Since the publication of our first report, "Navigating India: Lessons for Foreign Investors," in 2013, India has undergone a remarkable transformation. The country's population grew by 100 million. Fuelled by improved connectivity and digital infrastructure, the number of internet users has soared, with more than half of its citizens now connected to the internet— a significant increase from the mere 12 per cent recorded in 2013. India's GDP has more than doubled, rising from US$1.8 trillion in 2013 to US$3.9 trillion in 2024, underscoring the nation's robust growth trajectory. Per capita income has also improved, reaching US$2,700 in 2024 compared to US$1,400 in 2013.

The Indian government's ambitious programme of regulatory reforms, aimed at making the country an attractive option for international investors, is clearly bearing fruit. In the World Bank's 2020 "Ease of Doing Business" report, India rose to the 63rd position out of 190 countries, marking a significant improvement from its 134th place in 2013. In this compendium, we highlight business opportunities and discuss some of challenges India faces today.

One such challenge is the high-valuation multiples of Indian companies, which have historically dampened cross-border M&A. While these high-valuations present lucrative opportunities for businesses to monetise through listings, they also pose challenges in structuring deals, particularly those involving India-listed subsidiaries and combinations with non-Indian businesses. However, recent regulatory changes, such as permitting share swaps and foreign investors' growing acceptance of Indian securities, are paving the way for innovative deal structures.

India's commitment to achieving net-zero by 2070 is another key issue. The country is pressing ahead with legislative reforms and investment into energy transition on an unprecedented scale, with renewables at the heart of this drive. India has the potential to increase its renewable energy production vastly—whether in solar, wind, hydro, hydrogen or other forms of renewables—and it is making various incentives available to accelerate that process. Legislation and new schemes should make the country even more attractive to investors, and indeed the efforts are already paying off, with a significant number of large investments being committed in recent years.

Technology is also a growth sector. Several multibillion-dollar deals by companies such as Amazon and Apple emphasise the potential of the tech economy. Meanwhile, in infrastructure, the introduction of products such as infrastructure investment trusts and real estate investment trusts make investment by foreign companies more attractive

However successful an investment, there will come a time to exit. In this issue, we examine two ways of exiting Indian investments: through general partner-led secondary transactions and through the public market. Those wishing to exit must plan ahead and put the necessary protections into their documentation at an early stage to avoid potential pitfalls down the track.

India has also made significant strides in reforming its alternative dispute resolution framework, aiming to position itself as a global hub for international arbitration. The 2021 Mediation Bill is another progressive step in making commercial disputes easier to handle, and the supportive stance of Indian courts has amplified positive effects of the legislative reforms.

Investing in India has never been more attractive for foreign investors, and we hope you will find this issue an insightful read.

Indian cross-border investment riding high in booming debt finance market

Against a challenging macro-economic environment worldwide, India has proven resilient and demonstrated its huge potential for growth. With an increasingly favourable regulatory regime and greater avenues of investment, India’s attractiveness as a global market for investors will only continue.

India’s thriving IPO market bucks the global trend

India stands out globally as a market with strong growth in IPO volume, thanks to its dynamic regulatory framework, robust domestic capital market and a large retail investor base. IPOs are also gaining popularity among foreign investors as one of the available exit options from their investments.

Indian cross-border M&A: High valuation hurdles and the hopeful path ahead

Foreign investors in India have historically faced numerous challenges, from high-valuation multiples to regulatory limitations, but evolving market conditions are cause for hope.

The rise of single-asset GP-led secondaries in the Indian investment landscape

The market for private equity-led secondary transactions is growing, and India is steadily catching up with the global trend in embracing these innovative exit strategies.

India’s legal reform in dispute resolution encourages foreign investment

In the past decade, India has made significant strides in reforming its alternative dispute resolution (ADR) framework, aiming to position itself as a global hub for international arbitration. The supportive stance of Indian courts towards arbitration has amplified the positive effects of these reforms.

India’s legal reform in dispute resolution encourages foreign investment

In the past decade, India has made significant strides in reforming its alternative dispute resolution (ADR) framework, aiming to position itself as a global hub for international arbitration. The supportive stance of Indian courts towards arbitration has amplified the positive effects of these reforms.

While investing in India is not without its risks, the courts' and domestic companies' readiness to adopt modern dispute resolution methods offer foreign investors greater comfort than before

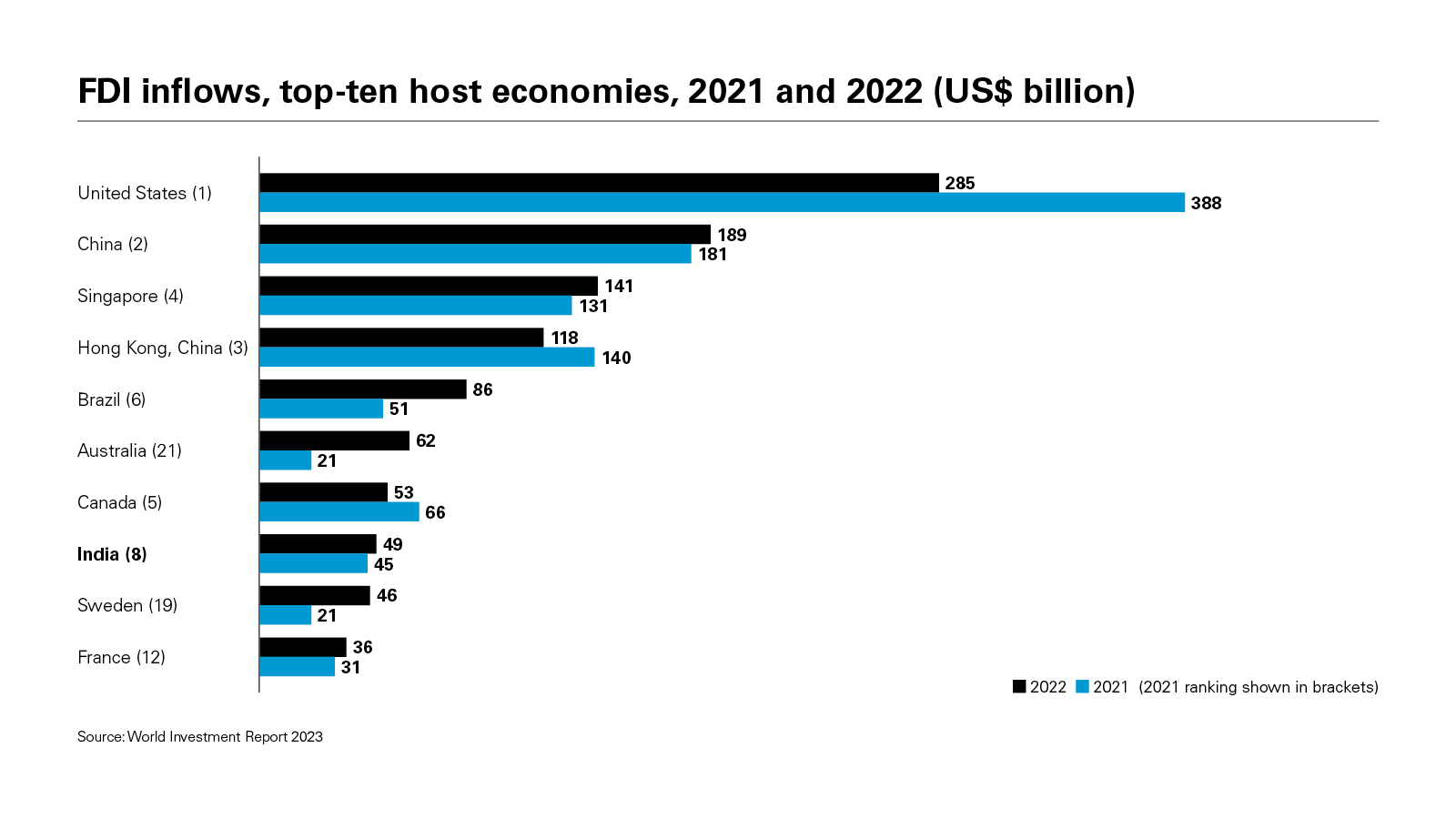

India continues to be an attractive destination for foreign investment, ranking as the world's eighth-largest recipient of foreign direct investment (FDI) in 2022.

With more foreign investors entering the Indian market, understanding how to create balanced contracts and build real relationships becomes fundamental to any business's success. Foreign companies need to consider a number of aspects to help them avoid, manage and resolve conflicts.

Balanced contracts and relationships based on due diligence

The most successful foreign companies in India are those that are committed to long-term, mutually advantageous arrangements with their Indian counterparts. Equal sharing of benefits among partners is essential, as any inequality could result in future complications. For instance, a partner with a minor financial interest might be more inclined to undertake risky bets, thereby opening the door to project delays, cost overruns, and other challenges tied to construction and project completion.

Including exclusivity and non-compete clauses in contracts also helps safeguard an investor's interest and ensures commitments are honoured, even if—or, more likely, when—tempting alternatives may be available. Similarly, the importance of rigorous compliance and accounting controls in all joint venture activities, including financial transactions and receivables, cannot be overstated. Independent auditors should be appointed for this purpose to verify the accuracy of accounts, and compliance with universally recognised accounting standards.

When feasible, contracts should be strengthened with collateral security, as unsecured commitments are inherently risky. In line with the norm in developing economies, a robust physical presence in India holds critical value throughout the investment's lifespan, starting with the due diligence phase.

Investors should therefore send credible analysts to investigate their prospective partners' financials, business operations, management style and cultural ethos. Foreign corporations should not settle for contractual arrangements in India that are lower than what they expect in developed markets.

Any good investment strategy also requires a robust exit strategy to curtail potential losses, mitigate conflicts and minimise disruption. Put options were historically a popular solution, as they grant investors the ability to liquidate their investments by selling their stake at a prearranged price. However, in practice, this may create challenges in India, as disputes can arise over whether the triggering conditions are met, or over price calculations. While no universal remedy exists, having multiple exit options and obtaining specialised advice would help minimise the risk of an investment becoming stranded.

Using alternative dispute resolution in India

India has steadily reformed its alternative dispute resolution (ADR) regime in the past decade to transform itself into a global centre for international arbitration and to streamline the enforcement of contracts. To achieve this, a series of changes were introduced to the Indian Arbitration and Conciliation Act of 1996 in 2015, 2019 and 2020.

Additionally, the supportive stance of Indian courts towards arbitration has amplified the positive effects of these changes. With the recently approved Mediation Bill 2021, organised commercial mediation in India is also set to take off.

The revamped 1996 Arbitration Act aims at promoting a least-interventionist approach by Indian courts, thereby providing some relief to foreign companies who would otherwise be faced with court battles even before arbitration commences.

If a valid arbitration agreement prima facie exists, courts will refer the matter to arbitration without further inquiry— as long as there are no specific non-arbitrable issues including insolvency, criminal offences, or those expressly falling within the domain of specialised courts.

Additionally, arbitral tribunals can now grant interim reliefs that are enforceable as Indian court orders, thus erasing the need to seek interim measures from courts once a tribunal is in place.

The reformed 1996 Arbitraton Act also aims to increase the efficiency of the arbitration process by mandating the parties to complete their written pleadings within six months from the date a tribunal is appointed, and for the tribunal to render an award within 12 months of having entered reference. This is extendable to a maximum of 18 months if the parties agree. In addressing fairness, the 1996 Arbitration Act disallows anyone with a direct or indirect stake in the dispute from acting as an arbitrator—a welcome shift from the earlier trend where it was not unusual for government officials to sit as arbitrators in disputes involving state-owned entities.

Indian courts are also embracing the realities of modern-day arbitration. For example, an Indian court recently held that third-party funding is essential to ensure access to justice, and that a third-party funder—who is neither a party to the arbitral proceedings nor the arbitral award—is not liable to pay any amounts awarded by the arbitral award. This should boost confidence for third-party funders to constructively engage with foreign companies involved in complex, cross-border disputes in India.

Mediation

The 2021 Mediation Bill is another progressive step. Under its framework, parties will have to try and settle their commercial disputes first through mediation before commencing litigation. The mediation process would last 180 days, extendable by another 180 days if parties mutually agree, and any valid settlement agreement would be final and binding, and automatically enforceable.

To ensure its effectiveness, the 2021 Mediation Bill also safeguards the confidentiality of the process as a whole by expressly prohibiting the use of any material from mediation proceedings in any later court or arbitration proceeding. The setting up of a Mediation Council is also proposed to develop appropriate guidelines and lay down standards for professional and ethical conduct of mediators. While these are promising developments, it will have to be seen how these changes materialise in the future.

As resolving disputes in Indian courts can take more than a decade, foreign companies should opt for offshore arbitration with Indian counterparts. Although contracts are often via Indian subsidiaries, the recent Supreme Court case of PASL Wind Solutions v. GE Power confirmed that Indian parties can select an arbitration seat beyond India.

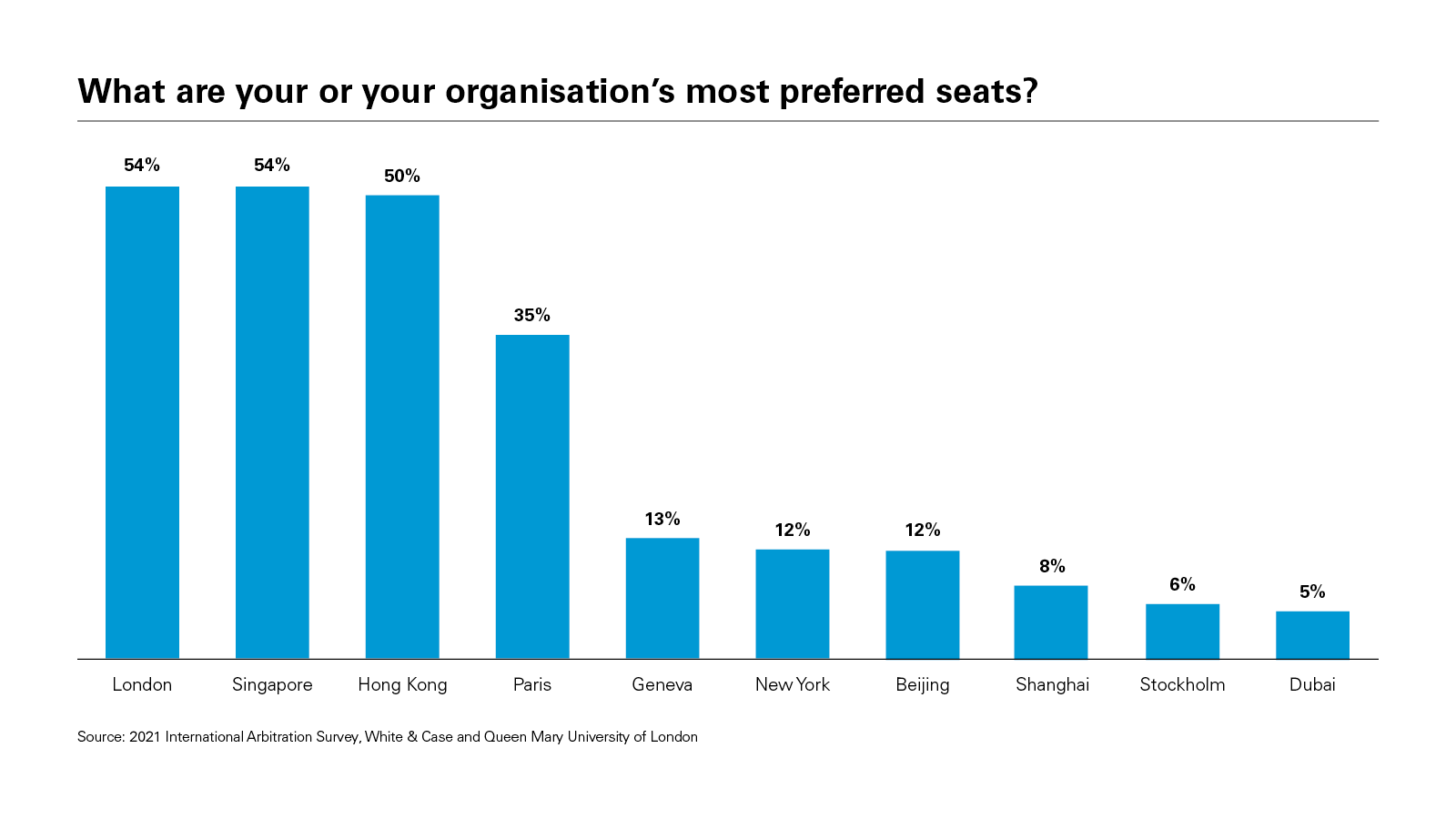

The 2021 survey jointly carried out by White & Case and Queen Mary University of London found Singapore and London were the most preferred arbitration hubs, and both could be attractive options for India-related disputes given the similarities between these jurisdictions' legal traditions and India.

In addition to selecting the seat of arbitration, foreign companies should also consider incorporating in their arbitration agreements the rules of some of the leading global arbitral institutions, such as the Singapore International Arbitration Centre, International Chamber of Commerce or the London Court of International Arbitration.

While institutional arbitration is set to grow in India, particularly with the establishment of the Mumbai Centre for International Arbitration, International Arbitration and Mediation Centre, Hyderabad, and the Delhi International Arbitration Centre, it is likely that global institutions with their longstanding reputations and well-established rules will have an edge over their Indian counterparts.

The previous decade has also witnessed foreign investors bringing disputes against India in relation to their investments under various bilateral investment treaties. Given India's non-membership in the International Centre for Settlement of Investment Disputes Convention, United Nations Commission on International Trade Law–based arbitrations under The Hague–based Permanent Court of Arbitration are common for India-related investment disputes.

From a foreign investor's perspective, it is crucial that any investment complies with Indian laws and is not affected by any illegality. To that end, it would be sensible for foreign companies to seek advice from their legal and financial advisers to make sure that they hold realistic expectations regarding the protection of their investments. The importance of obtaining specialised legal advice cannot be overstated when foreign companies are planning to restructure investments in India to get access to investment treaty protection.

India’s evolving investment treaty regime

Since the opening-up of Indian markets to foreign investment in 1991, India has signed 86 publicly known bilateral investment treaties (BITs) to date. However, since 2016, India unilaterally terminated 76 BITs, with only eight BITs currently in force. India is not alone in this: In 2020, European Union Member States terminated approximately 130 intra-EU BITs; and in 2022 the European Parliament called for an immediate coordinated exit from the Energy Charter Treaty.

However, an existing foreign company having an investment protected by a terminated BIT is likely to continue benefitting from the terminated BITs by virtue of the ‘sunset clause’ in those treaties. A sunset clause survives the BIT and extends treaty-based protections to the investor and its investment for a period of, typically, ten to 15 years.

In the past couple of years, India has signed comprehensive economic partnership or cooperation agreements with Mauritius and the UAE, neither of which contains an investor-state dispute resolution clause. In fact, there is a clear shift towards dispute resolution through consultation, mediation and panel procedures, emulating the World Trade Organization–style dispute resolution mechanism.

That said, to make its existing BIT regime more robust, India consulted with Bangladesh and Colombia, and issued joint interpretative statements in 2017 and 2018 respectively, in which detailed notes provide clarification of key provisions in those BITs and remove ambiguities that often arise from their interpretation. A sound legal understanding of these international agreements would be critical for foreign investors looking to structure their investments and to avoid exposure to risks in the longer term.

Positive outlook for dispute resolution in India

Investing in India is not without its risks, but the willingness of the courts and domestic companies to embrace modern dispute resolution methods means that foreign companies wanting to take advantage of Indian investment opportunities now have far more confidence than they may have previously that they can resolve disputes and protect their investments.

The Supreme Court has shown willingness to provide clarity on some of the areas of uncertainty which remain, and arbitration and mediation are much easier now than they were a few years ago.

The landscape will continue to evolve, and while proper professional advice is still absolutely critical, the risks can most certainly be mitigated to take advantage of India's opportunities.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: FDI inflows, top-ten host economies, 2021 and 2022 (US$ billion) (PDF)

View full image: FDI inflows, top-ten host economies, 2021 and 2022 (US$ billion) (PDF)

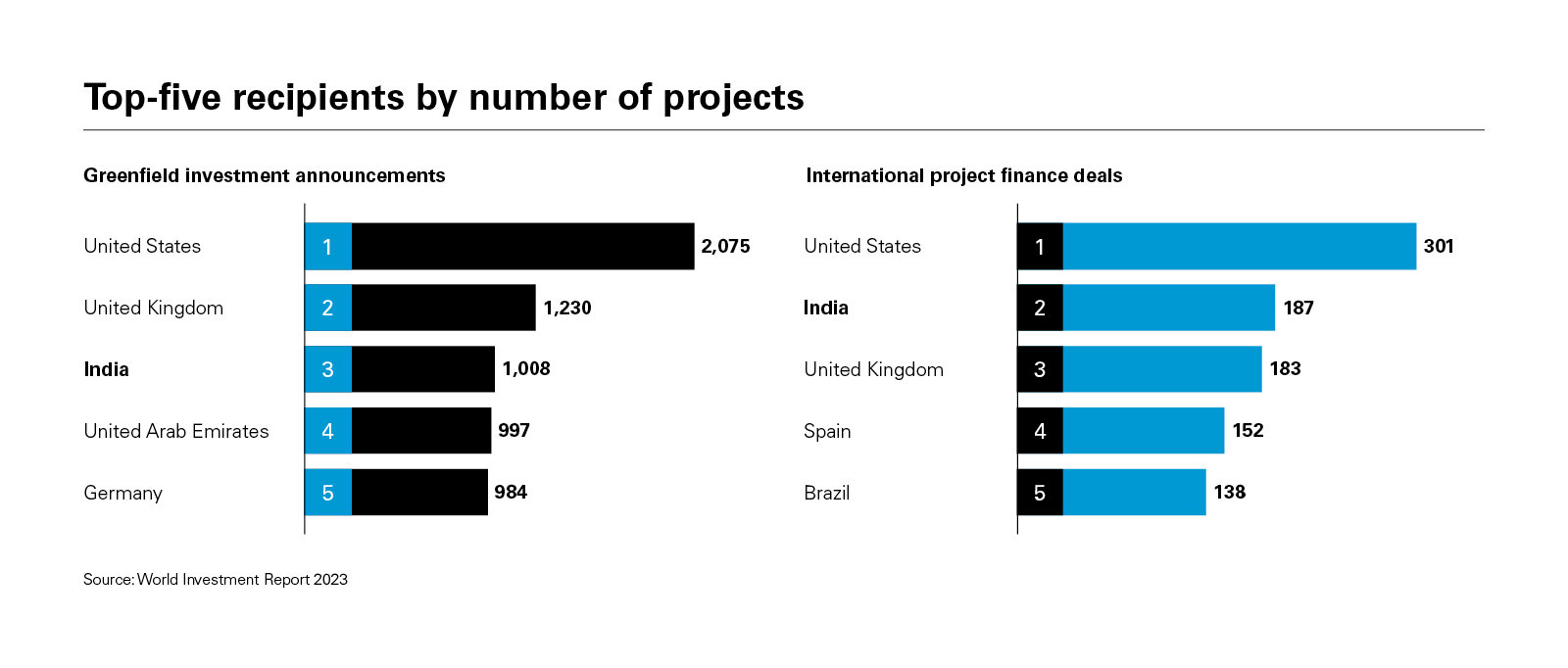

View full image: Top-five recipients by number of projects (PDF)

View full image: Top-five recipients by number of projects (PDF)

View full image: What are your or your organisation’s most preferred seats? (PDF)

View full image: What are your or your organisation’s most preferred seats? (PDF)