The White & Case Foreign Subsidies Regulation Quarterly (FSRQ) is an information and discussion resource regarding the EU Foreign Subsidies Regulation. FSRQ provides updates on recent enforcement activity and trends.

Below is a selection of recent developments and the key FSR statistics for M&A deals.

- A ramp-up in FSR enforcement

- Conditional clearance of ADNOC / Covestro

- Simplified filings for PE funds

- Upcoming FSR guidelines

- Upcoming FSR report and possible FSR reform

- Key statistics – M&A deals

A ramp-up in FSR enforcement

A ramp-up in FSR enforcement is underway, including a number of new ex officio probes with a focus on China, by both European Commission (EC) services in charge of the FSR - DG Competition and DG GROW.

The EC's recent dawn raids and in-depth investigation openings show a clear ramp-up in enforcement. The first use of the 'call-in' power confirms that below-threshold tenders are no longer off the hook.

Kasia Czapracka | Partner

On the DG Competition side:

- First ex officio in-depth investigation into China's airport-scanner manufacturer, Nuctech. On 11 December 2025, the EC opened an in-depth investigation into Nuctech. The investigation follows a probe launched in April 2024, accompanied by dawn raids at Nuctech's premises in Poland and the Netherlands; and

- Dawn raid of the Chinese e-commerce provider, Temu. On 10 December 2025, the EC reportedly raided Temu's premises in Ireland, as part of a probe into the company's possible non-EU subsidies.

On DG GROW side:

- New in-depth investigation into China Railway Rolling Stock Corporation ("CRRC"). On 5 November 2025, the EC opened a new investigation into CRRC, the Chinese State-owned rail equipment manufacturer, in relation to its participation in a Lisbon light-rail vehicles tender. The case was triggered by an FSR filing to the EC by a consortium led by Mota Engil, which included CRRC's Portuguese subsidiary. This is not the first time the EC has investigated CRRC. In 2024, the EC opened its first in-depth investigation under the FSR public procurement module, into CRRC's tender offer for rail equipment supply to Bulgaria. Back then, CRRC withdrew from the tender and the investigation was halted as a result, without any final finding of the EC on substance. The focus of the new investigation into CRRC appears to be similar, i.e., has the CRRC received subsidies from China that could distort the procurement process in the EU?;

- First "call-in" of the EC for a public tender below the threshold. In November 2025, the EC reportedly exercised for the first time its "call-in" powers under the FSR, for a public tender below the €250 million notification threshold. Neither the name of the tender nor the company involved have been disclosed; and

- Other FSR probes. The EC has made public statements that it is looking into the new nuclear project in Czechia, under the FSR. To date, however, no formal investigation has been opened.

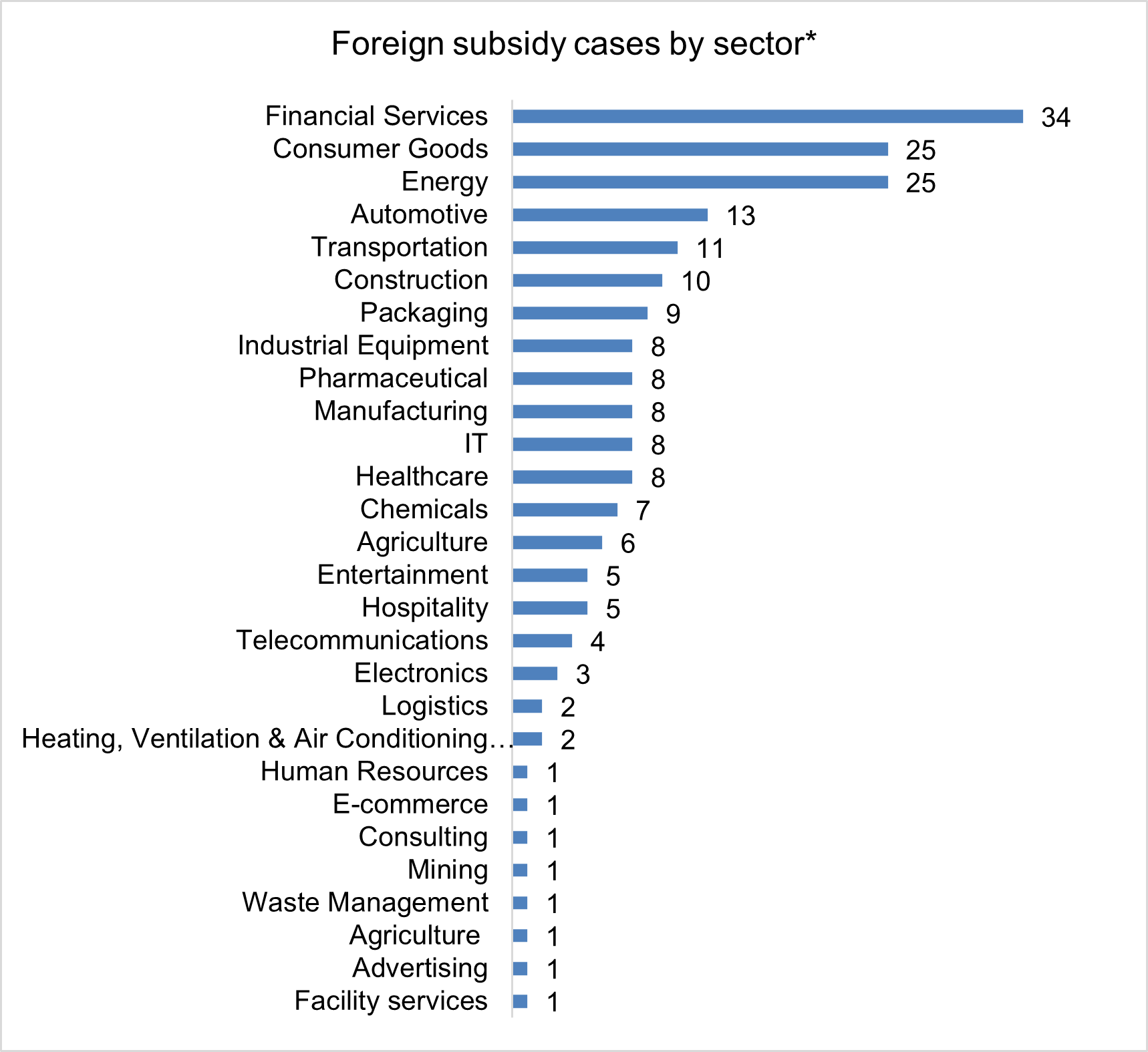

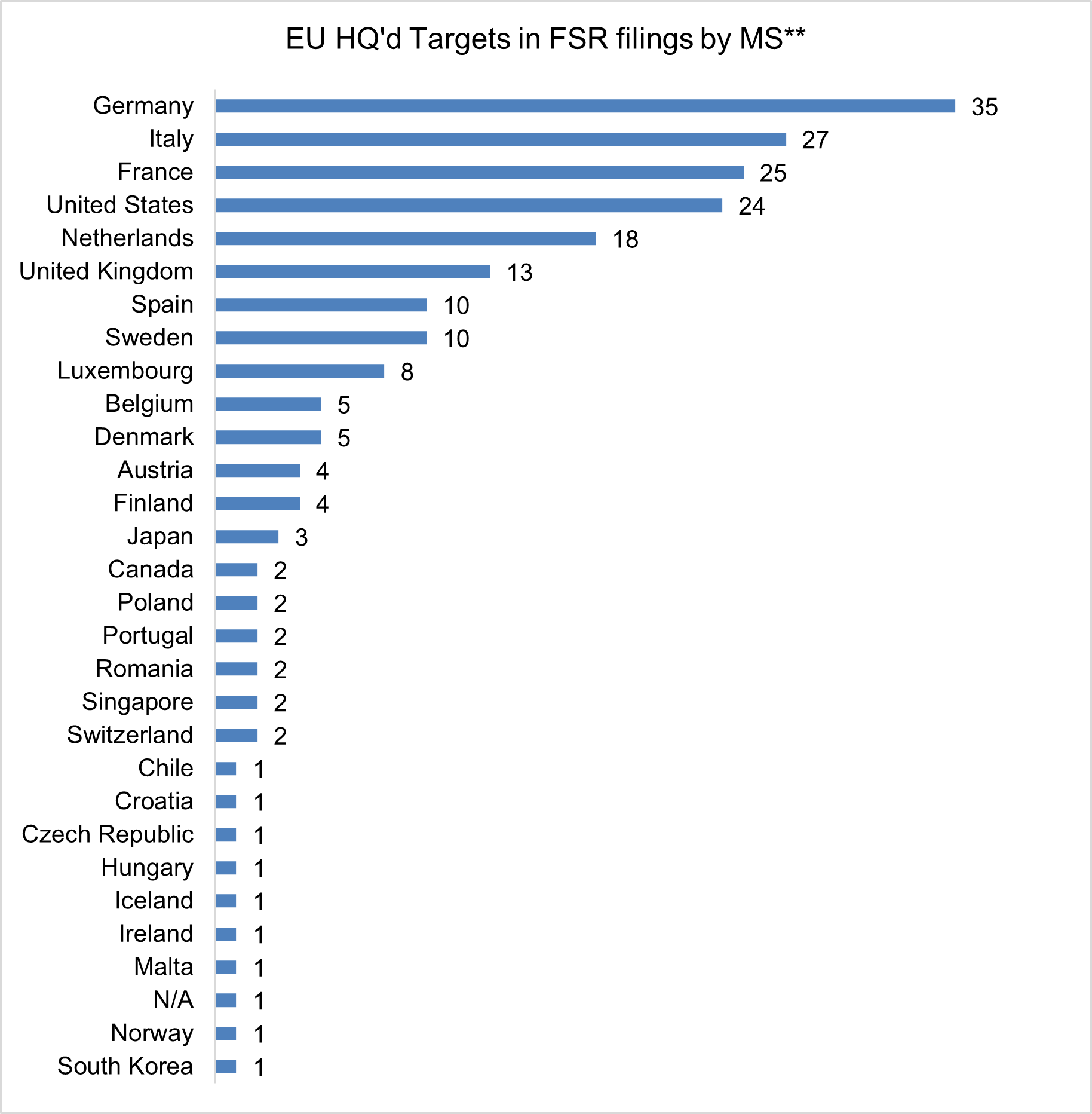

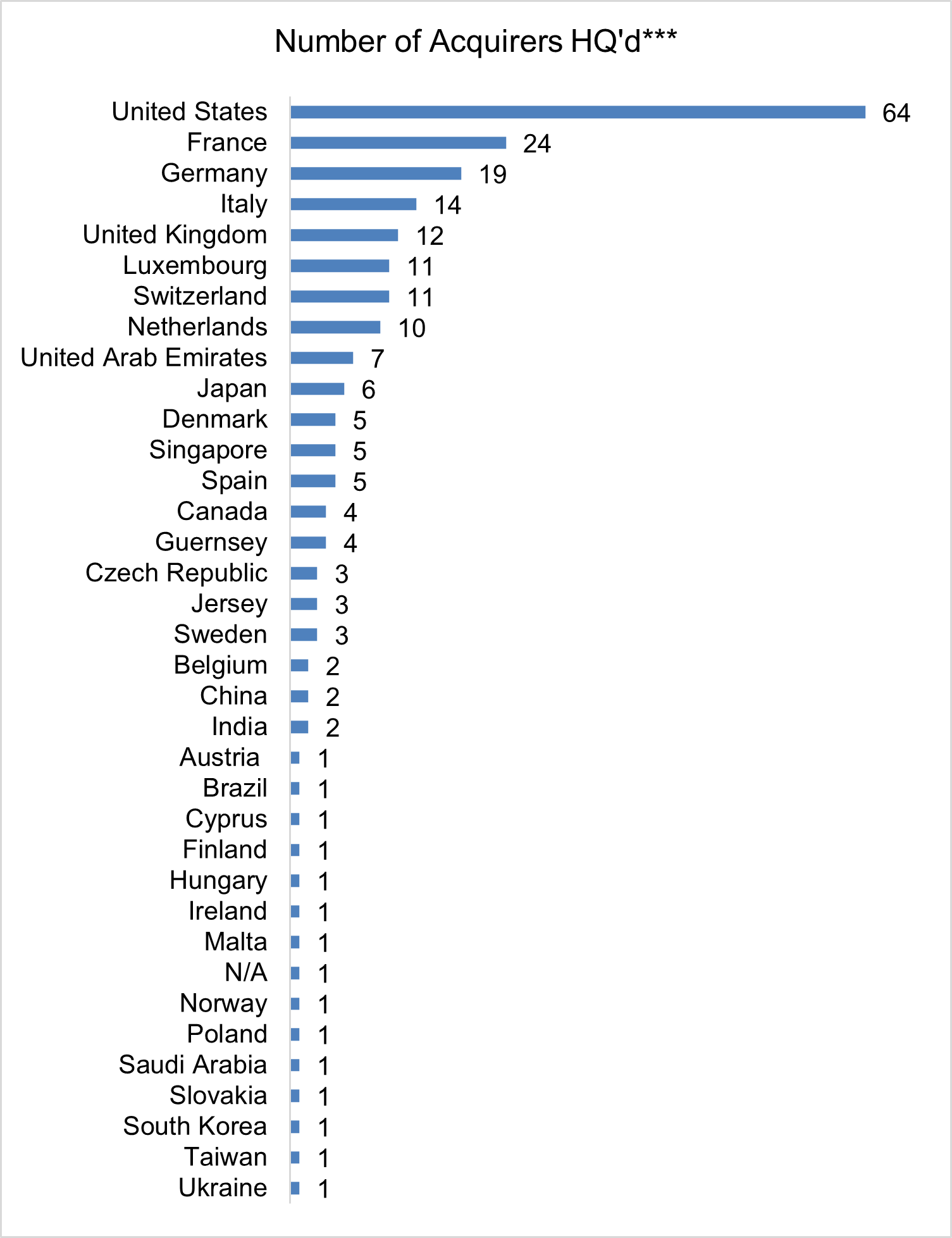

To date, the EC has received 200+ filings (8/month), with the top sectors being financial services, energy, and consumer goods. Top non-EU buyers are the US, UK, and UAE, while the main targets are based in Germany, Italy, and France.

Irina Trichkovska | Counsel

Conditional FSR clearance of ADNOC / Covestro

Conditional clearance of Abu Dhabi National Oil Company (ADNOC)'s €14.7 billion acquisition of German chemical giant, Covestro.

On 14 November 2025, the EC conditionally approved the transaction following four months of in-depth FSR investigation (and a long pre-notification process of around six months). The EC's allegations focused on the non-EU subsidies available to ADNOC, including, but not limited to, an unlimited State guarantee through an exemption from the ordinary bankruptcy rules. The EC also investigated if the planned capital injection into Covestro would constitute a subsidy. To address the EC's concerns, ADNOC committed that (i) its Articles of Association will not include any exemption from UAE bankruptcy laws for a period of ten years, and (ii) Covestro will grant access to certain sustainability-related licensed patents on transparent terms to eligible market participants for an unlimited duration.

This marks the second in-depth FSR review of a merger transaction —after the conditional clearance of e& / PPF in 2024 — both involving UAE-State linked buyers.

The EC's new guidance for PE funds marks a welcome shift towards pragmatism, significantly reducing the reporting burden for private equity sponsors and simplifying FSR notification requirements.

Marika Harjula | Counsel

Simplified FSR filings for PE funds

On 16 September 2025, the EC updated Question 26 of its FSR Q&As to simplify the disclosure requirements for PE funds.

- Specifically:

- Non-EU State-related Limited Partners (LPs) are no longer deemed "likely distortive" if:

- More than 50% of LP commitments are private LPs in the acquiring fund(s);

- They invest on the same terms as private investors; and

- They are passive investors and have no say over strategic decisions.

- If the funds of the non-EU State-related LPs in the PE fund from a single non-EU country exceed €45 million / 3 years, the PE fund needs to disclose:

- Non-EU State-related Limited Partners (LPs) are no longer deemed "likely distortive" if:

Upcoming launch of the FSR Guidelines

(To be published by 13 January 2026)

The FSR Guidelines are expected to provide further insight into the EC's approach to the notion of distortion, the balancing test, and the Commission's call-in powers for below-threshold M&A transactions. The draft text, published for public consultation in July 2025, received substantial feedback from more than 50 stakeholders.

James Killick | Partner

Upcoming FSR report and possible FSR reform

Under Article 52(2) of the FSR, by 14 July 2026, the EC is due to publish an FSR Report on its implementation and enforcement, to the European Council and the Parliament. Depending on the findings of the Report, the EC may propose legislative changes to the FSR, including an adjustment of the FSR thresholds for both M&A transactions and public procurement.

Strati Sakellariou-Witt | Partner

Key statistics – M&A deals

All statistics are updated as of 11 December 2025.

