The global pandemic has accelerated the world's transition to digital infrastructure. Remote working, social media and home streaming platforms have all seen significant growth and accelerated a growing trend that has been present for several years now. Data centers are at the heart of this digital revolution and as an asset class have continued to attract new investors and operators. At a time when "traditional" real estate asset values have fallen, data centers and potential development sites have continued to be in demand fuelling strong financial gains for those who are able to successfully participate.

New investors looking to raise debt on their investment in data centers face a particular set of challenges. Many traditional real estate lenders and their advisors are unfamiliar with the asset class and related income generating documentation, which has historically impacted on their appetite and approach. However with the growth in the sector and the number of new participants increasing every day, so the number of competitive lenders has increased, attracted no doubt by the number of large private equity participants with which they enjoy relationships, financing on an asset-by-asset basis.

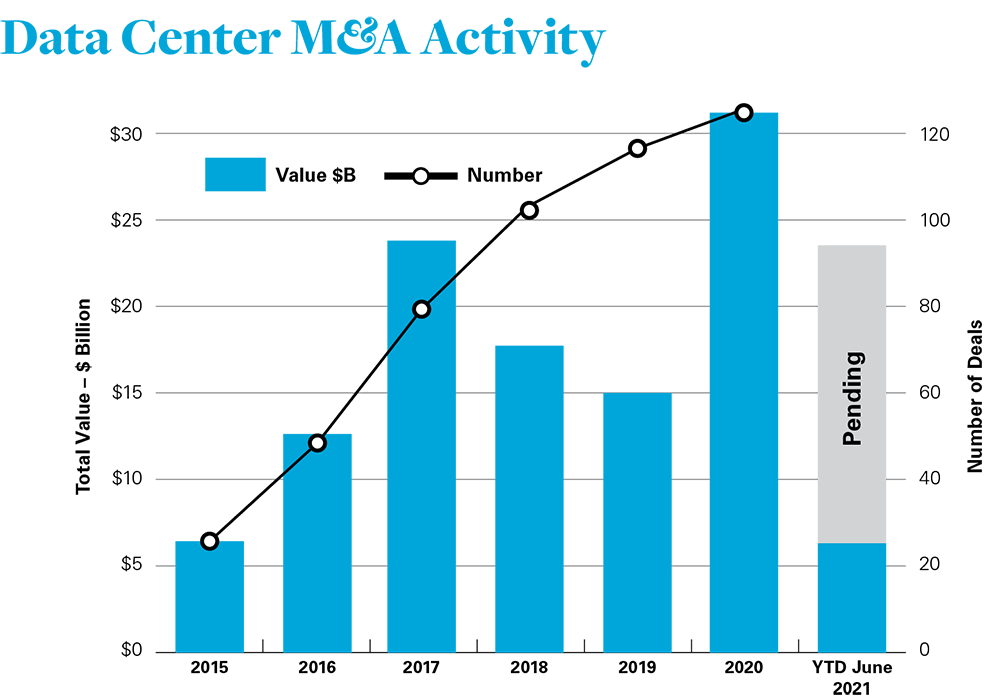

The value of data center oriented M&A transactions is pushing towards a new record in 2021 according to Synergy Research Group, and such demand will present opportunities for both new and existing market participants.

View the full PDF: Data Center M&A Activity

View the full PDF: Data Center M&A Activity

Depending on the lender(s) (or business line at a particular institution) involved, debt may be raised by financing the data center on the basis of principles used in leverage finance, corporate finance, project/infrastructure finance, or real estate finance transactions or a hybrid of some combination of the above.

The range of approaches to data center financings result in some lenders placing more weight on, for example, the value of the asset and therefore being more concerned with the preservation of such value and seek controls that achieve this objective whereas other lenders focus on the cashflows generated by the relevant data center operations. Lenders who traditionally act in the real estate finance space are likely to be more focused on the real estate and the equipment required for the data centers, whereas those who lend in the leverage space are more concerned with the net leverage of the borrower group. Differing underwriting approaches will result in different emphasis being given to enterprise value, value of the real estate and/or the value of the infrastructure. A number of dimensions will be impacted by the approach of the relevant lender including the size of the loan relative to leverage, the cost of the loan and the extent to which either or both of dealings with the asset or with the relevant customer contract(s) are regulated by the terms of the facility agreement.

In addition, the complex technical nature of data centers and the different business models undertaken (e.g., a colocation facility versus a data center occupied by a hyperscaler) will result in different aspects of the commercial deal becoming more or less key from an underwriting perspective.

For example:

- having a subordination, non-disclosure and attornment agreement or other tripartite agreement in place between the lenders and the customer may be a key concern for lenders where the data center has a single hyperscaler customer (assuming it is a hyperscaler which is willing to enter into such a tripartite agreement) but less so on a multi-user colocation services data center;

- financings in relation to the development of new data center space or greenfield sites will be more focused on assessing whether binding customer contracts have been entered into in relation to the data center capacity (in terms of power, area and costs) to be developed or whether there is to be any speculative overbuild, whereas financings of existing operational data centers will be more focused on revenues and performance to date as well as the ability for, and terms upon which, customers can terminate their contracts;

- power supply is a key aspect of the delivery of a data center and power is more typically an issue in infrastructure finance than in leverage or real estate finance transactions and therefore will be the subject of more focus of such lenders; and

- climate change and green energy. Data centers are large contributors to indirect carbon emissions given the large power demands for IT load capacity. This is increasingly moving from a peripheral consideration for lenders to mainstream.

Inevitably, lenders (regardless of approach) will also likely be focused on:

- the ability of the developer to execute the development and/or capex project to meet the requirements of the customer contract in relation to any relevant ready for service date with the lenders also wanting to be satisfied that there is credit capacity (whether through equity or sponsor support) to ensure that any cost overruns can be met;

- the ability of the operator to continue to provide the services required to the relevant customer(s), given the highly technical nature of such services; and

- the need to have a reliable route to enforcement should the borrower default, either in its obligations to the lenders or in relation to its obligations to the customer(s).

We anticipate international trade and import sanctions will also become an issue of elevated importance for both operators and lenders, particularly given the increasing scrutiny of certain suppliers and customers in this sphere over the last few years and the recent legislative steps taken by various European governments in relation to foreign investments, of which data centers tend to be an area of focus.

We expect data centers to continue to be highly in demand and to see new entrants in the data center space, both as investors and lenders. The differing perspectives and focus points of market participants will continue to shape the industry and the approach taken to financings.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP