Since the publication of our first report, "Navigating India: Lessons for Foreign Investors," in 2013, India has undergone a remarkable transformation. The country's population grew by 100 million. Fuelled by improved connectivity and digital infrastructure, the number of internet users has soared, with more than half of its citizens now connected to the internet— a significant increase from the mere 12 per cent recorded in 2013. India's GDP has more than doubled, rising from US$1.8 trillion in 2013 to US$3.9 trillion in 2024, underscoring the nation's robust growth trajectory. Per capita income has also improved, reaching US$2,700 in 2024 compared to US$1,400 in 2013.

The Indian government's ambitious programme of regulatory reforms, aimed at making the country an attractive option for international investors, is clearly bearing fruit. In the World Bank's 2020 "Ease of Doing Business" report, India rose to the 63rd position out of 190 countries, marking a significant improvement from its 134th place in 2013. In this compendium, we highlight business opportunities and discuss some of challenges India faces today.

One such challenge is the high-valuation multiples of Indian companies, which have historically dampened cross-border M&A. While these high-valuations present lucrative opportunities for businesses to monetise through listings, they also pose challenges in structuring deals, particularly those involving India-listed subsidiaries and combinations with non-Indian businesses. However, recent regulatory changes, such as permitting share swaps and foreign investors' growing acceptance of Indian securities, are paving the way for innovative deal structures.

India's commitment to achieving net-zero by 2070 is another key issue. The country is pressing ahead with legislative reforms and investment into energy transition on an unprecedented scale, with renewables at the heart of this drive. India has the potential to increase its renewable energy production vastly—whether in solar, wind, hydro, hydrogen or other forms of renewables—and it is making various incentives available to accelerate that process. Legislation and new schemes should make the country even more attractive to investors, and indeed the efforts are already paying off, with a significant number of large investments being committed in recent years.

Technology is also a growth sector. Several multibillion-dollar deals by companies such as Amazon and Apple emphasise the potential of the tech economy. Meanwhile, in infrastructure, the introduction of products such as infrastructure investment trusts and real estate investment trusts make investment by foreign companies more attractive

However successful an investment, there will come a time to exit. In this issue, we examine two ways of exiting Indian investments: through general partner-led secondary transactions and through the public market. Those wishing to exit must plan ahead and put the necessary protections into their documentation at an early stage to avoid potential pitfalls down the track.

India has also made significant strides in reforming its alternative dispute resolution framework, aiming to position itself as a global hub for international arbitration. The 2021 Mediation Bill is another progressive step in making commercial disputes easier to handle, and the supportive stance of Indian courts has amplified positive effects of the legislative reforms.

Investing in India has never been more attractive for foreign investors, and we hope you will find this issue an insightful read.

Indian cross-border investment riding high in booming debt finance market

Against a challenging macro-economic environment worldwide, India has proven resilient and demonstrated its huge potential for growth. With an increasingly favourable regulatory regime and greater avenues of investment, India’s attractiveness as a global market for investors will only continue.

