View full image "Europe leads the way in offshore wind" and "Rapid growth expected in US offshore wind"

View full image "Europe leads the way in offshore wind" and "Rapid growth expected in US offshore wind"

US offshore wind is poised for record investment

Oil & gas majors, foreign investors and global infrastructure funds, and US utilities are likely to be the most active in the segment.

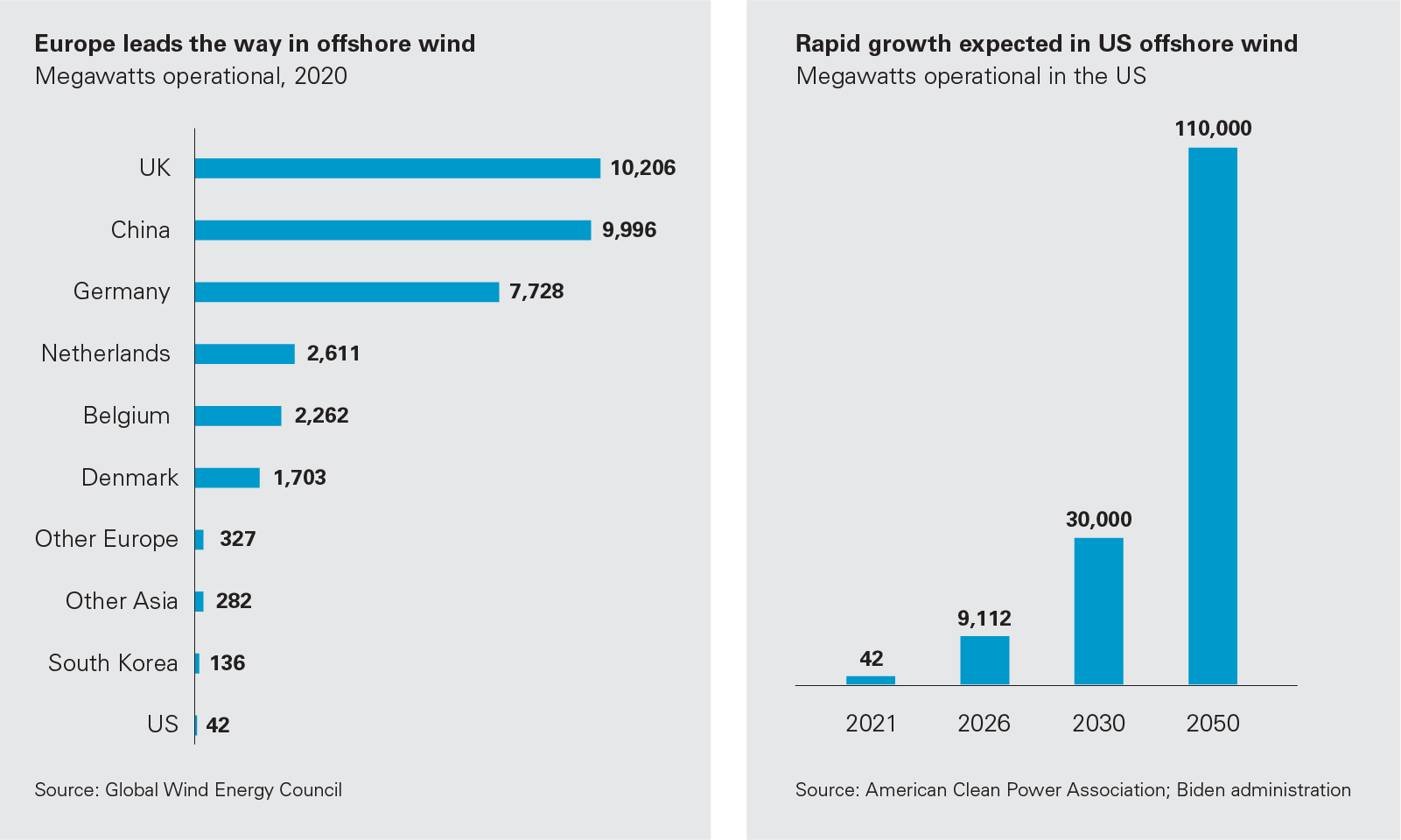

Europe is the leader in offshore wind, with nearly 25 GWs of installed capacity in 2020. Asia has about 10 GWs installed, the vast majority of which is Chinese. But despite the tremendous potential for offshore wind in the US, there are only two offshore wind farms operating in the country, with a combined total of 42 MWs of installed capacity.

That's about to change. The US is on the cusp of transforming itself from a laggard to a fast follower in offshore wind. In doing so, it will build on lessons from around the globe.

A recent sign of this shift came in May 2021 when the Biden administration approved the Vineyard Wind project off the coast of Massachusetts, an 800 MW windfarm that would start operating in 2023. The administration has a goal of permitting 16 offshore wind farms before the end of President Biden’s term, and in addition to approving Vineyard Wind, it began conducting or progressing environmental reviews for four other projects in 2021: Revolution Wind (Rhode Island), South Fork (New York), Ocean Wind (New Jersey) and Empire Wind (New York).

The American Clean Power Association estimates that the US could have 9,112 MWs of offshore wind capacity installed by 2026, which would bring the US close to where the UK and China are today in only five years. Moreover, the Biden administration recently set a goal of installing 30 GWs of US offshore wind capacity by 2030, and 110 GWs by 2050. A new standalone investment tax credit for projects that begin development before 2026 will incentivize developers to help the US achieve these goals.

The Biden administration also set a course for the US to reach net-zero greenhouse gas emissions economy-wide by no later than 2050. Many states, from Massachusetts to Virginia, had already set net-zero targets and are taking steps to achieve them, including issuing RFPs for offshore wind development.

All the while, technology continues to advance, bringing costs down and facilitating deployment at scale. That includes rapid development of floating turbines that will enable offshore wind generation in deep waters off the coasts of the Pacific Northwest, California, Hawaii and Maine. There is also interest in developing offshore wind projects in the Gulf of Mexico and the Great Lakes region.

To catch this wind, the US will not only need to install thousands of turbines, it will have to build the transmission and interconnection infrastructure to carry power to shore and deliver it to the grid. Success will depend on the ability to finance large projects as well as navigate often complex regulatory rules, particularly related to the environment. We hope the articles collected in this volume will help proponents in their efforts to accelerate development of offshore wind in the US.

Oil & gas majors, foreign investors and global infrastructure funds, and US utilities are likely to be the most active in the segment.

To meet project goals, proponents must understand rules related to the environment, species and habitats, and visual and noise impacts.

Government incentives are making it easier to finance offshore wind projects, and developers are taking lessons from Europe to manage costs and risk, and attract investors.

By Daniel Hagan, Fredrick Wilson, Aaron Bryant

How market design, regulation and financing will shape the future of offshore wind.

Oil & gas majors, foreign investors and global infrastructure funds, and US utilities are likely to be the most active in the segment

Despite the immense potential of offshore wind in the US, Europe and Asia-Pacific have led the way in developing offshore wind power to date. But as the barriers to development fall away, the US offshore wind market is gathering momentum.

The Biden administration has set an ambitious goal to operationalize 30 GWs of offshore wind capacity by 2030, and it has strengthened tax incentives to encourage offshore wind development.

Recent approval for the 8 GW Vineyard Wind project suggests that the Biden administration will make good on its pledge to accelerate the federal permitting process for offshore projects. And the recent announcement that the administration is opening parts of the California coast to offshore wind development could make way for more than 4 GWs of additional offshore capacity.

Given the trends toward energy transition and investors' growing appetite for renewables, the market may be on the cusp of record investment flows. As the US market picks up, investments will continue to originate from a variety of sources, but the following groups are likely to be particularly active, often due to their deep experience and expertise in the sector.

Oil & gas majors have substantial offshore exploration, development, construction and operation experience, and they have already started investing in the US offshore wind sector to take advantage of their substantial transferable expertise.

