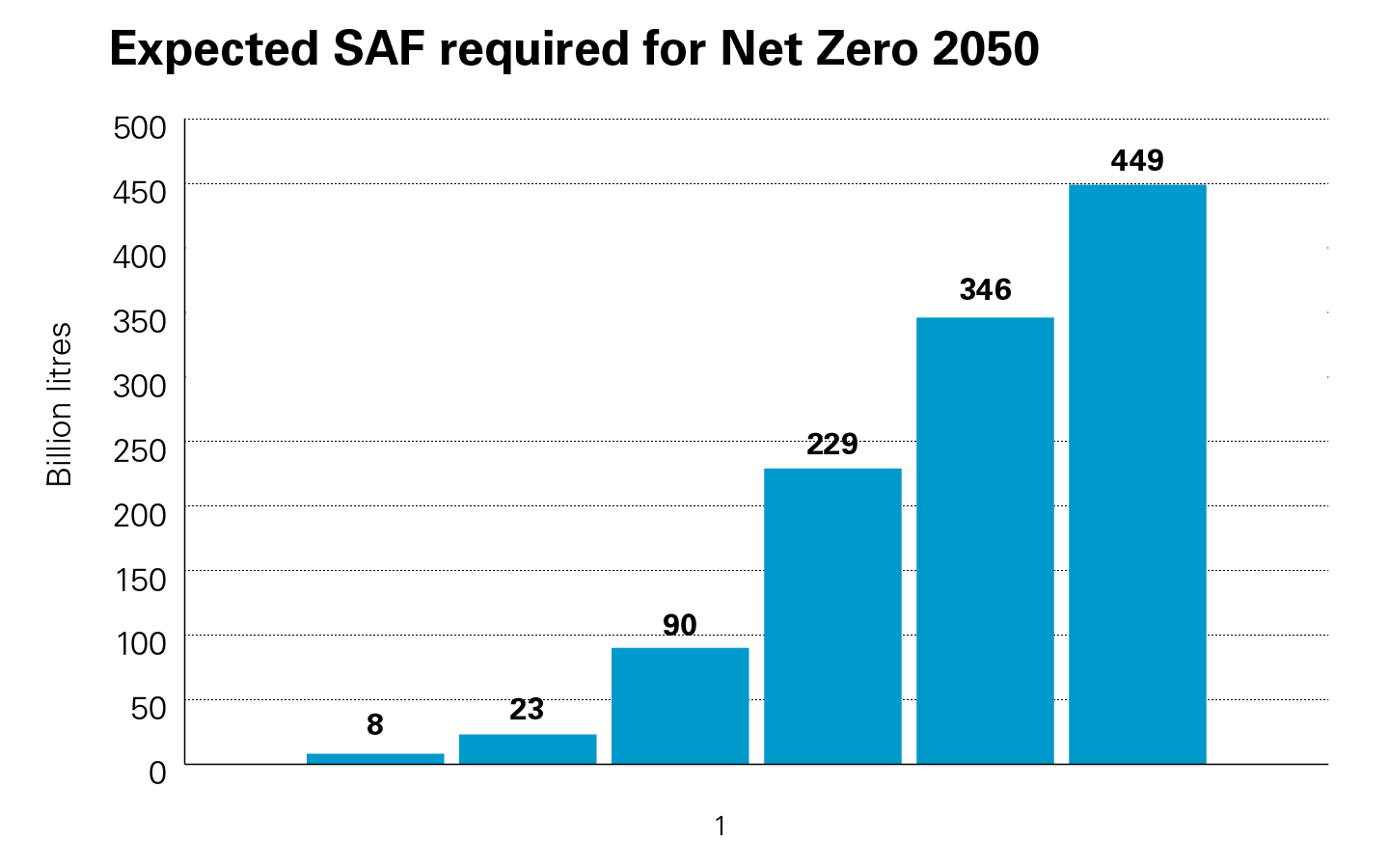

During the last several years, airlines have announced aggressive ESG targets. A significant component of many of these targets is the need for airlines to source more sustainable airline fuel and become less reliant on traditional jet fuel. As can be seen from the graph below, the supply of expected sustainable airline fuel that would be needed to achieve net zero by 2050 would require a significant increase, which represents a compelling opportunity for developers and financiers.