By sector

View full image

View full image

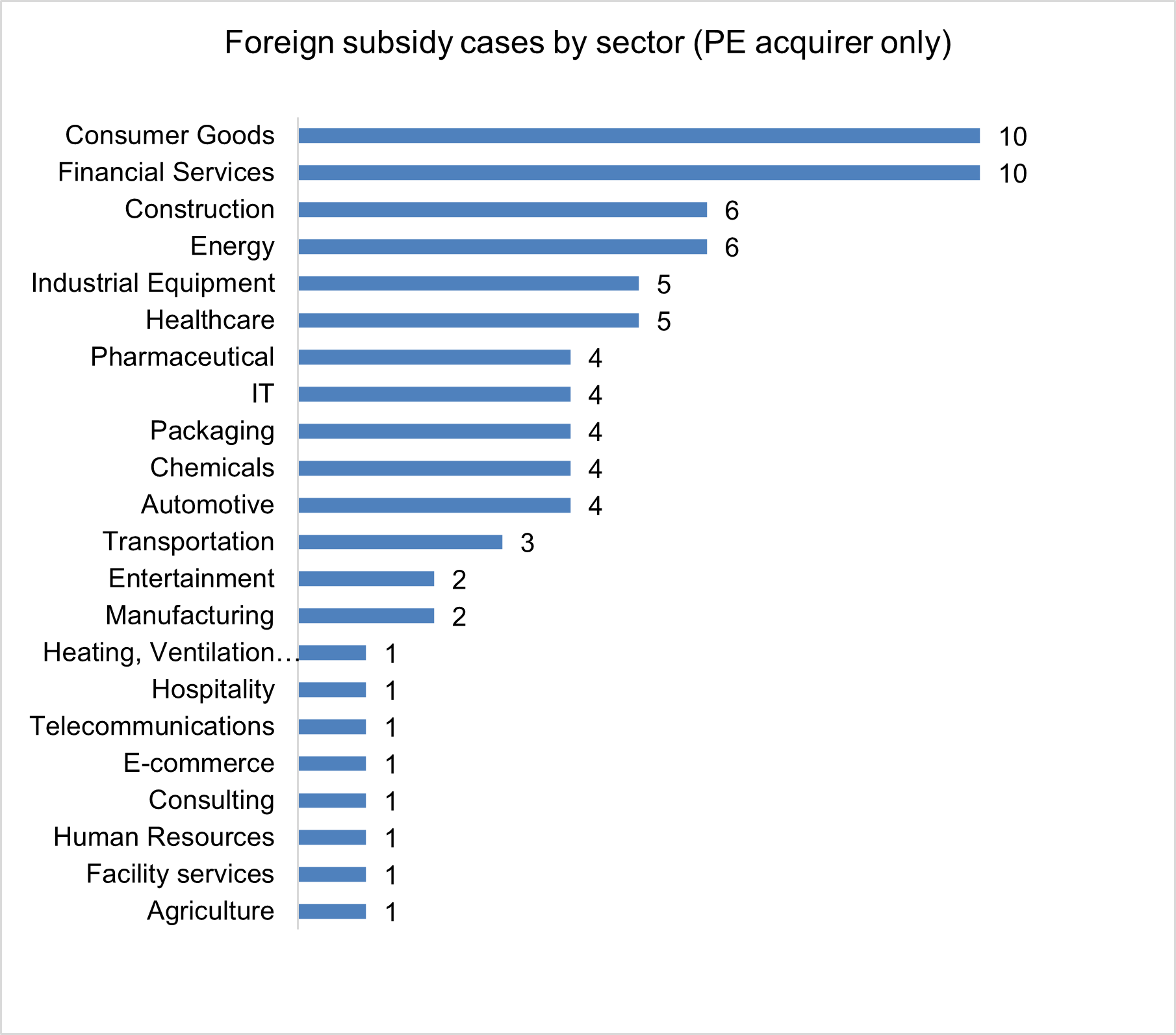

* Includes all cases (PE acquirer and non-PE acquirer)

By Sector (PE acquirer only)

View full image

View full image

By Target HQ country

View full image

View full image

** Reflects the number of targets by their HQ in FSR filings. In cases where there are multiple targets, each target is counted separately for its respective HQ country. As a result, the overall total does not match the total number of unique cases.

By Acquirer HQ Country

View full image

View full image

*** Reflects the number of acquirers by their HQ in FSR filings. In cases where there are multiple acquirers, each acquirer is counted separately for its respective HQ country. As a result, the overall total does not match the total number of unique cases.

Anastasios Tsochatzidis (White & Case, Trainee, Brussels) and Ines Amorim Afonso (White & Case, Trainee, Brussels) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2025 White & Case LLP