Since the publication of our first report, "Navigating India: Lessons for Foreign Investors," in 2013, India has undergone a remarkable transformation. The country's population grew by 100 million. Fuelled by improved connectivity and digital infrastructure, the number of internet users has soared, with more than half of its citizens now connected to the internet— a significant increase from the mere 12 per cent recorded in 2013. India's GDP has more than doubled, rising from US$1.8 trillion in 2013 to US$3.9 trillion in 2024, underscoring the nation's robust growth trajectory. Per capita income has also improved, reaching US$2,700 in 2024 compared to US$1,400 in 2013.

The Indian government's ambitious programme of regulatory reforms, aimed at making the country an attractive option for international investors, is clearly bearing fruit. In the World Bank's 2020 "Ease of Doing Business" report, India rose to the 63rd position out of 190 countries, marking a significant improvement from its 134th place in 2013. In this compendium, we highlight business opportunities and discuss some of challenges India faces today.

One such challenge is the high-valuation multiples of Indian companies, which have historically dampened cross-border M&A. While these high-valuations present lucrative opportunities for businesses to monetise through listings, they also pose challenges in structuring deals, particularly those involving India-listed subsidiaries and combinations with non-Indian businesses. However, recent regulatory changes, such as permitting share swaps and foreign investors' growing acceptance of Indian securities, are paving the way for innovative deal structures.

India's commitment to achieving net-zero by 2070 is another key issue. The country is pressing ahead with legislative reforms and investment into energy transition on an unprecedented scale, with renewables at the heart of this drive. India has the potential to increase its renewable energy production vastly—whether in solar, wind, hydro, hydrogen or other forms of renewables—and it is making various incentives available to accelerate that process. Legislation and new schemes should make the country even more attractive to investors, and indeed the efforts are already paying off, with a significant number of large investments being committed in recent years.

Technology is also a growth sector. Several multibillion-dollar deals by companies such as Amazon and Apple emphasise the potential of the tech economy. Meanwhile, in infrastructure, the introduction of products such as infrastructure investment trusts and real estate investment trusts make investment by foreign companies more attractive

However successful an investment, there will come a time to exit. In this issue, we examine two ways of exiting Indian investments: through general partner-led secondary transactions and through the public market. Those wishing to exit must plan ahead and put the necessary protections into their documentation at an early stage to avoid potential pitfalls down the track.

India has also made significant strides in reforming its alternative dispute resolution framework, aiming to position itself as a global hub for international arbitration. The 2021 Mediation Bill is another progressive step in making commercial disputes easier to handle, and the supportive stance of Indian courts has amplified positive effects of the legislative reforms.

Investing in India has never been more attractive for foreign investors, and we hope you will find this issue an insightful read.

Indian cross-border investment riding high in booming debt finance market

Against a challenging macro-economic environment worldwide, India has proven resilient and demonstrated its huge potential for growth. With an increasingly favourable regulatory regime and greater avenues of investment, India’s attractiveness as a global market for investors will only continue.

India’s thriving IPO market bucks the global trend

India stands out globally as a market with strong growth in IPO volume, thanks to its dynamic regulatory framework, robust domestic capital market and a large retail investor base. IPOs are also gaining popularity among foreign investors as one of the available exit options from their investments.

Indian cross-border M&A: High valuation hurdles and the hopeful path ahead

Foreign investors in India have historically faced numerous challenges, from high-valuation multiples to regulatory limitations, but evolving market conditions are cause for hope.

The rise of single-asset GP-led secondaries in the Indian investment landscape

The market for private equity-led secondary transactions is growing, and India is steadily catching up with the global trend in embracing these innovative exit strategies.

India’s legal reform in dispute resolution encourages foreign investment

In the past decade, India has made significant strides in reforming its alternative dispute resolution (ADR) framework, aiming to position itself as a global hub for international arbitration. The supportive stance of Indian courts towards arbitration has amplified the positive effects of these reforms.

