Real estate 2024: Emerging from the storm?

The real estate sector is looking ahead with more optimism, as interest rates peak and a clearer picture forms on valuation and future financial performance

14 min read

Explore Trendscape

Our take on the interconnected global trends that are shaping the business climate for our clients.

As interest rates peak and a clearer picture forms on valuation and future financial performance, the emerging green shoots signal a readiness among investors to get back to business.

By most measures, 2023 was a year to forget for real estate investors and dealmakers.

To get a read of what will drive and affect sector activity in the year ahead, White & Case has conducted its second annual survey of industry participants, with more than 260 senior decision-makers sharing their thoughts. Our findings show that after a volatile 24 months, the industry is looking ahead with more optimism as interest rates peak and a clearer picture forms on valuation and future financial performance.

Even though the outlook for 2024 is more positive, investors remain cautious. Rates are still high and geopolitical risk continues to loom large. On balance, however, the industry does appear to be in a more stable position than it was 12 months ago. The next year may not break any records for real estate deal activity and fundraising, but green shoots are emerging, and investors are ready to get back to business after a quiet 2023.

Section 1: Market overview and outlook

Cautious optimism: Real estate ready for recovery

Key Findings

- There is growing optimism around the short-term and long-term outlook for the global real estate sector

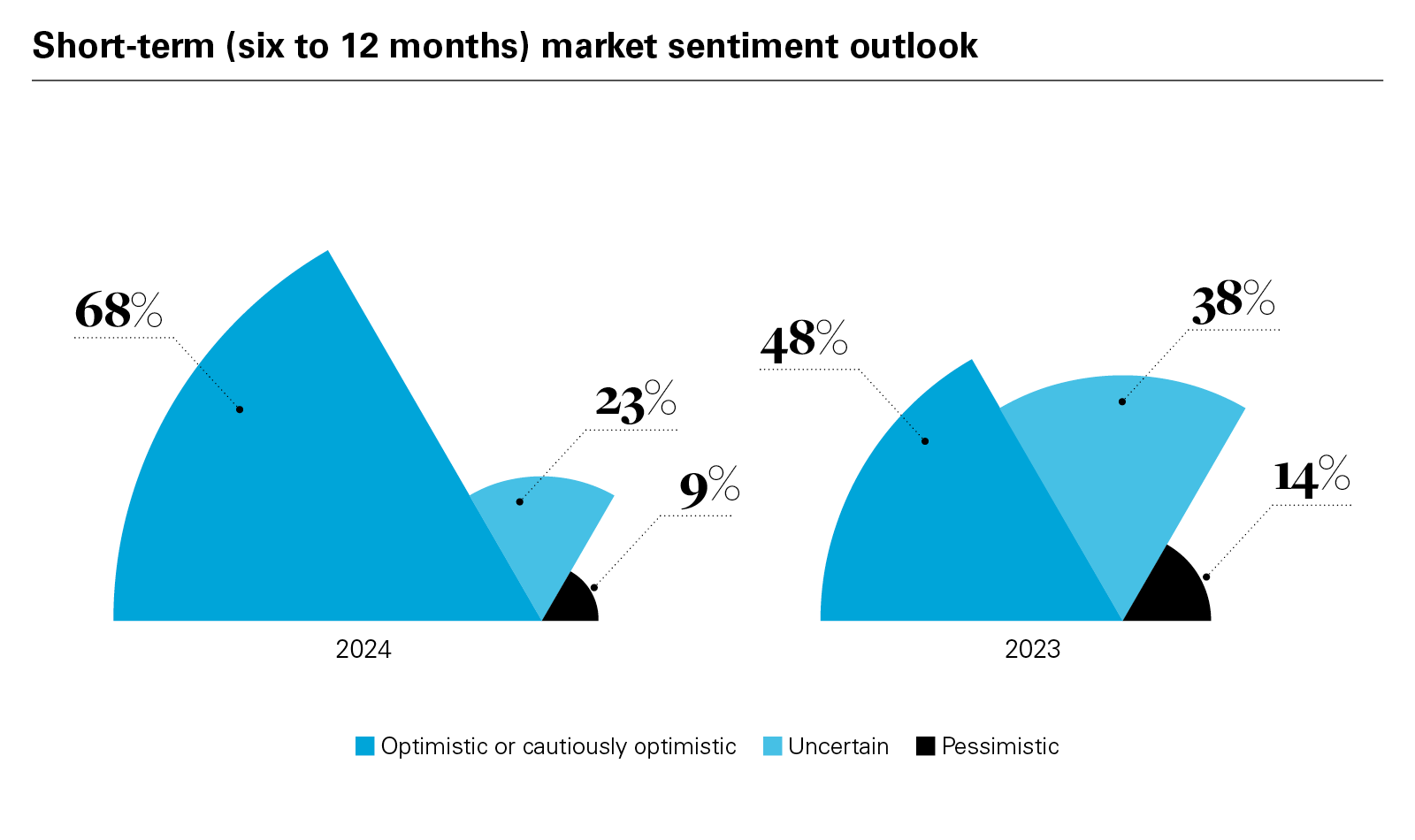

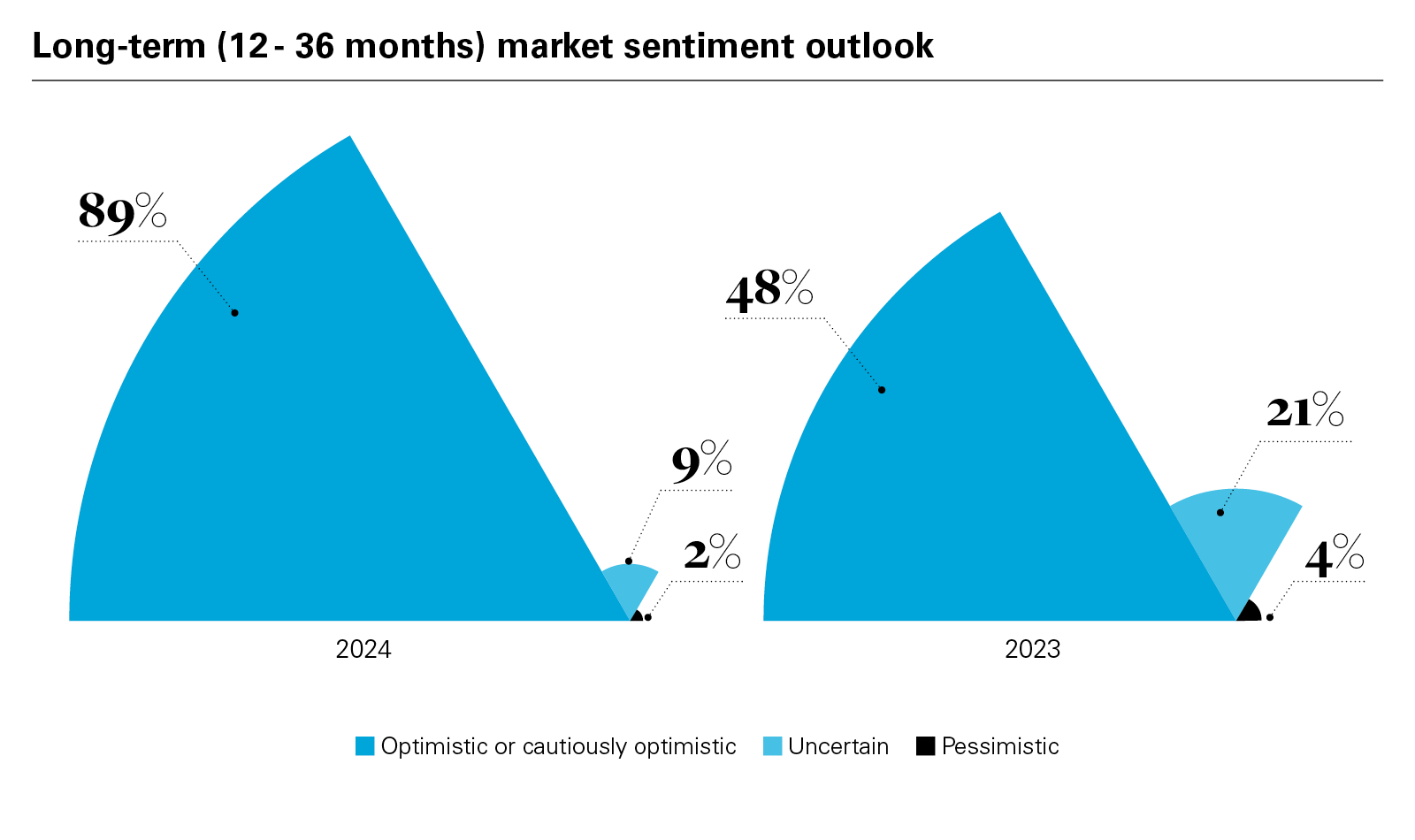

- More than two-thirds (68 percent) of respondents are more optimistic for the short term, with 89 percent optimistic for the long term. In the 2023 survey, only 48 percent and 75 percent were optimistic for the short term and long term respectively

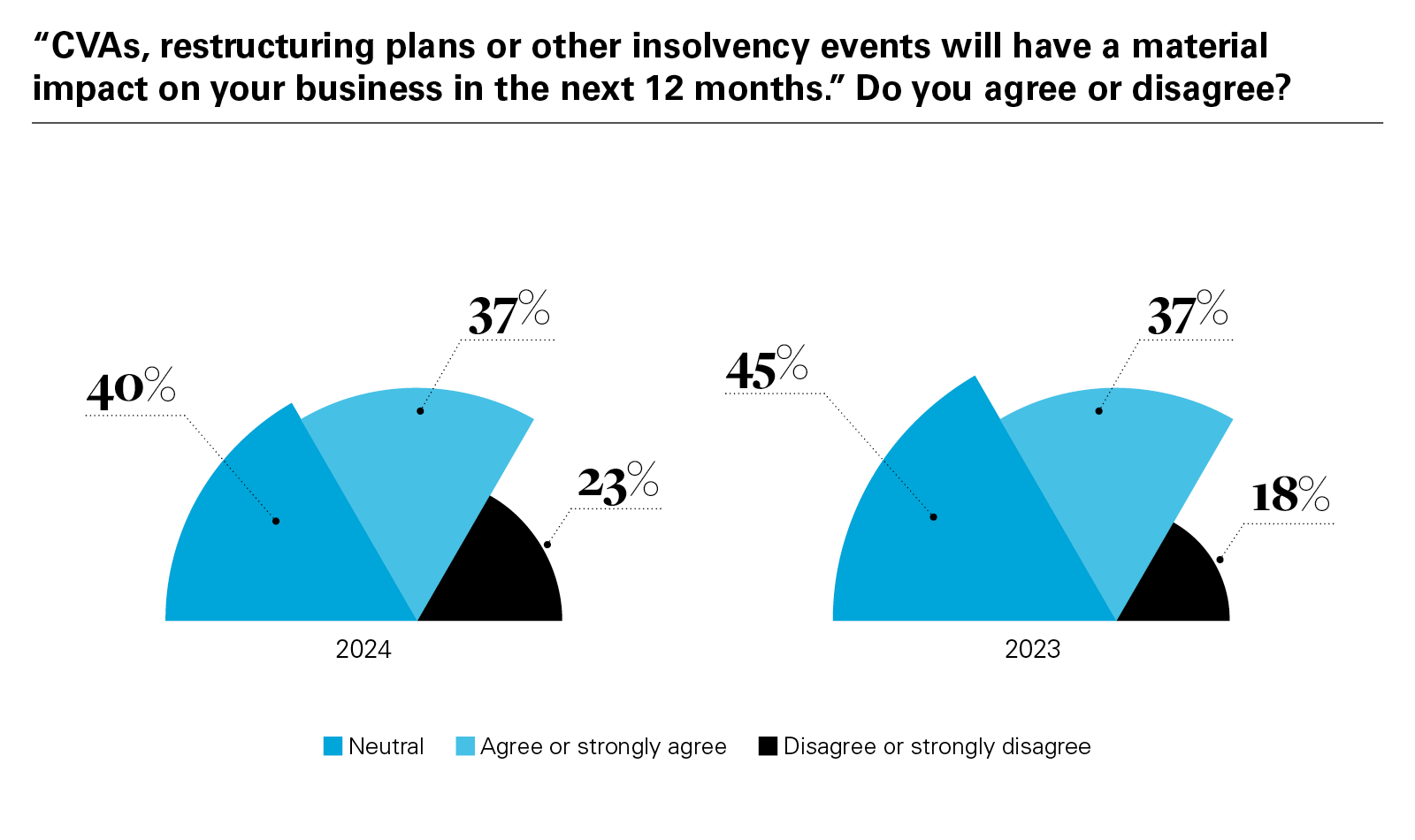

- Although survey respondents are more upbeat than a year ago, they remain cautious, with more than a third (37 percent) anticipating that CVAs, restructuring plans or other insolvency events will have a material impact on businesses during the next year—the same level as 2023

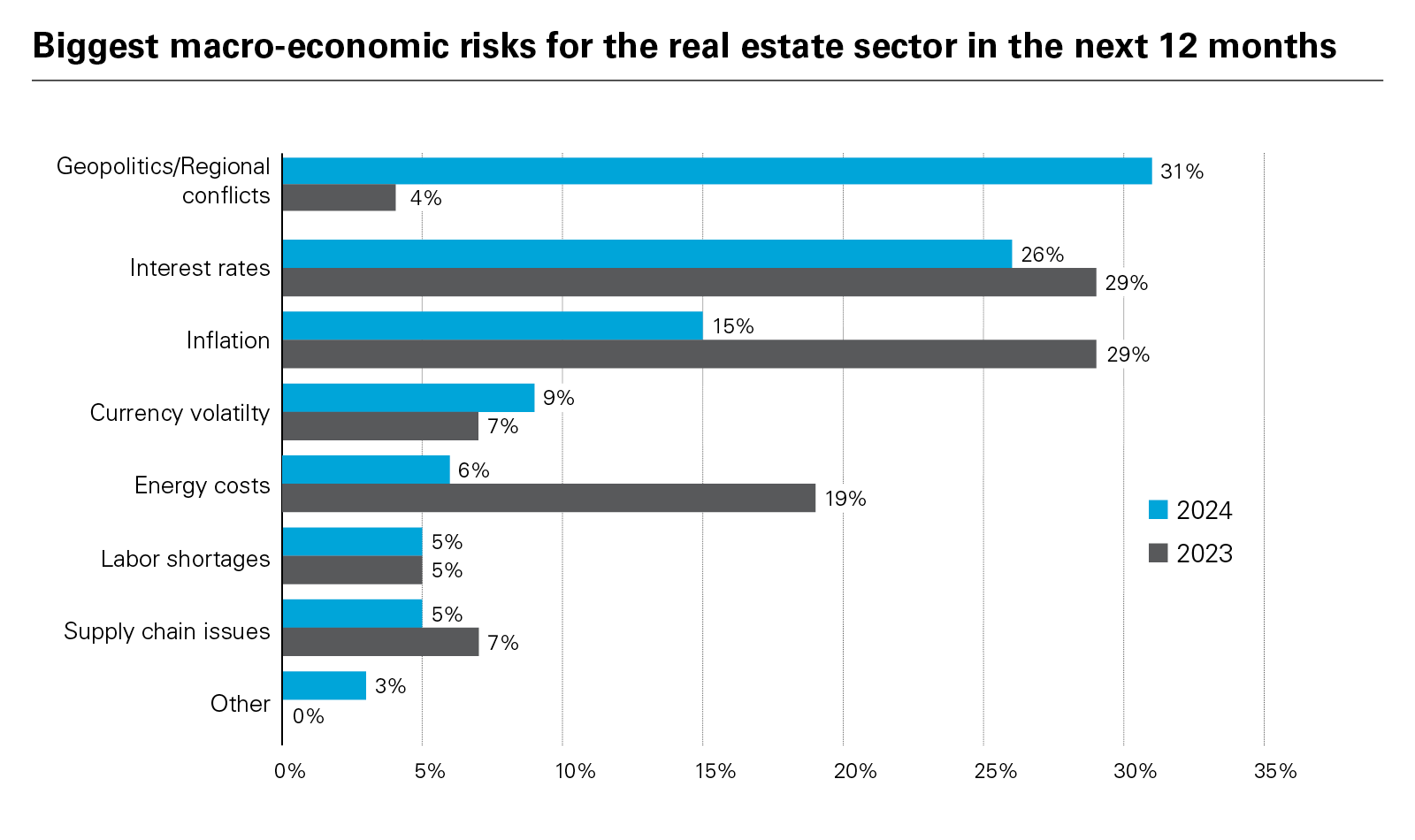

- Geopolitics and regional conflicts are seen as the primary macro-economic risk facing the sector (31 percent), followed by interest rates (26 percent) and inflation (15 percent)

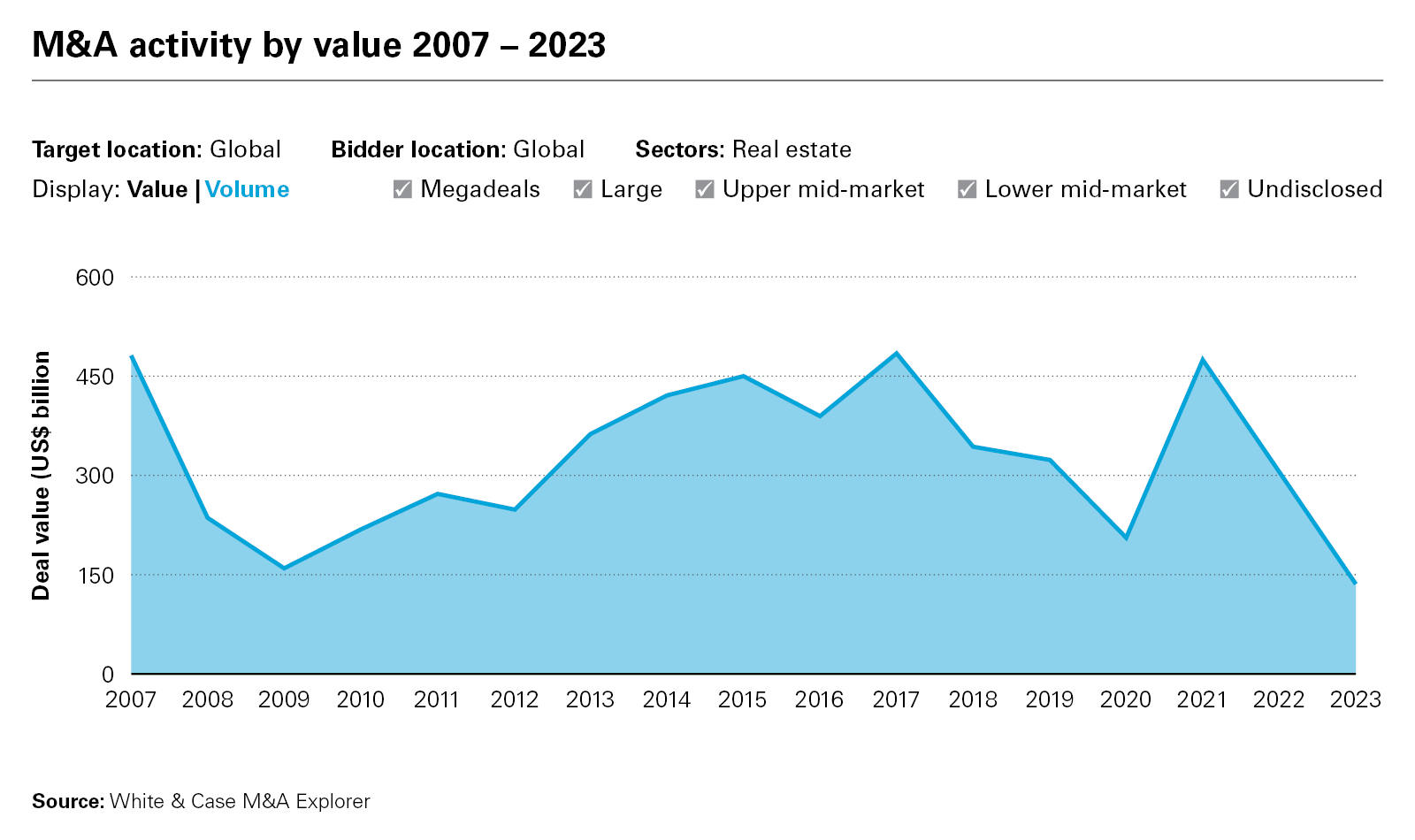

According to White & Case's M&A Explorer, global real estate deal value fell to the lowest levels since 2007, as year-on-year deal value dropped 52 percent from US$293.97 billion in 2022 to US$139.68 billion in 2023. Real estate fundraising activity, meanwhile, fell to the lowest levels seen since 2012, falling from US$224.63 billion in 2022 to US$138.83 billion in 2023, according to PERE.

View full image: M&A activity by value 2007 – 2023 (PDF)

View full image: M&A activity by value 2007 – 2023 (PDF)

The drops in deal value and fundraising reflect the negative impact of high inflation and rising interest rates on real estate markets in the US and Europe, and a liquidity squeeze in the key Chinese real estate sector in Asia-Pacific.

Better days ahead

For all the challenges that real estate markets have faced during the past 12 months, however, this year's survey findings suggest that the market may be starting to turn the corner, with respondents more optimistic about real estate prospects than a year ago.

More than two-thirds (68 percent) of respondents are more optimistic for the short-term, with 89 percent optimistic for the long term. In the 2023 survey, by contrast, only 48 percent and 75 percent were optimistic on the short-term and long-term outlook respectively.

View full image: Short-term (six to 12 months) market sentiment outlook (PDF)

View full image: Short-term (six to 12 months) market sentiment outlook (PDF)

View full image: Long-term (12 - 36 months) market sentiment outlook (PDF)

View full image: Long-term (12 - 36 months) market sentiment outlook (PDF)

A more stable picture for interest rates is driving renewed optimism. There is growing consensus that interest rates in the US, UK and Europe have peaked, and as long as rates stabilize and a lid is kept on inflation, real estate investment activity should start to rebound, with JLL anticipating that stable rates will narrow the gap between buyers and sellers on valuation, facilitating a smoother runway for deals.

"The market is in the process of resetting. If rates go down or stay flat, it will be a positive. If they rise again, it will be a negative," one survey respondent said.

The long-term fundamentals supporting real estate sub-sectors, such as logistics, are also giving real estate professionals.

"The focus on interest rates and inflation has meant that demand has been overlooked," the head of a European real estate developer and manager says. "If you look at logistics real estate, for example, the long-term structural tailwinds of e-commerce, nearshoring and supply chain resilience will continue to support favorable rent and vacancies dynamics, and opportunity to drive income growth."

Proceeding with caution

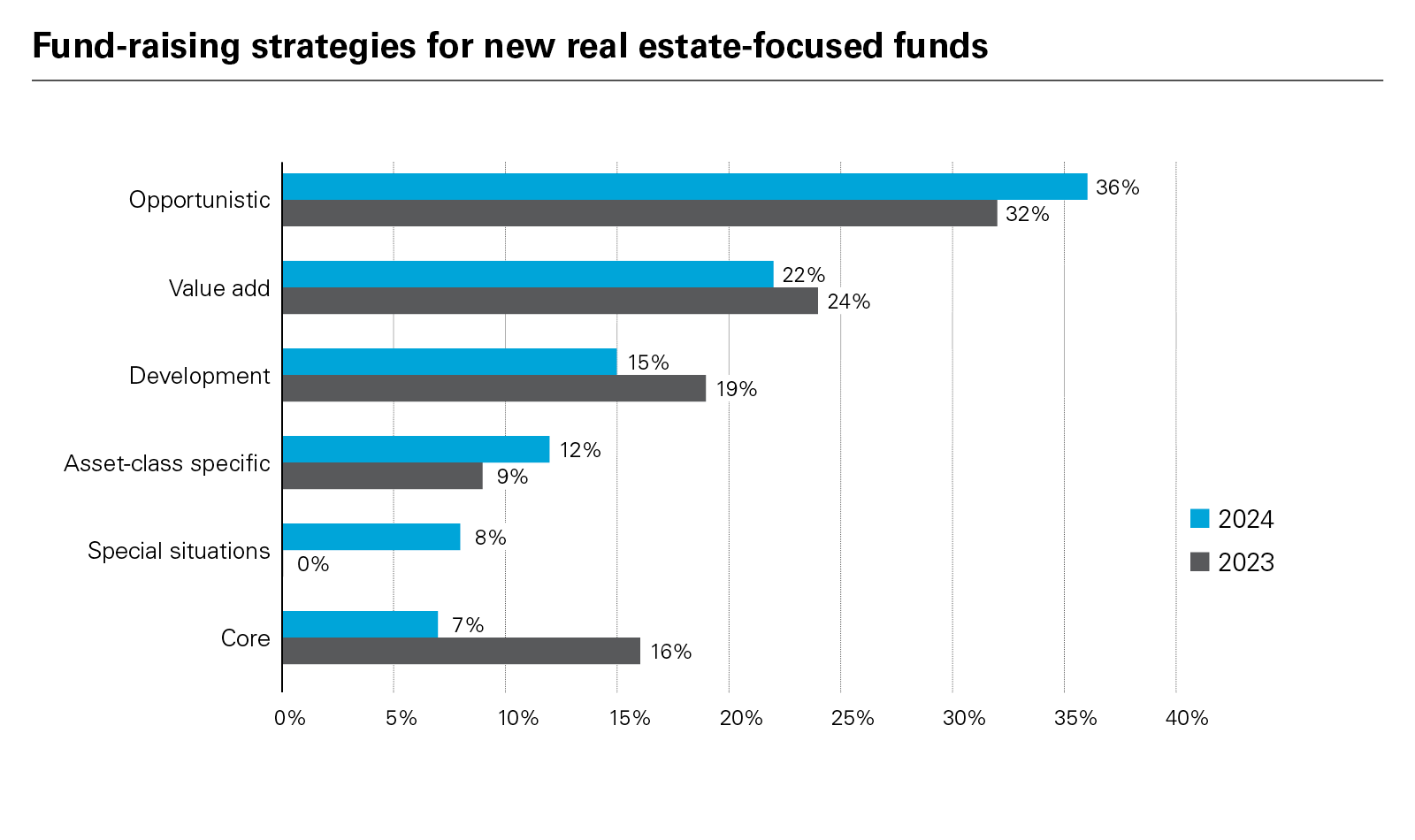

The survey findings also show, however, that respondents are not getting carried away. Opportunistic strategies, for example, rank as the most attractive for fundraising in 2024 (36 percent) with core value-add (22 percent) and development strategies (15 percent) some distance behind.

"Even if interest rates track downwards, real estate will still have to navigate a liquidity mismatch in the years ahead, and that will present opportunity for well-capitalized credit and opportunistic real estate dealmakers," the head of European real estate at a global private markets manager said in a post-survey interview.

More than a third (37 percent) also anticipate that CVAs, restructuring plans or other insolvency events will have a material impact on businesses during the coming year—the same level as 2023.

View full image: “CVAs, restructuring plans or other insolvency events will have a material impact on your business in the next 12 months.” Do you agree or disagree?

View full image: “CVAs, restructuring plans or other insolvency events will have a material impact on your business in the next 12 months.” Do you agree or disagree?

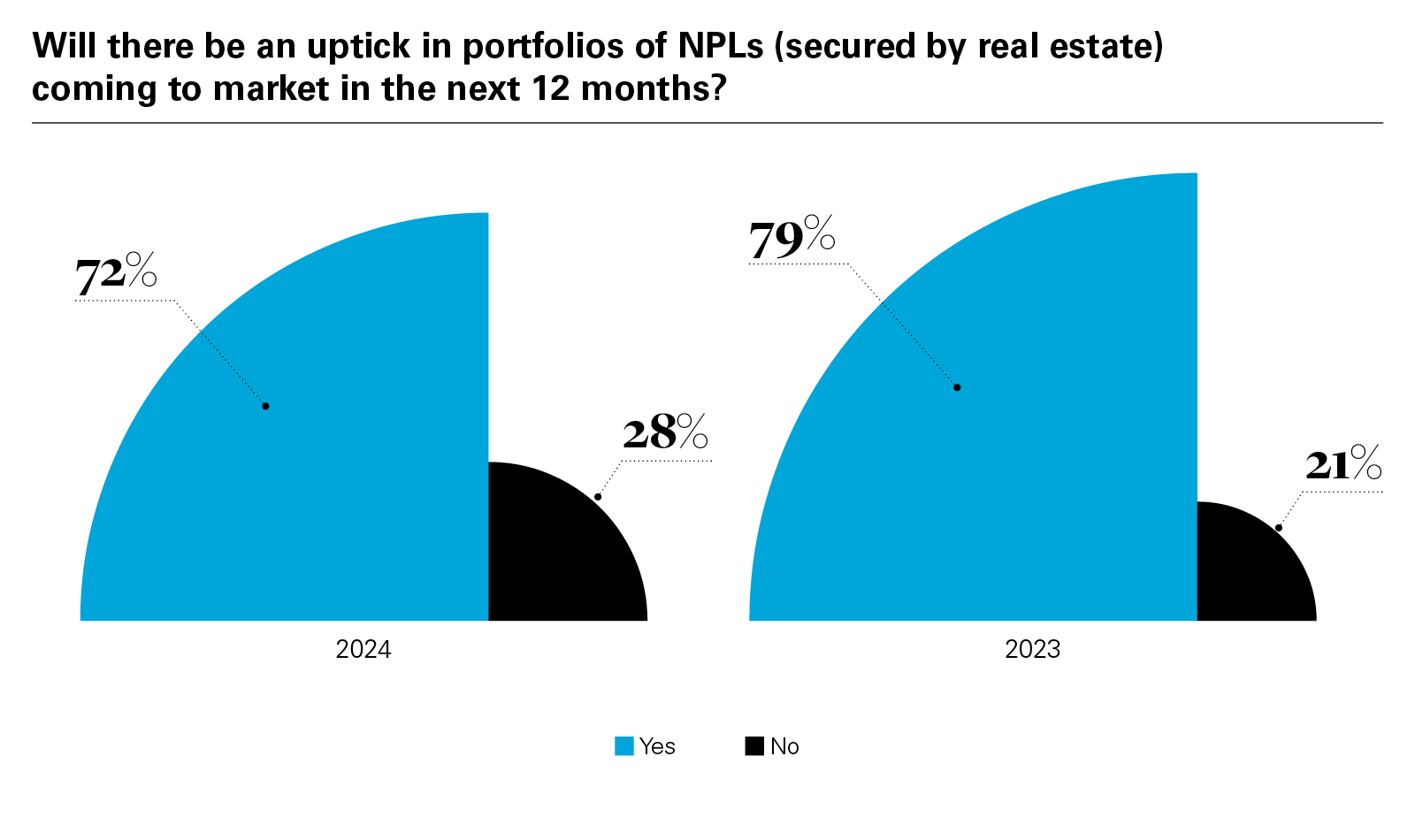

High rates and looming debt maturities are also set to keep pipelines of real estate non-performing loans at elevated levels, with almost three-quarters of respondents (72 percent) expecting an uptick in portfolios of NPLs secured by real estate to come to market in 2024. This is only a little lower than last year (79 percent).

View full image: Will there be an uptick in portfolios of NPLs (secured by real estate) coming to market in the next 12 months? (PDF)

View full image: Will there be an uptick in portfolios of NPLs (secured by real estate) coming to market in the next 12 months? (PDF)

Geopolitical risk is firmly on the radar too, with ongoing conflict in the Ukraine and Middle East, and the risk of proliferation, remaining major concerns. It comes as no surprise, then, that geopolitics and regional conflicts are seen as the primary macro-economic risk now facing the sector (31 percent) —ahead of interest rates (26 percent) and inflation (15 percent), which were identified as the primary macro-economic risks in the 2023 survey.

View full image: Biggest macro-economic risks for the real estate sector in the next 12 months (PDF)

View full image: Biggest macro-economic risks for the real estate sector in the next 12 months (PDF)

With the US, UK and India among the major global economies going to the polls in 2024, political instability ranks as the biggest socio-political risk for real estate (39 percent), some way ahead of political sanctions and changing social habits (both 14 percent).

Some investors, however, do believe that geopolitical risk has been oversold in markets like China, where sell-offs and falling valuations have overlooked underlying commercial drivers that continue to offer investors value.

Overall, the findings indicate that respondents remain sensitive to downside risk and shielding portfolios from macro and geopolitical uncertainty. The good news is that even though the macro backdrop still poses challenges, market conditions have improved when compared to last year.

Section 2: Sectors and fund strategies

Changing dynamics: Opportunity emerges as usage patterns shift

Key Findings

- More than a third of respondents (36 percent) see opportunistic fund strategies as the most attractive going into 2024, with special situations up at 8 percent from 0 percent last year

- Digital infrastructure (17 percent); living/residential (17 percent) and healthcare/life sciences (14 percent) are recognized as the real estate sectors most likely to outperform in 2024—in line with 2023 findings

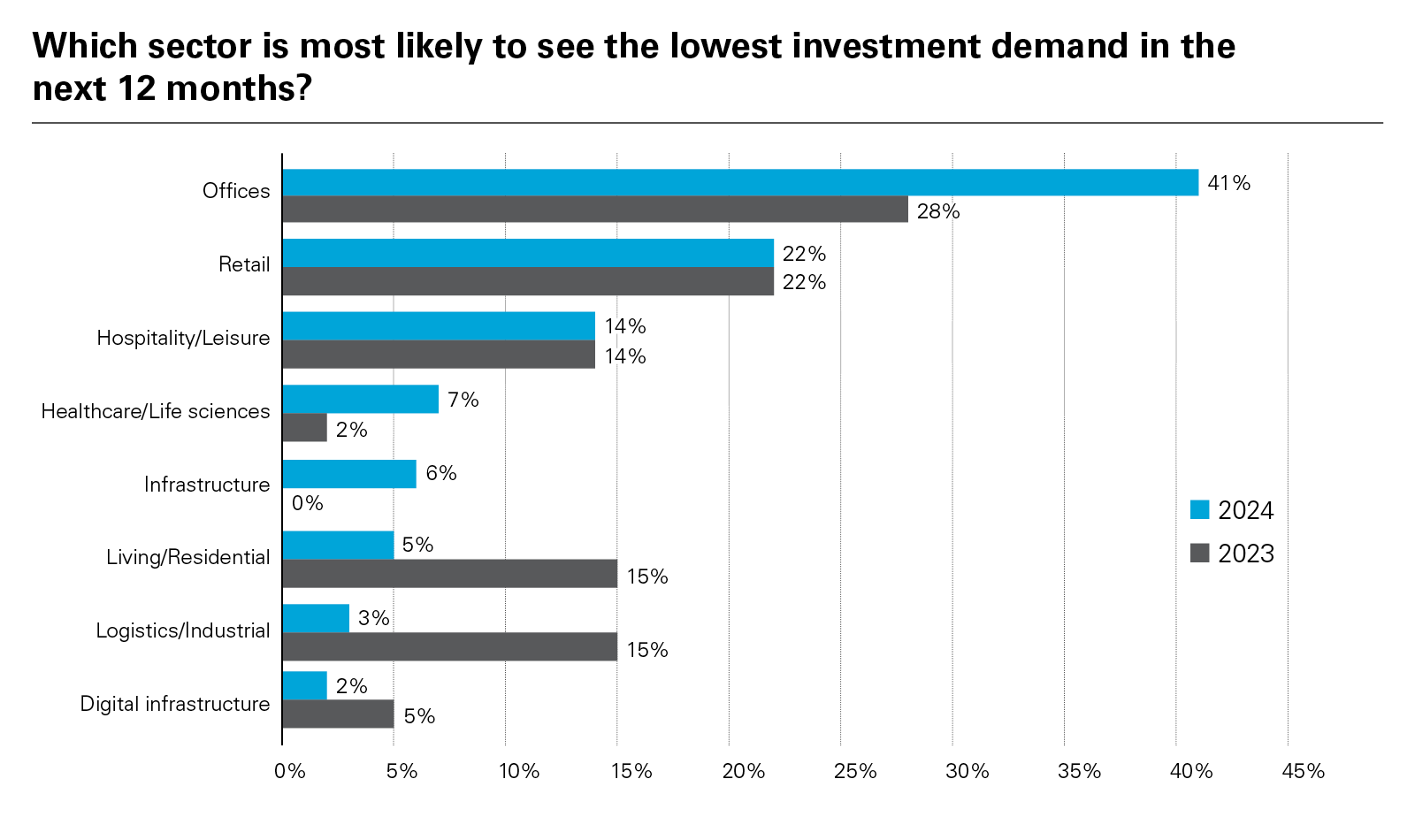

- Offices (41 percent); retail (22 percent) and hospitality/leisure (14 percent) have been selected as the sectors that will see the lowest investment demand during the next 12 months

The dislocation in real estate valuations during the past 12 months, coupled with tightening liquidity, a debt maturity wall and distress in Chinese real estate have put opportunistic fund strategies at the top of respondent rankings for 2024.

More than a third of respondents (36 percent) chose opportunistic fund strategies as the most attractive going into 2024, with the adjacent special situations category also gaining momentum, up at 8 percent from 0 percent last year.

View full image: Fund-raising strategies for new real estate-focused funds (PDF)

View full image: Fund-raising strategies for new real estate-focused funds (PDF)

The findings indicate that disruption caused by the rising interest rates as well as inflation to present an expanding pool of attractive investment opportunities in the months ahead, as a recalibration of real estate valuation and performance expectations washes through the industry.

A combination of factors are likely to be driven by this sentiment. With liquidity and financing costs still among the highest-ranked risks to real estate in 2024, despite interest rates flattening out, fund strategies that can unlock capital for real estate borrowers are taking center stage.

The largest real estate fund that closed in 2023, for example, was Blackstone Real Estate Partners X, which secured US$30.4 billion of capital commitments and will target opportunistic deals in rental, housing, hospitality and data centers.

Other strategies that fall under the opportunistic umbrella include real estate debt funds and real estate secondaries.

With PIMCO estimating that more than US$1.5 trillion of US real estate debt will mature by 2025, with US$650 billion and US$177 billion falling due in the same year in Europe and the Asia-Pacific respectively, real estate debt funds will be ideally placed to inject liquidity into companies with limited headroom in their capital structures.

Other strategies offering real estate companies and investors with liquidity have also gathered momentum, with Ares Management and Blackstone both closing real estate secondaries funds in December 2023, pushing real estate secondaries' share of overall real estate fundraising to 6 percent in 2023 from 0 percent in 2022, according to PERE figures.

"With the focus on inflation and interest rates, the liquidity challenges in the banking sector have been underappreciated," a real estate investment head said in a post-survey interview. "Remember that 2023 saw the second, third and fourth-biggest bank failures in history, and that by 2028, US$28 trillion of real estate debt will mature. Banks are also under regulatory pressure to down-weight real estate debt exposure, which has more than doubled from 2016/2017 levels. Refinancing is going to become more and more challenging.

A Europe-based logistics expert adds: "Debt maturities will drive significant market bifurcation in real estate. A strong player in a resilient sub-sector should not face any difficulties when refinancing. Lender support is still there for quality credits. Weak, highly leveraged players in underperforming subsectors will find it very difficult as maturities come into view."

Opportunistic funds could also take advantage of the secular shifts in real estate usage, where there have been big shifts in the aftermath of pandemic lockdowns.

Offices underperform, but digital infrastructure red hot

Lockdowns have had a significant impact on offices in particular, with employees continuing to work remotely even after restrictions were lifted, reducing demand for office space.

The survey findings rank offices as the sector that will see the lowest demand in 2024, with 41 percent of respondents bearish on offices—up from 28 percent in 2023. Retail ranked as the next sector to see the lowest investment demand (22 percent), with the long-term shift to online shopping continuing to eat into retail rents and valuations. Hospitality and leisure ranked third at 14 percent.

View full image: Which sector is most likely to see the lowest investment demand in the next 12 months? (PDF)

View full image: Which sector is most likely to see the lowest investment demand in the next 12 months? (PDF)

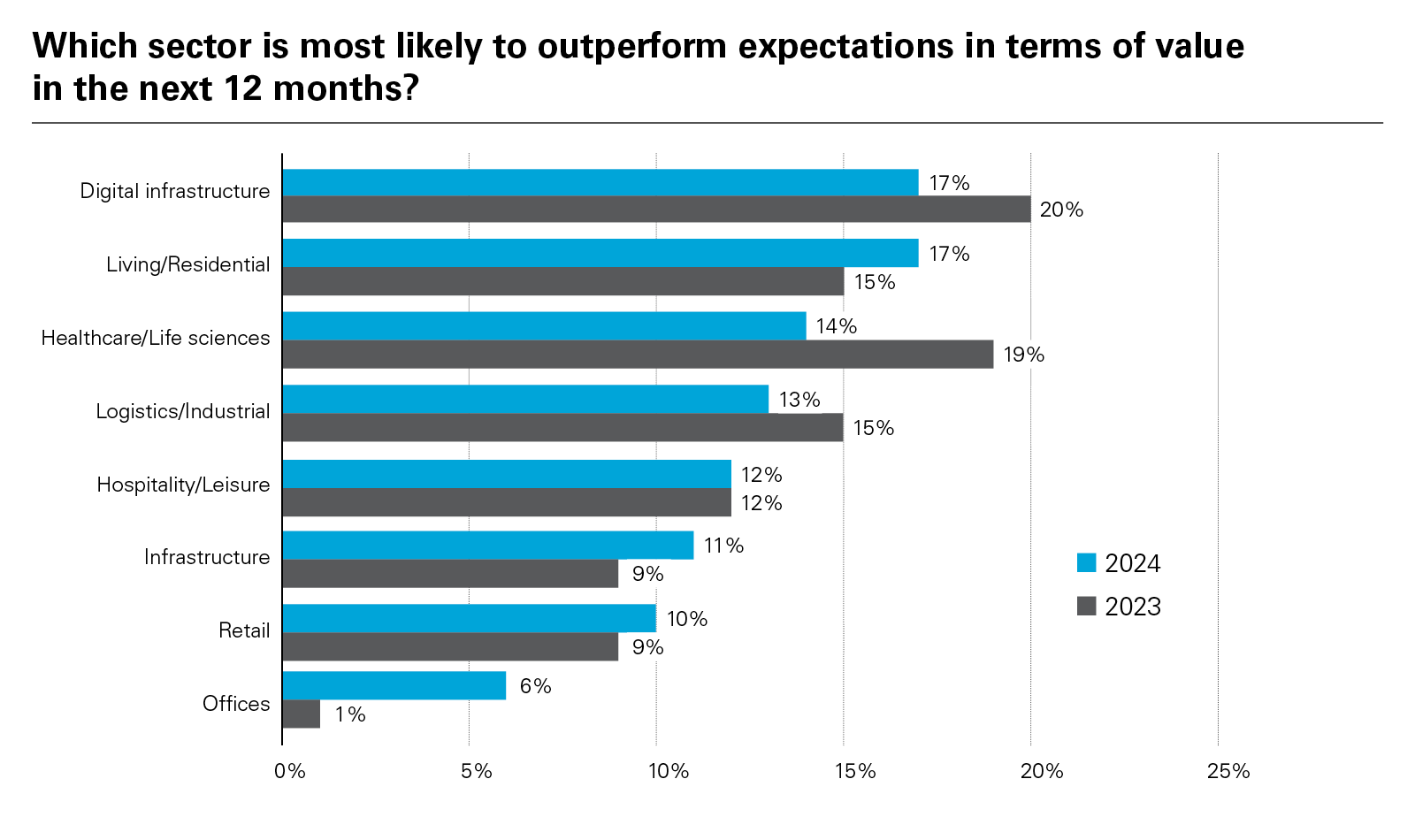

Respondents do, however, see potential for valuation outperformance in the digital infrastructure (17 percent), living/residential (17 percent) and healthcare/life sciences areas. In our previous survey, these sectors also ranked as the three most attractive areas for investment.

View full image: Which sector is most likely to outperform expectations in terms of value in the next 12 months? (PDF)

View full image: Which sector is most likely to outperform expectations in terms of value in the next 12 months? (PDF)

Demand for digital infrastructure continues to surge, as businesses and consumers require ever-larger amounts of data for work, shopping and entertainment. The rapid growth in Generative AI and data analytics is forecast to increase data demand even further (research consultancy Tirias Research estimates that Generative AI growth could see digital workloads increase by up to 50x by 2028).

The solid, long-term growth drivers underlying digital infrastructure and data centers have investors and dealmakers maintaining investment levels into the space despite wider market dislocation, with Mergermarket figures showing data center M&A holding steady in 2023 even as overall M&A markets saw double-digit declines in activity levels.

The residential/living sector has also held up well, despite rising interest rates and mortgage costs. Urbanization and the rising costs of home ownership are long-term drivers that will support residential asset valuations, according to Pimco, while in the student housing space, record numbers of students enrolled in tertiary education are pushing up demand for purpose-built student accommodations, according to the CBRE.

The optimism reflected in the survey around healthcare/life sciences is underpinned by strong underlying growth in life sciences and biotech, and an expansion in lab availability through the course of 2024, according to JLL research.

Demand for lab space is particularly strong in so-called "Tier 1" locations, where new commercial lab space is expanding and rental rates are showing resilient growth.

Opportunities, however, are emerging for investors with the risk appetite to take contrarian positions. European office space is one area that some investors see as oversold. European office vacancy rates are still tight, and more restrictive planning rules in Europe have prevented office overbuild.

Retail and shopping centers that have weathered the past ten years and are still performing, meanwhile, are likely to be robust assets that present attractive pricing dynamics.

Section 3: Operations, ESG and technology

Balancing act: Liquidity, tech-enablement and ESG place myriad demands on operators

Key Findings

- Availability and cost of financing (23 percent) ranks as the main operational risk for 2024, followed by construction costs (19 percent) and liquidity (17 percent)

- Political instability is the main socio-political risk (39 percent), with fall-out from political sanctions (14 percent) also prominent

- As the focus on political instability intensifies, environmental issues have ranked lower than in the previous survey (13 percent in 2024 vs 22 percent in 2023), but there has been progress when it comes to meeting investor-driven ESG requirements

- AI is emerging as an increasingly important technology for real estate operations, rising from 11 percent in 2023 to 26 percent in 2024

The survey findings highlight the multiple demands facing real estate operators, who are having to juggle ongoing liquidity and financing challenges with ESG implementation, digitalization programs and socio-political uncertainty.

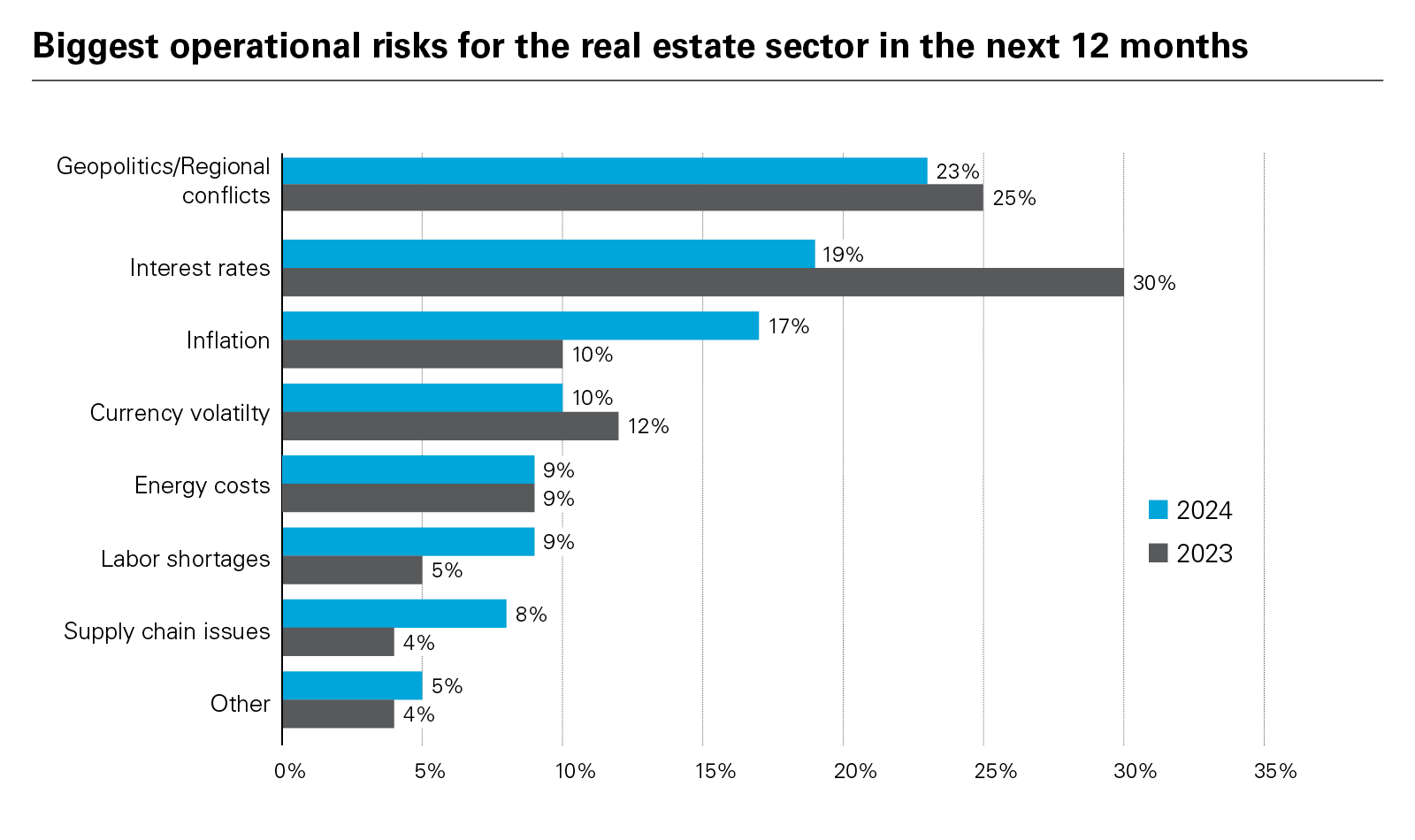

Respondents cited availability and cost of financing (23 percent) ranks as the main operational risk facing the industry in 2024, while construction costs (19 percent) and liquidity (17 percent) are seen as the other operational pressure points.

View full image: Biggest operational risks for the real estate sector in the next 12 months (PDF)

View full image: Biggest operational risks for the real estate sector in the next 12 months (PDF)

The focus on financing and liquidity underscores that even if interest rates flatten out in 2024, financing costs will remain materially above the ultra-low rates available to borrowers in 2021.

This is a significant operational challenge for real estate groups, as there is an estimated US$2 trillion of commercial real estate debt maturing by 2027 that will have to be refinanced at significantly higher costs, according to Capital Economics.

The lingering effects of inflation, meanwhile, remain on the minds of operators, with construction costs and resource availability the second-most pressing operational risk, chosen by 19 percent of respondents. This is, however, lower than the 30 prrcent figure recorded in last year's survey, suggesting that inflationary pressures and supply chains are stabilizing.

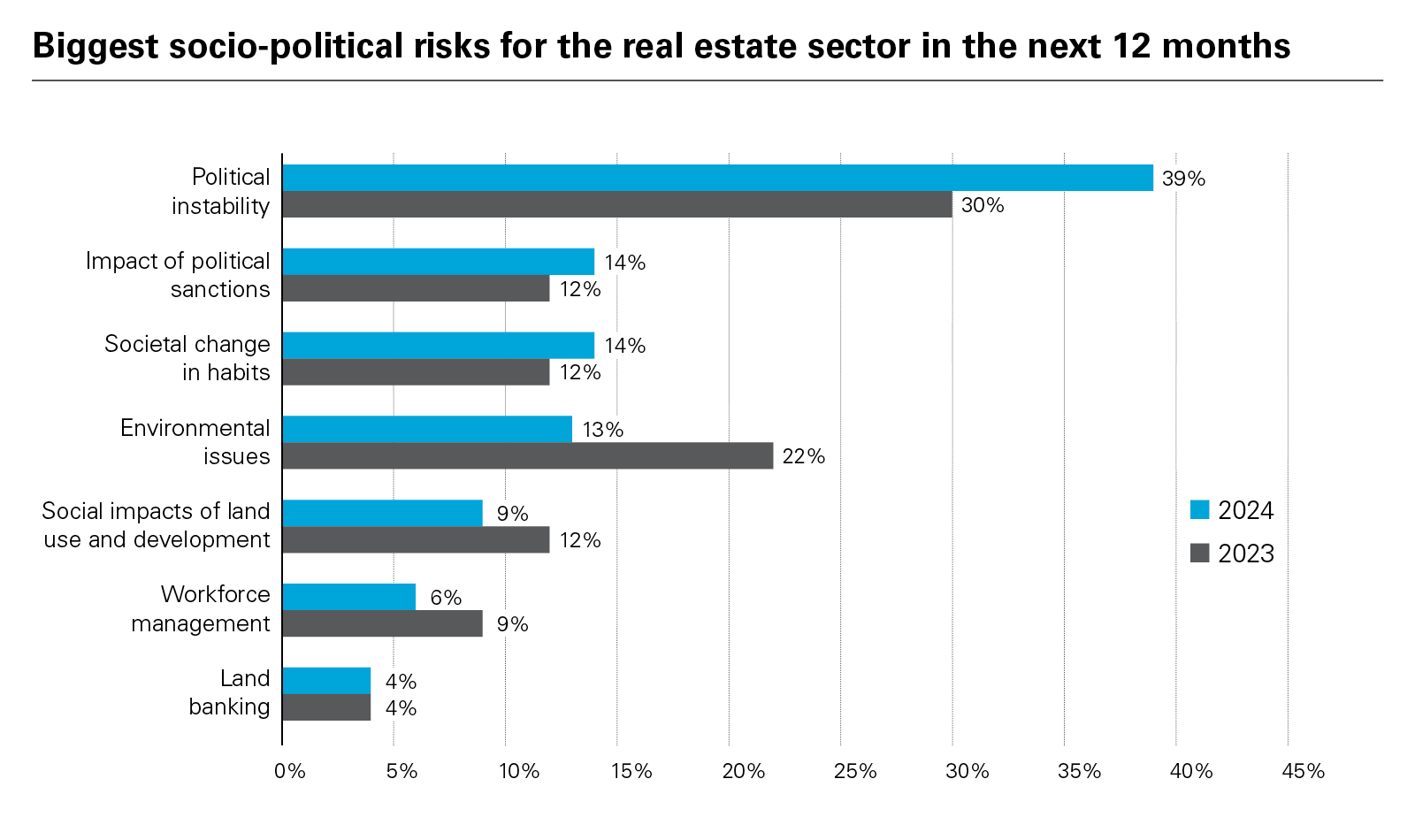

On the socio-political front, political instability ranks as the main socio-political risk, chosen by 39 percent of respondents. This is way ahead of the sanction regimes—the next biggest socio-political risk at 14 percent—and ahead of the 30 percent figure recorded in last year's survey.

View full image: Biggest socio-political risks for the real estate sector in the next 12 months (PDF)

View full image: Biggest socio-political risks for the real estate sector in the next 12 months (PDF)

With the US, UK and India among the major global economies going to the polls in 2024, real estate stakeholders are particularly attuned to political risk and changes in administrations and policy.

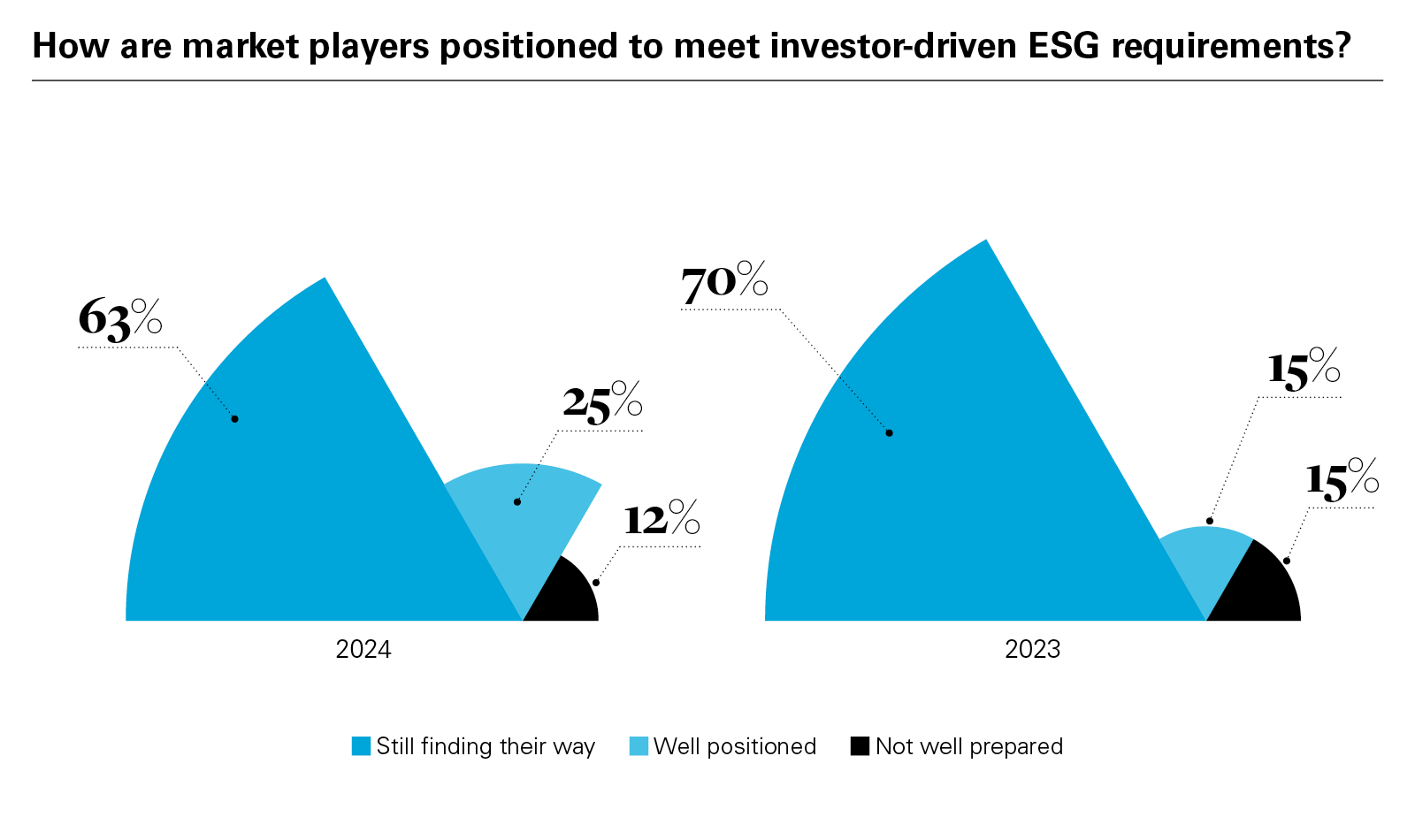

Interestingly, environmental issues have slipped down the risk agenda, from 22 percent of respondents last year to 13 percent in 2024, even though there appears to be more progress on meeting investor-driven ESG requirements. Last year, 70 percent of respondents said market players were still finding their way in this area, with 15 percent saying the industry was poorly prepared, and 15 percent saying it was well positioned.

This year, by contrast, a quarter of respondents said market players were well positioned to meet investor-driven ESG requirements, with 63 percent saying market players were still finding their way, and only 12 percent saying the market was not well prepared.

View full image: How are market players positioned to meet investor-driven ESG requirements? (PDF)

View full image: How are market players positioned to meet investor-driven ESG requirements? (PDF)

The immediate risks of liquidity shortages and political uncertainty may have pushed environmental risk down the agenda for the short term, but the fact that respondents point to ongoing progress on ESG compliance does suggest that ESG is now firmly embedded into real estate operations.

In a similar vein, digital integration has also become an integral part of real estate operations. Some 93 percent of respondents said technology and digital integration had become important or very important in future-proofing real estate operations, up from 86 percent last year.

There has, however, been a shift in what technologies real estate business are looking to implement.

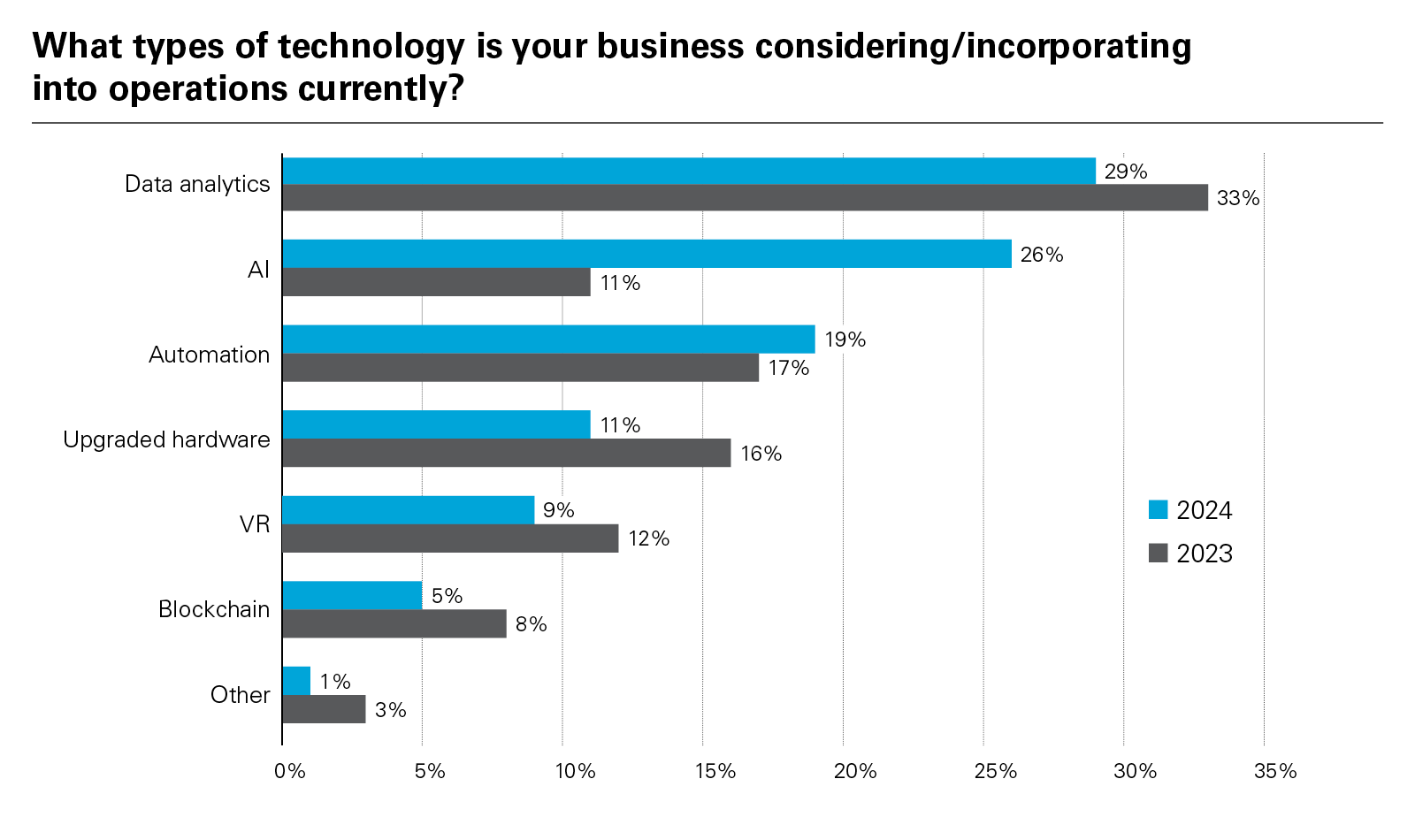

The findings have registered a big uptick in the focus on artificial intelligence tools. In 2023, only 11 percent chose AI as the main technology that companies were considering for implementation into operations. This has more than doubled to 26 percent in 2024, with only data analytics (29 percent) chosen by more respondents.

View full image: What types of technology is your business considering/incorporating into operations currently? (PDF)

View full image: What types of technology is your business considering/incorporating into operations currently? (PDF)

The practical implementation of AI tools in real estate may still be nascent, but the potential to drive value for real estate is clear. According to McKinsey, Generative AI could unlock between US$110 billion and US$180 billion for the real estate industry. The potential applications of AI in real estate are vast, ranging from processing leasing documentation, managing tenant inquiries and handling maintenance requests to facilitating virtual site tours or developing pipelines for real estate investors.

Pragmatic optimism

The disruptive impact of AI on the real estate industry will be one of the myriad complexities that real estate professionals have to continue navigating in 2024, with geopolitical risk, refinancing walls and ESG transition just some of the other major themes that will test investors and operators in the months ahead.

For all these ongoing challenges, however, there is a sense of cautious optimism building across real estate as interest rates peak, consensus forms on valuations and visibility on future performance improves.

Real estate professionals are not getting carried away, but after a period of stasis, M&A and fundraising are finally back on the agenda.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2024 White & Case LLP