View full image: Expected SAF required for Net Zero 2050 (PDF)

View full image: Expected SAF required for Net Zero 2050 (PDF)

Setting targets has been the easier part of a complex equation: large quantities of sustainable airline fuel at reasonable prices is needed, yet sustainable airline fuel is in short supply.

In this article, we will highlight why sustainable airline fuel is of growing importance, and we will explore key considerations that industry participants and financiers will need to tackle in various stages (from production through commercial viability) and from various viewpoints (namely, that of airline operators and sustainable airline fuel providers).

What is SAF?

Sustainable airline fuel (SAF) is airline fuel made from sustainable resources rather than petroleum. It is a "drop-in fuel" in that it must be blended with fossil (petroleum-based) jet fuel (FJF) but without the need for new post-production infrastructure or changes in equipment—in most cases, up to a maximum of 50 percent of the "dropped-in" fuel can be SAF. Theoretically, any feedstock-technology combination can produce SAF, provided it meets technical specifications and the relevant sustainability criteria. Currently, nine drop-in alternative jet fuels are certified and approved for use in commercial aviation,2 with the bulk of activity occurring in respect of SAF production from biomass, animal fats, oils and greases and alcohol (i.e., ethanol).

Why SAF?

"Sustainable aviation fuels represent the most meaningful solution currently available to reduce climate impact for the "hard-to-decarbonize" aviation industry" - Sara Bogdan, Head of Sustainability and ESG for JetBlue.

In 2021, global carbon emissions from aviation made up 2–3 percent of all CO2 emissions, and the aviation industry accounted for 3.5 percent of total man-made global warming.3 Notably, US aircraft emissions alone contributed roughly 24 percent of all such global aircraft CO2 emissions, and 9-–2 percent of all US transportation carbon emissions. Failing any new policy development, global aircraft CO2 emissions are forecast to possibly triple by 2050 due to increased growth of passenger airline travel and air freight.4

While aircraft CO2 emissions will continue to increase, governments and a number of airlines and other organizations around the world have also set targets to reduce aviation emissions. The Biden administration in the US has targeted a 20 percent reduction in aviation emissions by 2030 and is seeking to achieve net-zero greenhouse gas emissions from the US aviation sector by 2050.5 To achieve such reductions, the Biden administration has called for Congress to pass legislation with tax incentives for low carbon jet fuel and announced a government goal to supply 3 billion gallons of SAF per year by 2030.6 However, the aviation industry is generally viewed as difficult to decarbonize. Compared to the power or road transport sectors, which can utilize alternative technologies such as nuclear, solar and wind power stations and electric cars, no such solution for the aviation industry yet exists. Hydrogen fuel cell-powered aircraft or electric airlines may yet prove viable, but such technology, on the scale required to make an impact on emissions, is generally viewed as too far off for the time being.

Therefore, given that aircraft will not be able to be powered by anything but liquid fuels in the near- and mid-term, airlines will rely heavily on SAF to help reduce carbon emissions. Growing, sourcing and producing SAF also has the following benefits: 7

- Farms. growing biomass for the production of SAF, can boost revenues for farmers during off-seasons while achieving nutrient loss reduction and soil quality improvement;

- Environment. Growing biomass crops can control erosion, improve water quality and quantity, increase biodiversity and improve carbon storage levels in soil, leading to benefits at the farm and country level;

- Performance. Many SAFs burn cleaner in aircraft engines because they contain fewer aromatic compounds, which leads to lower local emissions near airports during takeoffs and landings. Having fewer aromatic compounds also helps minimize an airplane's vapor trail, thereby further decreasing aviation's climate impact; and

- Jobs. Expanding the production of SAF can help create and secure employment opportunities in the production of biomass itself, refinery construction, production infrastructure manufacturing and aviation through increased flight activity.

However, not all sources of SAF are equal and the production of some SAF can cause significant environmental problems. National policies that generate the required economic incentives are paired with sustainability criteria to ensure production of SAF that is actually beneficial for the climate.

What are the current sustainability criteria for SAF?

During the 2021 UN Climate Change Conference in Glasgow, the United Nation's civil aviation body, the International Civil Aviation Organization (ICAO), adopted an expanded set of sustainability criteria for SAF.8 Noting that some alternative fuels can actually make environmental problems worse and even increase emissions compared to fossil jet fuels, the sustainability criteria ensure the SAF that airlines will use in international flights is eligible for ICAO's emissions reduction program—the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), a global, market-based measure designed to offset international aviation CO2 emissions. With its in-built monitoring, reporting and third-party verification system, CORSIA gives producers of SAF certainty in making investments in sustainability.

For SAF to be eligible under CORSIA, it must adhere to the following criteria: 9

| Theme | Criteria |

|---|---|

| 1. Greenhouse Gases (GHG) | 1.1 Reduction of net GHG emissions of at least ten percent compared to the baseline life-cycle emissions values for aviation fuel on a life-cycle basis. |

| 2. Carbon Stock |

2.1 No feedstock production from biomass obtained from land converted after January 1, 2008, that was primary forest, wetland or peat land and/or contributors to degradation of the carbon stock in primary forests, wetlands or peat lands as these lands all have high carbon stocks. 2.2 Calculation of direct land use charge (DLUC) emissions in the event of land use conversion after January 1, 2008 (as defined, based on the Intergovernmental Panel on Climate Change land categories). Note that if DLUC greenhouse gas emissions exceed the default induced land use change (ILUC) value, the DLUC value will replace the default ILUC value. |

| 3. Water |

3.1 Implementation of operational practices to maintain or enhance water quality. 3.2 Implementation of operational practices to use water efficiently and avoid the depletion of surface or groundwater resources beyond replenishment capacities. |

| 4. Soil | 4.1 Implementation of agricultural and forestry best management practices for feedstock production or residue collection to maintain and/or enhance soil health (including physical, chemical and biological conditions). |

| 5. Air | 5.1 Limiting of air pollution emissions to minimize negative effects on air quality. |

| 6. Conservation |

6.1 No feedstock production from biomass obtained from areas that, due to their biodiversity, conservation value or ecosystems services, are protected by the state having jurisdiction over that area, unless evidence is provided that shows the activity does not interfere with the protection purposes. 6.2 Selection of low invasive-risk feedstock for cultivation and adoption of appropriate controls—intention: prevent the uncontrolled spread of cultivated non-native species and modified microorganisms. 6.3 Implementation of operational practices to avoid adverse effects on areas that, due to their biodiversity, conservation value or ecosystem services, are protected by the state having jurisdiction over that area. |

| 7. Waste and Chemicals |

7.1 Implementation of operational practices to ensure waste arising from production processes, as well as chemicals used are stored, handled and disposed of responsibly. 7.2 Implementation of responsible and science-based operational practices to limit or reduce pesticide use. |

| 8. Human and Labor Rights | 8.1 Production that respects human and labor rights. |

| 9. Land Use Rights and Land Use | 9.1 Production that respects existing land rights and land use rights (including formal and informal indigenous people's rights). |

| 10. Water Use Rights | 10.1 Production that respects existing water use rights of local and indigenous communities. |

| 11. Local and Social Development | 11.1 Production, in regions of poverty, which strives to improve the socioeconomic conditions of communities affected by the production operations. |

| 12. Food Security | 12.1 Production, in food insecure regions, which strives to enhance the local food security of directly affected stakeholders. |

At this time, CORSIA only applies to international flights between member states that have volunteered to take part. CORSIA does not apply to emissions from domestic flights within these member states as such emissions are administered by the United Nations Framework Convention on Climate Change and are covered by the Paris Agreement. As yet, there is no universal "sustainability criteria" for SAF in respect of offsetting CO2 emissions from aviation within the continental US.10 However, as part of the "SAF Grand Challenge," the US Department of Energy, the US Department of Transportation and the US Department of Agriculture, along with other US government agency partners, intend to develop a policy framework to enhance the sustainability of SAF through:

- Maximizing the environmental co-benefits of production;

- Demonstrating sustainable production systems;

- Developing low land-use change feedstock crops;

- Reducing the carbon intensity of SAF supply chains;

- Ensuring robust standards that guarantee environmental integrity through rigorous life-cycle analysis; and

- Enabling approvals of higher blend levels of SAF.11

Despite the above, the implementation of government policies in support of the production of SAF and the further development of sustainability criteria is not enough to achieve commercial viability in the fledgling SAF industry.

How do we get to commercial viability?

Current levels of sustainable feedstock (e.g., municipal waste, agricultural residues and cooking oil waste) are such that if all sustainable feedstock were dedicated to SAF production, annual production levels of 500 million tons of SAF could be achieved, which would be sufficient to meet the forecast jet fuel demand of all aviation by 2030.12 Scaling up SAF production to meet governmental net-zero ambitions, however, will depend on significant multi-stakeholder collaboration. One of the main challenges will be to develop appropriate commercial and financing avenues along with boosting incentives and implementing regulatory mechanisms.

Planning

Before getting the financing of a SAF production facility off the ground, a large amount of planning is required. Issues that will need to be dealt with before approaching financiers will include:

- Location. Given that SAF production facilities rely heavily on the factor inputs of biomass, proximity to sources of such biomass will be a big plus for investors;

- Revenue. Investors will want to see that the SAF production facility they are financing has a revenue stream that is certain and that forecasts of such revenues are accurate;

- Regulatory. Maximizing revenue from SAF production facilities will often depend on whether the end user (i.e., in most cases, the airline) is able to obtain maximum carbon trading offset credits, so the method of such SAF production will need to be accredited under any relevant sustainability criteria.

- Sponsors. Given the fledgling nature of the SAF industry, it is likely financiers will require that sponsor capital be injected unless they are satisfied as to the sponsor's credit standing or the sponsor has indicated it would be willing to give a bank guarantee or letter of credit as security for the SAF project.

Of particular importance to financiers is the certainty of the revenue stream—this is where having robust, long-term offtake agreements entered into with airlines or other market participants can play a key role in ensuring the commercial viability of a SAF project.

Offtake agreements

An offtake agreement is usually an agreement to purchase all or a substantial part of the output or product of a particular project. In the case of a SAF production facility, this would usually take the form of an airline agreeing to buy a certain amount of gallons of SAF over a certain period at an agreed fixed price (or semi-fixed price that varies depending on certain indices).

What should a good offtake arrangement achieve for both airline and sponsor/developer?

- Provide long-term guaranteed and stable cash flow to the sponsor/developer, allowing the sponsor/developer to "bank" the project.

- Noting current supply issues with airline fuel globally, provide a long-term, guaranteed and stable supply of aviation-grade fuel with producers closer to home.

- Allow both airline and sponsor/developer to better forecast the demand and supply of the product that is the subject of the offtake agreement so as to plan capital deployment.

- Assist with and sometimes provide for the establishment of a long-term strategic relationship by allowing for the airline to receive first offer rights to purchase significant volumes of SAF from the producer.

- Wholly or partially fix the price of SAF to be purchased under such offtake agreement.

- Allow airlines to wholly or partially implement their ESG objectives.

What SAF offtake agreements and financings have been agreed so far?

SAF offtake agreements are increasingly being negotiated and executed and SAF production facilities are continuing to be financed. We expect that as the demand for SAF grows, not only will more SAF offtake agreements be signed and more SAF production facilities be financed, but lenders will make commitments available at higher amounts in respect of such SAF projects. We also expect to see an increase in innovation by producers and offtakers to boost SAF supply, including efforts to produce "net-zero oil" through investment in direct air capture and other technologies for development of lower-carbon aviation fuels.13

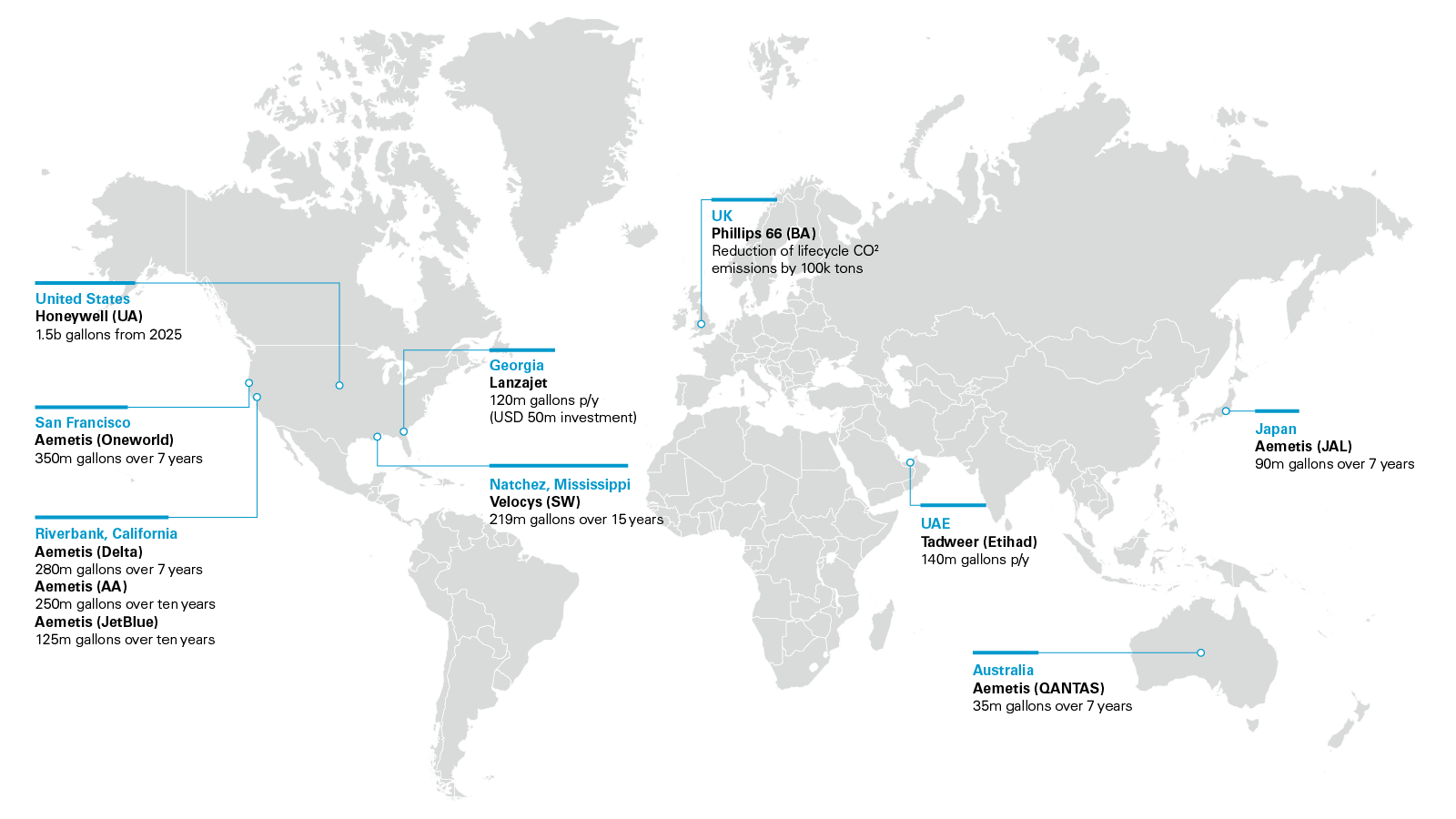

Set forth below are a few recent highlights of market activity globally that have been made available publicly in respect of executed SAF offtake agreements and related financings.

View full image: SAF map (PDF)

View full image: SAF map (PDF)

United States

| Date | Agreement | Parties | Plant | Technology | Capacity and/or Capital Raised | Environmental Claim |

|---|---|---|---|---|---|---|

| Apr. 26, 2022 | Offtake Agreement | JetBlue Aemetis | Aemetis Carbon Zero Plant – Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils, along with CO2 sequestration | 125m gallons of blended fuel over ten years from 2025 | Will provide significant environmental benefits, including a lower lifecycle carbon footprint and reduced contrails14 |

| Jan. 13, 2022 | Financing | LanzaJet Microsoft Climate Innovation Fund | Freedom Pines Fuels – Soperton, Georgia | World's first ATJ SAF production plant | 120m gallons p/y USD 50m investment | Will enable LanzaJet to bring lower-cost SAF and renewable diesel to the global market15 |

| Dec. 1, 2021 | Offtake Agreement | American Airlines Aemetis | Aemetis Carbon Zero Plant –Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils along with CO2 sequestration | 280m gallons of blended fuel over seven years from 2024 | Provides significant environmental benefits compared to petroleum jet fuel, including a lower life-cycle carbon footprint16 |

| Nov. 10, 2021 | Offtake Agreement | Southwest Airlines Velocys | Bayou Fuels Facility – Natchez, Mississippi | SAF from sustainable feedstock (forestry residues from plantation forests) and renewable power from a neighboring solar facility, as well as carbon capture | 219m pre-blended gallons over 15 years from 2026 | Avoidance of 6.5 million metric tons of CO2 over the term of the offtake agreement17 |

| Sept. 30, 2021 | Offtake Agreement | Delta Aemetis | Aemetis Carbon Zero Plant –Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils, along with CO2 sequestration | 250m gallons of blended fuel over ten years from 2024 | Helps Delta achieve its net-zero aviation goals, and supports Delta's customers to achieve their own sustainability goals18 |

| Sept. 10, 2021 | Offtake Agreement | United Airlines Honeywell Alder Fuels | N/A | Conversion of abundant biomass (e.g., forest and crop waste) into drop-in replacement crude | 1.5b gallons after commercialization in 2025 (expected) | Aims to completely replace the US' current fossil jet fuel consumption19 |

Global

| Date | Agreement | Parties | Plant | Technology | Capacity and/or Capital Raised | Environmental Claim |

|---|---|---|---|---|---|---|

| Mar. 15, 2022 | Offtake Agreement | Qantas Aemetis | Aemetis Carbon Zero Plant – Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils, along with CO2 sequestration | 35m gallons of blended fuel over seven years from 2025 | Significant environmental benefits, including a lower life-cycle carbon footprint and reduced contrails20 |

| Feb. 9, 2022 | Offtake Agreement | Japan Airlines Aemetis | Aemetis Carbon Zero Plant – Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils, along with CO2 sequestration | 90m gallons of blended fuel over seven years from 2025 | Builds on JAL's expanding effort for a future of net zero emissions by 205021 |

| Jan. 20, 2022 | Offtake Agreement (for operations at San Francisco International) | oneworld Aemetis | Aemetis Carbon Zero Plant – Riverbank, California | SAF from Zero carbon intensity electricity and negative carbon intensity hydrogen from waste wood and renewable oils, along with CO2 sequestration | 350m gallons of blended fuel over seven years from 2024 | Reduction of air pollution in local disadvantaged communities through reduction of orchard wood burning in fields22 |

| Dec. 2, 2021 | Offtake Agreement | British Airways Phillips 66 Limited | Phillips 66 Humber Refinery in North Lincolnshire | SAF processed from sustainable waste feedstock | N/A | Reduction of life-cycle CO2 emissions by almost 100,000 tons23 |

| Nov. 15, 2021 | Offtake Agreement | Etihad Airways Tadweer | First waste-to-SAF plant in the Middle East | SAF processed from municipal, commercial and industrial waste | 140m gallons of SAF p/y | Annual reduction of CO2 emissions of 1m tons24 |

Dealing with general industry pain points

Due to the current stage of the SAF market, financing the production of SAF can be challenging. While a typical limited recourse financing will need bankable offtake arrangements, feedstock and supply, an experienced developer and possibly government assistance by way of incentives, there are unique challenges that we expect to arise with regard to SAF that will need to be overcome in order to realize commercial viability:

- SAF currently sells for 2-6 times more than traditional jet fuel, which limits demand from airlines, and therefore affects the bankability of production facilities;

- There currently is limited availability of sustainable feedstock and a concurrent lack of funding research for the development of new feedstock feeding into SAF production;

- Currently, investing in SAF production is still a difficult proposition for lenders, which limits access to finance for SAF producers and continues to hamper efforts to boost supply levels;

- Financiers have capacity and resource issues so they prefer to invest in industries where developers can offer a "portfolio of ready projects" over industries in which developers can only offer investment opportunities on a project-by-project basis. Given the still-early stage of the SAF market, financing arrangers are therefore limited in their ability to structure and originate opportunities in SAF production that would help create a viable pipeline of portfolio-ready SAF projects; and

- With respect to the US market, demand for SAF is expected to increase and could consume an amount of several hundred million tons of biomass per year, which, as noted above, would be equivalent to the amount of all biomass currently available in the US.25

Legal hurdles

Specifically in the US, while the federal government continues to expand laws and policies to incentivize the use of SAF, there are several legal hurdles that, if overcome, would aid the commercialization of SAF. These include:

- Lack of clear, cohesive US federal policy in contrast to the European Union's Renewable Energy Directive and Emissions Trading System; and

- Piecemeal, opt-in, voluntary programs with varying incentives and mandates at the federal, state and regional levels—see, for instance, the Federal Renewable Fuel Standard Program, the California Low Carbon Fuel Standard, the Oregon Clean Fuels Program, the Washington Clean Fuels Program and Hawaii's SAF tax incentive program, to name a few.

Dealing with the above challenges will require the efforts of a large array of stakeholders in government, the aviation industry, finance and energy.

Outlook

Wide-scale adoption and production of SAF at reasonable prices will require wide ranging cooperation and alignment of interests. Industry insider and leader Sara Bogdan, Head of Sustainability and ESG for JetBlue has said to us that "to reach global net zero goals there needs to be aggressive and immediate action from many parties, including airlines, aircraft technology manufacturers, government, and the finance community to overcome the cost and supply challenges long plaguing the SAF market."

More and more governments are making bolder pledges with respect to the decarbonization of the aviation sector. Likewise, private sector aviation industry participants are continuing to set aggressive goals for themselves. However, the viable technology and market/commercial dynamics that will make this a reality are not where they should be. Producing and rolling out SAF is the short- to mid-term solution available now that can be commercially viable while making the decarbonization of the aviation sector a reality.

With government and regulatory support sure to fuel activity, the stage looks set for a dramatic increase in appetite for SAF and, as a result, of SAF production facilities. We are in regular dialogue with industry leaders with respect to SAF, and we expect the exponential growing demand for SAF will lead to rapid change and the continued re-direction of resources (financial and otherwise) into this ever-important industry.

1 https://www.iata.org/en/iata-repository/pressroom/fact-sheets/fact-sheet---alternative-fuels/#:~:text=We%20estimate%20that%20SAF%20could,in%20order%20to%20meet%20demand.

2 The aviation industry has developed the ASTM D4054 certification, a rigorous testing system that compares petroleum-derived to alternatively derived jet fuel to fully determine whether a fuel is "drop-in." The following table sets out the nine SAF alternative fuels that are currently ASTM D4054 certified:

| Approved SAF | Blend Ratio to FJF | Base Feedstock |

|---|---|---|

| Fischer-Tropsch (FT) Synthetic Paraffinic Kerosene (FT-SPK) | Max – 50% | Biomass (i.e., municipal solid waste, agricultural and forest wastes, and wood and energy crops) and non-renewables (coal and natural gas) |

| Hydroprocessed Esters and Fatty Acids Synthetic Paraffinic Kerosene (HEFA-SPK) | Max – 50% | Lipids from plant and animal fats, oils and greases (FOG) (i.e., fatty acids and fatty acid esters) |

| Hydroprocessed Fermented Sugars to Synthetic Isoparaffins | Max – 10% | Sugars |

| Fischer-Tropsch Synthetic Paraffinic Kerosene with Aromatics | Max – 50% | As with FT-SPK |

| Alcohol to Jet Synthetic Paraffinic Kerosene (ATJ) | Max – 50% | Individually, ethanol and isobutanol |

| Catalytic Hydrothermolysis Synthesized Kerosene | Max – 50% | As with HEFA-SPK |

| Hydroprocessed Hydrocarbons, Esters and Fatty Acids Synthetic Paraffinic Kerosene | Max – 10% | Bio-derived hydrocarbons, fatty acid esters, and free fatty acids—the only currently recognized source of bio-derived hydrocarbons is the tri-terpenes produced by the Botryococcus braunii species of algae |

| FOG Co-Processing | Max – 5% | FOG from petroleum refining |

| FT Co-Processing | Max – 5% | FT biocrude as an allowable feedstock for petroleum co-processing |

3 https://www.eesi.org/papers/view/fact-sheet-the-growth-in-greenhouse-gas-emissions-from-commercial-aviation.

4 https://www.eesi.org/papers/view/fact-sheet-the-growth-in-greenhouse-gas-emissions-from-commercial-aviation and https://www.c2es.org/content/reducing-carbon-dioxide-emissions-from-aircraft/.

5 https://www.reuters.com/business/cop/us-sets-goal-net-zero-aviation-emissions-by-2050-2021-11-09/.

6 https://www.reuters.com/business/energy/biden-renews-push-sustainable-aviation-fuel-tax-credit-2022-04-12/.

7 https://www.energy.gov/eere/bioenergy/sustainable-aviation-fuels.

8 https://www.edf.org/media/icao-council-approves-comprehensive-set-sustainability-criteria-sustainable-aviation-fuel.

9 https://www.icao.int/environmental-protection/CORSIA/Documents/ICAO%20document%2005%20-%20Sustainability%20Criteria%20-%20November%202021.pdf.

10 https://aviationbenefits.org/environmental-efficiency/climate-action/offsetting-emissions-corsia/corsia/corsia-explained/.

11 https://www.faa.gov/sites/faa.gov/files/2021-11/Aviation_Climate_Action_Plan.pdf.

12 https://www.weforum.org/press/2020/11/all-aircraft-could-fly-on-sustainable-fuel-by-2030-says-world-economic forumreport/#:~:text=Enough%20sustainable%20feedstock%20supplies%2C%20such,of%20all%20aviation%20by%202030.

13 https://www.oxy.com/news/news-releases/occidental-sk-trading-international-sign-first-agreement-for-net-zero-oil-created-from-captured-atmospheric-carbon-dioxide/.

14 https://www.globenewswire.com/news-release/2022/04/26/2429059/0/en/Aemetis-Signs-Agreement-with-JetBlue-to-Supply-125-Million-Gallons-of-Sustainable-Aviation-Fuel.html.

15 https://www.lanzajet.com/lanzajet-secures-industry-leading-innovative-financing-with-microsoft-climate-innovation-fund-to-construct-the-worlds-first-commercial-alcohol-to-jet-sustainable-fuel-plant/.

16 http://biomassmagazine.com/articles/18531/aemetis-signs-agreement-with-american-airlines-to-supply-saf.

17 https://www.velocys.com/2021/11/10/saf-offtake-with-southwest-airlines/.

18 https://www.reuters.com/business/aerospace-defense/delta-air-buy-sustainable-aviation-fuel-aemetis-over-1-bln-deal-2021-09-30/.

19 https://www.honeywell.com/us/en/press/2021/09/united-honeywell-invest-in-new-clean-tech-venture-from-alder-fuels-powering-biggest-sustainable-fuel-agreement-in-aviation-history.

20 https://www.aemetis.com/aemetis-signs-agreement-with-qantas-to-supply-35-million-gallons-of-sustainable-aviation-fuel/.

21 https://www.aemetis.com/aemetis-signs-agreement-with-japan-airlines-to-supply-90-million-gallons-of-sustainable-aviation-fuel/.

22 https://biofuels-news.com/news/oneworld-agrees-saf-deal-over-seven-years-beginning-in-2024/.

23 https://www.phillips66.com/newsroom/british-airways-phillips-66-limited-sign-sustainable-aviation-fuel-supply-agreement.

24 http://www.tradearabia.com/news/CONS_389709.html.

25 https://www.energy.gov/sites/prod/files/2020/09/f78/beto-sust-aviation-fuel-sep-2020.pdf.

Adam Conwell (White & Case, International Law Clerk, New York) contributed to the development of this publication.

White & Case means the international legal practice comprising White & Case LLP, a New York State registered limited liability partnership, White & Case LLP, a limited liability partnership incorporated under English law and all other affiliated partnerships, companies and entities.

This article is prepared for the general information of interested persons. It is not, and does not attempt to be, comprehensive in nature. Due to the general nature of its content, it should not be regarded as legal advice.

© 2022 White & Case LLP