On the path to net-zero: Legislating for energy transition in India

The Indian government is pressing ahead with legislative reforms and investments on an unprecedented scale in the energy transition. However, to achieve India’s ambitious goal of reaching net-zero by 2070, significant investment from the private sector is essential.

IEA estimates that the investment required for achieving India’s 2070 targets would be approximately US$160 billion per year between now and 2030

India is committed to reaching net-zero emissions by 2070 and achieving 50 per cent cumulative electric power-installed capacity from non-fossil fuel-based energy resources by 2030

At the UN Climate Change Conference held in Glasgow (COP26) in 2021, India committed to reaching net-zero emissions by 2070. This commitment was backed with other near-term targets for 2030, including achieving about 50 per cent cumulative electric power-installed capacity from non-fossil fuel-based energy resources, reducing the emissions intensity of its GDP by 45 per cent from the 2005 level, and increasing its non-fossil electricity generation capacity to 500 GWs.

India currently relies on fossil fuels to meet approximately 56 per cent of its energy needs. The International Energy Agency estimates that the investment required for achieving India’s 2070 targets would be US$160 billion per year, on average, between now and 2030.

Legislating for energy transition

In order to try and reach its energy transition goals, the Indian government has enacted the Energy Conservation Amendment Act 2022, which amended the Energy Conservation Act (ECA) 2001 and came into force on 1 January 2023.

Among the key changes brought by the legislation was the introduction of a carbon credit trading scheme. Per the ECA Amendment, carbon credit certificates can be issued by the government or other authorised agencies to registered entities compliant with the scheme, which can then sell these certificates. The ECA Amendment has also given the government the right to specify a minimum share of consumption of non-fossil sources as energy or feedstock by certain designated consumers, which include industries such as aluminium, fertilisers, iron and steel, cement, pulp and paper, textile, chemicals, railways, transport sector, petrochemicals, petroleum refineries, thermal power stations, hydro-power stations, electricity transmission companies and distribution companies, and commercial buildings or establishments. These changes have the potential to catalyse significant changes in India’s energy landscape.

US$2.4 billion

India's government has allocated US$2.4 billion to the National Green Hydrogen Mission to support production, use and exports of green hydrogen

Supporting green hydrogen

In January 2023, India launched its National Green Hydrogen Mission to support production, use and exports of green hydrogen and its derivatives. The mission provides financial incentive mechanisms for domestic manufacturing of electrolysers and production of green hydrogen, and will support pilot projects in emerging end-use sectors and production pathways.

Regions capable of supporting large-scale production or use of hydrogen will be identified and developed as green hydrogen hubs. The amount allocated to the mission is INR 197.4 billion (approximately US$2.4 billion), including an allocation of INR 174.9 billion (approximately US$2.1 billion) for the financial incentives, and the remaining for pilot projects, R&D and other mission objectives.

In June 2023, the Ministry of New and Renewable Energy (MNRE) released guidelines for two schemes implementing these financial incentives.

The Incentive Scheme for Electrolyser Manufacturing will be implemented through the Solar Energy Corporation of India (SECI) through a competitive bidding process. Successful bidders are eligible for financial incentives for five years starting with a base incentive of INR 4,440/kW (approximately US$53.31/kW) in the first year from the date of commencement of manufacturing of electrolysers, which will gradually reduce on an annual basis. The calculation of incentives will factor in the specific energy consumption of electrolysers, as this impacts the cost of green hydrogen, and local value addition. The second scheme, the Incentive Scheme for Green Hydrogen Production (under Mode 1) is also implemented through SECI. 'Mode 1’ anticipates bidding on the least incentive demanded over a three-year period through a competitive selection process. Successful bidders are eligible for financial incentives in terms of INR/kg of green hydrogen production for a period of three years from the date of the start of production, with the incentives capped each year and reducing from INR 50/kg (US$0.6/kg) in the first year to INR 30/kg (US$0.36/kg) in the third year.

The Indian government has introduced several measures to enhance solar domestic manufacturing capacity for renewables projects

Other incentives for renewable energy

The Indian government has also introduced several measures to enhance solar domestic manufacturing capacity for renewable projects. Recently, it concluded two tranches of allocations under the Production Linked Incentives (PLI) Scheme for high-efficiency solar photovoltaic (PV) modules. The winning bidders under this scheme will be paid financial incentives on an annual basis upon sales of high-efficiency solar PV modules for five years.

A total capacity of approximately 48 GWs was awarded to various companies, and a portion will be eligible for financial incentives totalling approximately INR 185 billion (approximately US$2.2 billion). Some of the winning bidders in the recent tranche include Reliance, Indosol, First Solar, Waaree, ReNew and Tata Power Solar.

Another way in which the government has tried to address grid access challenges for renewable energy consumers is through the passage of the Electricity (Promoting Renewable Energy Through Green Energy Open Access) Rules 2022. The rules aim to promote the generation, purchase and consumption of green energy, including from waste-to-energy plants, through improving open access.

Key features of the rules include the setting up of a nodal agency that streamlines the approval process for consumers seeking open access, with deemed approval after 15 days, providing certainty on the open access charges to be levied on green energy open access consumers, and allowing consumers to choose to receive green energy at their discretion. The Central Electricity Regulatory Commission has also announced the CERC (Connectivity and General Network Access to the Inter-State Transmission System) Regulations 2022, which aim to provide flexible, non-discriminatory open access to power producers, allowing them to withdraw and inject power without having to specify a transmission route, and to specify an offtaker when seeking connectivity.

Separately, the government announced in the recent National Framework for Promoting Energy Storage Systems Viability Gap Funding (VGF) scheme worth INR 37.6 billion (approximately US$451 million) to boost the set-up of battery energy storage system (BESS) projects. The scheme will fund up to 40 per cent of the capital cost for private developers of BESS projects that are economically justified but not financially viable.

The scheme envisages the development of 4000 MWh of BESS projects by 2030-31, with VGF being disbursed in five tranches linked to stages of implementation of the projects. To ensure that the scheme’s benefits reach consumers, a minimum of 85 per cent of project capacity will be made available to distribution companies (DISCOMs). More details are awaited.

Another key development for energy storage is the passage of guidelines to promote the development of Pumped Storage Projects (PSPs). The guidelines include transparent criteria for allotting project sites to developers, the removal of the upfront premium for project allocation, market reforms for monetisation of ancillary services provided by PSPs, enabling government land to be made available at a concessionary rate to developers, the exemption of PSPs from free power obligation, the rationalisation of environmental clearances for off-river PSP sites and utilisation of exhausted mines for development of PSPs. Certain state-controlled financial institutions will be required to treat PSPs at par with other renewable energy projects per the guidelines, while extending long-term loans of 20 to 25 years.

The government has also allocated INR 350 billion (approximately US$4.2 billion) in the national budget for 2023/24 towards energy transition, and announced a National Electricity Plan.

The private sector will be key to the energy transition process, and the government is introducing various measures to promote private sector investment.

Foreign investors are allowed to make 100 per cent investments in the renewable energy sector under the automatic route, without requiring prior government approval. The external commercial borrowing (ECB) limit set by the Reserve Bank of India under foreign exchange laws is US$750 million or equivalent per financial year per company, subject to satisfaction of additional requirements under ECB regulations. One increasingly common way for renewable energy companies, including government-backed entities, to raise money for energy transition through the ECB framework is the issuance of green bonds. Most recently, ReNew’s subsidiary Diamond II Limited raised US$400 million through an oversubscribed high yield green bond issuance.

There are also several renewable energy auctions planned. In April 2023, MNRE announced bidding goals for renewable energy power projects from 2023/24 to 2027/28. For each of these years, the government intends to issue bids for 50 GWs of renewable energy, consisting of solar, wind, solar-wind hybrid, round-the-clock renewable energy power, with or without storage, or any other combination based on market assessment or government directions.

The bids will be floated by state-appointed renewable energy-implementing agencies and in accordance with relevant standard bidding guidelines issued by the government and according to MNRE’s advice. A number of the bidding guidelines have been recently updated, notably for wind, solar, hybrid power and renewable energy power projects with energy storage systems. Among other things, these guidelines set out streamlined processes for bidding and evaluation of bids, specify requirements for earnest money deposits and guarantees, include standard provisions to be included in each model PPA issued along with bids, set out promoter/ sponsor shareholding restrictions, and address responsibility for transmission connectivity. MNRE also expects to auction 37 GWs of offshore wind capacity during fiscal years 2022 – 2030, with the initial eight GWs being offered in the next two years. A total of eight offshore wind energy zones have been identified off the coasts of the states of Gujarat and Tamil Nadu for this purpose.

The government’s efforts to promote energy transition have seen strong support from India’s private sector

Challenges to energy transition

Not unlike other nations, India's journey of transitioning to renewable energy is subject to several challenges, particularly expanding reliable energy access and use while maintaining consumer affordability and financial stability for DISCOMS; increasing the share of renewable energy sources in a reliable manner; and reducing carbon emissions to achieve ambitious climate objectives while meeting its social and economic goals.

A major limitation to reliable renewable energy access is India's grid infrastructure, which requires a significant upgrade to adapt to the intermittent nature of renewable power. Grids powered by renewable energy require a lot more effort to achieve stability in times of disruption than conventional energy sources, which can ramp up or down production as required.

Other operational issues commonly attributed to this mismatch include the overloading of transmission lines at certain times, demand-supply disparities, frequency and voltage issues, losses of electricity transmission, a lack of coordination among state-level transmission planners and central planning agencies, and in the context of renewable power, varied concentrations of renewable power generation across regions. The Ministry of Power reported that in 2021/22, the total electricity lost in transformation, transmission and distribution systems and electricity unaccounted for represented 19.27 per cent of the total available electricity.

Grid infrastructure issues are further exacerbated by the weak financial health of DISCOMs. Payment delays by state- owned DISCOMs have been common, leading to a build-up of receivables from offtakers and an increase in debt for renewable energy companies. In addition, DISCOMs have not been able to cover their own costs due to outdated billing systems, obsolete infrastructure, power loss and theft, and increases in energy costs.

Although the performance of DISCOMs has been noted to be improving, they are still incurring heavy operational losses. These issues have in turn previously resulted in project delays, retendering or cancellations. A number of states, including Andhra Pradesh, Uttar Pradesh and Gujarat, have attempted to renegotiate power purchase agreements (PPAs) signed with independent power producers to lower tariffs, which were historically much higher than they are today. Although these attempts have so far been unsuccessful, legal action to remedy this is lengthy, and producers suffer from reduced or no payment during the process. The MNRE is trying to remedy common issues, for example by revising the dispute resolution mechanism for disputes between developers, contractors and renewable energy-implementing agencies like SECI and NTPC.

Another challenge is managing the economy of coal-dependent states to steady the increasing share of renewable energy of some states. In the past years, renewable energy installations have been concentrated —up to 78 per cent according to MNRE—in only a few states such as Karnataka, Gujarat, Rajasthan, Maharashtra, Tamil Nadu and Andhra Pradesh. On the other hand, certain states such as Jharkhand, Chhattisgarh, Odisha, Telangana and West Bengal rely heavily on coal for their economic development. For the moment, India's focus has been to increase production on all fronts to ensure its energy security, but in the long run, it expects to gain significantly from its policy push supporting the domestic production of green hydrogen and other alternative fuels.

Energy transition also suffers from other challenges that are common to all infrastructure project development in India. Land acquisition for large-scale renewable projects is cost-intensive with limited government support. Even after being legally acquired, possession of land remains a challenge, and project companies have been dragged into legal battles over ownership. Finally, there are various permits to be obtained depending on the location of the site, including environment, wildlife, ceiling limits, government land allotment, ancestral property state laws, and so on. As all processes for permits and approvals are not effectively streamlined in states, these can take a lot of time to be obtained depending on the location.

Not unlike other nations, India’s journey of transitioning to renewable energy is subject to several challenges, particularly expanding reliable energy access and use while maintaining consumer affordability and financial stability for DISCOMS; increasing the share of renewable energy sources in a reliable manner; and reducing carbon emissions to achieve ambitious climate objectives while meeting its social and economic goals.

A major limitation to reliable renewable energy access is India’s grid infrastructure, which requires a significant upgrade to adapt to the intermittent nature of renewable power. Grids powered by renewable energy require a lot more effort to achieve stability in times of disruption than conventional energy sources, which can ramp up or down production as required. Other operational issues commonly attributed to this mismatch include the overloading of transmission lines at certain times, demand-supply disparities, frequency and voltage issues, losses of electricity transmission, a lack of coordination among state-level transmission planners and central planning agencies, and in the context of renewable power, varied concentrations of renewable power generation across regions. The Ministry of Power reported that in 2021/22, the total electricity lost in transformation, transmission and distribution systems and electricity unaccounted for represented 19.27 per cent of the total available electricity.

Grid infrastructure issues are further exacerbated by the weak financial health of DISCOMs. Payment delays by state-owned DISCOMs have been common, leading to a build-up of receivables from offtakers and an increase in debt for renewable energy companies. In addition, DISCOMs have not been able to cover their own costs due to outdated billing systems, obsolete infrastructure, power loss and theft, and increases in energy costs. Although the performance of DISCOMs has been noted to be improving, they are still incurring heavy operational losses. These issues have in turn previously resulted in project delays, retendering or cancellations. A number of states, including Andhra Pradesh, Uttar Pradesh and Gujarat, have attempted to renegotiate power purchase agreements (PPAs) signed with independent power producers to lower tariffs, which were historically much higher than they are today. Although these attempts have so far been unsuccessful, legal action to remedy this is lengthy, and producers suffer from reduced or no payment during the process. The MNRE is trying to remedy common issues, for example by revising the dispute resolution mechanism for disputes between developers, contractors and renewable energy-implementing agencies like SECI and NTPC.

Another challenge is managing the economy of coal-dependent states to steady the increasing share of renewable energy of some states. In the past years, renewable energy installations have been concentrated —up to 78 per cent according to MNRE—in only a few states such as Karnataka, Gujarat, Rajasthan, Maharashtra, Tamil Nadu and Andhra Pradesh. On the other hand, certain states like Jharkhand, Chhattisgarh, Odisha, Telangana and West Bengal rely heavily on coal for their economic development. For the moment, India’s focus has been to increase production on all fronts to ensure its energy security, but in the long run, it expects to gain significantly from its policy push supporting the domestic production of green hydrogen and other alternative fuels.

Energy transition also suffers from other challenges that are common to all infrastructure project development in India. Land acquisition for large-scale renewable projects is cost-intensive with limited government support. Even after being legally acquired, possession of land remains a challenge, and project companies have been dragged into legal battles over ownership. Finally, there are various permits to be obtained depending on the location of the site, including environment, wildlife, ceiling limits, government land allotment, ancestral property state laws, and so on. As all processes for permits and approvals are not effectively streamlined in states, these can take a lot of time to be obtained depending on the location.

Looking ahead

The government’s efforts to promote energy transition have seen strong support from India’s private sector.

The Reliance Group recently increased its energy transition commitments and is aiming to install at least 100 GWs of renewable energy-generation capacity by 2030, with projects including a fully integrated solar giga factory in Jamnagar. With a population in excess of 1.4 billion to manage, India’s demand for energy to run a growing economy is only expected to increase. At the same time, it has significant international commitments to uphold as far as its energy transition is concerned.

The government sees a solution in racing ahead with shifting India’s energy landscape. That effort, however, will be admittedly inadequate without significant investments from the private sector, both domestic and international. In the coming years, one should expect to see sustained policy, regulatory and operational efforts by the government in powering India’s effort to transition away from fossil fuels.

The author would like to thank Ramya Hari and Mallika Singh for their contributions to the article.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

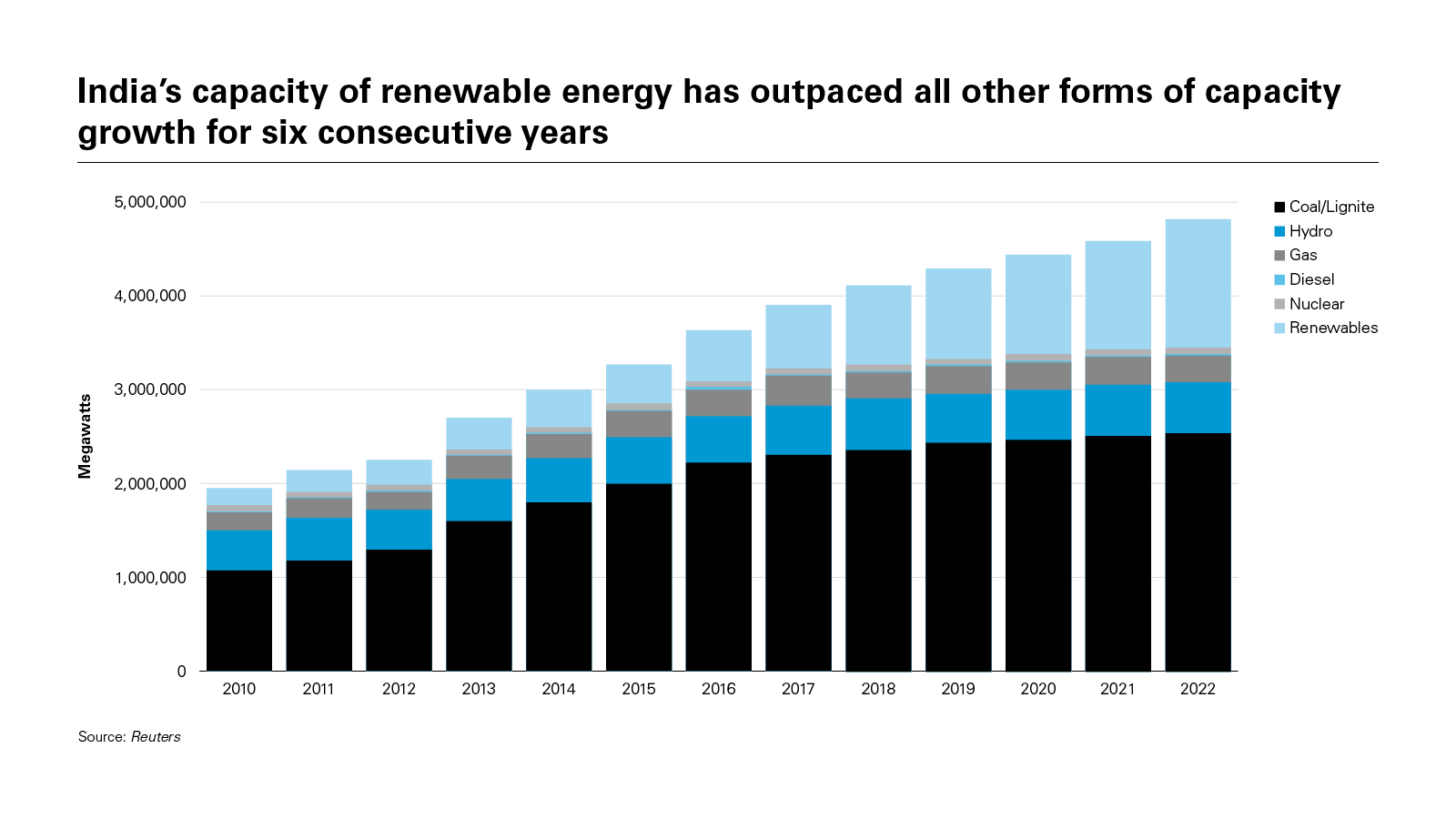

View full image: India’s capacity of renewable energy has outpaced all other forms of capacity growth for six consecutive years

View full image: India’s capacity of renewable energy has outpaced all other forms of capacity growth for six consecutive years

