Mining & metals 2026: Adapting to a policy-driven business cycle

2025 put mining & metals at the heart of geopolitical competition. In 2026, the sector faces a decision: Be a pawn or a player in a business cycle and environment structurally driven by a geopolitical race for mineral security and national power.

12 min read

In 2025, geopolitics drove events and investment in the mining & metals sector. The unprecedented degree of uncertainty, led by rapidly changing policies in the US and China, shifted markets into a deal cycle driven by politics instead of prices and supply/demand expectations. Trade flows and prices were similarly affected by pressure to stockpile as much supply as possible in the United States through the summer. The next 12 months promise a consolidation of the sector's ongoing politicization, providing opportunities and risks for miners and investors increasingly reliant on access to policy support across metals markets that are generally well supplied or over-supplied. 47 percent of respondents believe that political variables—mitigating geopolitical risks, securing policy support, or access to critical minerals—are the main priority for 2026.

In 2025, gold prices climbed about 65% and silver soared roughly 144%, marking their biggest annual gains in over four decades.

Source: BullionVault

Though the global economy dodged more extreme policy shocks in 2025, the IMF forecasts a slight moderation in global GDP growth to 3.1 percent for 2026, led by a pronounced slowdown in the US and China's deflationary headwinds. Continued strong cleantech uptake and pressure to electrify economies have not offset weakness from more traditional sources of demand, such as construction, first led by the ongoing recession in China's real estate sector and now common across developed markets faced with higher costs of capital. Aside from copper, whose price performance was primarily driven by US tariff risks and supply-side factors in 2025, base and ferrous metals prices remain subdued. In contrast, gold and silver have seen searing price growth, as banks, asset and wealth managers allocate more capital to precious metals in financial portfolios for returns and as a longer-term hedge against bond market volatility.

The tension between market conditions and confidence in potential upside for investors is striking. Half of respondents believe high prices and returns are key to attract and keep institutional capital in the mining sector, both of which are highly exposed to policy, China's domestic economic performance and generally well- supplied metals markets. Despite these conditions, 77 percent of respondents would recommend someone to invest in it. Gold, silver and copper were star price performers, but proliferating state interventions into markets are creating new avenues to realize returns, most visibly for rare earth elements (REEs), and shifting company strategies.

Factors that ostensibly limit the potential for M&A activity—volatile national policies, resource nationalism and the cost of capital—are also potential deal drivers. The ongoing attempted merger between Anglo American and Teck Resources is the highest-profile strategic partnership to emerge in the past several years, matching the 32 percent of respondents who believe M&A activity in 2026 will be likely to reflect these types of partnerships. Despite persistent market interest, however, relatively few such "mega" mergers have occurred. With the political focus on rare earths, battery metals and niche markets, where relatively small volumes of capital can meaningfully de-risk supply chains, junior and intermediate miners may disproportionately benefit, since many relevant projects are too small to drive majors' revenues.

In the year ahead, strategic partnerships between governments, government agencies and the private sector are likely to be the backbone of growth M&A in the sector. Should cost of capital pose a constraint, even as interest rates are expected to fall, miners can target assets eligible for policy support, such as preferential, state-backed lending or even the sale of equity to national governments as an implicit guarantee of a bailout or commensurate support. As one respondent noted, "growth in mining & metals will increasingly be shaped by governance rather than geology."

Neither bear nor bull market

The continued gap between the pace at which Chinese miners and the rest bring new mines to market, undershooting demand expectations, and shift to a policy-driven deal cycle have shifted the investment landscape. Majors continue to focus on capital discipline, eyeing opportunities to acquire prospective copper or critical minerals assets. By contrast, the expansion of policy support has unleashed a wave of interest into new projects among more risk-tolerant miners and investors seeking opportunities to deploy capital for various metals markets, whose price and supply dynamics are increasingly idiosyncratic.

Unsurprisingly, two-thirds of respondents expect copper and gold to be the big winners in 2026 following strong price growth over the previous year, with both commodities significantly outperforming US and European equity indices. Copper cracked US$12,000 a ton in December following output reductions, led by the loss of hundreds of thousands of tons from the Escondida, Collahuasi and Grasberg mines. Gold enjoyed a bumper year from consistently stronger central bank demand and the ongoing addition of gold to financial portfolios.

Elsewhere, the picture is more mixed. Lithium prices remain low, buoyed by voluntary reductions from lepidolite mines in China, pressure from Chinese policymakers to pare back ongoing price wars in the cleantech manufacturing sector and significant increase in battery storage demand. Cobalt enjoyed a significant boost from an eight-month export ban in the DRC that has since transitioned to a new quota system. However, EV manufacturers' shifting preference for lithium-iron-phosphate (LFP) chemistry batteries continues to eat away at future demand expectations. Nickel prices rose past US$16,000 a ton in December, thanks to the Indonesian government's active management of supply. China's export controls on battery metals have had a limited impact thus far on overall price levels.

In November 2025, Chinese steel enterprises recorded their lowest steel output since December 2023, with production down 10.9% year-on-year.

Source: National Bureau of Statistics of China

Steel markets continue to suffer from the weakness of real estate demand in China, while aluminum markets shifted into deficits with considerable future uncertainty about potential sanctions relief for Russian exporters and US tariff levels. Rare earths, particularly those used for permanent magnets, saw spot prices climb on export controls. The US Department of War's decision to take an equity position in MP Materials and offer a guaranteed ten-year offtake at roughly twice the spot price levels in China, an approach that has expanded since August, has fundamentally changed investor expectations. Rare earths enjoy a political bull market regardless of actual supply/demand dynamics.

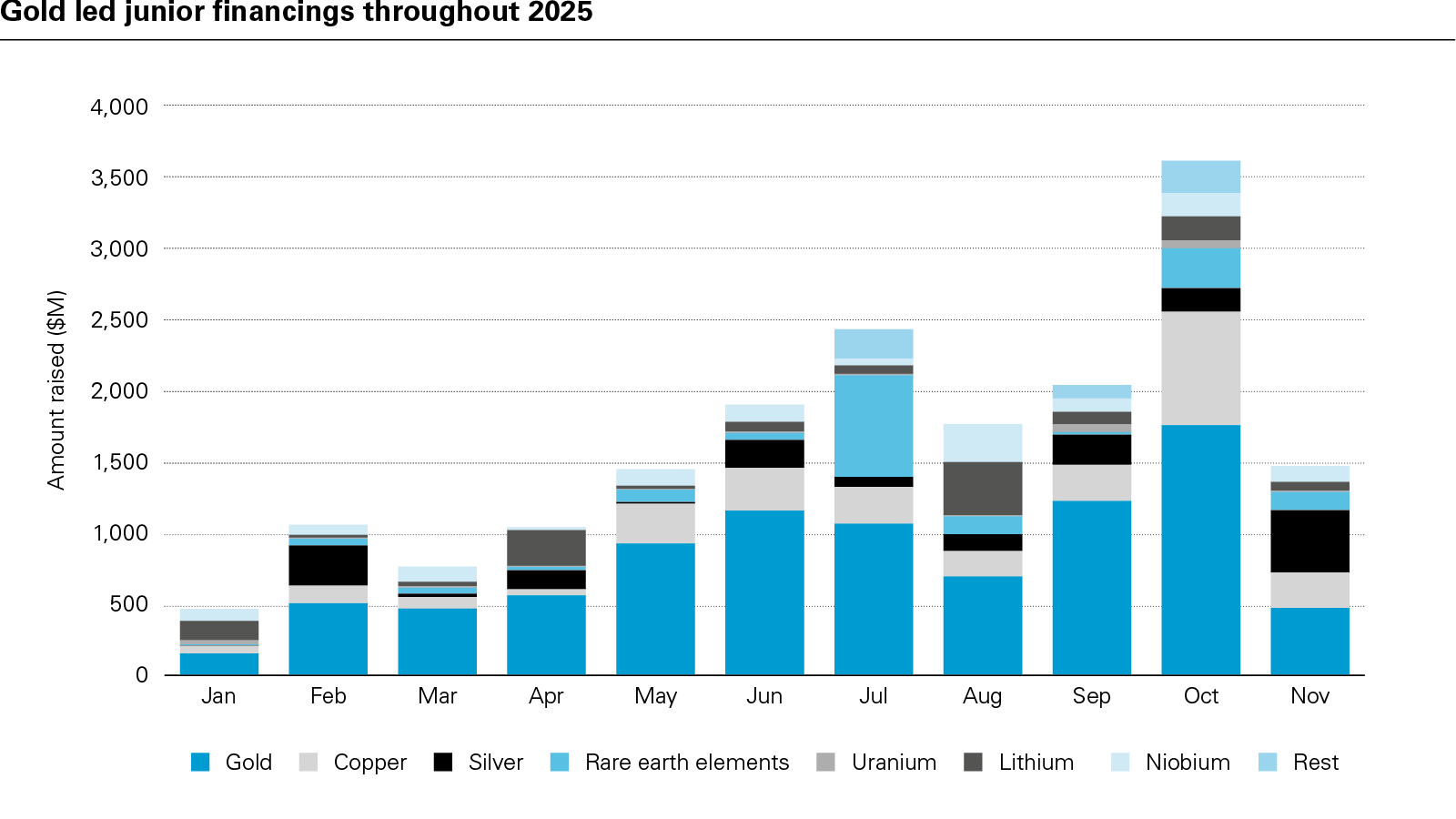

The broadly weak price environment points to consolidation for base metals, expected by 24 percent of our respondents. But miners are prioritizing copper, evidenced by the ongoing Anglo Teck merger. Another 29 percent of respondents expect that gold and precious metals are likeliest to experience consolidation. Instead of low prices and better value for money driving the merger cycle, 2026 may instead see a race for sure bets, inflating copper and gold asset values. Even as investors seek opportunities in critical minerals, junior and intermediate gold miners continue to raise more financing than any other metal, including copper.

View full image: Gold led junior financings throughout 2025 (PDF)

View full image: Gold led junior financings throughout 2025 (PDF)

Supply chain diversification "comes of age"

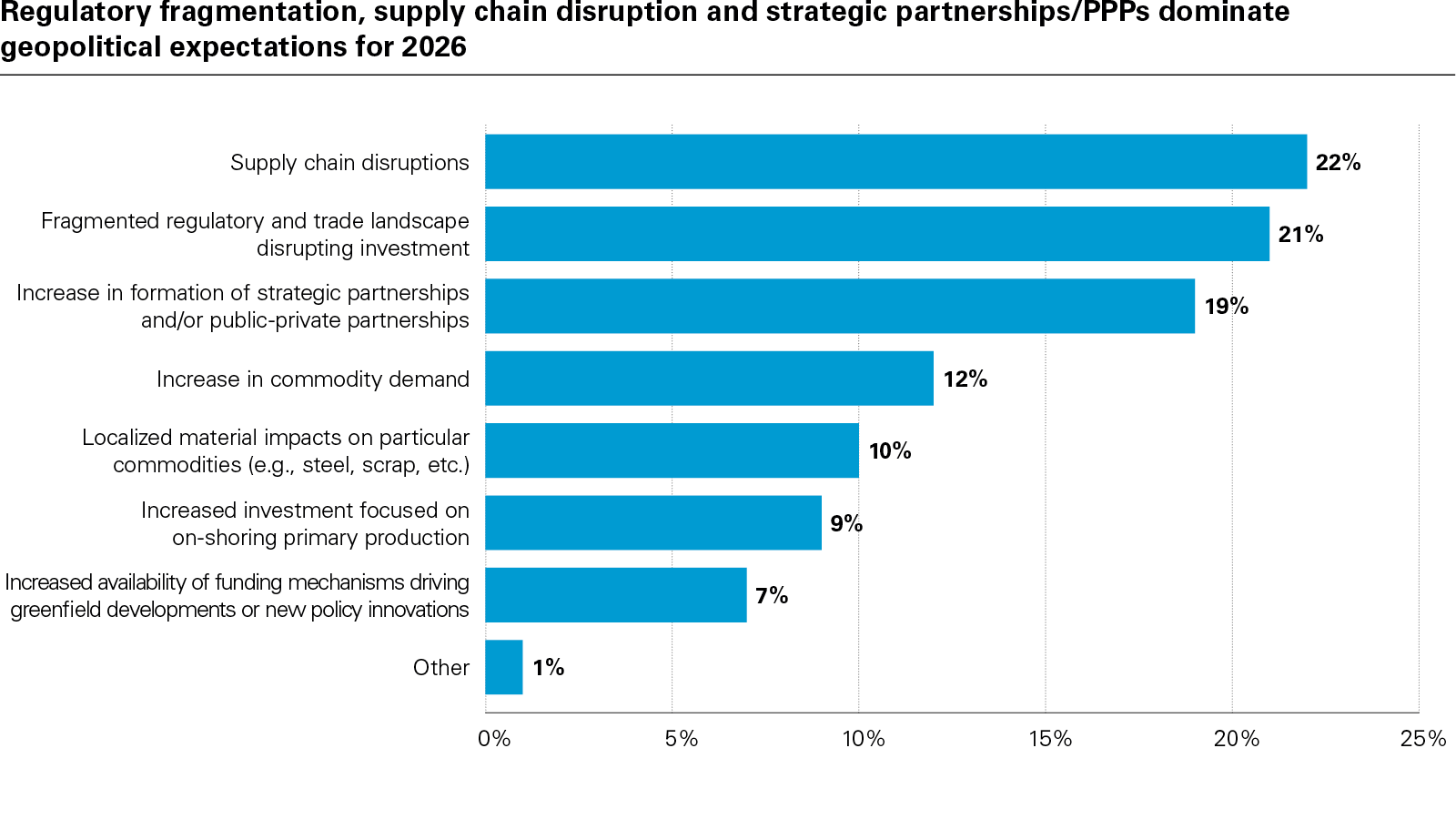

The unprecedented degree of policy support for new mining projects—and volatility of trade policy—reflects the geopolitical urgency of securing critical minerals supplies. This race to build or source minerals and metals from outside of China and without the involvement of Chinese sponsors has begun to create pricing premiums for rare earth elements. North American and European automotive and defense OEMs panicked last spring and summer over China's export controls and their limited stockpiles. Just-in-time supply chain management has become a material business risk. While REEs are an exceptional case, markets are structurally shifting from the pursuit of green or analogous premiums for security premiums, even as the EU doubles down on CBAM.

As supply chain diversification has matured, so have sector views of geopolitical risk. Disruptions to investment from the fragmentation of national policies remained the biggest risk in this year's survey, but a greater share of responses point to increased activity or potential upsides following a year of trade shocks. Chinese sponsors continue to expand supply faster at lower price points, but the scale of policy interventions and willingness to absorb higher prices can bolster project economics increasingly eligible for support. 39 percent of respondents expect state-backed financing will be the most common policy prescription from developed markets in the next 12 months.

View full image: Regulatory fragmentation, supply chain disruption and strategic partnerships/PPPs dominate geopolitical expectations for 2026 (PDF)

View full image: Regulatory fragmentation, supply chain disruption and strategic partnerships/PPPs dominate geopolitical expectations for 2026 (PDF)

Critical minerals projects are eligible for the up US$100 billion in lending the Trump administration has authorized through the US Ex-Im Bank for energy dominance. The EU's far less ambitious REsourceEU Action Plan commits €3 billion in funding, joined by €2 billion from the EIB and EBRD. Capital moving through policy lenders will create opportunities for western offtakers to pursue greater levels of vertical integration across their value chains with a lower level of risk and, in the case of more aggressive state interventions such as the US, with implicit state guarantees.

Markets, not policy, driving critical minerals demand

Planning for disruption is now embedded in corporate investment and procurement strategies. The race for security of supply is a double-edged sword for miners and investors. Policy support will lead to an over-expansion of supply, creating further volatility unless states more proactively become offtakers of last resort. One respondent believed "this mining sector 'gold rush' will run for two to three years before ending in a downturn." The more policy-driven the deal cycle is, the greater potential for shorter-term investment bubbles. Overall, smoothing out the traditional boom-bust cycle for key metals can stabilize prices and investment over time as policy frameworks evolve.

By contrast, demand-side drivers for critical minerals are increasingly market- rather than policy-driven. While US and European OEMs have pared back capex into EV and battery manufacturing, global EV sales growth reached 21 percent in 2025 . EU tariffs on auto imports from China targeted battery electric vehicles, leaving Chinese manufacturers an opening to significantly increase their European market share selling plug-in electrics. European sales growth reached 36 percent for the year.

In the first quarter of 2026, it is likely that emerging markets, excluding China, will account for more EV sales than the US, driven by lower costs and convenience. A growing number of companies are considering partnerships with Chinese firms to remain competitive, with some national governments, such as Türkiye, prioritizing tech transfer to establish competence in a national "EV champion" manufacturer.

Similar dynamics apply to solar PVs and batteries, both of which have seen large surges of uptake in frontier and emerging markets to partially offset policy-induced slowdowns within China. Data centers and AI will have a material impact for REE demand linked to semiconductors. But these use cases will be marginal for copper demand and other bulk commodities.

As cleantech, electrification and adjacent investments take on a greater share of demand, comparative costs of capital will increasingly determine marginal demand growth. Even as uncertainty lingers over the rate paths of the Federal Reserve, Bank of England and European Central Bank for the next 12 months, emerging markets have seen inflation normalize more rapidly than their developed market peers. Capex-intensive sectors, such as construction and cleantech, stand to benefit.

Navigating a polarized world – processing capacity is the key

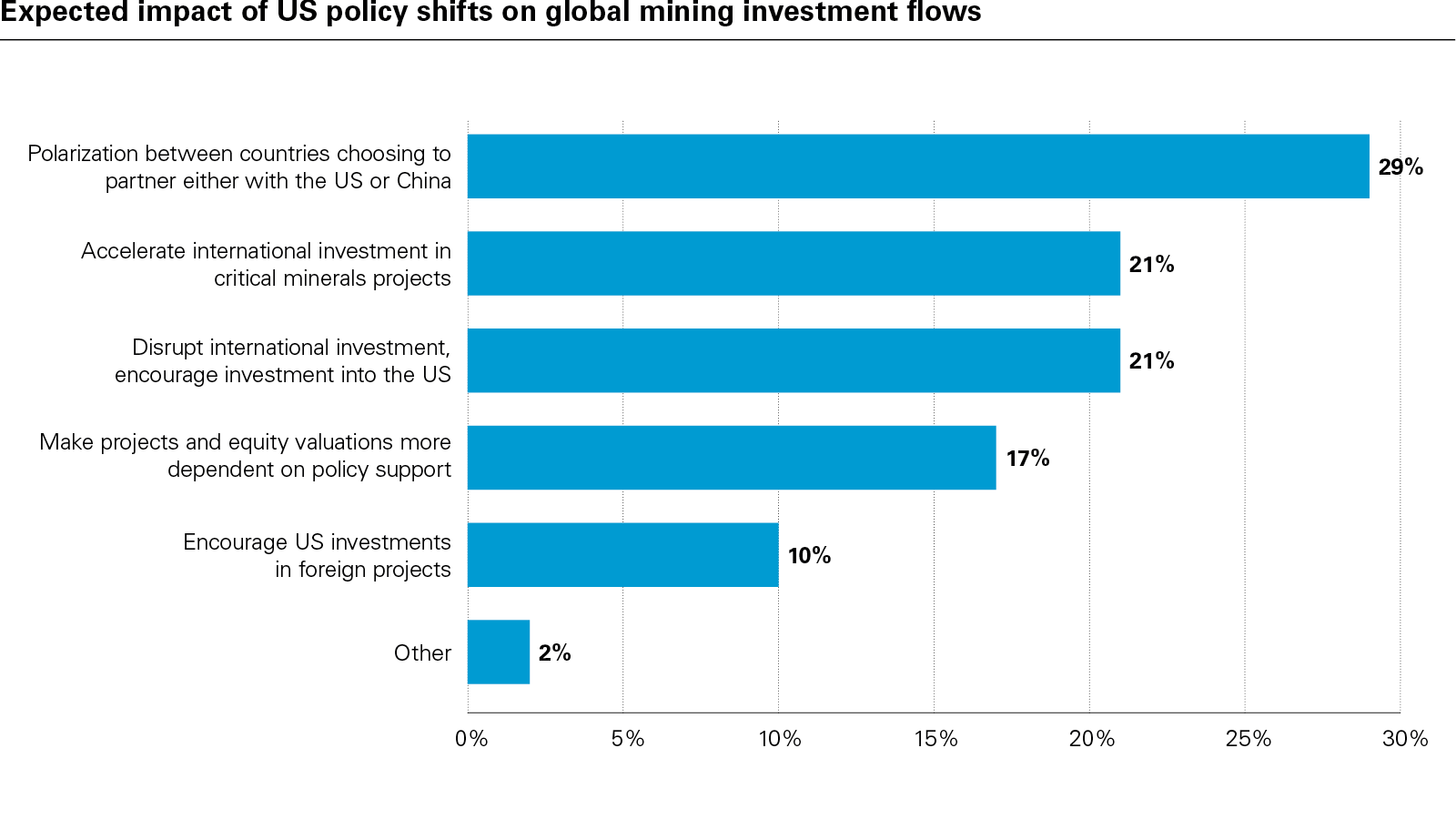

US-China tensions and the Trump administration's broader reorientation of US trade and foreign policy are contributing to geopolitical divergence. China's relative dominance in metals processing and refining capacity will continue to drive national policies focused on resource security. Projects' dependence on policy support or conditions will likely strengthen in the next 12 months. But there remains considerable uncertainty over investment flows. 73 percent of respondents expect a greater divergence between the US and China on trade and critical minerals policy over the next 12 months, but are far more divided on whether these dynamics will support investment into the US, into international projects, or otherwise into projects with Chinese participation.

View full image: Expected impact of US policy shifts on global mining investment flows (PDF)

View full image: Expected impact of US policy shifts on global mining investment flows (PDF)

Political reality and resource wealth constrain what remains viable. The US, Australia, Canada and Chile have advanced permitting reform or deregulation to accelerate critical minerals project development. But 46 percent of respondents cite red tape and administrative inaction as the EU's greatest barrier to critical mineral security, followed by 31 percent citing geographical access to resources. This gap heightens pressure on European firms to consider partnership with Chinese sponsors. Should US policy seek to punish these partnerships, investors will be under greater pressure to prioritize US projects, bidding up US assets. Conversely, Chinese sponsors can typically deliver projects at the lowest price point, inverting that calculus for emerging and frontier markets seeking to onshore more value-added production and build cleantech infrastructure.

The EU is also indicative of a broader challenge for policymakers setting ambitious targets within these constraints. Mines are vital for new supply, but the capacity to process and refine—China's chief competitive advantage—drives the ability to finance new mines through offtake arrangements, or otherwise more flexibly source concentrates and unprocessed ores. Australia's national critical minerals stockpile and offer to sell allies "shares" of its reserves present a complementary coordinating mechanism to back mid- and downstream investment or offset trade shocks.

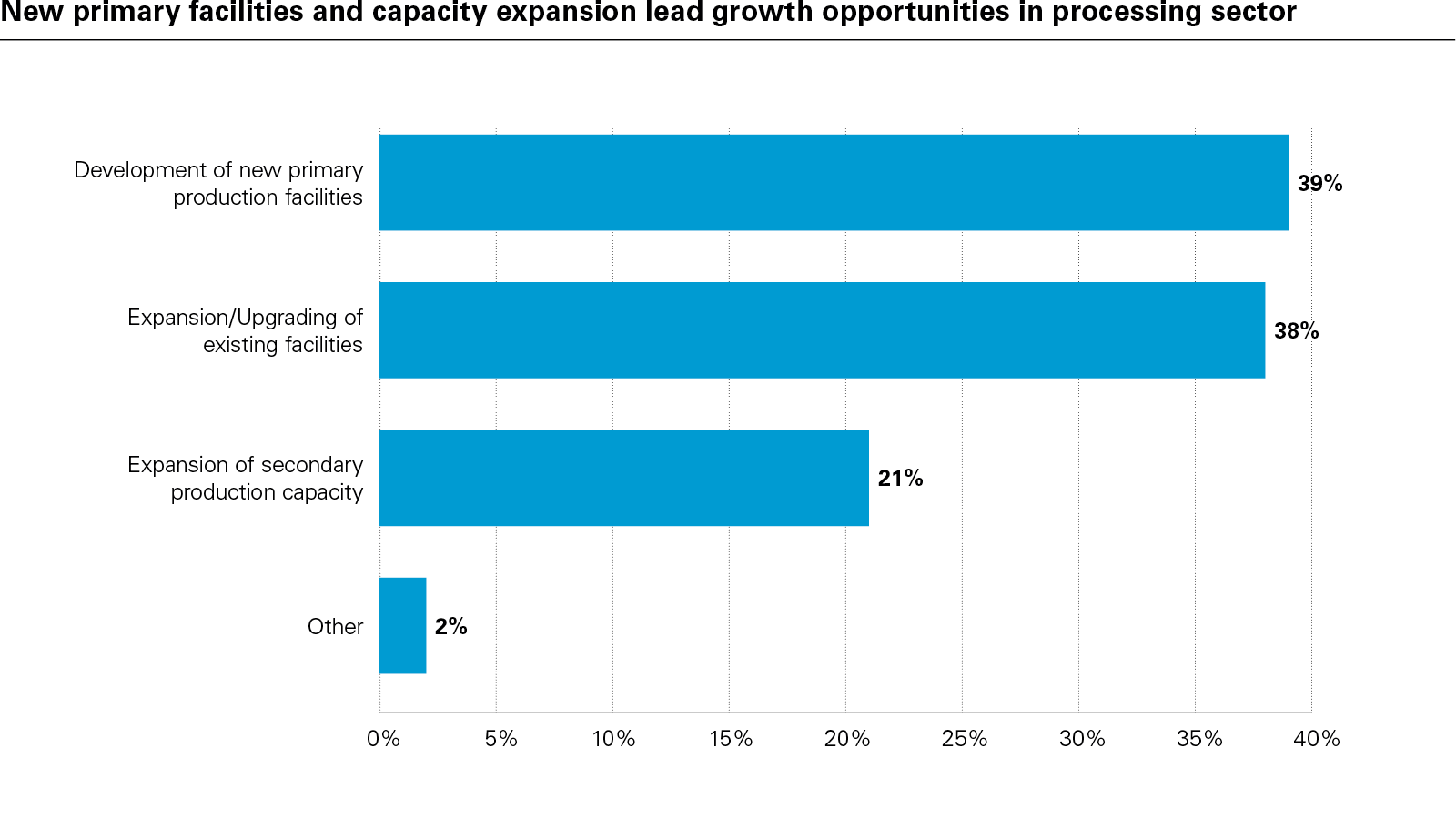

Refining onshore is often difficult in OECD countries despite commitments to diversify. Permitting and regulatory bottlenecks often make brownfield expansions of existing assets or acquiring them more attractive than greenfield investment. 41 percent of respondents highlighted the shortcomings of OECD policies faced with these bottlenecks. The preference for recycling and circularity, particularly in Europe, is secondary to expanding primary production. and existing policy interventions raise consumer costs without closing supply gaps effectively. But policies promoting circularity and new primary supply extra-territorially are often durable in developed markets because they offload environmental and operational risks to others.

View full image: New primary facilities and capacity expansion lead growth opportunities in processing sector (PDF)

View full image: New primary facilities and capacity expansion lead growth opportunities in processing sector (PDF)

The world of policy-driven asset values, trade flows, access to capital and partnerships is maturing. Political volatility can impede investment, but also creates a proliferating number of pathways for financing and project competitiveness. Wherever companies operate, social license to operate remains the bedrock of sector investment. Despite ESG's fall from favor in the financial sector, more than three-quarters of our respondents expect the industry will maintain or increase current adoption rates of relevant frameworks. As long as primary mined supply expansions are predominantly driven by non-OECD markets, these frameworks are essential to mitigate financial risk.

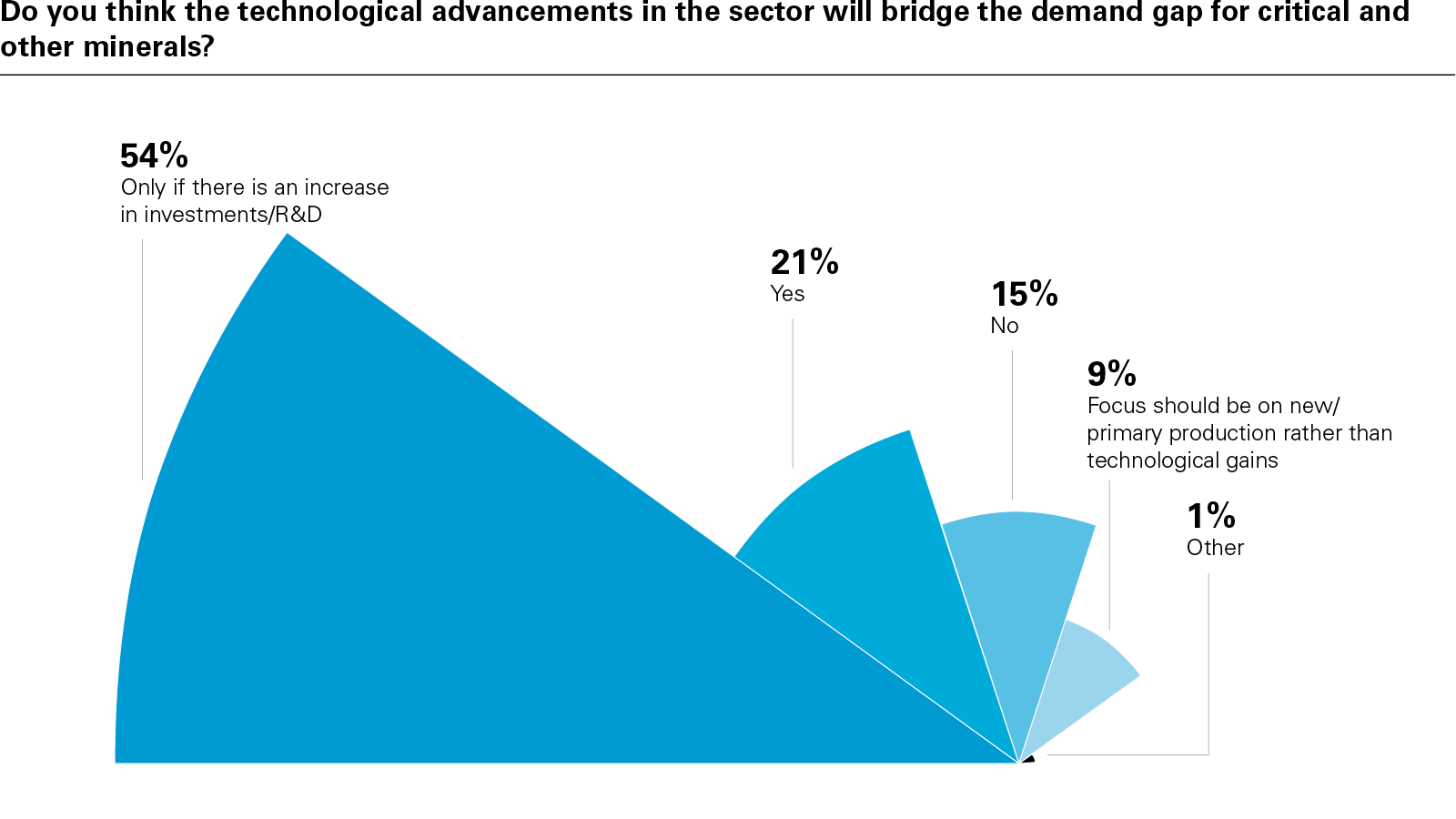

View full image: Do you think the technological advancements in the sector will bridge the demand gap for critical and other minerals? (PDF)

View full image: Do you think the technological advancements in the sector will bridge the demand gap for critical and other minerals? (PDF)

Mining & metals firms must deliver on local needs and requirements, as the international operating environment grows more complex. With so much uncertainty, companies face considerable pressure to find efficiencies, exploit existing assets, tailings and waste, and reduce costs wherever possible to meet future demand. Yet more than half of our respondents believe only an increase in R&D and investment into technological solutions can meaningfully bridge expected future shortfalls of critical minerals. Supply is increasingly geopolitical and policy-driven. Demand is not. 2026 will stress test miners' and investors' ability to manage US-China risks, while demand continues to evolve irrespective of shifts in American policy.

View full image: Respondents most frequently pointed to geopolitics, capital and investment as the defining forces shaping the sector in 2026, alongside a range of other factors influencing its direction. (PDF)

View full image: Respondents most frequently pointed to geopolitics, capital and investment as the defining forces shaping the sector in 2026, alongside a range of other factors influencing its direction. (PDF)

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2026 White & Case LLP