In 2021, for example, BP purchased a 50 percent interest in two US offshore wind assets, Empire Wind and Beacon Wind, from Equinor, the Norwegian multinational energy company, for a total cash consideration of approximately US$1.1 billion. These two projects were recently selected by the State of New York to satisfy some of its future power needs. The partnership will enable Equinor and BP to combine their strengths in the sector. Equinor will remain the operator of the projects through the development and construction phases, after which time the wind farms will be staffed equally by Equinor and BP.

Also in 2021, Chevron became the first US oil major to dip its toes into the offshore wind market. In April, it signed a deal with Norway's Moreld, an industrials company with offshore expertise, to develop technology for floating offshore wind turbines with the California-based firm Ocergy, which plans to compete for gigawatt-scale projects worldwide.

Trends have accelerated foreign investment in US renewables, including by sovereigns. Indeed, almost half of the 86 greenfield and M&A deals announced in US renewables in 2020 involved foreign investors. And a substantial number of US offshore wind projects are already owned by foreign investors.

Avangrid, the US-based subsidiary of Spain's Iberdrola, and Denmark-based Copenhagen Infrastructure Partners co-own Vineyard Wind, the recently approved offshore wind farm that will be built off the coast of Massachusetts.

The Qatar Investment Authority and Iberdrola collectively made a US$4 billion equity investment in Avangrid, a portion of which will be used for Avangrid's two offshore projects off the coast of New England, Vineyard Wind and Park City Wind.

Ørsted, a Danish power company, and Eversource, a US-based energy company, co-own Revolution Wind, an 880 MW offshore wind project that will be constructed off the coasts of Rhode Island and Massachusetts. The Bureau of Ocean Energy Management (BOEM) recently announced a Notice of Intent to prepare an Environmental Impact Statement for its construction and operations plan.

Ørsted is particularly active. It either owns or is a partner in seven BOEM leases—including the first operating US offshore wind farm, the Block Island Wind Farm, which it owns.

Infrastructure funds are likely to play an increasingly important role accelerating development of offshore wind in the US, partly in response to Biden administration policies meant to open the country to rapid development of offshore wind capacity, and partly due to deep interest in energy transition and ESG considerations.

In 2020, New York–based Apollo Global Management made a US$265 investment in US Wind to fund development of an offshore project in Maryland waters. The investment was made by Apollo's second infrastructure fund, Apollo Infrastructure Opportunities Fund II. US Wind is majority-owned by Renexia SpA, a leader in renewable energy development in Italy and a subsidiary of Toto Holding SpA. Apollo is not new to the space, having made an investment in 2018 in the Tullahennel Wind Farm, a 37 MW facility located off the coast of Ireland.

Many US utilities have set net-zero targets and are moving away from conventional power generation, sometimes urged on by shareholders that have a strong ESG focus. A number of these utilities are selling portions of their businesses and using the proceeds to invest in clean-power solutions.

Dominion Energy, a Virginia-based utility, has a goal of becoming the cleanest energy company in the US. In 2020, it sold its gas transmission and storage business and plans to reinvest some of the proceeds in renewables. In the same year, Dominion installed a 12 MW offshore wind demonstration platform off the coast of Virginia, setting the stage for a multi-gigawatt offshore wind project that it plans to develop in partnership with Ørsted in Virginia waters.

Public Service Enterprise Group, a utility based in New Jersey, is also partnering with Ørsted, in this case to develop the 1,100 MW Ocean Offshore Wind Farm. BOEM has already begun to prepare environmental statements for the project.

Exelon announced that it will sell its competitive generation assets. Building on its regulated utilities business, it aims to become the largest supplier of clean energy and sustainable solutions in the US.

OGE Energy announced that it is selling its interest in Enable Midstream, a pipeline company, to Energy Transfer. This is part of OGE's plan to become a pure-play generation company, and it has earmarked a portion of the sale to increase its renewables generation capacity.

* * *

The US offshore wind market is opening up, and there will be no shortage of investors targeting the space as it takes off. Those with offshore experience in other regions where the offshore wind sector is more advanced are likely to lead investment, along with US utilities that are aligning their strategies with energy transition, and sovereigns and global infrastructure funds that are focused on energy transition and ESG considerations.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP