European Union

The COVID-19 pandemic, and the ensuing lockdown measures—along with some landmark judgments— have led the European Commission's Directorate General for Competition to reflect on its approach to merger control notifications and reviews

17 min read

Subscribe

Stay current on your favorite topics

Key developments

The COVID-19 pandemic and the ensuing lockdown measures, as well as some landmark judgments and the finalization of a nearly 5 year long evaluation of procedure/jurisdiction, have led the European Commission's Directorate General for Competition to reflect on its approach to merger control notifications and reviews, both from a practical and procedural as well as substantive viewpoint.

EU merger control review processes suffered very little disruption due to Covid-19-related lockdowns in relation to both simplified and more complex cases

Early on in the crisis, because of the negative impact of COVID-19 on market tests and technical issues caused by remote working, the Directorate General for Competition recommended that companies delay their merger notifications where possible. Soon afterwards, the Commission began encouraging companies to submit their notifications electronically, either by e-mailing the Merger Registry or using the eTrustEx platform. The latest communication on this point insists that this measure is temporary, but we would not be surprised if it develops into a new best practice.

On September 11, 2020, in her speech on the future of EU merger control, European Commissioner for Competition Margrethe Vestager declared that in light of the current economic context and the necessity to "stay competitive in a fastchanging world", changes to merger notifications at the EU level ought to be envisaged. She foresaw that these changes could include a broader application of the simplified procedure, which would entail reduced information requirements for parties and a speedier review process. In particular, this could result in a reduction in pre-notification discussions in cases that are "so straightforward that there's really nothing to discuss before the merger is filed".

On March 26, 2021, the European Commission launched an impact assessment on policy options for further targeting and simplification of merger procedures, inviting stakeholders to submit their views by 18 June 2021. This was accompanied by the publication on the same day of a Staff Working Paper (SWP). This Paper summarises the European Commission's findings of its evaluation (launched back in August 2016) of procedural and jurisdictional aspects of EU merger control. With respect to simplification, the paper notes the potential room for the additional expansion of the simplified procedure, and identifies scope for reductions in the information requirements for simplified procedure reviews.

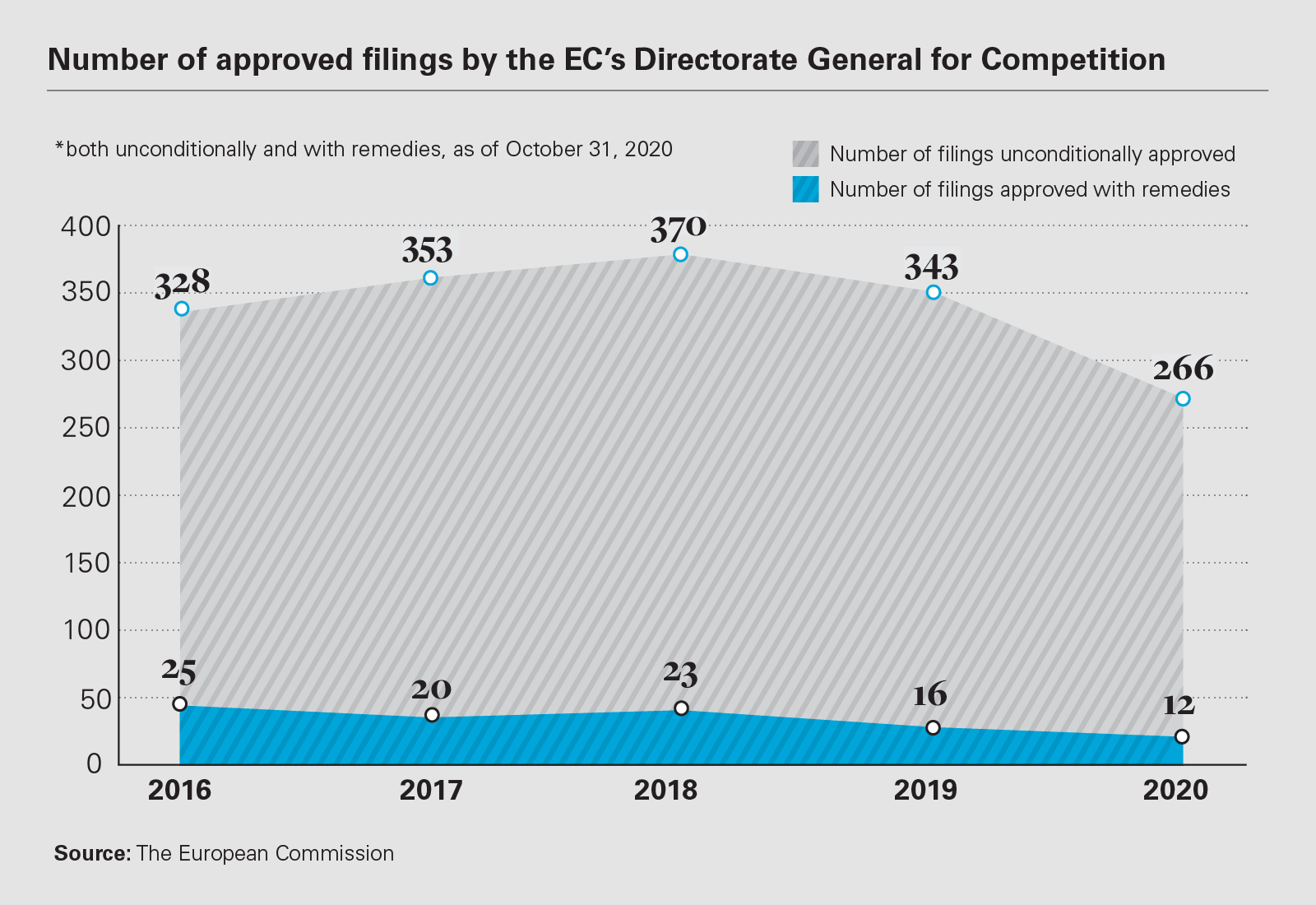

266

merger filings received by the EC's Directorate General for Competition in 2020 were approved unconditionally

In her speech, Commissioner Vestager also declared that the EU Merger Regulation ("EUMR") could be applied to so-called "killer acquisitions", where incumbents aim to acquire innovative targets to preempt future competition, even if the target does not meet the turnover-based thresholds. While the Commissioner excluded the introduction of value-based thresholds to catch such deals, she underscored that Article 22 of the EUMR already enables national competition authorities to refer to the EU transactions that raise potential competition concerns, even if they do not meet the national turnover thresholds.

The change in the EC's Article 22 referral policy became effective in March 2021 when the EC published its guidance on the application of the Article 22 referral mechanism (Article 22 Guidance). The EC now encourages national competition authorities to use the referral mechanism even where transactions do not meet the national merger control thresholds of the referring Member States.

The Article 22 Guidance details the categories of transactions which may be suitable candidates for referral. The EC's focus is predominantly on transactions in the digital and pharmaceutical sectors, but also on other sectors, for example, where innovation or access to competitively valuable assets is an issue.

The Article 22 Guidance states that the European Commission will generally not consider a referral appropriate if 6 months have passed since transaction closing, or where the transaction has been notified in one or several Member States that did not request a referral to the EC. However, the European Commission considers that in exceptional circumstances a later referral may be appropriate based on, for example, the magnitude of the potential competition concerns and of the potential detrimental effect on consumers.

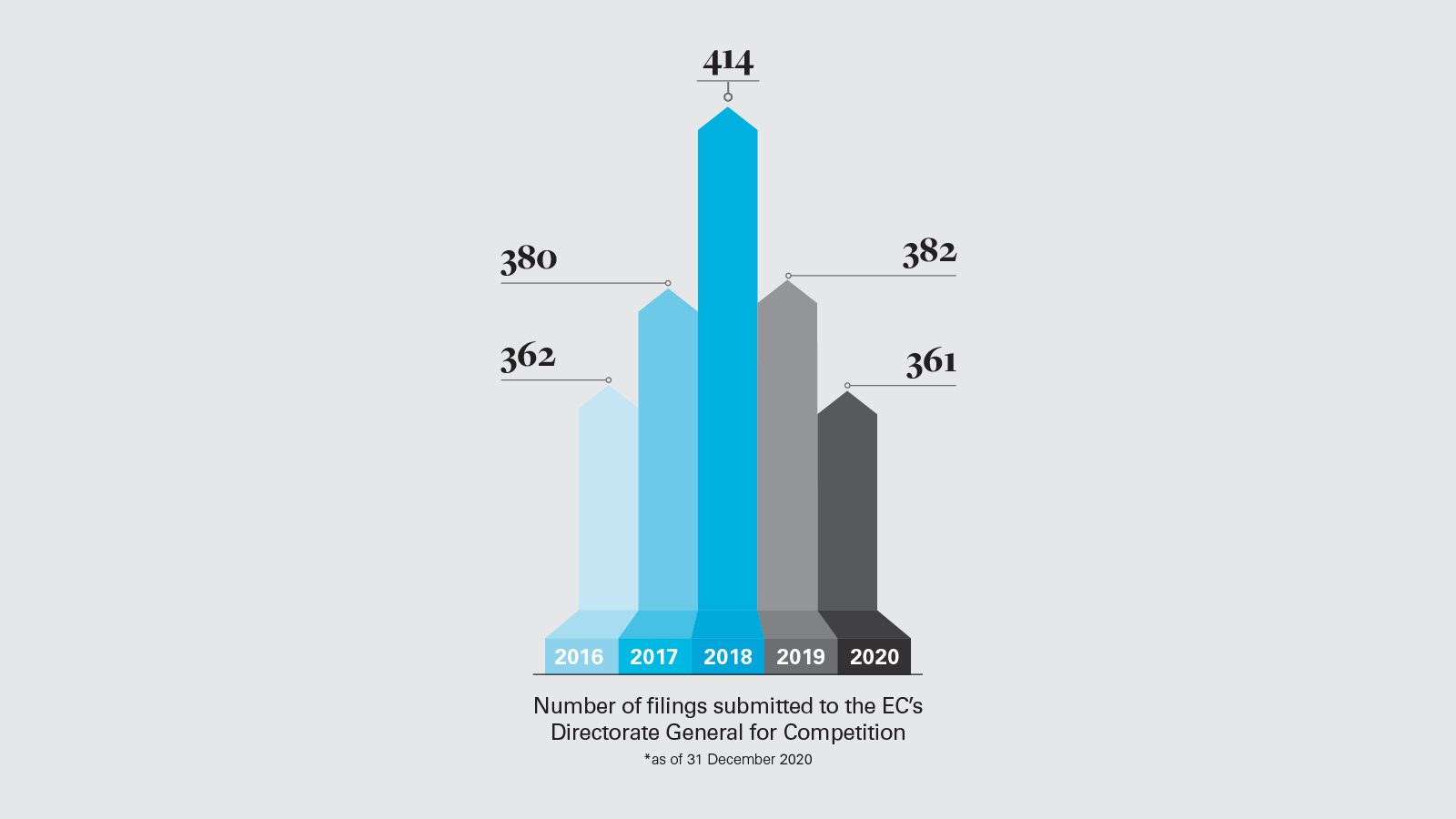

361

Number of notified filings received by the EC in 2020

The guidance implements a major policy change and has important consequences for dealmakers. Any transaction that could be assessed as threatening competition within the EU may now be reviewed by the EC – no matter how small the target, and even after the deal has closed. This impacts deal risk assessment, transaction timelines, and deal documentation for certain transactions.

Beyond procedural changes, Commissioner Vestager has announced a review of the substantive assessment to see whether the Commission "is getting things right". However, this review has been postponed until the Court of Justice rules on the Commission's appeal against the General Court's May 2020 judgment in CK Telecoms UK Investments v. European Commission, which clarifies the burden of proof that the Commission must meet in its merger decisions (see below for details).

In this landmark judgment, which is possibly the most relevant substantive development in the field of merger control in 2020, the General Court held that the Commission must produce sufficient evidence to demonstrate with a strong probability the existence of significant impediments to effective competition due to a proposed transaction. The required standard of proof is stricter than a mere "balance of probabilities", but still less strict than "beyond all reasonable doubt".

Another interesting development has been the Commission's recent questioning whether it should take into consideration public interest in merger reviews. There seemed to have been little space for such considerations in the highly politicized decision to prohibit Siemens' acquisition of Alstom. However, the recent clearance of PKN Orlen's acquisition of Lotos, which created a Polish energy champion, signaled that there might be room for policy considerations in the Commission's decision-making. Similarly, in commenting on the clearance of Aurubis' acquisition of copper scrap refiner Metallo, Commissioner Vestager signaled a public policy consideration when explaining that copper was "an important input needed for electric mobility and digitization. A well-functioning circular economy in copper is important to ensure a sustainable usage of resources in the context of the European Green Deal".

We also saw a few interesting developments in the area of commitments. In Nidec/Embraco, the Commission requested as part of the remedy package that Nidec fund certain capital expenditure investments of a plant in Austria, which appears to have been largely driven by the Commission's desire to keep that plant afloat. Earlier in 2020, the Commission allowed Nidec to buy back this plant, after its purchaser under the remedy package had announced its closure.

Moreover, in the pharmaceutical sector transaction between Takeda and Shire, the Commission accepted Takeda's request to waive the entirety of the commitments imposed by the Commission's conditional clearance, in light of several significant and permanent developments affecting the competitive landscape. This was the first time that the Commission waived divestiture commitments in their entirety since the General Court's May 2018 annulment of the Commission's rejection of Lufthansa's request to waive its commitments on the basis that the Commission did not carry out a careful examination of Lufthansa's arguments that significant market changes justified a waiver.

Finally, the Commission continues to be stringent when it comes to the enforcement of procedural rules in relation to provision of information as part of merger reviews. This trend started in 2014 with the Commission imposing a €20 million fine on a salmon-farming company for closing on the acquisition of a 48.5% stake in a rival before notifying the transaction. This fine was confirmed by the Court of Justice in March 2020. The trend continued throughout 2019 with a number of global companies receiving hefty fines for gun jumping violations. A few appeals against these fines are currently pending before the General Court.

Impact on merging parties

As with any other sector in the world, a key development affecting merger control process in 2020 was COVID-19. At least partially due to the difficulties in obtaining information from the parties in a pandemic, the Commission suspended reviews in five Phase II cases in early 2020.

The EU believes that it should review ‘killer acquisitions’ more consistently in order to protect nascent competition, affecting in particular the pharmaceuticals and digital sectors

The Commission might have been initially slightly more reluctant to open Phase II investigations to ensure that its strained resources were efficiently allocated to transactions raising serious concerns. However, with remote working becoming the "new normal", this effect has diminished and we do not expect it to be a long-term trend. In fact, by the time COVID-19-related lockdowns were lifted across the EU in the summer of 2020, Vestager concluded that EU merger control review processes suffered very little disruption in relation to both simplified and more complex cases.

Contrary to what one might instinctively expect in a stressed economy, we have also not seen an increase in successful "failing firm" defenses, for which the burden of proof has remained notably high.

The Commission's change in its Article 22 referral policy, effective from March 2021, under which it now encourages national competition authorities to use the referral mechanism even where transactions do not meet the national merger control thresholds of the referring Member States is likely to impact dealmakers going forward. Even if the Commission reviews only a few transactions per year under the new policy, the Article 22 Guidance creates legal uncertainty for parties to transactions falling below the EU Merger Regulation's thresholds. Parties to a transaction must now incorporate a specific Article 22 referral risk assessment, and reflect any risk in the transaction documents and timetable. For certain transactions, the merging parties may also want to consider whether to proactively contact the Commission to gain an early indication that the transaction is not a candidate for a referral.

A development which has had a strong impact on our advice to clients was the General Court's May 2020 judgment in CK Hutchinson, highlighting the increased importance of economic evidence in merger control review and a more stringent standard of proof. The General Court held that the Commission must go beyond demonstrating a reduction in competitive pressure when objecting to a transaction and prove, with a "sufficiently high degree of probability" that increases in prices will follow. This standard of proof is stricter than a mere "balance of probabilities", but still less strict than "beyond all reasonable doubt". This ruling goes in the same direction as the Court of Justice in European Commission v. UPS, where the court had acknowledged the added value of transparent econometric models to competition cases. While the judgment could influence the Commission's enforcement approach, it is still unclear how the Commission will react (the Commission's appeal is pending). Raising the Commission's standard of proof appears beneficial for the merging parties, but it also increases the risk of the parties having to undertake a more burdensome notification process.

