially catastrophic—for those already struggling with hunger. Even on the 1.5° Celsius trajectory proposed by the Intergovernmental Panel on Climate Change (IPCC) as a maximum, more ambitious and innovative adaptation interventions are needed to avoid widespread famine and forced migration in coming decades. Research and planning are required to assess how Africa's food security is to be achieved amid diminished agricultural potential, particularly in the face of water scarcity.

From self-sufficiency to global food powerhouse

Russia's invasion of Ukraine has had a devastating impact on Africa's food security, and has triggered a shortage of at least 30 million tons of food across the continent, especially wheat, maize and soybeans. Just replacing the 30 million tons of cereals that have been displaced due to the situation in Ukraine means approximately 36,000 square kilometers of farmland would be needed if Africa were to achieve the same cereal yield of 8.27 tons per hectare as in the United States. However, at Africa's current cereal yield of 1.75 tons per hectare, the required farmland would exceed a staggering 171,000 square kilometers. Improving yield is a key priority.

Enabling Africa to feed itself and realize its potential of becoming a global agricultural powerhouse requires development of large-scale commercial farming using cutting-edge technologies. It also requires effective support to small-scale farmers to enhance their production and competitiveness in the market. These need not be conflicting priorities. The challenges are significant but not insurmountable.

This implies mechanization on a grand scale. In 2019, the agricultural value added per farmworker in the US exceeded US$100,000. In sub-Saharan Africa, it amounted to a mere US$1,526. Over the past three decades, Africa tripled its cereal production. But its yield barely increased, with almost all the growth resulting from the expansion of cultivation areas. This stands in stark contrast to Southeast Asia, which has also significantly increased its cereal output, but the gains have been almost entirely through yield improvement. Significant improvements in productivity will also benefit Africa's biodiversity, as it will reduce the need to cultivate vast tracts of virgin land in order to meet the continent's demands.

A comprehensive overhaul of both upstream and downstream supply chains will be necessary to add tens or hundreds of millions of tons of new cereal production in Africa. Infrastructure will need to be improved to the point at which seed, fertilizer, equipment and other production necessities can be transported to farms. Ideally, these agricultural necessities should be manufactured in Africa, requiring the construction of new factories with their own supply chains. Downstream, infrastructure bottlenecks must be cleared to facilitate commerce and distribution, establish new agro-processing plants and create new wholesale and retail businesses.

The debt raised to finance African agricultural projects can be serviced through the reduction in expenditures currently allocated to food imports. Since demand for food is perennial, strong business cases are possible if the structural impediments to production can be overcome.

Investment in agrifoodtech saw a 44 percent decline globally from 2021 to 2022. Not so in Africa, where it has grown substantially in recent years, from US$185 million in 2020 to US$482.3 million in 2021, and to US$640 million in 2022. However, this investment represents less than 1 percent of the total amount spent on imported food.

In addition to overcoming structural obstacles to production, planning needs to be pragmatic, focusing on large-scale agrifood projects, developing bankable business cases and managing investment risks to create an environment attractive to private sector investors. Governments have a crucial role to play in this by taking responsibility for the creation of a regulatory environment supportive of a substantially expanded agricultural sector in Africa. The shift toward large-scale agriculture, however, must not come at the expense of small-scale farmers, who are an integral part of Africa's agricultural landscape.

There has never been a more opportune moment for a fundamental shift in Africa's agricultural sector. Africa should be able to feed itself with its locally produced food; it should also be contributing significantly to feeding the world.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: Six key levers that collectively can ignite Africa's agricultural renaissance (PDF)

View full image: Six key levers that collectively can ignite Africa's agricultural renaissance (PDF)

View full image: Africa’s largest indigenous companies with US$500+ million annual revenues in agriculture & food chain (PDF)

View full image: Africa’s largest indigenous companies with US$500+ million annual revenues in agriculture & food chain (PDF)

View full image: Modern commercial agriculture, at scale in Africa, will require enhancement of all aspects of the value c (PDF)

View full image: Modern commercial agriculture, at scale in Africa, will require enhancement of all aspects of the value c (PDF)

View full image: Agriculture value added per worker 1991 to 2019, projected to current (PDF)

View full image: Agriculture value added per worker 1991 to 2019, projected to current (PDF)

View full image: Amount of long-leased (typically to foreign entities) as a percentage of all arable land (PDF)

View full image: Amount of long-leased (typically to foreign entities) as a percentage of all arable land (PDF)