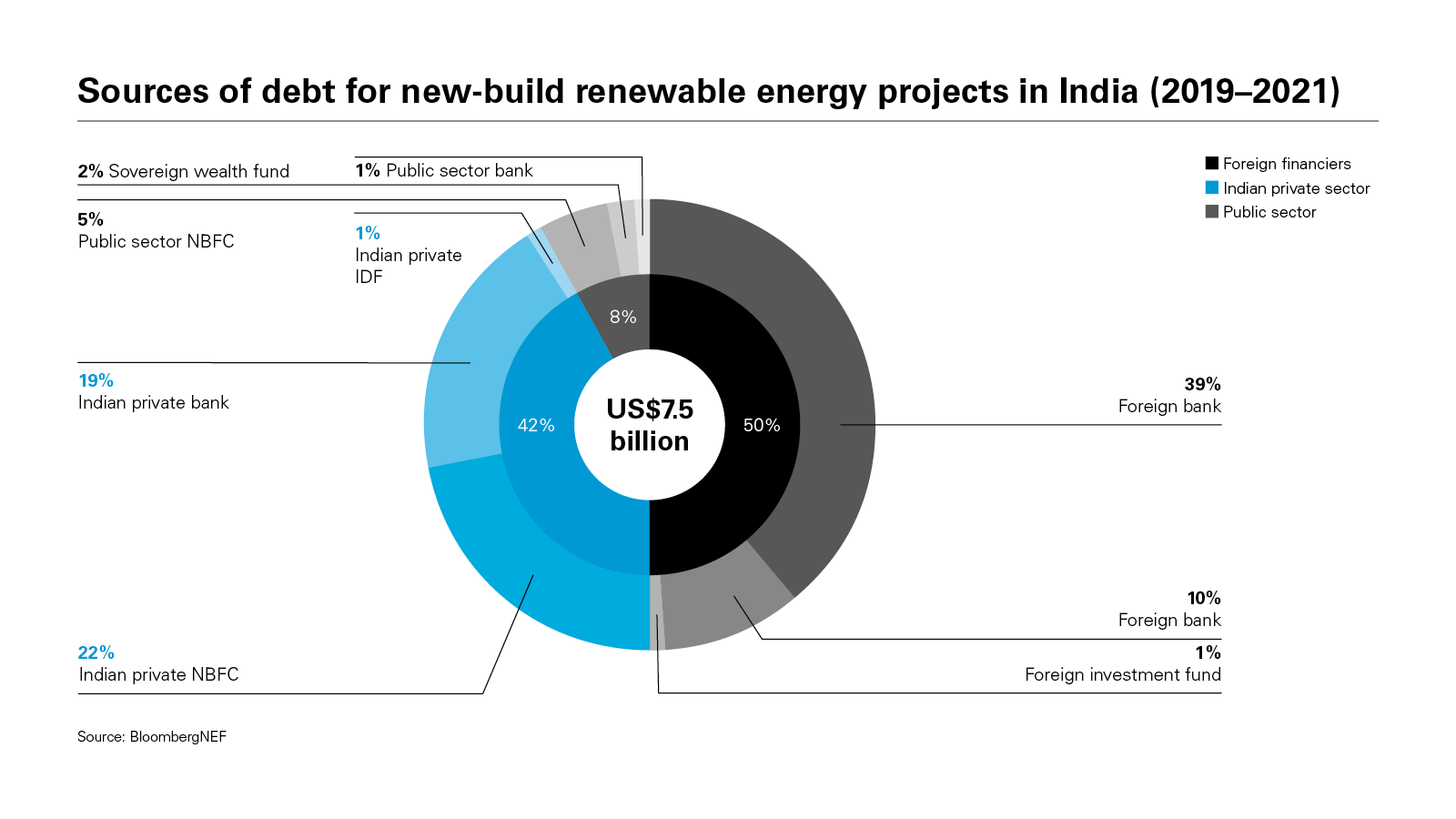

View full image: Sources of debt for new-build renewable energy projects in India (2019–2021) (PDF)

View full image: Sources of debt for new-build renewable energy projects in India (2019–2021) (PDF)

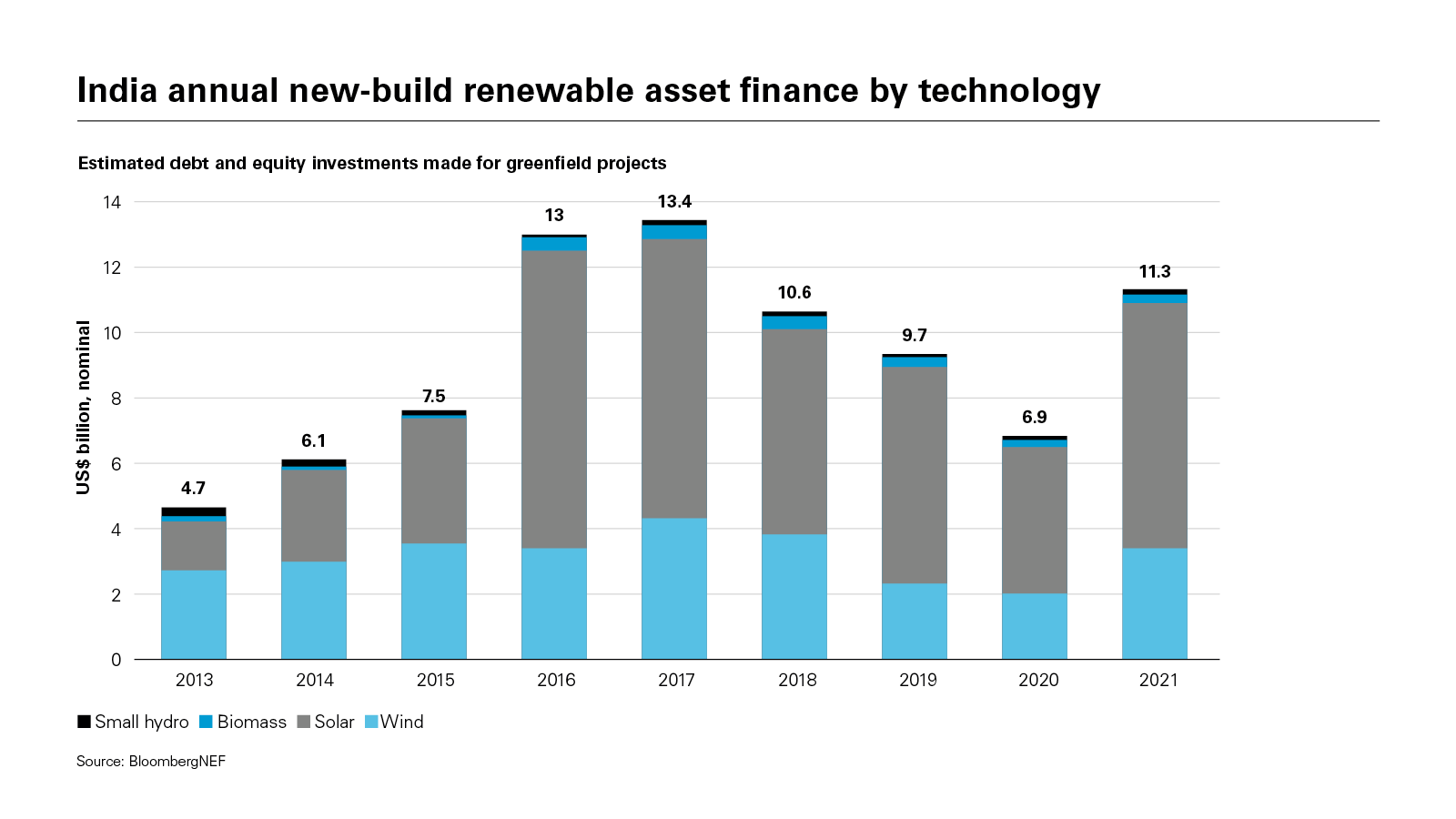

View full image: India annual new-build renewable asset finance by technology (PDF)

View full image: India annual new-build renewable asset finance by technology (PDF)