Another relevant development for our clients' preparation for a merger review process but also for their timing and cost expectations is the Commission's increased reliance on internal documents. In in-depth investigations, the Commission now typically requests a production of responsive documents from a broad selection of custodians. The scope of this exercise is starting to resemble the Hart-Scott-Rodino process in the US to which expansive documents productions have been reserved until recently. Lengthy pre-notification periods and hundreds of pages of standard merger notification forms also place a heavy burden on companies, in particular when compared to the US system, where initial notifications are quite thin.

If, as suggested by Commissioner Vestager, the Commission is planning to once again treat simple cases in a simple way, the burden on notifying parties will be reduced. However, we remain skeptical that this will happen.

Finally, while the Commission has long been cooperating with other global authorities, such cooperation is increasing and becoming closer. It is therefore crucial for parties to transactions that are notifiable in more than one jurisdiction to think carefully the choreography of the filings and ensure a consistent approach to substantive issues.

Recent changes in priorities

As an established authority, the Commission applies EU merger control rules consistently across industries. Generally, the Commission is more likely to express concerns in transactions taking place in consolidated industries. Over the past years, the most prominent examples of this were several four-to-three mergers in the telecoms industry, which have since 2012 all been reviewed in in-depth investigations. The Commission's approach has changed gradually over the years and it has generally applied a tougher stance by requesting structural remedies that would ensure the entry of a fourth telecoms player in the market.

However, in November 2018, following an in-depth review, the Commission unconditionally cleared the acquisition of Tele2 NL by T-Mobile NL, combining the third and fourth- largest mobile network operators in the Netherlands. The companies successfully demonstrated that the merger would generate efficiencies and benefit consumers, and also showed that the other two mobile operators in the Dutch market had different strategies and incentives based on multi-play offers that combined mobile and fixed services.

The Commission raised concerns about all other recent four-to-three mergers in the telecoms industry. To address these concerns, the buyers had to offer access to suitable network and divestment remedies, such as divestment of Spectrum together with network capacity. The T-Mobile NL/Tele 2 NL non-conditional clearance is therefore an exception, for now. However this success shows that, in the right circumstances and with well-prepared arguments, even four-to-three mergers in the telecoms industry can be approved unconditionally.

As has been demonstrated by the EC's change in Article 22 referral policy and by the results of its evaluation of procedure/jurisdiction (published in its Staff Working Document on 26 March 2021), the Commission also seems to believe that it should more consistently review "killer acquisitions" to protect nascent competition, affecting in particular the pharmaceutical and digital sectors.

Number of filings submitted to the EC’s Directorate General for Competition (PDF)

Number of filings submitted to the EC’s Directorate General for Competition (PDF)

Key enforcement trends

The Commission has not prohibited any transactions since 2019, when it issued three prohibition decisions in Wieland/Aurubis, Siemens/Alstom and Tata Steel/ThyssenKrupp. In these cases, the parties were leaders in their markets, and the Commission considered that the EEA was the relevant geographic market, despite the companies arguing that markets were global and competition from Chinese players fierce. These prohibitions demonstrate the Commission's reluctance to define global markets and, at least in those decisions, to acknowledge the impact of competition from, for example, Asian competitors.

While this was the highest number of prohibitions since 2001, it clearly did not point to a trend of more prohibitions. Having said this, antitrust concerns shared by the Commission during the review process led the parties reportedly to abandon three deals in 2020 and early 2021: in Johnson & Johnson/ TachoSil and Fincantieri/Chantiers de l'Atlantique, the Commission preliminarily concluded that it was unlikely that a timely and credible entry from other players would offset the possible negative effects of the proposed transactions, which could significantly reduce competition and lead to higher prices, less choice and reduced incentives to innovate. Similarly, in Boeing/Embraer the Commission was also reluctant to acknowledge the impact of competition by international players from China, Japan and Russia and had raised possible concerns.

A number of cases have been cleared with remedies in recent times. In 2020, two out of the three Phase II remedy cases (Google LLC/Fitbit Inc. and Fiat Chrysler/ Peugeot) involved purely behavioral commitments. Nevertheless, structural remedies remain the norm, possibly covering all or a substantial part of the overlapping business. In BASF/Solvay's Polyamide Business, the Commission was worried there would be price increases in the markets for nylon compounds and nylon fibers because the transaction reduced the number of EEA suppliers. BASF divested several facilities and, to strengthen the divestiture buyer's position on the market, created a production joint venture between the merged entity and the divestiture buyer. It also entered into long-term supply agreements with the divestiture buyer to meet the divestment business' requirements and thus preserve the viability of the facilities.

A recent example of a mixed structural / behavioral remedy is PKN Orlen/Grupa Lotos, where PKN divested part of its stake in Lotos' refinery and several other facilities, as well as sold Lotos' 50% stake in the jet fuel-marketing joint venture the latter maintained with BP. The remedy package also included the commitment to make available up to 80,000 tonnes of jet fuel per year to competitors in via an annual open tender.

Recent studies and guidelines

On December 9, 2019, Commissioner Vestager announced that the Commission would start a review of the two-decades-old Market Definition Notice to see whether it needs to be adjusted for a digitalized and globalized world. The adoption of a new notice is expected for 2022.

The review process is raising a number of interesting topics, including how to properly take into account that geographic markets are more and more global; the role of the small significant non-transitory increase in price (SSNIP) test in digital services, which are often available for free; the right approach to defining markets in data-intense industries, which often function as ecosystems; and the need to update the existing approach to internet sales.

In addition, the Commission's interest in common ownership— where investors hold minority stakes in multiple companies active in the same industry—has been recently revived.

In its Dow/DuPont investigation, the Commission measured the level of common ownership in the industry based on (i) the number of shareholders that together held more than a certain percentage of the shares in each of the main industry players, (ii) the number of reported equity holders with shares in all competitors, and (iii) the level of equity collectively held in each competitor by these common reported shareholders.

In September 2020, the Commission published a 336-page Joint Research Centre report on common shareholding in Europe, which concluded that, while common ownership leads to greater market power, the phenomenon is very complex and it is difficult to conclude whether competition is harmed. We therefore expect that this question will continue to be assessed on a case-by-case basis.

Number of approved filings by the EC's Directorate General for Competition

Number of approved filings by the EC's Directorate General for Competition

Looking ahead

Overall, the most significant impact on merger control could be the more widespread use of Article 22 of the EUMR to capture transactions, such as "killer acquisitions", that do not meet the threshold of the regulation nor of any of the 27 national merger control rules in the EU. This would create significant legal uncertainty as it would significantly increase regulatory risk for small transactions that do not meet the applicable thresholds.

Commissioner Vestager's promise of a broader application of the EUMR's simplified procedure is certainly welcome, but, if it happens, will not take place until the first quarter of 2022. This could be further expanded by increasing the thresholds for affected markets to capture more cases that are unlikely to cause a significant impediment to effective competition.

THE INSIDE TRACK

What should a prospective client consider when contemplating a complex, multijurisdictional transaction?

Above all else, it is in the parties' interest to plan ahead. The timing of filings should be planned backwards, starting from the expected closing or long-stop date. If an authority could potentially object to all or part of the transaction, it is paramount to identify all potential roadblocks and to set hard deadlines to ensure the success of the process. Detailed project management is therefore essential to successful merger notifications.

In your experience, what makes a difference in obtaining clearance quickly?

One item that recurrently affects the outcome of merger notifications is the support, or lack of support, of other market participants. When customers or companies involved at any level of the relevant supply chain provide strong opinions either in favor of or against a transaction, this will strongly affect the outcome of the review process. While DG Comp takes a dim view of perceived attempts to unduly influence the reactions of market participants, it is still important to explain the rationale of the transaction to its customers.

What merger control issues did you observe in the past year that surprised you?

In its CK Hutchinson judgment, the General Court ruled that the Commission must go beyond demonstrating a reduction in competitive pressure when objecting to a transaction. Instead, the Commission has to prove, with a "sufficiently high degree of probability" that increases in prices will follow.

While the judgment could potentially influence the Commission's enforcement approach, it is still unclear how the Commission will react. Raising the Commission's standard of proof appears beneficial for merging parties; however, it also increases the risk of companies having to undertake a more burdensome notification process.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP