Making the trading system work for Africa

The African Continental Free Trade Area could trigger a new era in intra-African trade.

By Mukund Dhar, Africa Interest Group Leader

As our last edition of Africa Focus was published in September 2020 in the midst of the COVID-19 pandemic, some progress had been made on the development, trial and authorization of COVID-19 vaccines. However, there was no assurance of efficacy or effectiveness, and there was profound uncertainty in our personal and professional lives, with unprecedented upheaval in the global economy.

This spring 2021 issue comes to you in a changed environment: Multiple vaccines have been approved; millions of vaccine doses are being manufactured and administered every day; and a return to normality feels no longer like a matter of hope, but of time. Therefore, while uncertainty in our lives and disruption in the global economy continues, we can perhaps permit ourselves to review the business and legal environment in Africa with a renewed sense of cautious optimism and against the backdrop of groundbreaking changes that raise important issues for companies and financial institutions doing business in Africa.

Nearly the entire African continent is involved with the African Continental Free Trade Area (AfCFTA), a single trade and investment market with a combined GDP of close to US$3.4 trillion. Trading under these new arrangements started on January 1, 2021. At the same time, development finance institutions have mounted a robust response to the COVID-19 pandemic by harnessing support from international investors and aggressively funding infrastructure and development. Several sectors of Africa’s economy continue to offer private equity and venture capital investment opportunities, while multilateral development banks are successfully supporting post-COVID recovery and growth in key African sectors. Meanwhile, innovative technologies and new approaches to decommissioning mining assets are transforming Africa’s mining industry and enabling sustainable exits.

This sixth edition of Africa Focus begins with "Making the trading system work for Africa," which explains how AfCTA's plan for virtually all African nations to open their markets to each other may have arrived at exactly the right time to spark change. "African development finance institutions" discusses how African DFIs are achieving positive impacts by funding recovery responses, leading the way with sustainable lending and attracting commercial lenders to African markets.

The article "Private equity in Africa: Trends and opportunities in 2021" highlights several industries in Africa that remain attractive private equity and venture capital destinations, particularly for those focused on long-term investments, and "Ensuring sustainable exits from African mining" discusses how mining companies can improve the ways they decommission and close their operations as well as factors that mining companies, regulators and other stakeholders can consider when formulating rules to reflect environmental, social and governance principles.

In "European multilateral development banks in sub-Saharan Africa," we examine how multilateral development banks, including the European Investment Bank, the European Bank for Reconstruction and Development and others, are collaborating with other key stakeholders and acting as catalysts for growth.

Finally, in "African mining 4.0: An innovative sunrise for African miners," we discuss how new transformative technologies, rapidly becoming available to the mining industry, are ushering in a new era of increased productivity, efficiency, safety and growth for miners.

We welcome your suggestions for any topics to review in our upcoming issues. For now, we hope this issue of Africa Focus helps you navigate the rapidly changing business landscape and explore current opportunities for doing business and investing in Africa.

The African Continental Free Trade Area could trigger a new era in intra-African trade.

Rising to challenges, funding a recovery response and leading the way to sustainable lending.

Despite challenges, Africa remains an attractive PE and VC investment destination.

The development of mine decommissioning and closure laws.

Supporting post-COVID recovery and growth in key sectors.

Transformative technologies are ushering in a new era of efficiency, safety and growth.

Rising to challenges, funding a recovery response and leading the way to sustainable lending

Subscribe to receive Africa Focus

World in Transition

Our views on changing dynamics in energy, ESG, finance, globalization and US policy.

Although the nature and scale of the COVID-19 pandemic created an arguably unprecedented challenge, the response of African DFIs has been robust.

African Development Finance Institutions (DFIs) have traditionally played a leading role as:

Although the nature and scale of the COVID-19 pandemic created an arguably unprecedented challenge, the response of African DFIs has been robust. For example, two of the largest, most decisive and immediate responses to the pandemic in Africa included:

At the same time, African DFIs are broadening the products they offer.

How have African DFIs funded these crucial initiatives at a time when there is pressure on member state shareholders to allocate available capital to domestic recovery and pressure on DFIs to intervene across both public and private sectors? In 2020, investor confidence in these institutions remained strong, and macroeconomic policies in developed economies continue to make African DFI risk attractive for investors seeking yield. African DFIs have taken advantage of this opportunity by raising capital in both loan and debt capital markets through some innovative processes.

As a result, African DFIs have an opportunity to become arguably the most relevant financial institutions for the continent's recovery. By harnessing support from international investors and deploying lending proceeds toward sustainable development goals and other sustainability outcomes, as their roles continue to evolve, African DFIs can achieve a potentially exciting outcome.

The sustainable finance market is a natural source of funding for DFIs, given their respective developmental mandates and their role in financing a sustainable recovery from the pandemic in addition to their roles in financing value-accretive supply chains on the continent, creating jobs and supporting industrialization.

African DFIs have been successful in accessing the deep liquidity in this market through proceeds-linked products for green, social and other sustainability purposes. For example: AfDB raised US$3 billion under its Fight Covid-19 social bond, its largest US-dollar benchmark bond to date; Africa Finance Corporation (AFC) incorporated a green tranche into its US$3 billion GMTN program and raised a CHF 150 million green bond; and Banque Ouest-Africaine de Développement (BOAD) raised €750 million under a sustainability bond at the lowest interest rate it has ever achieved in the bond market.

The potential severity of the economic shock across sub-Saharan Africa led many to anticipate general credit deterioration in the assets on the balance sheets of Africa's financial institutions. An innovative example of strategic capital raising in the loan market, was AFC's US$250 million subordinated Tier 2 loan from the US International Development Finance Corporation. This is consistent with similar activity in the commercial bank sector (See AfDB's Tier 2 capital investment into Nedbank below), and AFC described it as complementary to its strategy of further strengthening its investment capacity and diversifying its investor base.

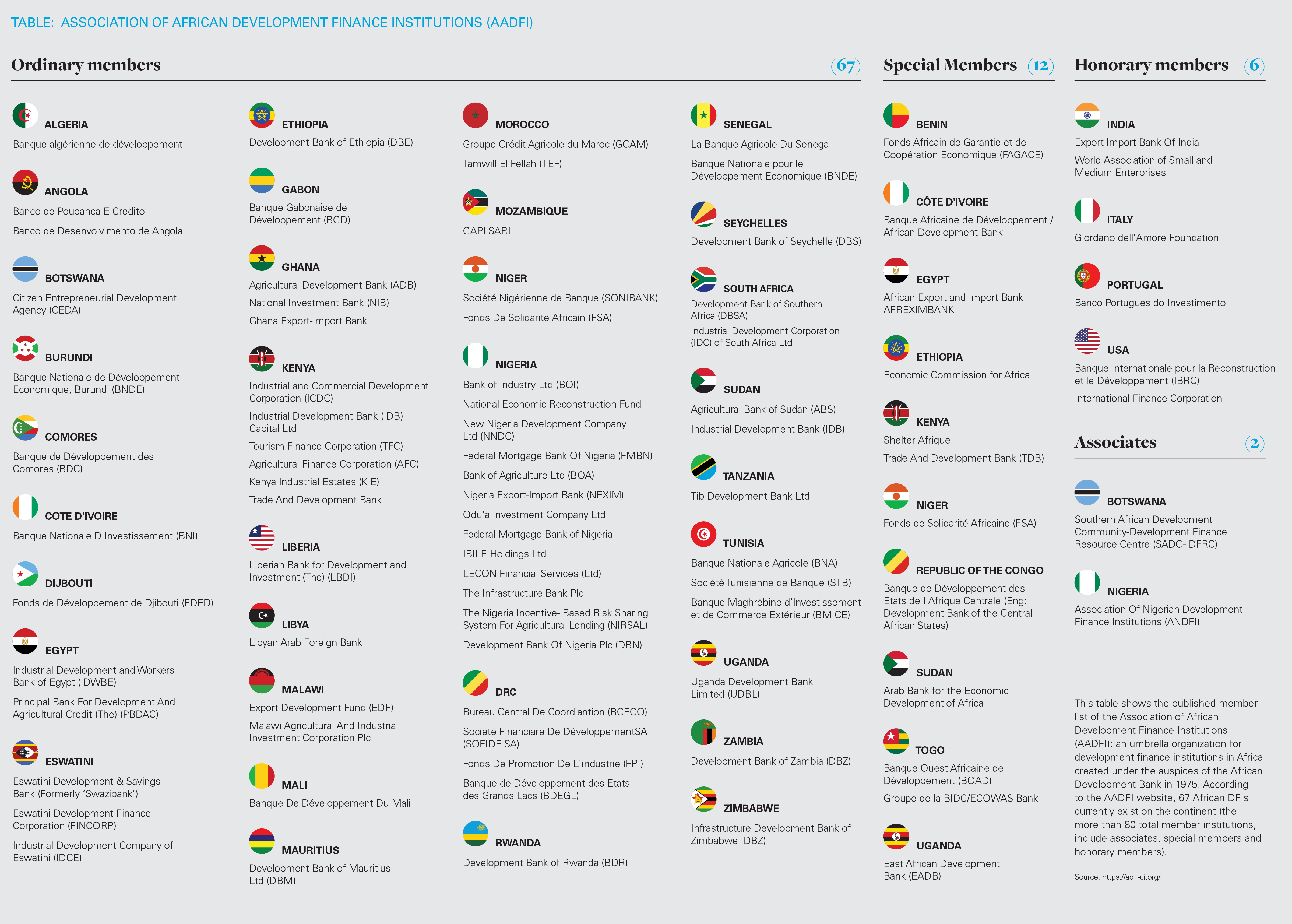

A large number of DFIs exist across Africa (see the Table). However, despite innovations in credit enhancements and structuring (see below), in general terms access to global debt capital and loan markets in volume continues to be dominated by a small number of leading multilateral African or regional DFIs, a theme we expect to continue despite those innovations, since clients indicate that investor demand for high grade African DFI names as a basis for exposure to the continent continues to grow.

AFC attracted a diverse investor base—from Asia-Pacific, the Middle East and Africa, the UK, Switzerland, Germany and other EU countries—in its US$700 million Regulation S Eurobond offering maturing June 2025. The investor confidence in these institutions opens new investment opportunities. For example, Afreximbank tapped into under-utilized Japanese liquidity with a NEXI-backed US$520 million facility, continuing the trend of international bank capital inflows to the African economy and demonstrating "the power of using public resources to leverage private financing for development"1. And investors in the UK, the EU, the US, Asia-Pacific and the Middle East and North Africa over-subscribed for BOAD's sustainability bond offering.

Innovative structuring, particularly the addition of credit enhancement, has also played a role. These institutions do not require credit support in order to raise capital. AfDB is AAA rated (by Moody's, Standard & Poor's, Fitch), and AFC, Afreximbank, BOAD and Eastern and Southern African Trade and Development Bank (TDB) all have investment-grade ratings2.

Nonetheless, the use of credit enhancement has enabled these institutions to borrow on more favorable terms, including longer tenors and lower interest rates. Notable examples from 2020 include: TDB's MIGA-backed ten-year loan from a syndicate of international commercial banks (with the first major deployment in Africa by MIGA of a guarantee against the risk of "non-honoring of financial obligations by a regional development bank"); Afreximbank's NEXI-backed loan; and Bank of Industry (BoI)'s3 €1 billion and US$1 billion facilities, which benefited from credit support from its main shareholder, the Central Bank of Nigeria, in the form of a structured guarantee arrangement and a currency swap to mitigate foreign exchange risks.

BoI is also a case study in how African DFIs can attract commercial lenders to African credit.

Afreximbank arranged BoI's original US$750 million financing in 2018, this borrower's first international syndicated loan and a transaction which, according to Afreximbank, re-opened the syndicated loan market to Nigerian financial institutions. In 2020, as joint co-ordinator with Credit Suisse, it facilitated access for BoI to international finance by committing underwritten debt financing despite the adverse market conditions and (of particular relevance to the €1 billion transaction closed in March 2020) volatility in crude oil prices.

In the end, both facilities were upsized for over-subscription, and each was supported by more than 20 African and international lenders, both commercial and developmental.

The growing trend of providing capital for developmental or social, not purely economic, impact is not new to African DFIs, given their existing developmental impact mandates.

At a national level, BoI aims to "catalyze domestic production and facilitate job creation on a transformational scale, enhance local industry competitiveness, attract domestic and foreign investments, integrate our local industries into domestic, regional and global value chains, grow our export earnings and positively impact the overall economic development of Nigeria."4 The proceeds of BoI's 2020 borrowings will be used to on-lend to eligible institutions that do not operate in "negative sectors," which include coal mining, coal-powered projects and projects that may lead to environmental degradation, while the proceeds of TDB's loan financing are for application to trade finance and COVID-related purposes.

The increase in sustainable finance as the source of funding accelerated the specific change towards financing the resilience of the African economy against the impact of climate change as part of a drive to "build back better." Examples include AFC's use of its green bond proceeds toward renewables projects in Djibouti and Cote d'Ivoire. In addition, proceeds from AfDB's ZAR 2 billion investment in UNSDG-linked notes issued by Nedbank under its domestic MTN program, listed on the green bonds segment of the Johannesburg Stock Exchange, will be used in accordance with Nedbank's Sustainable Development Goals Framework, in alignment with AfDB's "High 5" priorities (Light Up and Power Africa, Feed Africa, Industrialize Africa, Integrate Africa and Improve the Quality of Life for the People of Africa).

African DFIs are very well positioned to continue to enjoy the support of international investors at continental, regional and national levels. The ability of African DFIs to harness this support and channel the proceeds makes them arguably the most relevant financial institutions for the continent's recovery through the pandemic and future growth.

Beyond innovation in, and diversification across, the products they offer, African DFIs will likely continue to use Tier 2 and sustainable finance products in both the loan and the debt capital markets. Moreover, the requirements of development financing institutions and sustainable finance investors into African DFIs might drive one of the most exciting outcomes of these institutions' evolving role.

When deploying the proceeds of these investments, African DFIs have the opportunity to move from the traditional approach of negative sector exclusions to a more positive impact approach that links the proceeds (or the economic terms) of their lending to sustainable development goals or other sustainability outcomes.

This table shows the published member list of the Association of African Development Finance Institutions (AADFI): an umbrella organization for development finance institutions in Africa created under the auspices of the African Development Bank in 1975. According the AADFI website, 67 African DFIs currently exist on the continent (the more than 80 total member institutions, include associates, special members and honorary members).

1 Afreximbank's press release (https://www.afreximbank.com/mufg-leads-on-ground-breaking-520-million-covid-19-response-facility-for-afreximbank/).

2 AFC: A3 (Moody's); Afreximbank: Baa1 (Moody's) / BBB- (Fitch); BOAD: Baa1 (Moody's) / BBB (Fitch); TDB: Baa3 (Moody's) / BB+ (Fitch).

3 Nigeria's state-owned development bank, rated B2 (Moody’s) / B (Fitch).

4 Bank of Industry press release (https://www.boi.ng/boi-concludes-us1000000000-syndicated-term-loan-in-the-international-market/)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2021 White & Case LLP

View full image 'Association of African Development Finance Institutions (AADFI)' (PDF)

View full image 'Association of African Development Finance Institutions (AADFI)' (PDF)