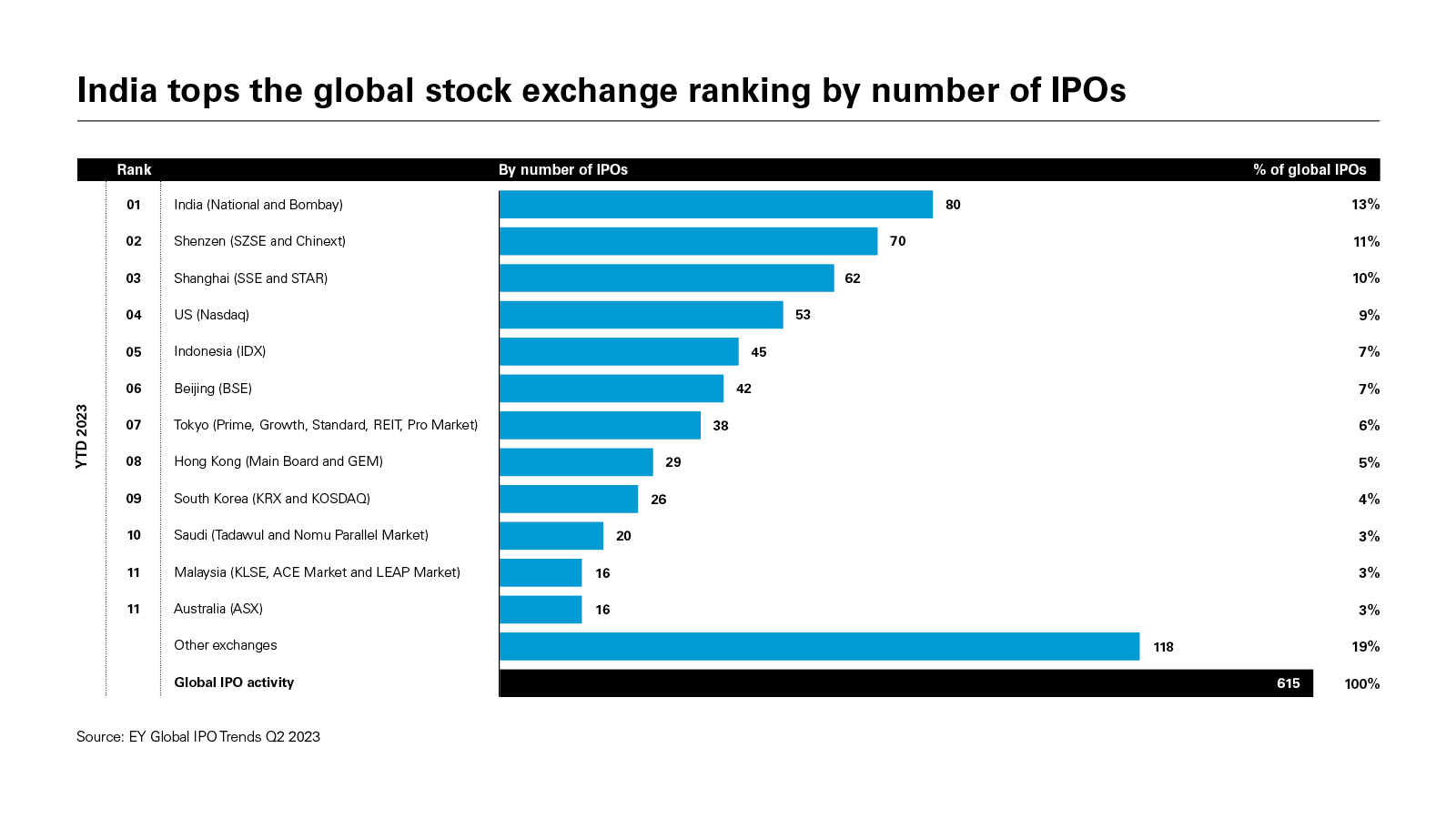

India’s thriving IPO market bucks the global trend

India stands out globally as a market with strong growth in IPO volume, thanks to its dynamic regulatory framework, robust domestic capital market and a large retail investor base. IPOs are also gaining popularity among foreign investors as one of the available exit options from their investments.

Indian cross-border M&A: High valuation hurdles and the hopeful path ahead

Foreign investors in India have historically faced numerous challenges, from high-valuation multiples to regulatory limitations, but evolving market conditions are cause for hope.

The rise of single-asset GP-led secondaries in the Indian investment landscape

The market for private equity-led secondary transactions is growing, and India is steadily catching up with the global trend in embracing these innovative exit strategies.

India’s legal reform in dispute resolution encourages foreign investment

In the past decade, India has made significant strides in reforming its alternative dispute resolution (ADR) framework, aiming to position itself as a global hub for international arbitration. The supportive stance of Indian courts towards arbitration has amplified the positive effects of these reforms.

India’s thriving IPO market bucks the global trend

India stands out globally as a market with strong growth in IPO volume, thanks to its dynamic regulatory framework, robust domestic capital market and a large retail investor base. IPOs are also gaining popularity among foreign investors as one of the available exit options from their investments.

India's IPO market grew to US$3.26 trillion in 2023 from US$22 billion in 2021

IPOs are gaining in popularity due to a robust domestic capital market with a large retail investor base fuelled by a dynamic regulatory framework overseen by SEBI

While planning and executing investments into India, it is important for foreign investors to plan their exit options from their investments. Among the various choices available, public market exits through initial public offerings (IPOs) are gaining in popularity. This is largely due to a robust domestic capital market with a large retail investor base, fuelled by a dynamic regulatory framework overseen by the Securities and Exchange Board of India (SEBI).

SEBI, formed in the wake of liberalisation of the Indian economy in the 1990s, has grown in strength with every passing decade. As a regulator with twin objectives of promoting Indian capital markets and regulating capital markets, it has over time managed to walk this tightrope and oversee the growth of the Indian market from lows of US$55 billion in 1993 to US$3.26 trillion in 2023.

Through regulation and oversight, SEBI has developed a robust regulatory framework for public market transactions. These include novel features for promoting retail participation while also protecting these investors. A balance of commercial interests and regulatory prudence has helped Indian issuers raise capital from domestic and foreign investors with increasing deal sizes.

This framework has also resulted in the public market exit becoming an increasingly popular option for foreign investors. This option allows foreign investors to release public market valuations and sell large stakes, while providing them with a liquid versatile stock exchange framework to sell any remaining holdings in their portfolios.

The popularity of public market exits has also brought with it a regulatory pivot from SEBI to ensure a level playing field. Some of these regulatory positions need to be evaluated and factored in by investors at the stage of their entry into an Indian investment to minimise issues that may arise while planning their exit with the passage of time.

Shareholder rights in companies undertaking an IPO

The basic structure for protection of contractual rights under shareholder agreements in India requires that the terms of the shareholder agreement are also included in the charter documents of the company. Once the decision to undertake a public offering of equity shares is made, pre-IPO investors with special rights need to get comfortable with the position that these special protections will fall away: These rights are not required once the company is publicly traded. All shareholders in a publicly traded company are afforded the same rights and protections under law, and there should be no special treatment for any constituency.

While pre-IPO investors have become used to this premise, the timing and the way these rights fall away are things that present some issues. The process for completing an IPO is a long, drawn-out affair which may extend up to a year or longer, and accordingly pre-IPO investors want to ensure that they have the protections of special rights for as long as possible, up to the actual listing of the equity shares.

Market practice has evolved to allow for these rights and protections for pre-IPO shareholders to be retained up to the date of the 'red herring' prospectus; the rationale being that once the company files the 'red herring', the IPO is imminent, and the exit contemplated by pre-IPO investors is all but assured.

However, in recent regulatory pronouncements, SEBI has asked that all rights be removed from charter documents at the stage of filing of a draft prospectus with them for approval—some three to nine months prior to the 'red herring' prospectus stage. This creates a legal dilemma for pre-IPO investors, where they give up the legal safeguard of their rights, but the potential IPO is not yet a certainty.

Currently, a balance has been struck where the shareholder agreement subsists but the charter documents are amended to remove the special rights as of the date of filing with SEBI. This is not an ideal legal position for the company and pre-IPO investors if a dispute were to arise in relation to the management of the company. The conflict between the shareholders' agreement and the charter documents may only be settled using dispute resolution mechanisms and will certainly result in an erosion of value.

Information sharing and continuous disclosure obligations

In an effort to bring more transparency to the initial public offering pricing process in India, SEBI introduced a requirement for mandatory disclosures of key performance indicators (KPIs) by issuers. This was largely prompted by the increase in the filings for IPOs by new-age technology companies that were generally loss-making, in the growth phase of their business and with differing standards of disclosure of financial information. This created a perception that there was no parity of information shared across categories of investors at different stages of a company's investment cycle, with early-stage investors or private equity investors having a different set of metrics from investors in the IPO.

SEBI mandates that an issuer is required to disclose all KPIs that have been disclosed to investors in the previous three years, along with an explanation on how they have been historically used to analyse, track, and monitor the company's business and financial performance. The comparison of these indicators over time must also be explained based on additions or dispositions to the business.

Typically, pre-IPO investors are provided a large amount of data under their contractual arrangements, which is in line with the risk adopted by an investor in the start-up or growth phase of a business. The kind of information shared includes business plans, projections and financial data. The intended outcome of the SEBI position is that this information is included in the offering documents, so all investors have the same level of information to evaluate an investment decision in the issuer. This assumes that the information shared with pre-IPO investors is beyond the mandatory disclosures prescribed by law for an IPO. This additional data set of performance indicators will allow investors to better evaluate the pricing of shares in an IPO and make an informed decision in relation to investing in the IPO and post-IPO trading performance.

SEBI requires the KPIs to be approved by the audit committee of an issuer and to be certified by the statutory auditors or peer-reviewed by independent chartered accountants (ICA). Often, the KPIs provided to pre-IPO investors in the three years preceding the IPO are not audited or reviewed by the statutory auditors or an ICA. Depending on the stage at which the issuer received the pre-IPO investment, information may have been culled out of internal management financial reports, internal estimates or even prepared with assumptions and may not have reflected the actual business and financial performance. The data may often have been presented without the rigor required for an independent audit.

Pre-IPO investors, being sophisticated investors, would have had the means to discern this information, fully understanding the risks with the data. However, when presenting this information in prospectus to public market investors, the KPIs must be subjected to audit procedures to ensure that the information is audited or derived from the restated and audited financial information. This presents practical challenges of differing magnitudes. For example, auditors may refuse to audit certain information or find themselves in a position where the data cannot be subjected to an audit. The jury is out on what happens when a pre-IPO investor sees significantly different information in an issuer company's offer document compared to what was shared with them historically.

The role of a ‛promoter'

A unique feature of the IPO process in India is the requirement for an IPO-bound company to declare a major shareholder as a 'promoter'. The legal definition and concept are meant to capture an entity that, through shareholding and management, controls the company. The designation comes with a requirement to agree to a statutory lock-up of shareholding up to a prescribed per centage, as well as routine periodic reporting of specific information. The promoters have to provide specific information to be included in the prospectus, specifically relating to material litigations and provide underwriters with various linked confirmations. These disclosures carry the attendant liability risk for misstatements and omissions in the prospectus.

With an increasing number of private equity investors taking control positions in Indian companies, the designation of 'promoter' presents some challenges. Private equity fund structures that house their investments in special purpose vehicles are faced with the prospect of naming their global asset managers as promoters.

Investors may also, through dialogue with SEBI, get a determination of the company having no promoter and being professionally managed. In such scenarios, a major shareholder would need to step up to provide its shareholding to satisfy the statutory lock-in. Entities that are designated as promoters may also be asked to provide contractual representations and warranties in underwriting agreements.

When making investment decisions in relation to control or when assessing their partners in Indian ventures, investors should keep all these issues in mind. While none of them present regulatory dealbreakers, they do present issues to consider if an IPO is the preferred route of exit.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

View full image: India tops the global stock exchange ranking by number of IPOs (PDF)

View full image: India tops the global stock exchange ranking by number of IPOs (PDF)