Greece

The new president of the Hellenic Competition Commission (HCC), Ioannis Lianos, is a well-known academic particularly attuned to public interest issues. In 2020, Lianos led an HCC initiative to launch a dialogue around the potential integration of sustainability concerns in EU competition law, including merger control.

15 min read

Subscribe

Stay current on your favorite topics

The review of a competitor cooperation can raise questions under the cartel prohibition clauses of the ARC: They cannot be reviewed as part of merger control proceedings, so it is common practice to review such questions in parallel but separate proceedings

Key developments

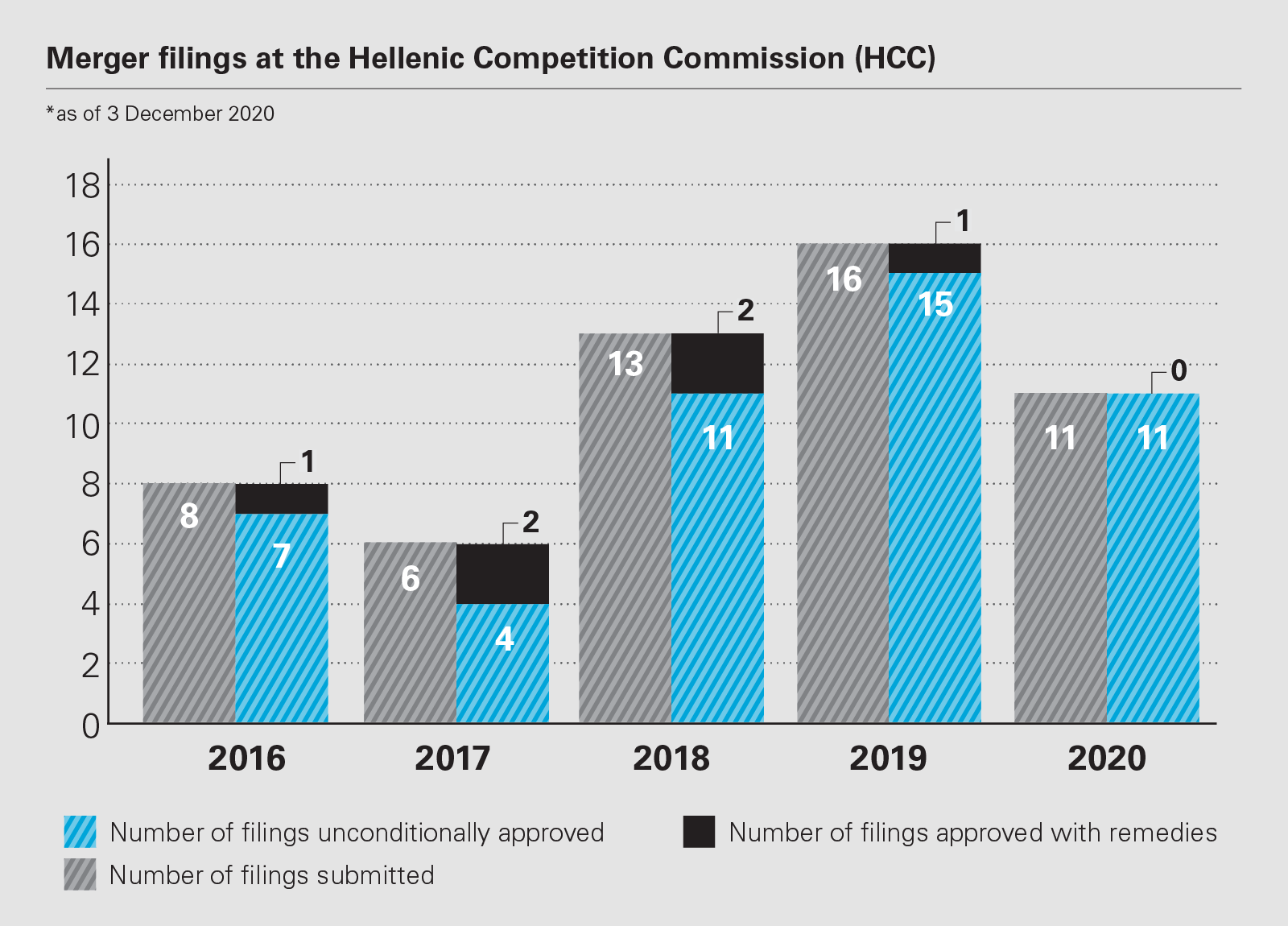

From January 2019 until September 2020, the Hellenic Competition Commission (HCC) has reviewed 27 notified transactions, and launched five in-depth (Phase II) investigations.

Remedies were only accepted in the aluminium recycling market deal between Mytilineos and EPALME; they were behavioural and aimed to address vertical foreclosure concerns. All other transactions were cleared unconditionally.

The remaining Phase II investigations came in a variety of markets, including railway maintenance services, electronics retail, online gambling, and chemical products for crop protection.

Arguably, the most important merger decision of the HCC over the past year concerned the clearance of a privatisation in which the incumbent railway operator, TrainOSE, which is a subsidiary of Italian State Railways, sought to acquire sole control of the incumbent railway maintenance services provider, EESTY.

The transaction formed part of Greece’s privatisation and, by extension, fiscal adjustment programme. As the HCC noted, the merger led to two monopolists being consolidated into one, vertically integrated.

The HCC examined whether the merged entity would have the incentives and ability to foreclose potential rivals, whether in the primary market of railway transport services, or the secondary market of maintenance services. To determine this, it asked for the opinion of market players and the Independent Railway Authority (RAS).

It was notable that RAS downplayed the risk of foreclosure of rival railway operators, relying on the applicable regulatory framework and the niche character of maintenance services.

When looking at the risk that other maintenance services providers could be excluded as a result of the deal, the HCC placed particular emphasis on the regulatory framework, which is enforced by RAS, and the risk of antitrust enforcement against potential foreclosure and discriminatory practices.

It noted that a potential entrant would not only have TrainOSE as a potential customer, but other railway cargo carriers. The HCC also hinted at potential efficiencies arising as a result of the deal, accepting that because of the merger, EESTY could expand its activities in other railway transport markets.

Because of these reasons as well as the fact that no other company had expressed an interest in acquiring EESTY the HCC cleared the transaction unconditionally.

In its examination of Mytilineos' acquisition of EPALME, the HCC launched a Phase II investigation to assess whether the merged entity would be in a position to foreclose upstream rivals from the provision of recycling services, and downstream rivals from the supply of primary aluminium.

The HCC identified a number of issues in relation to the markets for primary and secondary aluminium and recycling services that could prevent effective competition. Notably, in light of EPALME's monopolistic position in the recycling market, the HCC said the likelihood of tying recycling services with the purchase of primary aluminium would increase as the result of the contemplated transaction.

However, the regulator cleared the transaction, subject to behavioural remedies. Mytilineos committed to maintaining EPALME's solvent customer base, refrain from tying the supply of primary aluminium with the aftermarkets related to recycling, and from engaging in exclusivity practices, for a period of three years.

Another Phase II investigation concerned the acquisition of sole control by Olympia Group, owner of PUBLIC retail stores, of the Media Markt retail stores. Both PUBLIC and Media Markt sell a wide range of technology equipment.

The HCC launched an investigation focusing on whether brick-and-mortar and online channels were easily interchangeable. It also looked at whether there would be potential noncoordinated effects of the transaction, arising from the similarity in the merging entities’ portfolios.

Referring to European Commission and French precedents in cases where an online channel exerted sufficient competitive pressure on the brick- and-mortar channel to form a single relevant market, as well as market test feedback, the HCC concluded that the relevant product market included both channels in Greece. It left open the question of whether sales from foreign marketplaces, such as Amazon and eBay, should also be included.

It also delineated markets based on the type of devices sold, with an emphasis on ‘black’ and ‘grey’ goods like TVs, stereos, computers and smartphones where the merging companies had higher market shares.

According to the HCC’s market share analysis, the merged entity’s share would not exceed 20 per cent in either black or grey goods. It also showed that the change in market share would not exceed 200 points in either case.

Based on these findings, the high levels of competition due to the convergence of offline and online channels, and the recent expansion of several retail chains into black and grey goods, the HCC was convinced that the transaction would not raise competition concerns and cleared it unconditionally.

A final case worth examining involved Chinese state-owned chemical company ChemChina's plans to acquire, through its Dutch subsidiary, Adama, sole control over Alfa, its exclusive distributor in Greece. Adama already held a minority shareholding in Alfa.

The transaction had horizontal effects, since both companies overlapped in the wholesale supply of crop protection products. There were also vertical effects, given that Adama's group was mainly active in the upstream market of supply, whereas Alfa was active in the downstream market of distribution.

The HCC found that the merged entity’s combined market share in the overall market of crop protection products would be 25-35 per cent, making it the leader in Greece.

However, the market share analysis broken down by protected crop and enemy - such as insects - segments identified a number of markets whereby the combined strength of the entity would be even higher.

The HCC broke down the affected markets into three categories: markets where the merged company would hold a high share with an increment exceeding 5 per cent; markets where the entity would hold a high share, but with a low increment; and markets where the high share would not be attributed to the transaction, but to the ongoing distribution agreement between Adama and Alfa.

It focused more on the first group, but also downplayed the noncoordinated effects of the merger due to the presence of powerful competitors like BASF and Bayer, the transient nature of high market shares, the declining trend of the parties’ shares, and the fact that the target already distributed Adama’s products in the relevant market segment.

In assessing the coordinated effects of the deal, the HCC found that Alfa was dependent upon competing suppliers, and not vice-versa. It would not make business sense to retaliate against them, because they could easily substitute other distributors for Alfa, while Alfa needed them to have a presence in a number of segments.

The HCC also examined whether Alfa would have the power to become a one-stop-shop for end users, given its potential to distribute Adama fertilisers, and providing bundled rebates taking advantage of its wide portfolio. The HCC held that such bundles were unlikely to produce foreclosure effects, and, in any case, reserved its rights to pursue enforcement against abusive practices in the future, if need be.

As a result, the HCC cleared the transaction unconditionally, pursuant to an in-depth Phase II investigation. The HCC also validated two ancillary restraints, namely a non-compete clause and a transitional services and supply agreement between the seller and the acquirer.

Impact on merging parties

Unlike the current state of the law in the EU and in most EU member states, Greek competition law includes a mandatory 30-day filing deadline after the signing of the transaction. Given the deadline, actual prenotification discussions with the HCC can be limited in time and depth.

However, the HCC’s Directorate General (DG) encourages such discussions, given that they can prevent significant errors and omissions in the filings, expedite the actual launching of the investigation, and streamline clearance. That being said, Greece has no ‘real’ prenotification stage in the sense of the EU system.

On that note, the HCC’s recent merger control practice has confirmed that parties should anticipate that concentration investigations will not be launched immediately after the notification is filed, because the HCC will deem the notifications incomplete. Specifically, according to merger control decisions published in 2019 and the first half of 2020, in all but the Olympia/Media-Saturn case, the notification form was incomplete and the parties had to supply additional information. Delays in launching the investigation ranged from 20 to 85 days.

In most cases, the HCC merger investigation is straightforward and predictable. During the investigation, the HCC’s DG frequently sends requests for information (RFIs) to the parties by e-mail, and carries out market tests. The case teams may also hold informal meetings with the companies involved, and organise interviews with third parties. The HCC’s past activity demonstrates a track record of keeping to deadlines, once the notification is formally accepted and the investigation launched.

Moreover, there are signs that, even post-clearance, the HCC can continue to monitor the effects of a merger. In 2018, the HCC cleared the acquisition by passenger-shipping leader Attica Group of its main competitor, Hellenic Seaways, subject to strict behavioural remedies for three years, and monitoring of the remedies.

In December 2019, the HCC launched an investigation to assess Attica’s compliance with the remedies. In August 2020, the HCC announced its decision to fine Attica Group €29,792 for breaching one of its commitments, and also ordered the extension of that commitment by an additional year.

In June 2020, the HCC decided to modify a previously accepted commitment from supermarket chain Massoutis to divest a store on Andros Island. Given the lack of interest for the store, and the "unfavourable economic situation affecting the country," the HCC agreed to allow Massoutis to sell a different store on the island.

In April 2020, the HCC published its final report on its inquiry into the Greek supermarket sector. The sector has undergone a long period of consolidation over the past decade, mainly through HCC clearance decisions. The HCC’s report confirmed that, despite the numerous mergers, market concentration remained at healthy levels.

As of late August 2020, the HCC had not published any merger decisions covering the COVID-19 period.

Recent changes in priorities

The HCC's recent merger control activity has demonstrated an increased focus on the vertical effects of concentrations. In most cases where the HCC identified affected markets, its competition concerns were vertical.

In the TrainOSE/EESTY case, given the vertical relationship between railway transport services on the one hand, and maintenance services on the other hand, the HCC assessed whether the merged entity would have the incentive and ability to foreclose potential rivals from entering in those markets.

In Mytilineos/EPALME, the HCC examined whether the merged entity would be in a position to foreclose upstream rivals from the provision of recycling services, and downstream rivals from the supply of primary aluminium.

In Andromeda/Perseus, a merger between fish farms, there were vertically affected markets due to the target's shares in fish feed markets. However, those market shares were downplayed by the HCC as the target was previously jointly controlled by the acquirer, and the switch to sole control would not create competition risks.

Vertical considerations also came into play in the HCC’s examination of logistics company COSCO's intention to acquire joint control over logistics and rail service provider Pearl. The HCC took the view that the dominant presence of the incumbent railway operator TrainOSE and other likely entries in the logistics market, coupled with the absence of any incentive from the second holder of joint control over Pearl, were unlikely to lead to the foreclosure of COSCO's rivals from the joint venture’s services.

In Adama/Alfa, the HCC examined whether the merged entity would be able to combine Adama’s wide agrochemical portfolio and Alfa's customer base in order to foreclose competitors by creating a one-stop shop distribution point for customers and offering bundle rebates. The HCC ultimately decided it was unlikely that competitors would be foreclosed as a result of such practices, but reserved its enforcement powers for the future.

In merger filings before the HCC, parties are therefore best advised to identify all potential vertical overlaps and carry out an assessment of the vertical effects of the merger.

The HCC has also demonstrated its capacity to cooperate with other independent Greek regulators when reviewing transactions. For example, in both the Alpha Media joint venture and Motor Oil/Alpha Media cases, the HCC got in touch with the National Council of Radio and Television, requesting information to gain technical insights and a more comprehensive view of the relevant markets.

It also asked for the opinion of the railway authority RAS in the TrainOSE/EESTY case, to evaluate whether the merged entity would have the incentive and ability to foreclose potential rivals from entering the primary market or the relevant aftermarkets.

The HCC's merger control activity in 2020 has not exposed any particular industry as suffering from increased consolidation.

The technocratic nature of the HCC means that it does not take political considerations into account - but at the same time, 2019 was a turbulent year for the body. After a long and stable period of independence between 2009 and 2018, the previous government appointed as president and members of the HCC people who had previously held positions as advisers to members of the executive.

The opposition contested those appointments and, in the wake of winning the July 2019 election, it presented new legislation on rules on conflicts, which was adopted by parliament. The Competition Act was amended and the HCC president, vice-president, two commissioners and the director-general were ousted. New appointments came in in September 2019.

Merger enforcement has not been affected by this political turbulence, and it is hoped the new appointees will perform their duties in a manner befitting the HCC tradition of de-politicisation.

The new president of the HCC, Ioannis Lianos, a well-known academic, is particularly attuned to public interest issues and has written extensively in favour of integrating such issues into competition enforcement. It remains to be seen whether such issues will now acquire a specific role in merger enforcement.

Key enforcement trends

The HCC did not block any transactions in the past year. In a total of five cases reaching Phase II, the HCC required remedies only in one, and the remedies were behavioural. Indeed, the HCC has historically blocked only one transaction, in the very early days of Greek merger enforcement - although this case was subsequently cleared by the Minister of Development based on the then applicable system of ministerial authorisation, which has long been repealed.

Recent studies and guidelines

In September 2020, the HCC published a draft staff discussion paper on sustainability issues and competition law. The paper formed part of the HCC's initiative to launch a dialogue around the potential integration of sustainability concerns in EU competition policy and legal analysis.

In the field of merger control, the paper suggested that environmental and sustainability concerns could play a role in the definition of relevant markets, the assessment of efficiencies and the provision of remedies. Member states could also be allowed to deal with local sustainability issues by making use of article 21(4) EUMR, and through the review of mergers under national competition law.

Also in the field of advocacy, the HCC was, at the time of writing, carrying out three sector inquiries, in relation to e-commerce; basic consumer goods; and fintech. It is possible that the results of these inquiries will touch upon merger control.

Looking ahead

As of the time of writing, an expert committee is proposing to amend the Greek Competition Act. The committee is expected to propose no major changes in the merger rules, other than the possibility to accept commitments and clear transactions with remedies in Phase I. Such a possibility has not been available to the HCC and to notifying parties; remedies are only possible in Phase II proceedings.

No other amendment is foreseen.

Merger filings at the Hellenic Competition Commission (HCC) (PDF)

Merger filings at the Hellenic Competition Commission (HCC) (PDF)

THE INSIDETRACK

What should a prospective client consider when contemplating a complex, multi- jurisdictional transaction?

Market definition is critical to the outcome of a case before the HCC. However, the average number of merger cases handled by the HCC do not tend to exceed 10 or 15 per year. As a result, the HCC may often lack the necessary experience and data in relation to specific industries, which may in turn delay its market test and analysis. It is therefore important that notifying parties have readily available as much market data as possible to allow the HCC to expedite its knowledge gathering and education with respect to the relevant markets.

In your experience, what makes a difference in obtaining clearance quickly?

Early engagement with the HCC's DG and case handlers may lead to a short yet fruitful pre-notification period. After notifying, parties are encouraged to maintain open channels of communication with the DG and case handlers, in order to address any requests and concerns that might arise.

What merger control issues did you observe in the past year that surprised you?

Market investigations in all merger cases handled by the HCC in 2019 and so far in 2020 were officially launched two weeks or more after the notification was filed. This is probably due to the mandatory notification deadline of 30 days post-signing, which causes parties to rush the HCC notification before it is deemed complete and satisfactory to case handlers.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP